- Bulk Chemicals

- India Precipitated Silica Market

India Precipitated Silica Market Size, Share, and Growth Forecast, 2026 - 2033

India Precipitated Silica Market by Application (Rubber, Agrochemicals, Food & Feed, Personal Care & Oral Care, Coatings, Inks & Paints), and Country Analysis for 2026 - 2033

India Precipitated Silica Market Size and Trends Analysis

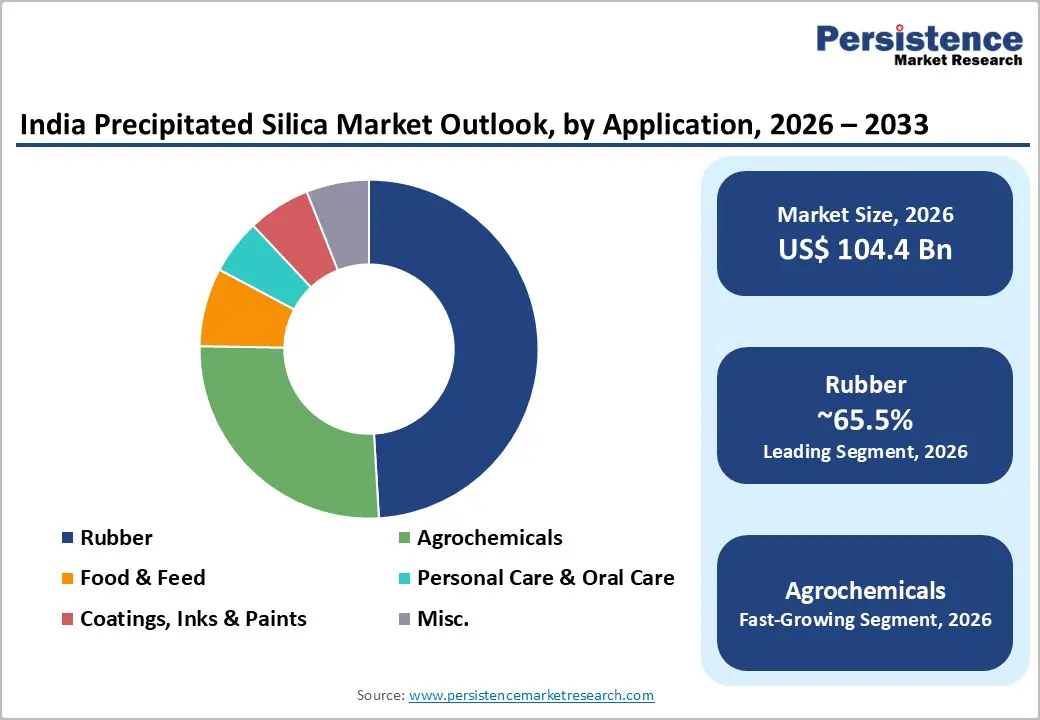

The India precipitated silica market size is likely to be valued at US$ 94.5 million in 2026 and is projected to reach US$ 210.1 million by 2033, growing at a CAGR of 10.5% between 2026 and 2033.

This trajectory reflects structural demand from India's automotive and tyre industries, large-scale agrochemical sector, and diversifying end-use segments, including oral care and animal feed. The market recorded a strong growth anchored by the rapid adoption of highly dispersible silica (HDS) in fuel-efficient tyre manufacturing. Regulatory mandates for fuel efficiency, government infrastructure programs driving vehicle demand, and deepening agrochemical penetration in India's agricultural sector collectively underpin this sustained demand trajectory.

Key Industry Highlights:

- Leading Application Segment: Rubber leads the India Precipitated Silica Market with approximately 65.5% market share in 2026, driven by strong tyre production growth, BEE rolling resistance norms, and rising SUV penetration, increasing silica loading per tyre.

- Fastest-Growing Application Segment: Agrochemicals is the fastest-growing segment, supported by rising pesticide demand, new molecule registrations, and export volume recovery.

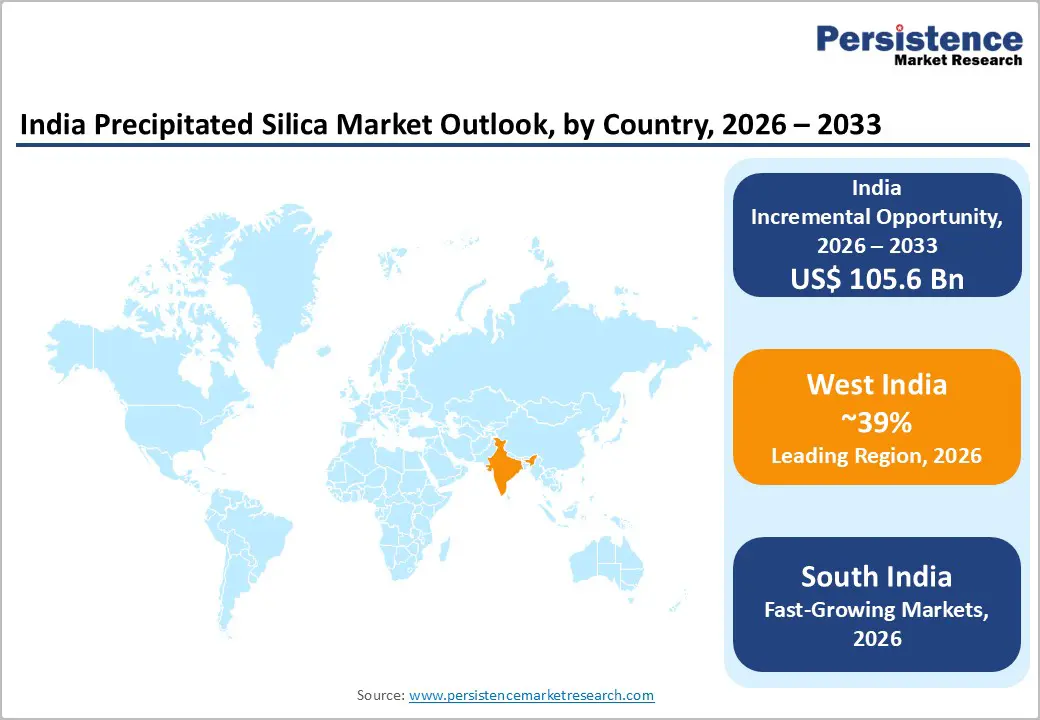

- Leading Regional Market: Southern India dominates the market, anchored by Tamil Nadu’s tyre manufacturing ecosystem and large-scale HDS capacity expansion at Cuddalore, strengthening its position as the country’s primary high-performance silica hub.

- Fastest-Growing End-Use Opportunity: Animal feed and premix applications are emerging as the fastest-growing non-tyre segment, supported by rising protein consumption, 8.5% annual poultry production growth, and increasing demand for high-absorption carrier silica

- Capacity Expansion Catalyst: Major investments by Tata Chemicals Limited (INR 775 crore for 50 ktpa expansion) and AksharChem India Limited (Dahej capacity expansion to 18,000 TPA) are strengthening domestic supply and reducing import dependence.

| India Market Attributes | Key Insights |

|---|---|

| India Precipitated Silica Market Size (2026E) | US$ 104.4 Mn |

| Market Value Forecast (2033F) | US$ 210.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 10.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.6% |

Market Dynamics

Growth Drivers

Automotive Tyre Sector Mandates Shift Demand Toward High-Performance Silica Grades

India's tyre and automotive industries are the foundational pillars of demand in the India Precipitated Silica Market, where precipitated silica serves as an irreplaceable reinforcing filler that enhances wet grip, rolling resistance, tread wear, and fuel efficiency.

According to the Automotive Tyre Manufacturers Association (ATMA), India has over 41 tyre-producing companies operating across more than 62 manufacturing plants. Tyre exports from India surged 50 % in FY22 and continued with approximately 15% growth in FY23, reflecting India's strengthening position as a global tyre supply hub. India's Ministry of Road Transport has progressively adopted Bureau of Energy Efficiency (BEE) labelling norms requiring passenger car tyres to meet rolling resistance limits, directly mandating higher HDS content in tread compounds. Import restrictions reclassified several tyre categories from "Free" to "Restricted" in 2020, reducing foreign inflows by more than 80% and channelling silica demand firmly toward domestic supply chains.

Vehicle production data from the Society of Indian Automobile Manufacturers (SIAM) confirms that India crossed 5.8 million passenger vehicles produced in FY24, with SUV sales at an all-time high, increasing tyre dimensions and the corresponding silica dosage per unit. These interlinked factors create a multi-year volume corridor in the India Precipitated Silica Market with clear pricing latitude for HDS grades.

Agrochemical Sector Adopts Precipitated Silica as a Functional Carrier and Flow Aid

Precipitated silica performs critical technical functions in agrochemical formulations, acting as a free-flow agent, carrier for active ingredients, and anti-caking additive in wettable powders, granules, and soluble concentrate formulations. In India's highly competitive and weather-sensitive agrochemical market, where carrier performance directly affects field efficacy and shelf stability, the transition to higher-grade silica is accelerating.

NITI Aayog projects pesticide demand to reach 79,233 tonnes and fertiliser consumption to reach 339 lakh tonnes by 2030. The Ministry of Chemicals and Fertilizers approved registration of 11 new agrochemical molecules, including fungicides and herbicides, in March 2024, supporting product launches that require high-purity silica carriers.

Indian agrochemical exports to the US and Brazil witnessed healthy volume momentum in H1 FY2025 as global channel inventories normalised following the FY2024 destocking cycle. For the Indian Precipitated Silica Market, this broad agrochemical expansion signals sustained demand from a segment distinct from rubber, providing meaningful diversification to overall demand.

Government-Backed Rural Housing and Infrastructure Programs Sustain Downstream Demand

Large-scale government construction and infrastructure initiatives sustain vehicle ownership, agricultural mechanisation, and consumption of coatings and sealants, all of which indirectly anchor precipitated silica demand across multiple application segments. India's Union Budget for FY 2024 to 2025 allocated capital expenditure of USD 133 Billion, equivalent to 3.4% of GDP, fueling nationwide infrastructure development.

The PMAY-U program sanctioned 1.18 crore houses with 86.6 lakh already completed, adding to the residential construction base that consumes coatings and sealant-grade silica. India's real estate market is projected to reach USD 5.8 Trillion by 2047, contributing 15.5% of GDP. The warehousing sector is expected to see demand for 159 million sq ft of logistics space by 2047 at a 4 % CAGR, supporting industrial floor coatings that use silica as a flatting agent. By underpinning the broader industrial and construction ecosystem, these programs provide a sustained policy floor for the Indian Precipitated Silica Market beyond its core rubber and agrochemical segments.

Market Restraining Factors

Feedstock Price Volatility and Sodium Silicate Input Costs Constrain Margin Stability

Precipitated silica is produced primarily through the reaction of sodium silicate with sulfuric acid, making production costs directly exposed to sulfuric acid price cycles and sodium silicate availability. Both inputs are derived from commodity chemical chains subject to global pricing volatility. When sulfuric acid prices spike, as experienced during global supply disruptions in 2022 and 2024, domestic producers face margin compression unless long-term procurement contracts are secured. Smaller producers lacking captive raw material sourcing or long-term agreements with sulfuric acid suppliers face disproportionately higher input costs, limiting their ability to compete on pricing with larger integrated players in the India Precipitated Silica Market.

Competition from Chinese Imports and Global Diversion Pressures Domestic Pricing

The Indian agrochemical and speciality chemicals sectors remain exposed to competitive pricing from Chinese manufacturers who redirect export volumes when trade flows are disrupted elsewhere. The US imposed an additional approximately 54% tariff on Chinese pesticide imports, incentivising Chinese producers to divert agrochemical and speciality chemical volumes to markets in Latin America, Asia, and Africa, increasing competitive pressure on Indian silica-intensive formulation exports. Although India's tyre sector is partially shielded by the 2020 import restrictions, formulation-grade and food-grade silica segments remain vulnerable to lower-cost imports. This competitive dynamic can suppress domestic silica pricing and compress realisation per tonne in segments beyond rubber tyres.

Key Market Opportunities

Oral Care and Personal Care Premiumization Opens High-Value Specialty Silica Demand

Precipitated silica serves as both a gentle abrasive and rheology modifier in toothpaste formulations, and its demand in India's personal care and oral care segment is being shaped by two converging trends: premiumization among urban consumers and reformulation toward natural, low-VOC oral care products. BIS Standard IS 6356:2001 formally recognises precipitated silica among accepted polishing agents for toothpaste, providing regulatory certainty for formulators. According to India's Ministry of Chemicals and Fertilisers, demand for speciality chemicals, including precipitated silica, has recorded approximately 10.2 % annual expansion since 2021

Colgate-Palmolive India has publicly committed to tripling revenues from premium oral care segments, where margins are 5 to 8% points higher, mandating specialised silica grades that deliver enhanced whitening and mouth-feel. Despite this, rural oral hygiene penetration remains low, with only 20% of urban consumers brushing twice daily, indicating structural volume upside as awareness campaigns and income growth reach Tier 2 and Tier 3 markets. For market participants in the India Precipitated Silica Market, this segment represents an actionable, high-margin growth channel distinct from commodity tyre silica.

Bio-Based and Green Silica Production from Rice Husk Ash Presents a Differentiated Supply Opportunity

India's status as the world's second-largest rice producer generates vast quantities of rice husk ash (RHA), a renewable agricultural byproduct that contains 85 to 95% amorphous silica by weight. Producing precipitated silica from RHA using an alkali-acid precipitation process is energy-efficient, avoids the high-temperature fusion used in conventional sand-based routes, and generates calcium carbonate as a marketable co-product, lowering effective production costs by approximately 20% per kilogram versus conventional routes.

Blue Ocean Biotech established India's first fully green precipitated silica plant using 100% rice husk ash, powered entirely by renewable energy, setting a commercial precedent for sustainable supply. In a co-development initiative backed by USD 28 Million in funding from FMO and DEG, partners including Goodyear Tire and Rubber and the Indian Institute of Science designed the world's first commercial-scale green silica plant in India for tyre applications. For companies targeting export markets with mandatory Environmental Product Declaration (EPD) requirements or sustainability procurement criteria, bio-based silica from RHA in India's agricultural belt offers a compelling differentiator within India precipitated silica market.

Animal Feed Sector Creates New Demand for High-Absorption Functional Silica Grades

Precipitated silica functions as a high-performance carrier and anti-caking agent in feed premix applications, and India's rapidly evolving animal protein economy is creating structural demand for these grades. Per capita consumption of non-milk animal products in India rose from less than 6 kg in 1960 to 17 kg in 2021, and with India's population at 1.4 billion and projected to exceed 1.5 billion by 2050, alongside an expected doubling of incomes, demand for protein-rich animal products is set to accelerate. Poultry production grew at 8.5 % annually between 2000 and 2022, and India is the third-largest beef exporter globally.

PPG Industries published research confirming that its FLO-GARD precipitated silica products offer over 40 times higher carrying capacity compared to maltodextrin in bulk food and feed applications, with absorption efficiency above 66% by weight, demonstrating the functional superiority of speciality silica in feed premix manufacturing. Corn, wheat, and soybean meal constitute nearly two-thirds of India's animal feed consumption, and with corn imports projected to potentially surpass 20 million metric tonnes by 2034 under rapid income growth scenarios, high-volume feed production will require reliable, performance-grade silica carriers. India precipitated silica market is well-positioned to capture demand from this segment as domestic feed manufacturers upgrade formulation quality.

Category-wise Analysis

Application Insights

Rubber leads the application segment of accounting for approximately 65.5 % of total revenue in 2026. Its sustained dominance reflects the fundamental role of precipitated silica as a reinforcing filler in tyre tread compounds. Silica-reinforced tyres demonstrate measurably superior wet grip and a significant reduction in rolling resistance compared to carbon black-filled compounds, which translates directly into fuel efficiency gains that meet mandatory BEE tyre labeling norms. India's rubber industry is the fifth largest globally by consumption and the second-largest consumer of natural rubber worldwide, with Kerala contributing approximately 78 % of natural rubber output.

Natural rubber production recorded a 2.1 % year-on-year improvement in FY24, and synthetic rubber production surged 16.9 % in the same period, with April to October FY25 output at 333,436 tonnes, registering a further 4.8 % gain. With over 41 tyre companies across 62 plants and tyre exports at an all-time high, the structural link between rubber demand and precipitated silica consumption is long-duration and well-anchored. Tata Chemicals has committed INR 775 crore to expand its HDS silica plant in Cuddalore, Tamil Nadu, adding 50 ktpa capacity to serve this segment.

Agrochemicals are the fastest-growing application segment. India's agrochemical market is forecast to advance at a CAGR of 11.8% between 2024 and 2029, supported by government registration of new active molecules, Integrated Pest Management (IPM) adoption, and a shift toward higher-efficacy formulations that require superior carrier materials. Precipitated silica's high surface area and absorption capacity make it the preferred carrier for wettable powders and granular insecticide and fungicide formulations, ensuring uniform distribution and extended shelf stability.

India's pesticide demand is projected by NITI Aayog to reach 79,233 tonnes, and fertiliser consumption to hit 339 lakh tonnes by 2030. Export volume growth of 5 to 6 % in FY2025, driven by global destocking normalisation, reflects a volume-led recovery trajectory for Indian agrochemical producers that directly generates silica carrier demand. Kerala, Punjab, and Maharashtra are also enforcing stricter regulatory frameworks for highly hazardous pesticide molecules, accelerating reformulation toward safer, silica-carried alternatives.

Competitive Landscape

India precipitated silica market exhibits a moderately consolidated structure, where a few established manufacturers command a significant share, particularly in the rubber and tyre segment, while smaller regional players operate in niche applications. Leading companies such as Tata Chemicals Ltd, Madhu Silica Private Limited, AksharChem India Ltd, PPG Industries, Evonik Industries, and Solvay play a crucial role in shaping competitive dynamics through capacity expansions, product innovation, and strong distribution networks.

Domestic players like Tata Chemicals and Madhu Silica maintain strong positions due to integrated operations and long-standing relationships with tire manufacturers. Meanwhile, multinational companies compete through advanced grades such as highly dispersible silica (HDS) and speciality variants for high-performance and sustainable applications. Although entry barriers remain high due to capital intensity and technical know-how requirements, competition is intensifying with rising demand from the automotive, agrochemical, and personal care industries.

Key Industry Developments:

- In November 2025, Tata Chemicals Ltd: The company approved a INR 775 crore investment to expand its precipitated silica plant in Cuddalore, Tamil Nadu, adding 50 ktpa capacity over 27 months to its existing 13.8 ktpa facility, strengthening its position in the India Precipitated Silica market and addressing rising demand from the rubber and automotive tyre industries.

- In July 2025 , Aksharchem India Ltd: The company commissioned a 6,000 tonnes/year capacity expansion at its Dahej, Gujarat precipitated silica plant, increasing total production capacity to 18,000 tonnes/year effective June 24, 2025, strengthening its position in the India Precipitated Silica market by enhancing product range, improving raw material synergies, and expanding supply to the tyre and rubber industries.

- In January 2025, Evonik Industries: Effective January 1, 2025, Evonik launched “Smart Effects,” a newly formed entity created through the strategic merger of its Silica and Silanes business lines under the Advanced Technologies division. The integration combines precipitated silica, fumed silica, and silane technology platforms to enhance innovation capabilities and financing strength across global markets, including India. With around 3,500 employees worldwide, the move is expected to strengthen Evonik’s value proposition in high-performance rubber and tyre applications, supporting the evolving demand dynamics of the India precipitated silica market.

Companies Covered in India Precipitated Silica Market

- Evonik Industries

- W. R. Grace & Co

- PQ Corporation

- Tata Chemical

- PPF Industries

- Anten Chemical Co. Ltd

- Huber Engineered Materials

- PPG Industries, Inc.

- IQE Group

- Solvay S A.

- Oriental Silicas Corporation

- Tosoh Silica Corporation

- Ineos

Frequently Asked Questions

The India Precipitated Silica Market is projected to be valued at US$ 104.4 Mn in 2026.

The Rubber segment is expected to account for approximately 65.5% of the India Precipitated Silica Market by Application in 2026.

The market is expected to witness a CAGR of 10.5% from 2026 to 2033.

India Precipitated Silica Market growth is driven primarily by rising tyre and automotive demand for high-dispersion silica under BEE norms, accelerating agrochemical formulation upgrades requiring high-purity carrier silica, and sustained government-led infrastructure and housing expansion supporting downstream industrial applications.

Key market opportunities in the India Precipitated Silica Market lie in premium oral and personal care formulations requiring specialty abrasive grades, scalable bio-based green silica production from rice husk ash for export-driven sustainable supply chains, and expanding animal feed premix applications demanding high-absorption functional silica carriers.

Key players in the Precipitated Silica Market include Tata Chemicals Ltd, Madhu Silica Private Limited, AksharChem India Ltd, PPG Industries, Evonik Industries, and Solvay.