- Technology

- 5G Test Equipment Market

5G Test Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

5G Test Equipment Market by Equipment (Oscilloscopes, Signal & Spectrum Analyzers, Vector Signal Generators, Network Analyzers, Over-the-Air (OTA) Test Equipment, Others), Frequency Band (Sub-6 GHz, Millimeter Wave (mmWave), Dual-Band (Sub-6 GHz + mmWave)), End-user, and Regional Analysis for 2026 - 2033

5G Test Equipment Market Size and Trends Analysis

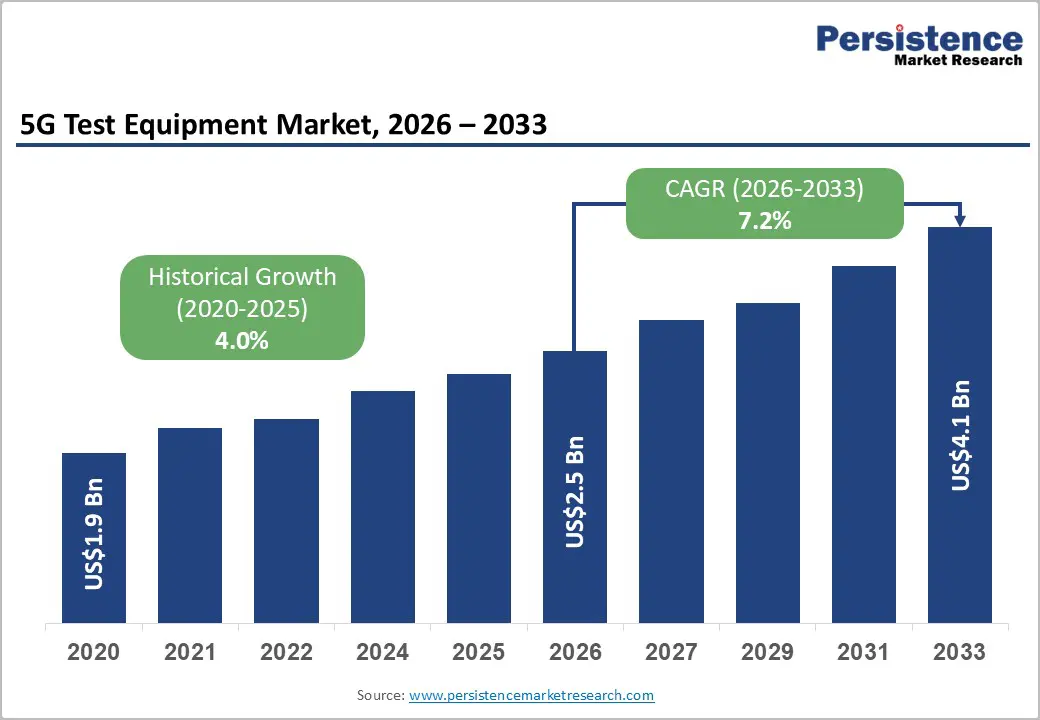

The global 5G test equipment market size is projected to rise from US$2.5 billion in 2026 to US$4.1 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by the surge in 5G devices and IoT connectivity, regulatory mandates for spectrum compliance, and the rise of Open RAN requiring multi-vendor testing. Asia Pacific leads in market size, while North America excels in innovation-driven solutions. Expanding enterprise adoption of private 5G networks and continuous advancements in test instrumentation further support market momentum.

Key Industry Highlights:

- Leading Equipment: Signal & spectrum analyzers dominate with over 26% market share in 2026, valued at over US$ 653.0 Mn, driven by the need for precise frequency, signal quality, and interference analysis across frequency bands. Vector Signal Generators hold ~21% share, while OTA test equipment is the fastest-growing at 10.9% CAGR, fueled by massive MIMO, mmWave deployments, and complex device-network interactions.

- Leading Frequency Band: Sub-6 GHz holds more than 56% market share in 2026, valued at above US$ 1.4 Bn, preferred for wide-area coverage and reliable indoor penetration. mmWave is the fastest-growing at 11.4% CAGR, driven by ultra-high-speed, low-latency applications such as autonomous vehicles, AR/VR, and smart factories.

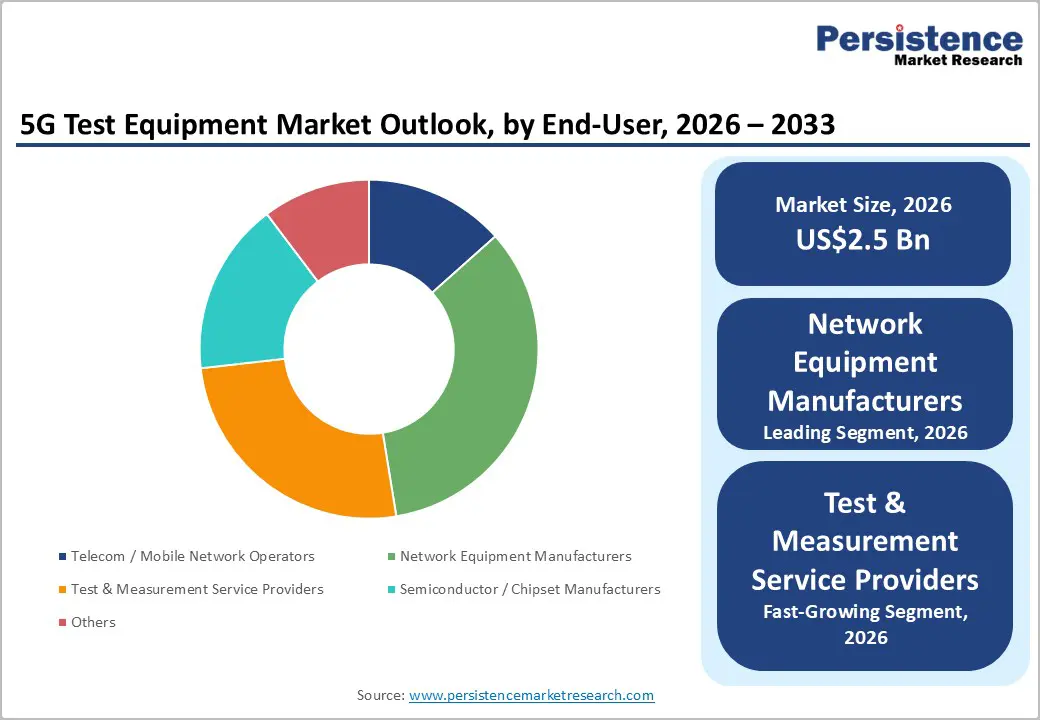

- Leading End-user: Network equipment manufacturers command the largest share at over 33% in 2026, valued at over US$ 828.8 Mn, requiring advanced testing for base stations, small cells, and mmWave infrastructure. Test & measurement service providers are growing fastest at 10.8% CAGR, driven by complex Open RAN, private 5G, and network slicing validation needs.

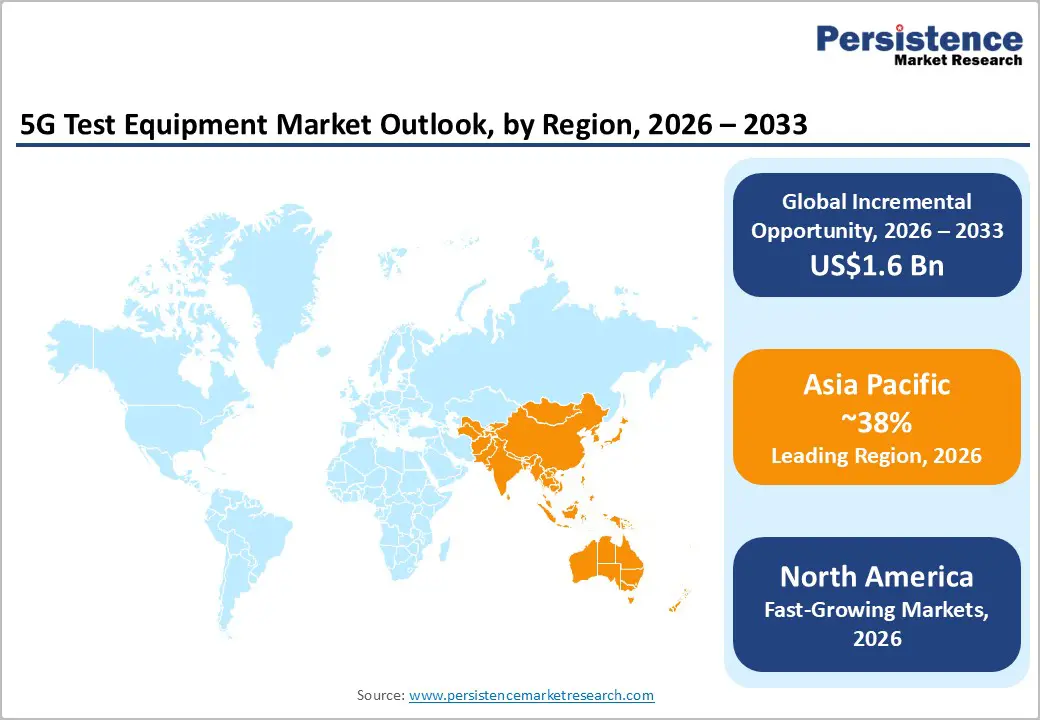

- Leading Region: Asia Pacific leads with over 38% share in 2026, valued at US$ 1.0 Bn, supported by China ~1.2 billion 5G subscriptions and dense 5G infrastructure. North America holds 31% share, valued at US$ 778.5 Mn, led by the U.S., while Europe accounts for more than 17% share by 2033, driven by regulatory harmonization and private network validation.

- Market Dynamics: AI-enabled autonomous testing, network slicing validation, and real-time performance monitoring present growth opportunities for equipment manufacturers and service providers, particularly in premium market segments.

| Key Insights | Details |

|---|---|

|

5G Test Equipment Market Size (2026E) |

US$2.5 Bn |

|

Market Value Forecast (2033F) |

US$4.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.0% |

Market Dynamics

Driver - 5G Infrastructure Rollout and Network Complexity Escalation

The global rollout of 5G infrastructure and escalating network complexity are driving demand for advanced 5G test equipment. Technologies such as massive MIMO, beamforming, mmWave, and dense small-cell deployments require rigorous validation of signal performance, latency, and throughput across multiple frequency bands. The transition to standalone 5G cores further expands testing needs for network slicing, virtualization, and cloud-native architectures. Operators must validate performance across diverse use cases, including eMBB, URLLC, and mMTC, each requiring specialized test protocols. Continuous upgrades, multi-vendor deployments, and lifecycle testing amplify the scope and criticality of 5G validation. By the end of 2025, 5G connections are projected to reach approximately 2.9 billion, roughly one-third of all mobile subscriptions worldwide, underscoring rapid network expansion and increasing complexity.

Open RAN and Private 5G Network Validation Requirements

Open RAN architectures introduce multi-vendor, disaggregated network environments, significantly increasing interoperability, conformance, and performance testing requirements across radio units, distributed units, and centralized units. Operators must validate fronthaul interfaces, timing synchronization, and software-defined functions to ensure network stability, driving higher demand for advanced 5G test equipment. Private 5G networks require customized validation for latency, reliability, security, and spectrum usage. Unlike public networks, each private 5G deployment is use-case specific, increasing the frequency and depth of pre-deployment and acceptance testing. By the end of 2024, over 4,700 private LTE/5G networks had been deployed worldwide, highlighting the growing need for bespoke validation and test equipment.

Restraint - Capital Intensity and High Cost of Advanced Testing Infrastructure

The 5G test equipment is highly capital-intensive, with advanced lab systems costing hundreds of thousands to millions of dollars and base station deployments ranging from US$100,000–200,000 per site. mmWave deployments require 1.5–2× higher CAPEX due to denser infrastructure needs. Smaller operators and regional test service providers face significant financial barriers, while manufacturers must continually upgrade equipment to comply with evolving 3GPP standards, creating recurring depreciation and operational cost pressures.

Technological Obsolescence Risk and Rapid Innovation Cycles

The acceleration of wireless technology development cycles creates a perpetual obsolescence risk for testing infrastructure. Emerging technologies, including Open RAN architecture, network disaggregation, software-defined networking (SDN), and AI-driven network optimization, render legacy testing platforms functionally obsolete within 3–4 years. This compressed innovation cycle compounds capital recovery challenges and discourages investment among price-sensitive market segments. The proliferation of proprietary testing solutions developed by large network operators creates fragmented testing ecosystems, reducing standardization and extending development timelines for equipment manufacturers.

Opportunity - Network Slicing Validation and Service Assurance Testing Requirements

Network slicing, the ability to partition physical network infrastructure into isolated virtual networks with customized performance characteristics, creates new testing requirements absent in previous wireless generations. Ensuring performance isolation across slices demands validation of latency, bandwidth, and reliability independent of concurrent traffic. This drives demand for specialized test and measurement services and software-enabled platforms capable of real-time monitoring of network slice performance. These emerging needs present significant growth opportunities for service providers and vendors.

Artificial Intelligence Integration and Autonomous Testing Automation

Artificial intelligence (AI) and machine learning (ML) technologies are moving from experimental domains into operational 5G testing platforms, creating significant differentiation opportunities for early-adopting equipment manufacturers. AI-powered testing solutions enable automated signal classification, predictive anomaly detection, and self-optimization capabilities that reduce operational complexity and accelerate time-to-market for new network deployments. Equipment manufacturers and service providers that integrate AI-enhanced testing platforms capitalize on the growing demand for advanced, efficient, and intelligent testing solutions, particularly in premium market segments.

Category-wise Analysis

Equipment Insights

Signal & spectrum analyzers dominate the global market, capturing more than 26% market share in 2026 with a value exceeding US$ 653.0 Mn due to 5G networks demanding precise frequency, signal quality, and interference analysis. They are essential for validating mmWave and sub-6 GHz performance, ensuring compliance with 3GPP standards, and optimizing network coverage and capacity. As 5G deployment grows, these analyzers help manufacturers and operators detect, troubleshoot, and fine-tune complex radio signals, making them indispensable for device and network testing. Vector Signal Generators maintain approximately 21% market share in 2026, providing essential signal generation capabilities for device testing and network validation.

Over-the-Air (OTA) test equipment demonstrates the highest growth rate at 10.9% CAGR due to the increasing complexity of devices and networks, especially with massive MIMO and mmWave technologies. OTA testing enables accurate evaluation of real-world wireless performance, including beamforming, interference, and multi-antenna interactions, without relying on cabled connections. The surge in 5G smartphones, IoT devices, and network densification drives demand for comprehensive OTA solutions to ensure regulatory compliance, signal quality, and end-user experience. The shift toward virtualized and small-cell networks requires flexible and scalable OTA testing setups.

Frequency Band Insights

Sub-6 GHz holds over 56% market share in 2026, with a value exceeding US$ 1.4 Bn, as most commercial 5G deployments prioritize wide-area coverage and reliable indoor penetration, which these frequencies provide. Network operators and device manufacturers require extensive testing for interoperability, spectrum efficiency, and signal quality at sub-6 GHz bands. The high adoption of smartphones and IoT devices operating in sub-6 GHz drives continuous demand for conformance, performance, and network optimization testing. This makes sub-6 GHz testing equipment indispensable for ensuring seamless 5G service delivery.

Millimeter Wave (mmWave) is expected to grow at the highest rate, with a CAGR of 11.4% due to its critical role in enabling ultra-high-speed, low-latency communications required for advanced applications like autonomous vehicles, AR/VR, and smart factories. The dense deployment of mmWave cells and complex beamforming technology creates a strong need for precise testing and measurement solutions. Equipment capable of validating high-frequency performance, signal integrity, and interference management is in high demand, driving rapid market growth.

End-user Insights

Network equipment manufacturers command the largest market share at over 33% in 2026 with a value exceeding US$ 828.8 Mn, due to their critical need to validate complex 5G network deployments, including base stations, small cells, and mmWave infrastructure. They require advanced testing to ensure interoperability, spectrum efficiency, and compliance with 3GPP standards. Rigorous performance evaluation of network elements under high traffic and diverse environmental conditions drives sustained demand for signal analyzers, network emulators, and conformance testing solutions. This ensures reliable service delivery and minimizes network downtime.

Test & measurement service providers are expected to grow at a CAGR of 10.8%, due to the increasing complexity of 5G networks and devices. Operators and OEMs often lack in-house expertise or high-cost equipment for end-to-end testing, driving demand for outsourced services. These providers fulfill critical needs such as network validation, device certification, and interoperability testing across frequency bands. Emerging technologies like Open RAN, private 5G networks, and network slicing require specialized testing, further boosting service adoption.

Regional Insights

North America 5G Test Equipment Market Trends

North America holds over 31% share in 2026, reaching US$ 778.5 Mn value, supported by strong technological leadership and advanced regulatory frameworks. The U.S. benefits from mature nationwide 5G coverage by major carriers and stringent FCC conformance requirements that drive sustained demand for advanced testing solutions. High private-sector investment in Open RAN, edge computing, and network virtualization, combined with the presence of global leaders such as Keysight and National Instruments, accelerates innovation. FCC’s emissions-focused, streamlined compliance approach enables faster certification cycles, fostering rapid product upgrades and competitive market dynamics.

Asia Pacific 5G Test Equipment Market Trends

Asia Pacific dominates the global market, accounting for more than 38% market share in 2026, with a value reaching US$ 1.0 Bn, expected to grow at the highest rate. China leads the region with ~1.2 billion 5G subscriptions by end-2025 and over ~4.4 million deployed 5G base stations as of March 2025, supported by near-universal 5G smartphone adoption. Japan has achieved near-saturation 5G coverage ~98% population by late 2024/early 2025, while India reached ~365 million 5G subscribers by mid-2025, reflecting rapid post-2022 rollout momentum. Growth is reinforced by strong electronics manufacturing ecosystems, government-backed domestic technology programs, cost-efficient testing services, and dense urban deployments enabling mmWave economics. ASEAN markets such as Vietnam, Thailand, Indonesia, and the Philippines are emerging as high-potential hubs driven by national digital economy initiatives.

Europe 5G Test Equipment Market Trends

Europe is expected to hold more than 17% share by 2033, driven by regulatory harmonization efforts and a well-established telecommunications infrastructure. Regulatory oversight through ETSI and national frequency authorities mandates rigorous conformance, interoperability, and spectrum compliance testing, sustaining consistent demand for test and measurement solutions. The region demonstrates a strong focus on network slicing validation, service assurance, and cross-vendor interoperability, particularly for enterprise and private 5G deployments. The European Union’s proposed Digital Networks Act (DNA) signals long-term regulatory intent toward greater harmonization across member states, which could reduce testing fragmentation and improve scalability for solutions achieving EU-wide acceptance.

Competitive Landscape

The 5G test equipment market exhibits a semi-consolidated competitive structure with pronounced leader dominance and fragmented mid-tier competition. Companies are focusing on differentiation through high-precision, low-latency testing solutions, covering base stations, user equipment, and network slices. Strategic partnerships with telecom operators and network equipment providers are leveraged to ensure early adoption and integration into 5G rollouts. Firms are investing in R&D to reduce testing time, improve accuracy, and expand service offerings, maintaining a competitive edge in a technologically complex market.

Key Industry Developments:

- In November 2025, Keysight Technologies validated the industry’s first PTCRB 5G NR non-terrestrial network (NTN) test cases under 3GPP Release 17, enabling faster certification of satellite-based 5G devices. The milestone strengthens Keysight’s leadership in advanced RF and performance testing as mobile and satellite networks increasingly converge.

- In September 2025, VeEX Inc. introduced the MTX642 2x400GE Multi-Service Handheld test set, the industry’s most compact dual 400GE portable test solution supporting next-generation optical transceivers. Designed for fast field operations, the device enables efficient troubleshooting, installation, and commissioning of high-speed 400GE networks with simplified, predefined test configurations.

- In July 2025, Anritsu Corporation launched new software options for its MT8000A Radio Communication Test Station to evaluate 5G device RF performance in compliance with 3GPP Release 17. The updates support advanced technologies such as 1024QAM downlink and Tx Switching 2Tx-to-2Tx uplink, enabling higher throughput, improved uplink stability, and more accurate testing of next-generation 5G devices.

Companies Covered in 5G Test Equipment Market

- Keysight Technologies

- Spirent Communications

- Tektronix, Inc.

- Anritsu Corporation

- LitePoint

- MACOM Technology Solutions

- Viavi Solutions

- Rohde & Schwarz

- Teradyne, Inc.

- National Instruments Corporation.

- GL Communications Inc.

- Exfo Inc.

- Others

Frequently Asked Questions

The global 5G test equipment market is projected to be valued at US$2.5 Bn in 2026.

The need for high-precision validation of complex 5G networks, devices, and services to ensure performance, reliability, and compliance with evolving global standards is a key driver of the market.

The 5G test equipment market is expected to witness a CAGR of 7.2% from 2026 to 2033.

The increasing demand for AI-driven test solutions for next-generation devices and networks is creating strong growth opportunities.

Keysight Technologies, Spirent Communications, Tektronix, Inc., Anritsu Corporation, MACOM Technology Solutions are among the leading key players.