- Medical Devices

- Robotic X-ray Systems Market

Robotic X-ray Systems Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Robotic X-ray Systems Market by Product (Robotic C Arm, Twin Robotic X-ray, Overhead Tube Suspension (OTS) X-ray, and Others), by Application (Orthopedics, Surgery, and Trauma), by End-user (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 - 2033

Robotic X-ray Systems Market Share and Trends Analysis

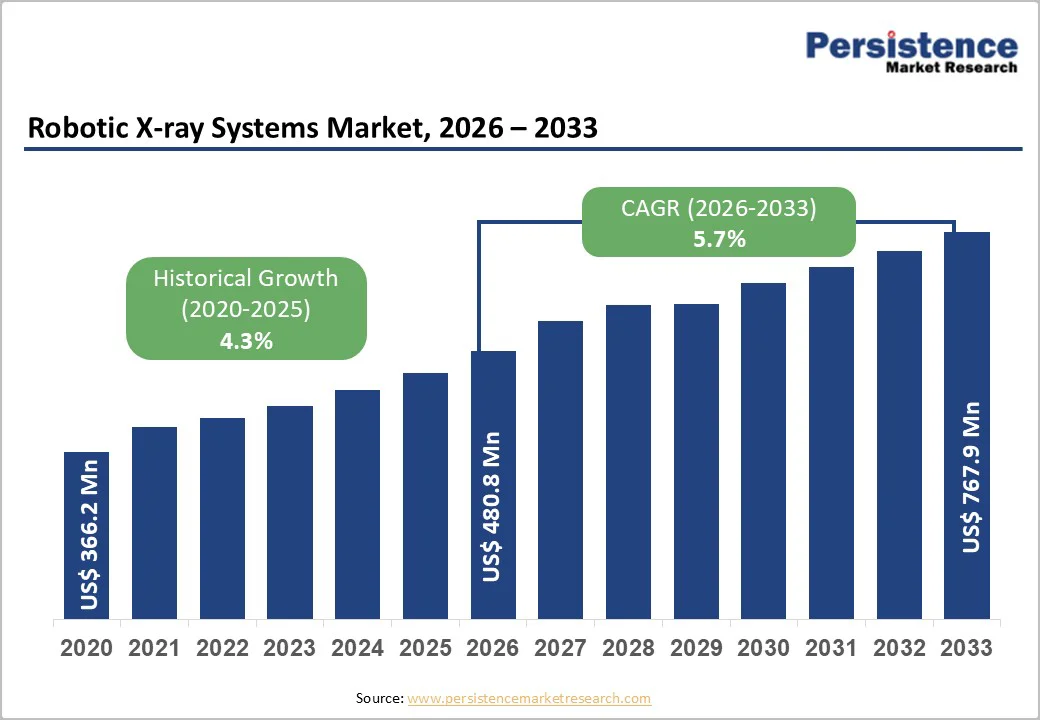

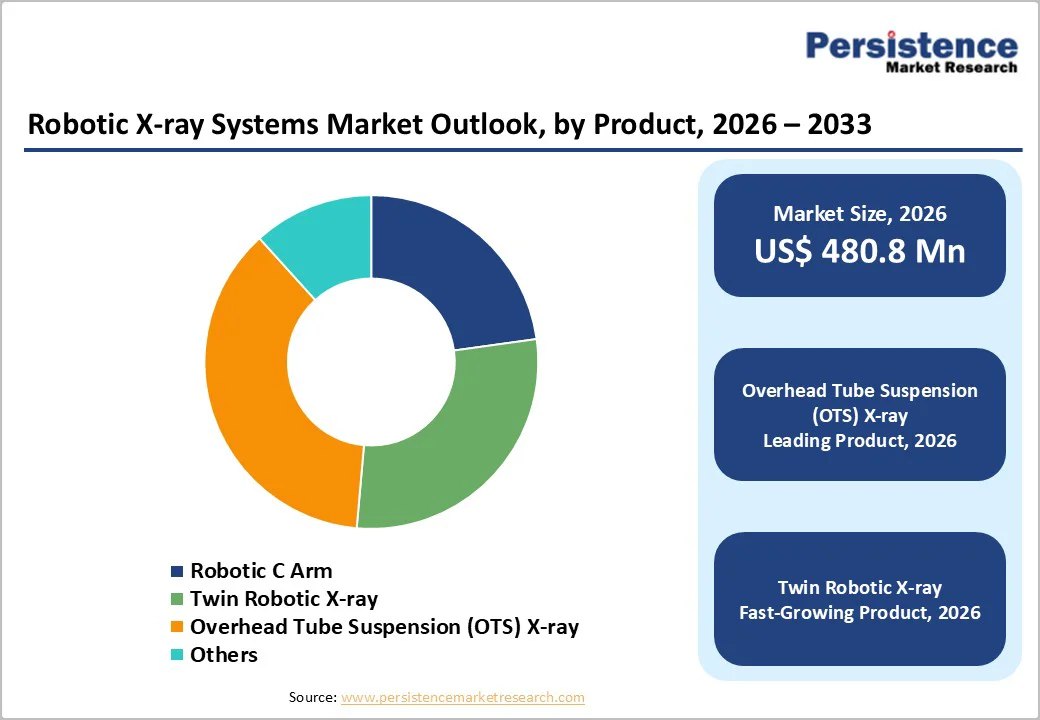

The global robotic X-ray systems market size is estimated to grow from US$ 480.8 million in 2026 to US$ 767.9 million by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

Global demand for robotic X-ray systems is surging due to the need for high-precision imaging, automated positioning, and faster workflow throughput in hospitals, surgical centers, and trauma units. Rising caseloads in orthopedics, emergency medicine, and minimally invasive procedures are accelerating the shift toward robotic radiography for reproducible, operator-independent imaging. Advancements in AI-based auto-positioning, dose optimization, and integrated digital workflows are improving diagnostic accuracy and reducing technician workload. Additionally, growing investments in hospital modernization, digital radiology upgrades, and clinical automation are further boosting market growth.

Key Industry Highlights

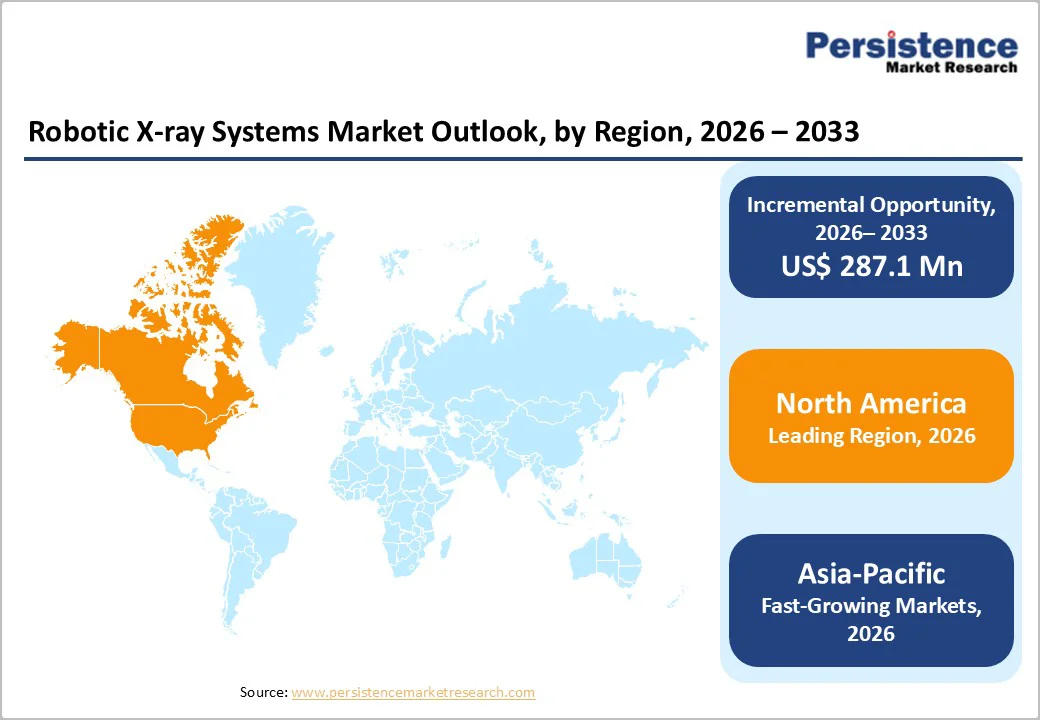

- Leading Region: North America leads the global robotic X-ray systems market with a 46.8% share, supported by strong healthcare infrastructure, early adoption of robotic imaging platforms, and continuous investment in AI-enabled radiology technologies.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, fueled by rapid healthcare infrastructure expansion, rising patient volumes, and increasing procurement of advanced digital radiography systems across China, India, and Southeast Asia.

- Leading Product Segment: Overhead tube suspension (OTS) X-ray systems dominate the product category due to their high precision, wide clinical versatility, and strong adoption in high-volume hospitals and imaging centers.

- Fastest-Growing Product Segment: Twin robotic X-ray systems represent the fastest-growing product segment, driven by enhanced automation, multi-angle imaging capability, and increasing preference for advanced workflow efficiency.

- Leading Application Segment: Orthopedics holds the largest share in application segmentation, supported by growing demand for accurate skeletal imaging, rising fracture incidence, and high utilization in surgical planning and follow-up.

- Fastest-Growing Application Segment: Trauma is the fastest-growing category, driven by rising emergency caseloads, demand for rapid and reproducible imaging, and greater integration of robotic systems in high-acuity emergency and trauma departments.

| Key Insights | Details |

|---|---|

|

Robotic X-ray Systems Market Size (2026E) |

US$ 480.8 Mn |

|

Market Value Forecast (2033F) |

US$ 767.9 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.3% |

Market Dynamics

Driver - Growing Demand for High-Quality Digital Radiography Driven by Clinical & Demographic Shifts

Hospitals and diagnostic centers are rapidly upgrading from analog systems to advanced digital radiography (DR) to achieve sharper imaging, faster processing, and more efficient workflow. The shift toward DR is also driven by the need for better dose control and automated, repeatable patient positioning. Robotic X-ray systems fit directly into this transition, offering precise robotic movement that enhances image consistency and supports high-throughput environments.

Moreover, aging populations and the rising incidence of chronic and trauma-related conditions are increasing the frequency of radiographic examinations. Orthopedic injuries, degenerative disorders, and emergency trauma cases require repeated imaging for diagnosis and monitoring. As patient volumes grow, providers need systems that deliver accuracy, speed, and minimal retakes. Robotic X-ray solutions address these needs by improving positioning efficiency and maintaining consistent image quality across high-demand clinical settings.

Restraints - High Capital Burden and System Integration Barriers Restrict Near-Term Adoption

Robotic X-ray systems face slower uptake due to significant upfront investment requirements and long payback periods, particularly for smaller hospitals and standalone clinics with limited capital budgets. Beyond the purchase price, facilities must also account for installation, room modifications, staff training, and ongoing maintenance factors that collectively raise the total cost of ownership and make decision-makers more cautious about large-scale imaging upgrades.

Adoption is further constrained by integration and regulatory challenges. Retrofitting robotic X-ray systems into existing PACS, EMR platforms, and legacy modality fleets often requires extensive compatibility work, extending deployment timelines. Alongside this, strict medical device approvals, radiation safety regulations, and compliance documentation increase development and certification costs for manufacturers. These integration and regulatory hurdles combine to slow market expansion despite the technology’s strong long-term value.

Opportunity - Growing Shift toward Intelligent Automation and Remote Imaging Capabilities

The integration of AI with robotic X-ray systems is creating new value layers through features such as automated patient positioning, dose-optimized protocols, and computer-assisted detection. These enhancements improve workflow speed, reduce retake rates, and deliver more consistent diagnostic-quality images. As imaging platforms become increasingly software-driven, vendors can introduce upgradeable AI modules and subscription-based tools, and are creating growth opportunities.

Furthermore, remote and operator-assist imaging models are emerging as major growth avenues. Robotic X-ray systems that can be monitored or guided by centralized imaging specialists enable high-quality radiography in rural, underserved, or low-staffed ambulatory centers. This approach helps overcome local workforce shortages while ensuring uniform imaging standards across distributed networks. The combination of intelligent automation and remote-operability positions robotic X-ray systems as a key enabler of scalable, decentralized diagnostic care.

Category-wise Analysis

By Product

The overhead tube suspension (OTS) X-ray segment is projected to dominate the global robotic X-ray systems market in 2026, accounting for a revenue share of 36.9%. The segment’s strong performance is primarily driven by the expanding installation of fully automated DR rooms, increasing preference for ceiling-mounted systems that offer wide clinical coverage, and their suitability for high-throughput environments such as emergency departments and orthopedic imaging suites.

OTS systems also provide superior flexibility for complex patient positions, enabling faster workflow, reduced retakes, and consistent image quality factors that collectively strengthen their leadership in hospital and large imaging-center deployments. Additionally, their seamless integration with advanced imaging software boosts operational efficiency, while growing investments in the modernization of radiology infrastructure continue to accelerate demand for OTS-based robotic systems.

By Application Insights

The orthopedics segment is projected to dominate the global robotic X-ray systems market in 2026, accounting for a revenue share of 57.4%. This is driven by the high volume of musculoskeletal cases requiring frequent imaging for diagnosis, surgical planning, and postoperative monitoring. Robotic X-ray systems support orthopedics by enabling precise, repeatable positioning, which is essential for assessing fractures, spinal alignment, and joint replacement outcomes. Their ability to deliver consistent, high-resolution images with minimal retakes further enhances clinical efficiency.

Growing orthopedic procedure volumes, including trauma repairs and joint reconstruction, continue to reinforce the segment’s leading position in the market. Additionally, the rising adoption of minimally invasive orthopedic surgeries and the corresponding need for accurate intraoperative imaging further accelerate demand for robotic X-ray systems in this segment.

By End-user Insights

The hospitals segment is projected to dominate the global robotic x-ray systems market in 2026, accounting for a revenue share 53.8%. This is driven by the high patient volume and broad clinical workload across emergency, orthopedic, and surgical departments, which increases the need for fast, automated imaging solutions. Hospitals also have greater capital budgets to invest in advanced radiography infrastructure, enabling the adoption of robotic systems that improve workflow efficiency and reduce retakes. Their ability to integrate seamlessly with PACS and existing imaging fleets further strengthens utilization.

Ongoing expansion of hospital radiology suites and modernization initiatives across developed and emerging regions continue to reinforce the segment’s leadership. Additionally, the growing shift toward smart hospitals and automated imaging workflows is pushing providers to adopt robotic systems to enhance throughput and clinical accuracy.

Region-wise Insights

North America Robotic X-ray Systems Market Trends

The North America market is expected to dominate globally with a value share of 46.8% in 2026, with the U.S. leading the region due to its rapid adoption of advanced imaging technologies and strong investments in radiology automation. High procedure volumes across emergency care, trauma centers, and orthopedic departments further accelerate demand for robotic X-ray systems.

The region also benefits from well-established healthcare infrastructure, faster technology approvals, and a strong presence of leading manufacturers. Growing hospital modernization programs and early integration of AI-driven imaging workflows continue to drive regional growth. Additionally, increasing emphasis on reducing imaging turnaround times and improving clinical productivity is driving deeper penetration of robotic X-ray systems across high-acuity settings.

Europe Robotic X-ray Systems Market Trends

Europe is expected to achieve a steady growth, driven by rising demand for high-precision diagnostic imaging and increasing adoption of automation technologies across hospital radiology departments. Continuous investments in upgrading healthcare infrastructure, particularly in Western Europe, are supporting the shift toward advanced digital and robotic X-ray systems.

The region is also benefiting from the growing need to manage aging populations, which significantly increases imaging volumes. Additionally, strong regulatory emphasis on radiation safety and workflow efficiency is encouraging hospitals to transition to more automated, dose-optimized imaging solutions. Emerging collaborations between technology developers and European research institutions are further propelling product innovation and market growth.

Asia Pacific Robotic X-ray Systems Market Trends

Asia Pacific is expected to register a relatively higher CAGR of around 7.4% between 2026 and 2033, fueled by the rapid expansion of healthcare infrastructure and increasing investments in modernizing radiology departments across China, India, and Southeast Asia. Rising patient volumes driven by expanding populations, urban migration, and a growing burden of trauma, orthopedic injuries, and age-related degenerative conditions continue to push hospitals toward high-efficiency imaging solutions. Favorable government programs aimed at strengthening diagnostic capacity, such as China’s tiered healthcare reform and India’s PM-ABHIM initiative, are accelerating the adoption of digital and automated radiology systems.

Moreover, increasing penetration of AI-enabled imaging workflows, PACS upgrades, and integrated diagnostic platforms is creating a strong demand pool for robotic X-ray systems with higher throughput. The growing presence of global manufacturers, along with rising local production and assembly capabilities in China and South Korea, is significantly reducing procurement costs and improving accessibility for mid-sized healthcare facilities.

Competitive Landscape

The global robotic x-ray systems market is highly competitive, with major players such as Siemens Healthineers AG, GE HealthCare, Koninklijke Philips N.V., Canon Medical Systems Corporation, Carestream Health, leveraging extensive imaging portfolios, advanced robotics integration capabilities, and strong global distribution networks. Companies are prioritizing innovation in fully automated, AI-assisted, and high-throughput robotic X-ray systems designed to enhance diagnostic accuracy, reduce technician workload, and improve patient positioning efficiency.

Market participants are actively investing in next-generation robotic arms, intelligent auto-positioning algorithms, radiation dose-optimization technologies, and seamless integration with PACS/RIS platforms to strengthen clinical performance. Strategic initiatives include mergers and acquisitions to expand automation and imaging software capabilities, partnerships with hospitals and radiology institutes for workflow optimization trials, and geographic expansion across high-growth regions such as Asia Pacific, Latin America, and the Middle East.

Key Industry Developments:

- In March 2025, GE HealthCare announced an expanded collaboration with NVIDIA at GTC 2025, strengthening their ongoing partnership to accelerate innovation in autonomous imaging. The initiative focuses on advancing autonomous X-ray technologies and developing autonomous applications in ultrasound to enhance diagnostic speed, consistency, and workflow automation.

- In July 2025, Canon Medical Systems introduced the Radrex i5 / Flex Edition, a compact general-radiography X-ray system featuring a range of newly added capabilities designed to enhance imaging performance and operational efficiency.

Companies Covered in Robotic X-ray Systems Market

- Siemens Healthineers AG

- GE HealthCare

- Koninklijke Philips N.V.,

- Canon Medical Systems Corporation

- Carestream Health.

- Samsung Healthcare

- Shimadzu Corporation

- Fujifilm Holdings Corporation

- North Star Imaging Inc

- Nikon Corporation Industrial Solutions Business Unit

- X-RIS srl

- Others

Frequently Asked Questions

The global robotic X-ray systems market is projected to be valued at US$ 480.8 Mn in 2026.

Rising demand for high-precision, automated imaging that improves workflow efficiency and diagnostic accuracy are driving the global robotic x-ray systems market.

The global robotic X-ray systems market is poised to witness a CAGR of 5.7% between 2026 and 2033.

Rapid integration of AI-driven automation, remote imaging workflows, and advanced decision-support tools is creating opportunities in the market.

Siemens Healthineers AG, GE HealthCare, Koninklijke Philips N.V., Canon Medical Systems Corporation, Carestream Health are some key players in the robotic X-ray systems market.