- Medical Devices

- Robotic Ultrasound System Market

Robotic Ultrasound System Market Size, Share, and Growth Forecast, 2025 - 2032

Robotic Ultrasound System Market by Product Type (Cart/Trolley-based Systems, Compact/Handheld Systems), Application (Radiology, Cardiology, Obstetrics & Gynecology, Others), End-use (Hospitals & Clinics, Ambulatory Surgical Centers, Specialty Clinics/Diagnostic Imaging Centers, Academic & Research Institutes), and Regional Analysis for 2025 - 2032

Robotic Ultrasound System Market Size and Trends Analysids

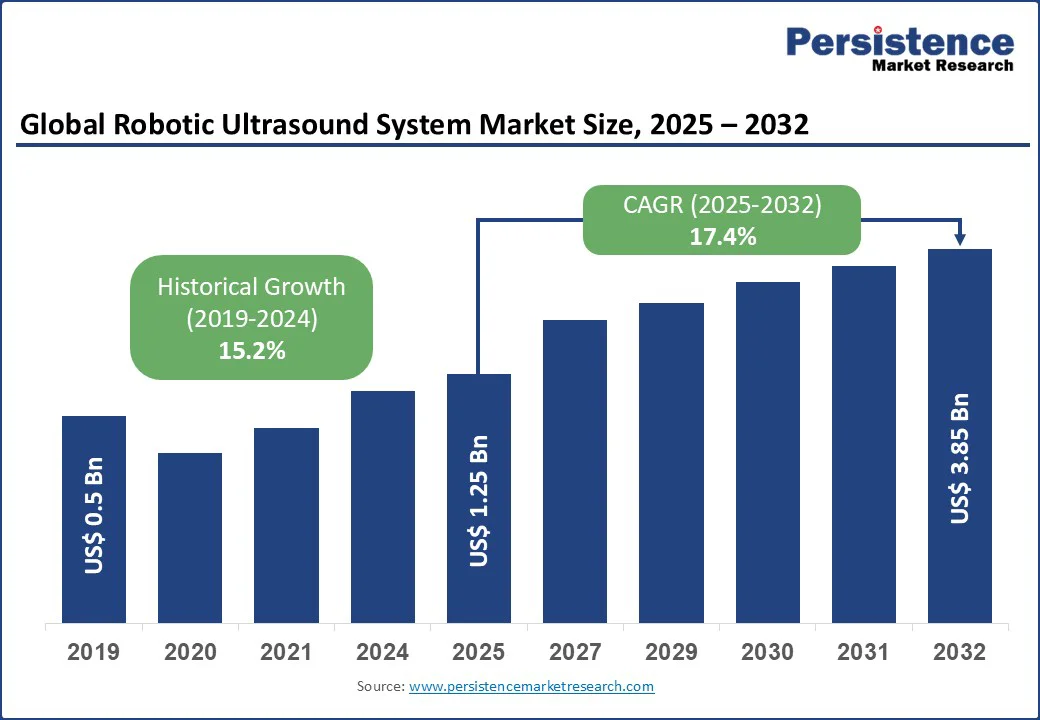

The global robotic ultrasound system market size is likely to be valued at US$ 1.25 Bn in 2025 and reach US$ 3.85 Bn by 2032, growing at a CAGR of 17.4% during the forecast period from 2025 to 2032.

The robotic ultrasound system market is experiencing rapid growth, driven by advancements in automation, artificial intelligence (AI), and increasing demand for precise, non-invasive diagnostic tools across healthcare settings.

Robotic ultrasound systems, known for their precision, reproducibility, and ability to reduce operator dependency, are critical for applications in radiology, cardiology, and obstetrics. The rise in chronic diseases, coupled with technological innovations in imaging, supports market expansion.

Key Industry Highlights

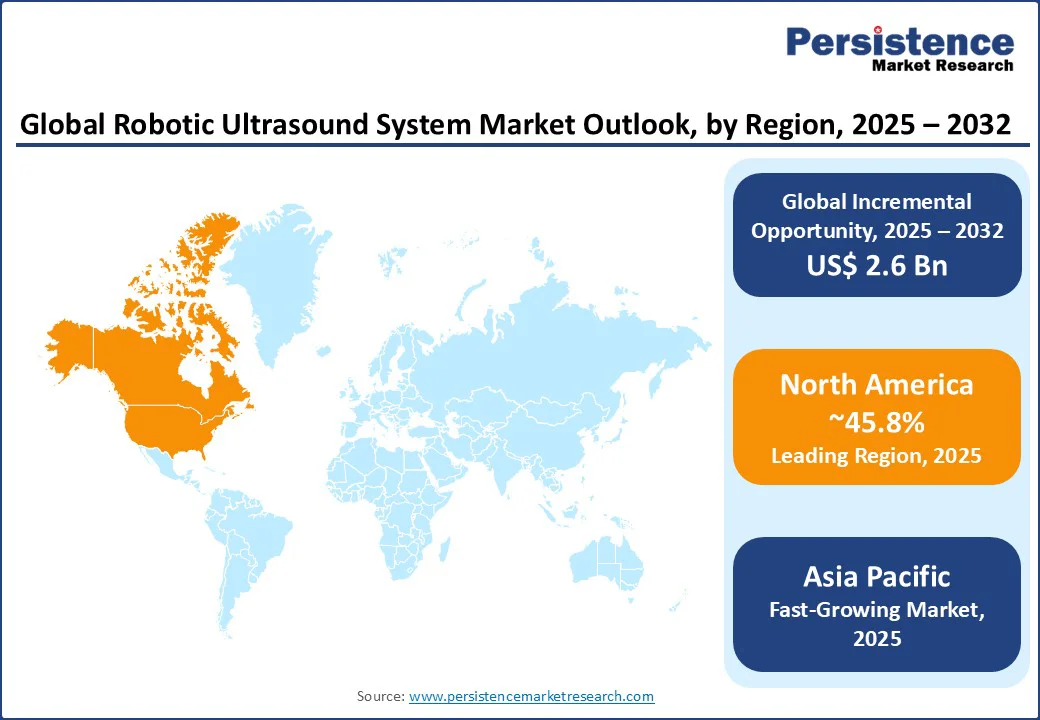

- Leading Region: North America holds 45.8% market share in 2025 of the global robotic ultrasound system market, propelled by advanced healthcare infrastructure, high adoption of AI-driven diagnostics, and significant R&D investments in the U.S.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rising healthcare investments and increasing prevalence of chronic diseases in China and India.

- Investment Plans: (November 2023) The Bill & Melinda Gates Foundation provided a total of $60 million to Philips to support the adoption of AI-powered handheld ultrasound technology, aiming to improve maternal health globally.

- Dominant Product Type: Cart/Trolley-based systems account for nearly 68.5% of the market share, due to their superior imaging capabilities and widespread use in hospitals.

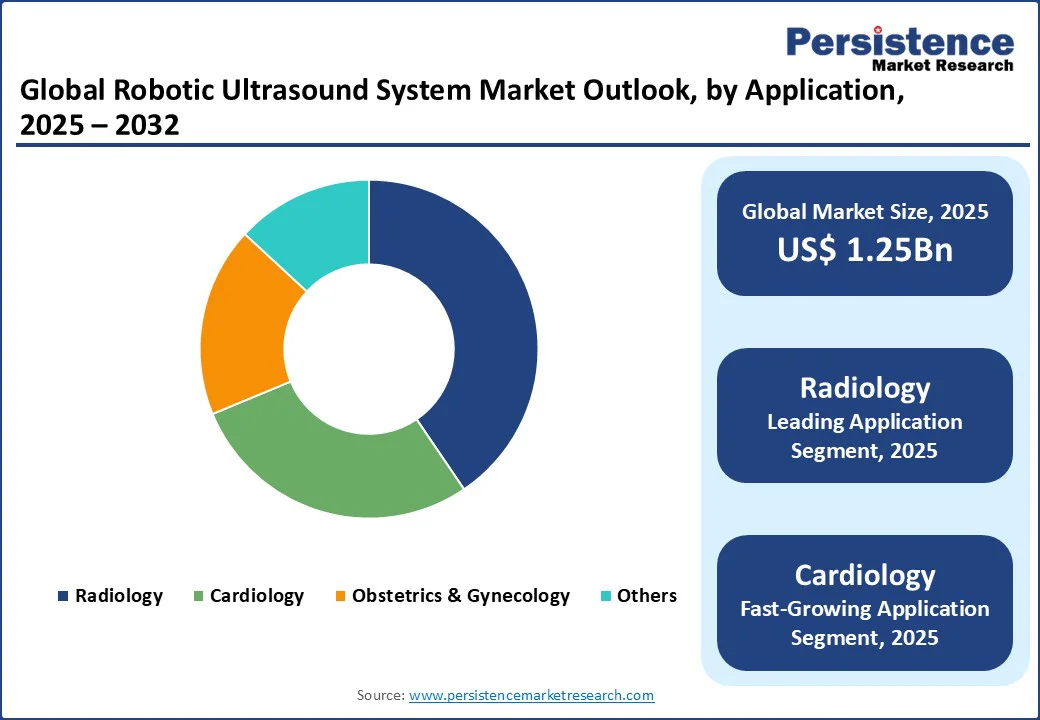

- Leading Application: Radiology contributes over 40.2% of market revenue, driven by demand for precise diagnostic imaging in general and specialized procedures.

|

Global Market Attribute |

Key Insights |

|

Robotic Ultrasound System Market Size (2025E) |

US$ 1.25 Bn |

|

Market Value Forecast (2032F) |

US$ 3.85 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

17.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

15.2% |

Market Dynamics

Driver: Advancements in AI and Robotics Enhance Diagnostic Precision

The robotic ultrasound system market is witnessing significant growth due to advancements in AI and robotics, which enhance diagnostic precision and efficiency. AI-integrated systems enable automated image analysis, real-time guidance, and standardized scanning protocols, reducing human error and improving reproducibility.

According to the World Health Organization, noncommunicable diseases (NCDs), such as cardiovascular diseases, cancer, diabetes, and chronic respiratory diseases, are responsible for 74% of all deaths worldwide, driving demand for accurate diagnostic tools.

In North America, companies such as GE Healthcare and Siemens Healthineers reported an increase in sales of AI-enabled ultrasound systems in 2024. In the Asia Pacific, China’s focus on smart hospitals and Japan’s advancements in robotic imaging fuel market growth. These technological innovations, coupled with rising demand for non-invasive diagnostics, ensure sustained market expansion through 2032.

Restraint: High Costs and Limited Accessibility in Developing Regions

The robotic ultrasound system market faces challenges due to high costs and limited accessibility in developing regions. The development and deployment of robotic systems require significant investment in advanced technologies, such as AI and robotic arms, leading to high equipment costs. In 2023, the average cost of a robotic ultrasound system ranged from $100,000 to $500,000, posing a barrier for smaller healthcare facilities.

Price volatility of components, such as semiconductors, further impacts production costs. Additionally, competition from traditional ultrasound systems, which are more affordable, limits adoption in cost-sensitive markets. Regulatory complexities and a lack of trained technicians in regions such as Latin America and Africa hinder market penetration, restraining overall growth despite technological advancements.

Opportunity: Growing Demand for Telemedicine and Remote Diagnostics

The increasing focus on telemedicine and remote diagnostics presents significant opportunities for the robotic ultrasound system market. Robotic systems enable remote imaging through tele-ultrasound capabilities, addressing healthcare access challenges in rural and underserved areas.

In North America, companies such as Philips and Esaote are innovating with tele-ultrasound solutions for rural clinics. Government initiatives, such as the EU’s Digital Health Strategy, promote remote diagnostics, creating opportunities for manufacturers to develop compact, AI-driven systems.

The rising prevalence of chronic diseases and the need for real-time diagnostics in emergency settings further drive demand for robotic ultrasound systems, positioning them as a critical tool for healthcare modernization through 2032.

Category-wise Insights

By Product Type

- Cart/Trolley-based systems hold the largest market share, approximately 68.5% in 2025, due to their superior imaging capabilities and widespread use in hospitals. These systems offer high-resolution imaging and multiple transducer ports, making them ideal for complex diagnostic procedures. Companies such as GE Healthcare and Siemens Healthineers lead with extensive portfolios, catering to demand in North America and Europe.

- Compact/Handheld systems are the fastest-growing segment, driven by their portability and suitability for point-of-care (POC) diagnostics. These systems are gaining traction in emergency and rural settings, with brands such as FUJIFILM SonoSite and Philips expanding offerings in the Asia Pacific and North America, supported by demand for accessible, real-time imaging.

By Application

- The radiology segment accounts for over 40.2% of market revenue in 2025, driven by its wide application in general and specialized diagnostic imaging. Robotic ultrasound systems enhance precision in imaging soft tissues and organs, with major players such as Fujifilm Holdings and Mindray supplying advanced systems for radiology centers in North America and the Asia Pacific.

- The cardiology segment is the fastest-growing application, propelled by rising cardiovascular disease prevalence and demand for real-time imaging. Robotic systems are used in echocardiography, with companies such as Koninklijke Philips and Samsung Medison innovating for high-performance applications. Growth in Europe and the Asia Pacific supports this segment’s rapid expansion.

By End-use

- Hospitals & Clinics account for the largest market share, approximately 65.3% in 2025, driven by high adoption of robotic ultrasound systems for comprehensive diagnostics. These facilities rely on advanced imaging for radiology and cardiology, with players such as GE Healthcare and Siemens dominating in North America and Europe.

- Specialty Clinics/Diagnostic Imaging Centers are the fastest-growing end-use, fueled by increasing demand for specialized diagnostics and outpatient care. These centers adopt compact systems for accessibility, with companies such as Esaote and Mindray expanding offerings in Asia Pacific and North America to meet growing needs.

Regional Insights

North America Robotic Ultrasound System Market Trends

North America dominates the robotic ultrasound system market, accounting for 45.8% of the market share, driven by advanced healthcare infrastructure and high adoption of AI-driven diagnostics in the U.S. and Canada. The U.S. healthcare sector relies on robotic systems for precise imaging.

Canada’s focus on telemedicine drives demand for compact systems, per Health Canada reports. Major players such as GE Healthcare and Philips dominate with extensive distribution networks, catering to hospitals and specialty clinics.

Government investments, such as the $47.35 billion NIH funding for AI in healthcare, ensure sustained market growth through 2032. A significant portion of this funding supports various research programs, including those focused on AI and healthcare innovation.

Asia Pacific Robotic Ultrasound System Market Trends

Asia Pacific is the fastest-growing region, fueled by rising healthcare investments and the increasing prevalence of chronic diseases in China and India. China, a leader in smart hospital initiatives, contributes significantly to market growth, per the China Health Commission.

India’s healthcare sector, supported by initiatives such as Ayushman Bharat, boosts demand for robotic systems. The region’s growing medical tourism and expanding diagnostic centers drive adoption, with companies such as Mindray and Fujifilm Holdings expanding their presence. Technological advancements and government-led digital health initiatives ensure the Asia Pacific’s rapid market growth through 2032.

Europe Robotic Ultrasound System Market Trends

Europe is the second fastest-growing region, driven by stringent regulations, rising demand in cardiology and radiology, and healthcare modernization in countries such as Germany and France. The European healthcare industry is a substantial sector within the EU, with healthcare expenditure averaging €3,685 per person in 2022, supporting demand for robotic ultrasound systems.

Germany’s focus on precision diagnostics and France’s investments in telemedicine fuel adoption. The EU’s Digital Health Strategy promotes AI-driven diagnostics, increasing demand for advanced systems. Companies such as Siemens Healthineers and Esaote innovate to meet regulatory and consumer demands, driving market growth through 2032.

Competitive Landscape

The global robotic ultrasound system market is highly competitive and fragmented, with numerous domestic and international players ranging from large corporations to regional manufacturers.

Leading companies such as GE Healthcare, Siemens AG, and Koninklijke Philips dominate through extensive product portfolios and global distribution networks. Regional players such as Mindray focus on cost-effective solutions in the Asia Pacific. Companies are investing in AI, robotics, and tele-ultrasound technologies to enhance market share, driven by demand for precise diagnostics in radiology and cardiology.

Key Industry Developments

- March 2025: Wipro GE Healthcare introduced the Versana Premier R3, an AI-powered ultrasound system manufactured in India. This system integrates artificial intelligence to enhance clinical efficiency, streamline workflows, and improve diagnostic accuracy.

- June 2024: Philips introduced an AI-integrated robotic ultrasound arm for cardiac diagnostics, enabling semi-autonomous probe manipulation, strengthening its position in Europe and the Asia Pacific. These applications received FDA 510(k) clearance and are designed to enhance the efficiency and accuracy of cardiac diagnostics.

Companies Covered in Robotic Ultrasound System Market

- GE Company

- Fujifilm Holdings Corporation

- Siemens AG

- Koninklijke Philips N.V.

- Toshiba Medical System Corp.

- Hitachi Medical Corp.

- Mindray Medical International Ltd

- Samsung Medison Co., Ltd

- Esaote SpA

- Others

Frequently Asked Questions

The Robotic Ultrasound System market is projected to reach US$ 1.25 Bn in 2025.

Advancements in AI and robotics, along with rising demand for non-invasive diagnostics, are the key market drivers.

The Robotic Ultrasound System market is poised to witness a CAGR of 17.4% from 2025 to 2032.

The rising demand for telemedicine and remote diagnostics is the key market opportunity.

GE Healthcare, Siemens AG, Koninklijke Philips, and Fujifilm Holdings are key market players.