- Medical Devices

- Robotic Dentistry Market

Robotic Dentistry Market Size, Share, and Growth Forecast 2026 - 2033

Robotic Dentistry Market by Component (Robotic Systems, Software, Services), Application (Implantology, Endodontics, Orthodontics, Oral & Maxillofacial Surgery, Others), End-user (Dental Hospitals & Clinics, Dental Academic & Research Institutes, Others), and Regional Analysis, 2026 - 2033

Robotic Dentistry Market Share and Trends Analysis

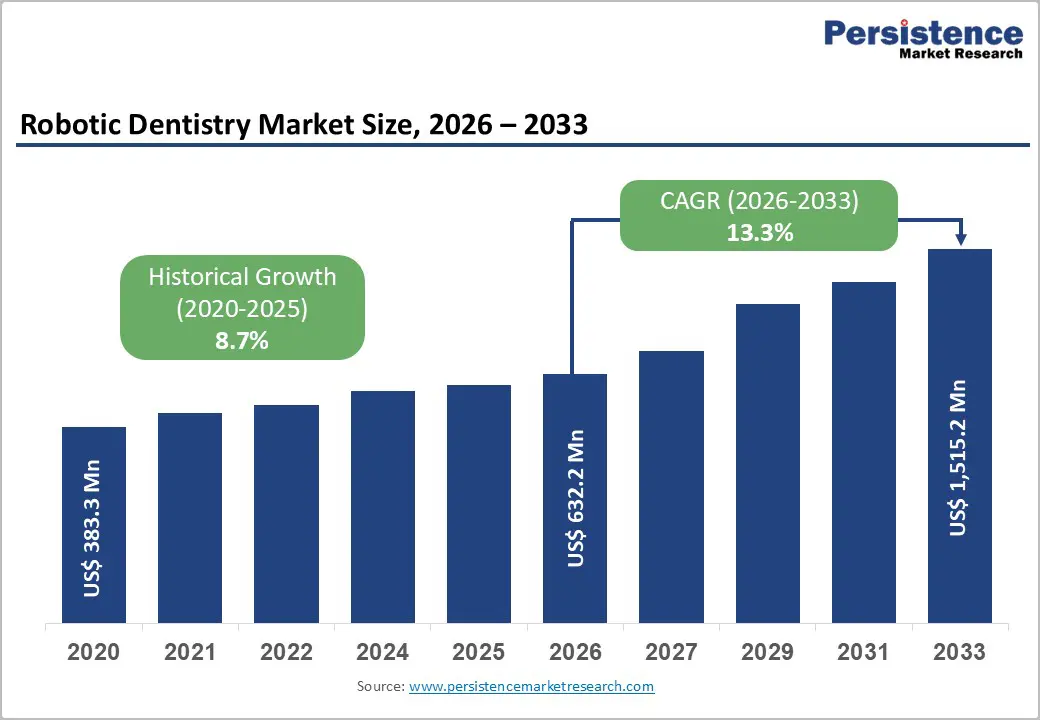

The global robotic dentistry market size is expected to be valued at US$ 632.2 million in 2026 and projected to reach US$ 1,515.2 million by 2033, growing at a CAGR of 13.3% between 2026 and 2033.

This accelerated growth trajectory reflects the convergence of rising oral disease burden, expanding dental implant volumes, and rapid digitalization of dental practices, which together are making robotic assistance increasingly attractive for precision-critical procedures such as implantology and oral & maxillofacial surgery. The market is further strengthened by clinical evidence demonstrating that robot-guided systems can significantly improve accuracy, reduce chair time, and enable minimally invasive, flapless approaches, thereby enhancing patient outcomes and practice efficiency. As technology matures and costs decline, adoption is expected to broaden from early adopters in large specialty centers toward group practices and progressive general dentists, particularly in regions with high digital dentistry penetration and favorable reimbursement frameworks.

Key Industry Highlights:

- North America is the leading region in the robotic dentistry market, supported by high dental expenditure, early adoption of digital and robotic technologies, dense networks of implant specialists, and clear FDA regulatory pathways that have enabled broad clinical deployment of systems like Yomi®.

- Asia Pacific represents the fastest-growing regional opportunity, with rising oral disease burden, expanding middle-class demand for implants and aesthetic dentistry, and significant investments in advanced dental infrastructure and training across China, India, Japan, and ASEAN markets.

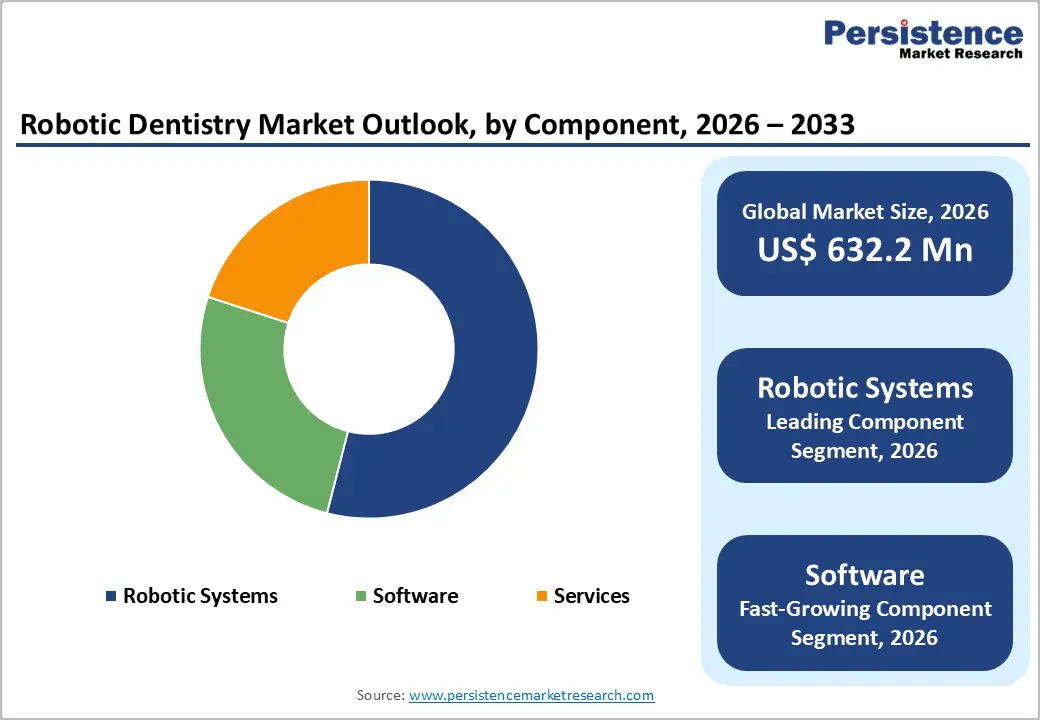

- Robotic Systems are the dominant component segment, accounting for the largest share of market revenues as implant-focused robotic platforms form the technological backbone of robotic dentistry and anchor subsequent sales of software, upgrades, and service contracts.

- Software and AI-enabled planning tools are the fastest-growing segment, as platforms like YomiPlan® AI streamline case planning, automate anatomy segmentation, and deliver recurring revenue models that enhance vendor economics and unlock value for digitally mature dental practices.

- A major opportunity lies in expanding robotic dentistry beyond implantology into full-arch reconstructions, guided bone reduction, and additional indications, particularly within large dental hospitals and academic institutes in high-growth regions seeking to differentiate through precision, efficiency, and minimally invasive care.

| Key Insights | Details |

|---|---|

| Robotic Dentistry Market Size (2026E) | US$ 632.2 million |

| Market Value Forecast (2033F) | US$ 1,515.2 million |

| Projected Growth CAGR (2026 - 2033) | 13.3% |

| Historical Market Growth (2020 - 2025) | 8.7% |

Market Dynamics

Drivers - Growing Burden of Oral Diseases and Implant Procedures

A key growth driver for the robotic dentistry market is the persistent global burden of oral diseases and associated demand for restorative procedures, particularly implants. The World Health Organization (WHO) estimates that oral diseases affect nearly 3.5-3.7 billion people worldwide, making them among the most prevalent non-communicable conditions. Untreated dental caries, periodontitis, and tooth loss frequently necessitate implant-based rehabilitation, and as populations age and retain teeth longer, the volume and complexity of implant cases are rising. Clinical evidence shows that robot-assisted implant placement can achieve sub-millimeter and sub-degree deviations from planned position and angulation, improving safety near anatomical structures and supporting long-term implant survival. These clinical advantages, combined with the high economic cost of implant failures, are encouraging specialized implant centers and oral & maxillofacial surgeons to invest in robotic platforms as a way to standardize quality and differentiate services.

Digital Transformation of Dentistry and Workflow Efficiency Gains

The broader digital transformation of dentistry is another powerful driver accelerating adoption of robotic systems. Analyses of digital dentistry adoption indicate that around 40-53% of dental offices in some markets now use intraoral scanners, while advanced imaging such as CBCT and CAD/CAM systems show annual growth rates of roughly 8-9%, reflecting a strong trend toward integrated digital workflows. Robotic platforms such as Yomi® by Neocis leverage this digital infrastructure by combining CBCT-based planning with haptic guidance, enabling real-time execution of precise surgical plans. Clinical data from multi-site studies report procedure time savings of approximately 45% for partial-arch and up to 80 minutes for full-arch implant cases when using robotic assistance compared with freehand techniques. These efficiency gains translate into higher chair utilization, increased case throughput, and improved patient experience, providing a compelling economic rationale for technology investment by dental hospitals, clinics, and group practices.

Restraints - High Capital Costs and Limited Reimbursement

Despite strong clinical value propositions, high upfront capital costs for robotic systems and uncertain reimbursement pathways remain major barriers to widespread adoption. Dental robots and associated planning software typically require investments that only larger specialty practices, hospital-based oral surgery departments, or corporate dental chains can easily absorb. In many countries, dental services are only partially covered by public or private insurance, and robot-assisted procedures may not receive differentiated reimbursement compared with conventional implant surgeries, limiting immediate financial payback. As a result, smaller independent clinics may delay adoption or rely on referrals to robotically-equipped centers, slowing penetration in some markets.

Training Requirements and Workflow Change Management

Another restraint is the learning curve associated with integrating robotics into existing clinical workflows. Studies of digital technology adoption in dentistry show substantial variation in readiness, with some clinics using up to 20 digital devices while others still rely on purely analog processes. Robotic systems require not only capital investment but also training of dentists, auxiliaries, and support staff, as well as adjustments to scheduling, case planning, and patient communication. Concerns about setup time, perceived complexity, and the need for additional education can initially deter adoption, particularly among older practitioners or in regions where digital dentistry is less entrenched.

Market Opportunities

Software and AI-Driven Planning as a High-Growth Revenue Stream

A major opportunity in robotic dentistry lies in the software layer, particularly AI-enabled planning platforms, workflow automation, and cloud-based analytics. Next-generation solutions such as YomiPlan® AI are being designed to automatically segment critical anatomical structures from CBCT scans and streamline implant planning, significantly reducing preoperative time for clinicians. As robotics platforms proliferate, recurring revenues from software licenses, upgrades, and data-driven decision-support tools are expected to grow faster than hardware alone, mirroring trends seen in other surgical robotics domains. Vendors can also leverage aggregated and de-identified procedural data to refine algorithms, improve case selection guidance, and provide benchmarking dashboards that help practices optimize utilization and clinical outcomes. This software-centric expansion underpins the expectation that the software segment will be the fastest-growing component of the market during the forecast period.

Expansion into New Clinical Indications and Emerging Markets

Robotic dentistry vendors are also actively extending indications beyond single-tooth implants to complex full-arch reconstructions, guided bone reduction, and potentially future applications in endodontics or orthognathic procedures. The U.S. Food and Drug Administration (FDA) 510(k) clearances for robotic-guided bone reduction and edentulous full-arch implant protocols have already broadened the clinical utility of systems like Yomi®, with clinical studies reporting average full-arch surgery times as low as 21 minutes in some settings. At the same time, emerging markets in the Asia Pacific and parts of Latin America are investing in advanced dental infrastructure, driven by a rising middle class, medical tourism, and public awareness of oral health. As costs decline and training hubs are established, manufacturers have the opportunity to deploy scalable robotic solutions tailored to high-volume implantology centers and university hospitals in these regions, unlocking substantial long-term demand.

Category-wise Analysis

Component Insights

By component, robotic systems constitute the leading segment, representing 5.4% share in 2025, reflecting the capital-intensive nature of hardware deployments and the dominance of implant-focused robotic platforms. Systems such as Yomi® integrate robotic arms, haptic interfaces, and navigation hardware that enable rigid instrument guidance relative to the preoperative plan, which is essential for achieving the high accuracy and consistency documented in clinical literature. Early adopters, primarily implantology centers, oral & maxillofacial surgery departments, and large multi-chair clinics, focus initially on acquiring hardware to establish robotic capabilities, after which they layer on software modules and service contracts. Over the forecast period, the installed base of robotic systems will form the foundation for recurring revenues from software updates, AI-enabled planning tools, and maintenance services.

Application Analysis

Within applications, Implantology is the clear leading segment, accounting for an estimated 60% or more of robotic dentistry procedures in 2025, as nearly all commercially available dental robots today are optimized around implant placement workflows. The precision requirements of implant surgery, especially near nerves, sinuses, and in full-arch restorations, align well with robotic advantages. Prospective clinical studies of robot-guided implant placement show mean angular deviations often below 1.5 degrees and depth deviations under 0.2 mm, outperforming freehand techniques and even many static guides. Additionally, the ability to facilitate minimally invasive, flapless approaches can reduce patient morbidity and accelerate recovery, which is particularly valuable for older or medically complex populations requiring implants. As awareness of these benefits grows among both clinicians and patients, implantology is expected to remain the anchor application for robotic dentistry.

End-user Insights

By end user, dental hospitals & clinics (including large specialty practices and group practices) are the dominant segment, likely capturing over 70% of robotic dentistry revenues in 2025, given their role as primary providers of surgical dental care. These institutions typically handle higher volumes of complex implant and oral surgery cases, possess the capital budgets required for technology investments, and can more easily integrate robotic workflows into multi-disciplinary care teams. Academic centers and teaching hospitals are also key early adopters, using robotic systems to train residents and conduct clinical research, but their share of total commercial procedures remains smaller compared with private clinics. Over time, consolidation in the dental sector and the rise of corporate dental service organizations are likely to further concentrate robotic systems in networked clinic groups that can standardize protocols and leverage economies of scale.

Regional Insights

North America Robotic Dentistry Market Trends and Insights

North America is the leading regional market in robotic dentistry, accounting for roughly 39-42% of global revenues in the mid-2020s, driven by high healthcare expenditure, rapid adoption of digital technologies, and the presence of pioneering companies such as Neocis. The United States hosts the majority of installed dental robots, supported by a dense network of oral & maxillofacial surgeons, implantology centers, and group practices that have both the patient volume and capital budgets to justify investment. Regulatory clarity from the U.S. Food and Drug Administration (FDA)-including multiple 510(k) clearances for robotic implant systems and expanded indications such as full-arch treatment and guided bone reduction has further de-risked adoption and reinforced clinician confidence.

The region also benefits from a strong innovation ecosystem that integrates robotics with digital imaging, AI-driven planning, and practice management software. Clinical studies carried out in North American centers have documented substantial gains in accuracy and efficiency with robotic assistance, including procedure time reductions of up to 45% in partial-arch and 80 minutes in full-arch implant cases. These outcomes align with broader trends in digital dentistry adoption, where a significant share of the U.S. dentists already use intraoral scanners, CBCT, and CAD/CAM solutions, creating a natural foundation for robotics integration. As reimbursement frameworks slowly evolve and more group practices seek differentiation in competitive urban markets, North America is expected to maintain its leadership position.

Asia Pacific Robotic Dentistry Market Trends and Insights

Asia Pacific is the fastest-growing region in the robotic dentistry market, supported by a large and aging population, rising disposable incomes, and rapid expansion of private dental clinics and hospital networks in China, Japan, India, and ASEAN countries. Oral disease prevalence is high in many of these markets, and growing middle-class awareness of aesthetics and oral function is fueling demand for implants, orthodontics, and complex restorative procedures. Governments and private investors are putting capital into advanced medical infrastructure, with dental wings of tertiary hospitals and high-end clinics increasingly adopting digital imaging and CAD/CAM systems, laying the groundwork for robotics.

Manufacturing and cost advantages in the Asia Pacific, combined with thriving dental tourism hubs in countries such as India and Thailand, offer additional incentives for clinics to differentiate with state-of-the-art surgical technologies, including robotics. Japan’s strong robotics industry and high technology readiness make it a natural incubator for advanced dental applications, while China’s large patient pool and policy interest in high-end medical devices create long-term potential for localized robotic dentistry solutions. As training programs, reference centers, and regional partnerships develop, the region is expected to post double-digit growth rates and gradually narrow the adoption gap with North America and Europe.

Competitive Landscape

The robotic dentistry market is characterized by increasing competition driven by rapid technological advancements and the growing adoption of digital dentistry solutions. Market participants are focusing on developing advanced robotic platforms that enhance procedural accuracy, reduce surgical time, and improve patient outcomes. Companies are investing significantly in research and development to integrate artificial intelligence, 3D imaging, and real-time navigation technologies into robotic systems. Strategic collaborations with dental clinics, hospitals, and research institutions are also becoming common to expand clinical adoption.

Key Developments:

- In November 2025, Neocis launched its next-generation AI-powered dental robotic platform, Yomi S, designed for dental implant surgery. The system received FDA clearance and was developed to improve surgical precision, workflow efficiency, and patient outcomes.

- In September 2025, Tajmeel Clinic launched a new dental innovation centre called SmileVerse in Abu Dhabi that integrated robotics, artificial intelligence, and advanced digital workflows into everyday dental care to enhance precision, comfort, and efficiency.

Companies Covered in Robotic Dentistry Market

- Neocis

- Dentsply Sirona

- Planmeca

- Institut Straumann AG

- Zimmer Biomet

- 3Shape

- Carestream Dental

- Ivoclar Vivadent

- Cybermed

- Vatech

- Hiossen

- Theranautilus

Frequently Asked Questions

The global robotic dentistry market size is expected to reach about US$ 632.2 million in 2026, supported by rising implantology volumes, digital workflow adoption, and growing acceptance of robot-assisted dental surgery among clinicians and patients.

Demand is driven by the high global burden of oral diseases, growth in dental implant procedures, and documented benefits of robotic systems in improving surgical accuracy, reducing chair time, and enabling minimally invasive, digitally planned treatment workflows in modern dental practices.

North America currently leads the robotic dentistry market, underpinned by strong healthcare expenditure, rapid digital dentistry adoption, a high concentration of implant specialists, and clear FDA regulatory pathways that have enabled early commercialization of systems such as Yomi®.

A key opportunity lies in AI‑enabled software and planning platforms, as vendors develop tools like YomiPlan® AI to automate anatomy segmentation, optimize implant planning, and provide data-driven decision support, creating high-growth, recurring software revenue streams.

Major players include Neocis, Dentsply Sirona, Planmeca, Institut Straumann AG, Zimmer Biomet, 3Shape, Carestream Dental, Ivoclar Vivadent, Cybermed, Vatech, Hiossen, Theranautilus, X‑Nav Technologies, and Align Technology, Inc., many of which focus on integrating robotics with broader digital dentistry ecosystems.