- Sensors & Controls

- Robotic Refueling System Market

Robotic Refueling System Market Size, Share, Trends, Growth, and Forecasts (2025 - 2032)

Robotic Refueling System Market by Fuel Pumped (Gasoline, Natural Gas, Petrochemicals), by Payload-carrying Capacity (Up to 50 kg, 50.01–100 kg, 100.01–150 kg), by Frequency (Less than 1 GHz, 1 GHz to 6 GHz, More than 6 GHz), by Vertical (Mining, Automobile, Oil & Gas, Aerospace, Military & Defense, Warehouse & Logistics, Marine & Shipping, Construction), and Regional Analysis

Robotic Refueling System Market Size and Forecast Analysis

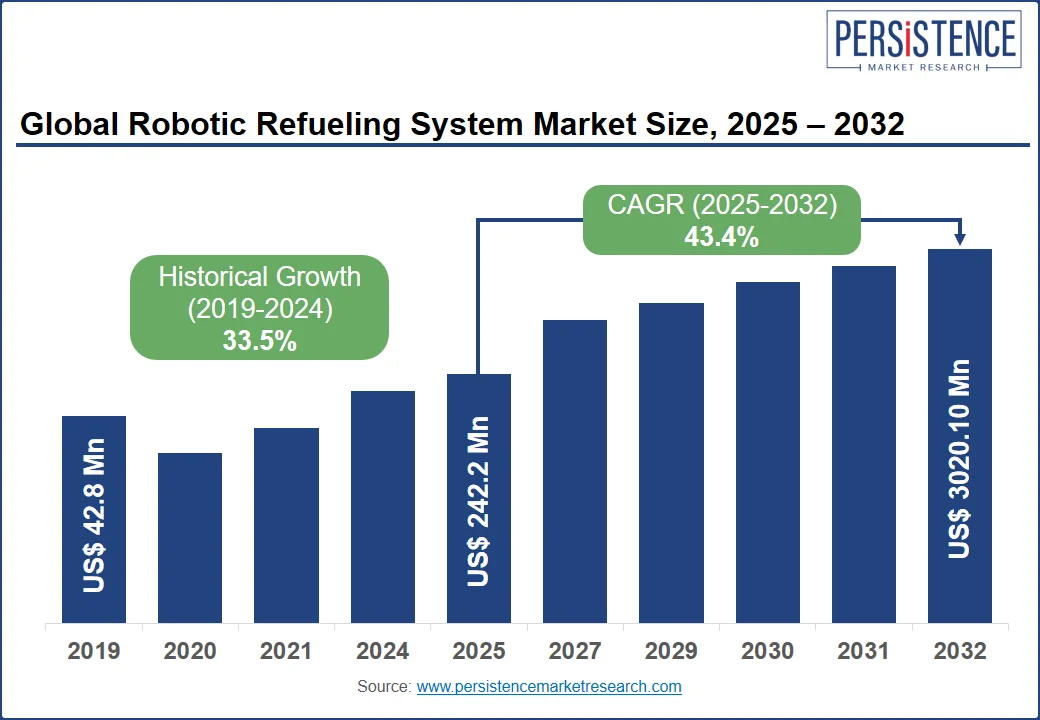

According to Persistence Market Research, robotic refueling systems sales are expected to reach US$ 242.2 million by 2025. A recent report estimates that robotic refueling systems will reach US$ 3,020.10 million by 2032, with a 43.4% CAGR.

Robotic refueling systems are continuously evolving as robotics and automation advance. Sensor technologies, navigation autonomy, fueling mechanisms, and integration with other robotic systems have all improved over the past few years. The cost-effectiveness, versatility, and adaptability of robotic refueling systems may increase as the technology matures.

Increasing interest in scientific research-based projects and studies has led to a constant demand for these robots in the marketplace. The increasing use of technologies and the availability of advanced sensors has contributed to the growth of the market.

For instance, limited initial capabilities were demonstrated for the U.S. Army Aviation and Missile Research, Development, and Engineering Center to test that theory. The demonstration introduced the Autonomous & Robotic Remote Refueling Point, or AR3P, developed by the Center's Aviation Development Directorate and Operational Energy Lab. An autonomous robot refueling operation was demonstrated to stakeholders as a proof-of-concept and a potential material set of solutions.

| Report Attributes | Details |

|---|---|

|

Robotic Refueling System Market Size (2025) |

US$ 242.2 Million |

|

Robotic Refueling System Market Value (2032) |

US$ 3,020.10 Million |

|

Robotic Refueling System Market CAGR (2025 to 2032) |

43.4% |

2019 to 2024 Robotic Refueling System Market Outlook Compare to 2025-2032 Forecast

Persistence Market Research (PMR) estimates robotic refueling system sales will grew by 49.6% between 2019 and 2024. According to analysts, global sales will grow by 40.8% between 2025 and 2032.

There's growing interest in robotic refueling systems for commercial uses such as transportation, mining, agriculture, and construction has seen a rise in recent years. Commercial sectors have begun to use them even though they were originally designed for industrial and military purposes.

Robotic refueling has a global potential, not just limited to specific regions. In the future, the market is expected to experience significant growth worldwide as automation and efficient fueling solutions become more prevalent across industries.

As industries in these regions modernize and automate rapidly, emerging economies present significant opportunities in the future. Diverse industries will benefit from the market's continued growth as it offers numerous benefits, including cost savings, safety, and efficiency. A robotic refueling system can improve efficiency and reduce operational costs in industries where large fleets of vehicles and equipment require regular refueling.

Key Market Trends for Robotic Refueling System Market

- With the advancement of technology and the demand for Industry 4.0, robotic refueling systems are becoming more popular in the market.

- Aerospace projects are fueling the demand for robotic refueling systems with a growing number of projects

- As investments in research and development increase, and emerging markets grow, demand for robotic refueling systems is on the rise.

- Robotic refueling systems are in high demand due to the growth of automation in the space industry and the demand for space-related projects.

- With rising safety concerns and growing demand for autonomous vehicles, the market is expected to expand.

- As environmental concerns grow and artificial intelligence is used to develop these systems, the demand will continue to grow.

- Increasing demand for advanced sensors and cost-effective solutions is expected to drive the market upward.

- Low operational costs, greater flexibility, and increased security will result in an increase in fuel dispensing demand.

Country-wise Insights

How much Revenue can the Robotic Refueling System Market Generate in North American Region?

Market Share for Robotic Refueling Systems in North America is Expected to Increase

| United States (2025-2032) | Projected Market Value |

|---|---|

|

Robotic Refueling System in United States Market Size (2025) |

US$ 13.5 million |

|

Robotic Refueling System in United States Market Size (2032) |

US$ 368.3 million |

|

Robotic Refueling System in United States Market (CAGR) |

39.2% |

The North American robotic refueling system market is expected to dominate the global market. In 2032, PMR projects the North American robotic refueling system market to reach US$ 634.95 million.

The growth of the IT sector and the adoption of technologies are expected to drive the demand for robotic refueling systems. Over the next few years, the demand for advanced technologies and autonomous vehicles is expected to grow.

The rising demand for space technologies and products will lead to an increase in the number of robots on the market. Robotic refueling systems are growing in popularity in developed countries such as the United States and Canada due to improved infrastructure as well as the need for more efficient and reliable refueling solutions.

Military and defense industries will significantly adapt these robots in the coming years, driving sales in the market. RE2 Robotics has also been awarded contracts by the US Army to develop autonomous ground vehicle refueling (AGVR) prototypes. As a whole, North America has been a key region for the growth and adoption of robotic refuelers in the market

Is the Robotic Refueling System Projected to Grow Significantly in Asia Pacific Region?

Government Initiatives and Programs to Promote Robotic Refueling System Market

Projected Market Value (2032):

| Countries | Details |

|---|---|

| China | US$ 673.6 million |

Projected CAGR (2025 to 2032):

| Countries | Details |

|---|---|

| China | 42.7% |

Projected Market Value (2032):

| Countries | Details |

|---|---|

| South Korea | US$ 161.9 million |

Projected CAGR (2025 to 2032):

| Countries | Details |

|---|---|

| South Korea | 41.3% |

Global robotic refueling system sales are expected to be dominated by the Asia Pacific region over the forecast period. Mining and marine & shipping industries have grown substantially in these regions, increasing demand for robotic refueling systems.

In the Asia Pacific, sales of robotic refueling systems are expected to reach US$ 1,295.4 million by 2032. Emerging markets like Asia-Pacific are expanding their fuel-handling infrastructure, increasing demand for robotic refueling systems.

China and India's growing shipping and logistics industries will result in more demand in the future. In addition, safety concerns of workers and the high demand for mining activities will likely increase demand in the coming years for robotic refueling systems.

Refueling operations are also increasingly being carried out by drones, especially in the aviation industry. Moreover, robotics companies and energy firms are collaborating more frequently in the region, which should fuel the market's growth. Overall, robotic refueling systems are increasingly being adopted and growing in the Asia Pacific region.

Category-wise Insights

How do Robotic Refueling Systems Fuel Pumps Expect to grow in the Future?

The Market for Robotic Refueling Systems is Expected to be Dominated by Gasoline in the Near Future

Based on the robotic refueling system fuel pumped segment is classified into gasoline, natural gas, petrochemicals, and others. Sales of gasoline are expected to increase over the next few years. By 2032, the market is predicted to grow at a CAGR of 40.7%. The increasing number of gasoline platforms and the use of vehicles is expected to increase demand for robotic refueling systems.

Refueling operations in the military can be challenging and risky, especially in remote or hostile environments. Using robotic refueling systems, military vehicles, aircraft, and other equipment can be refueled reliably and efficiently. As a result of the deployment of these systems, logistical capabilities can be enhanced, manpower requirements can be reduced, and operational readiness can be improved.

Fully automated robotic refueling systems are offered by Autofuel and Green Fuel Technologies Corp. Using robots to refuel vehicles eliminates the need for human attendants and reduces fueling time. Asia Pacific gas stations are only beginning to install robotic refueling systems, but more stations are likely to install these systems after testing and commissioning. Though robotic refueling systems are still relatively new, they are a growing trend that is likely to gain traction in the future.

Which Application will drive the Robotic Refueling System Market in the Future?

The Mining Industry will dominate the Market for Robotic Refueling Systems

The mining robotic refueling market is predicted to dominate over the next few years. Mining is expected to grow at a CAGR of 40.6% over the next few years. Future growth of robotic refueling systems will be driven by increased investment in the mining industry.

As autonomous haulage trucks are increasingly adopted, the robotics refueling market has surged. With these systems, mining vehicles such as trucks, excavators, and other heavy equipment can be refueled with less risk, increased productivity, and reduced downtime.

Using a robotic refueling system can greatly increase the efficiency, safety, and speed of the refueling process. A reduction in costs and improved operational efficiency can be achieved through the use of this technique. It is expected that the market for robotic fueling systems will continue to grow as several companies develop systems specifically for mining. For instance, in July 2020, BHP Mitsubishi Alliance (BHA) committed approximately US$ 68 million to autonomous hauling at the Daunia coal mine.

Competitive Landscape

Throughout the years, robotic manufacturers have developed new products as well as incorporated innovations and modified existing products in order to meet the requirements of a variety of applications. As one of their key strategies, robotic refueling system vendors also increase their service centers and develop customer relationships.

- In May 2023, new docking systems for the International Space Station will be tested. ISS uses free-flying robotic assistants called Astrobees. There are three cube-shaped robots roaming the station including Honey, Queen, and Bumble. Among the duties they perform are helping crew members complete ISS National Laboratory-sponsored experiments to test new technology that may aid future space missions. In-orbit manufacturing processes, satellite servicing, and orbital refueling all require this technology.

- In May 2023, Thales Alenia Space, Italy's largest space company, announced that 235 million euros ($256 million) of pandemic relief funds will be awarded for an experiment to demonstrate orbital servicing in 2026. In addition to a dexterous robotic arm and test capabilities, the servicer will be able to perform refueling, component repairs, orbital transfers, and atmospheric reentry in 2026.

Companies Covered in Robotic Refueling System Market

- Scott Technology

- Fuelmatics AB

- Rotec Engineering B.V.

- Neste Oyj

- Shaw Development LLC

- Plug Power Inc.

- Aerobotix

- Airbus S.A.S

- The Boeing Company

- ABB Group

- KUKA

- Simon Group Holdings

- FANUC Corporation

- Husky Corporation

Frequently Asked Questions

The market is expected to reach US$ 242.2 million by 2025.

The market is projected to grow to US$ 3,020.10 million by 2032.

The market is expected to grow at a CAGR of 43.4% during this period.

They are automated systems designed to refuel vehicles or equipment without human intervention, using robotics and advanced sensors.

Growth is driven by advancements in automation, sensor technologies, and increased demand for scientific research-based robotic projects.