- Automation & Robotics

- Robotic Grippers Market

Robotic Grippers Market Size, Share, and Growth Forecast, 2026 - 2033

Robotic Grippers Market by Product type (Mechanical Grippers, Vacuum Grippers, Magnetic Grippers, Soft or Compliant Grippers, Hydraulic Grippers, and Miscellaneous (Other types)), Application (Pick and Place, Assembly and Installation, Material Handling and Transfer, Machine Tending, Packaging and Palletizing, Inspection and Sorting, and Misc.) , Industry (Automotive and Transportation, Electronics and Semiconductor, Food and Beverage and Packaging, Logistics, Medical Devices, Metal and Fabrication, Consumer Goods, Agriculture, and Misc.) and Regional Analysis for 2026 - 2033

Robotic Grippers Market Size and Trends Analysis

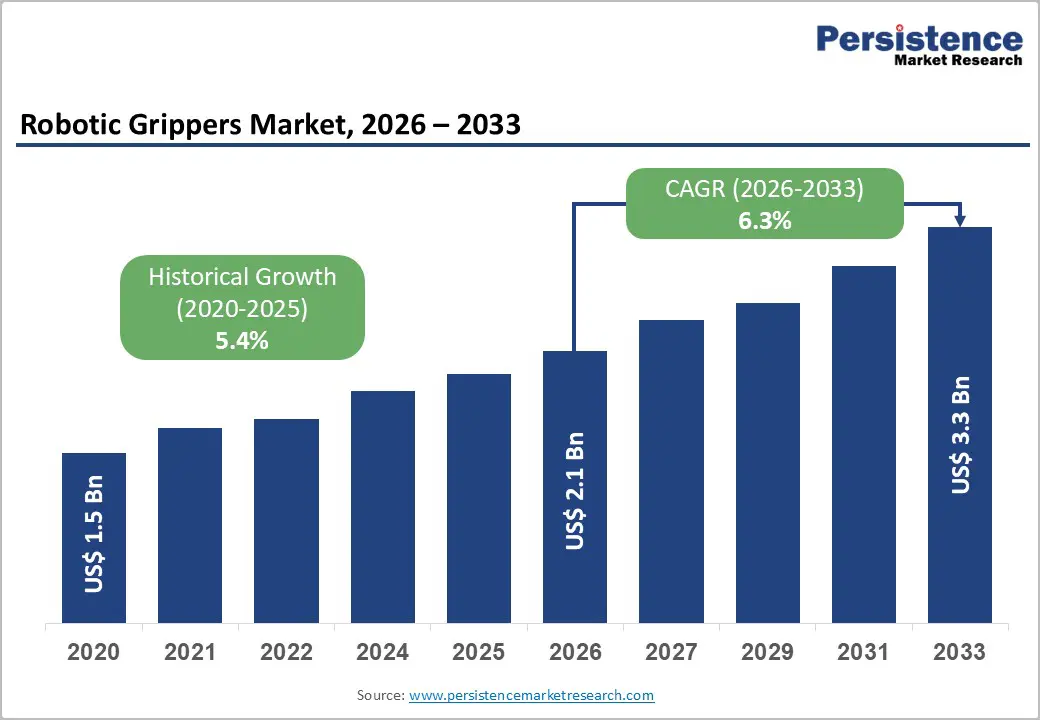

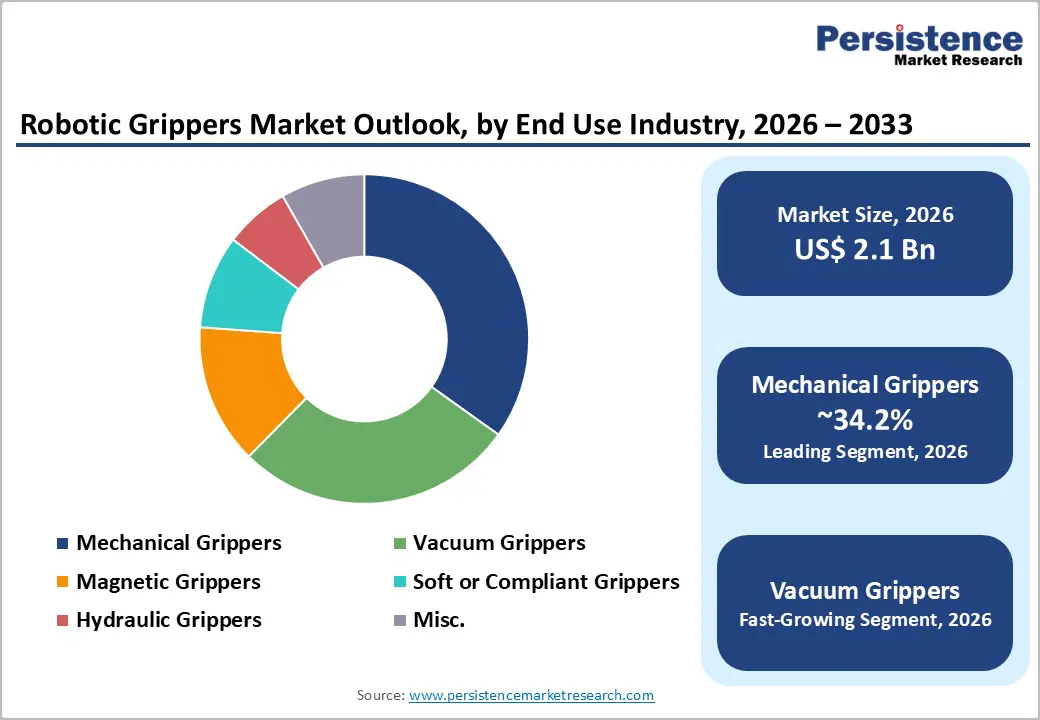

The global robotic grippers market size is likely to be valued at US$ 2.1 billion in 2026 and is projected to reach US$ 3.3 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

This trajectory reflects sustained adoption of industrial automation across automotive assembly lines, semiconductor fabrication, and food packaging operations worldwide. Key catalysts include CHIPS Act investments exceeding US$ 500 billion in U.S. semiconductor capacity expansion and EU semiconductor market growth of 12.3 percent in 2022. B2B e-commerce structural transformation, with a CAGR of 14.5 percent from 2017 to 2026 and a gross merchandise value increase from US$ 9,837 billion to US$ 36,163 billion, amplifies logistics automation requirements that support precise gripper deployment. These macro trends position robotic grippers as mission-critical components within precision manufacturing ecosystems.

Key Industry Highlights:

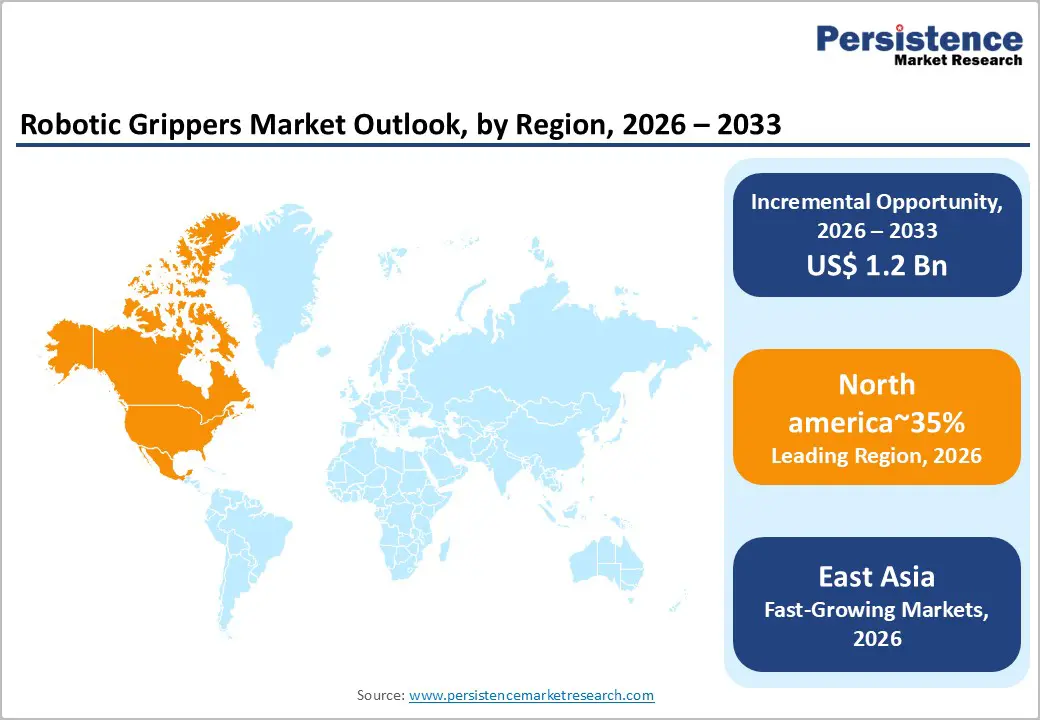

- Regional Leadership: North America leads the global robotic grippers market with a 35% share, driven by CHIPS Act incentives, EV platform assembly, and the expansion of Intel, TSMC, and Samsung fabs, which require cleanroom-compatible grippers.

- Emerging East Asian Hub: East Asia holds a 20 percent share, supported by semiconductor dominance, advanced automotive robotics, energy-efficient SMA grippers, and government automation mandates such as Made in China 2025.

- European Market Scenario: Europe accounts for 25% share, fueled by automotive premiumization, food and beverage processing automation, IP69K hygiene standards, and EU Machinery Directive compliance for collaborative robots.

- Leading Product: Mechanical Grippers dominate with 34.2% share, preferred for robustness across automotive stamping lines and metal fabrication operations, offering high repeatability and precision for heavy payload handling.

- Fastest-Growing Product: Soft and vacuum grippers are the fastest-growing, driven by delicate object manipulation needs in food, agriculture, medical, and semiconductor applications, and energy-efficient, lightweight automation.

- Leading End-user: Automotive commands a 22% share, driven by EV assembly, handling of lightweight composites, and adoption of multi-finger tooling for chassis, battery, and body-in-white applications.

| Key Insights | Details |

|---|---|

| Robotic Grippers Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 3.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Dynamics

Drivers - Semiconductor Manufacturing Capacity Expansion and Precision Handling Requirements

Semiconductor fabrication facilities require robotic grippers capable of handling silicon wafers, microchips, and delicate components with sub-micron precision to prevent contamination and yield loss during high-volume production cycles. The U.S. CHIPS Act catalysed over US$500 billion in private semiconductor investment across 28 states by 2025, targeting a 200% expansion in fabrication capacity by 2032 and a tripling of the domestic output share from 10 percent to 14 percent of global capacity. Leading-edge logic capacity is shifting from near-zero to a meaningful global share, necessitating grippers that meet Class 1 standards and support 300 millimetre wafer transport protocols.

Global semiconductor sales reached US$75.3 billion in November 2025 alone, representing 29.8 percent year-over-year growth, driven by AI data centers and automotive electronics. The robotic grippers market experiences direct demand as new fabs integrate end-to-end automation from wafer handling to advanced packaging. Gripper OEMs supplying vacuum and soft grippers certified for semiconductor protocols capture sustained revenue as Intel, TSMC, and Samsung expand their North American and European facilities to meet the processing requirements of billions of transistors per second. Cleanroom-compatible mechanical grippers supporting FOUP (Front Opening Unified Pod) transfer protocols are becoming procurement standards for these capital-intensive greenfield projects.

Automotive Electrification and Lightweight Materials Assembly Automation Mandates

Automotive OEMs are increasingly deploying robotic grippers optimised for handling lightweight composite materials, battery modules, and precision electronic components essential to electric-vehicle platform assembly. BMW Group's May 2024 expansion of 3D-printed bionic grippers across its Landshut and Munich plants achieved a 30 percent weight reduction while handling CFRP roofs, floor assemblies, and door components, underscoring the grippers' role in EV structural complexity.

Global EV production has 3 times the semiconductor content per vehicle compared with internal combustion engines, requiring grippers to manage thermal management modules, power electronics, and high-voltage interconnects. The robotic grippers market benefits as OEMs standardise gripper interfaces compatible with ISO 10218 collaborative robot safety standards across global manufacturing footprints. Destaco's June 2025 eRDH Series Electric Parallel Gripper launch targets automotive applications with four teachable sensors and selectable grip configurations, reflecting OEM requirements for flexible end-of-arm tooling supporting multiple vehicle platforms. Regional regulatory mandates for CO2 emissions reduction through lightweighting are accelerating gripper adoption, as OEMs replace manual handling with precision automation while maintaining 98 percent uptime across 24/7 production schedules.

Food Processing Hygiene Standards and High-Speed Packaging Line Integration

Regulatory bodies worldwide enforce stringent hygiene protocols for food-contact grippers, driving adoption of IP69K-rated, corrosion-resistant designs compatible with frequent washdown cycles. Festo's December 2025 HPSX Universal Adaptive Gripper launch utilises a food-grade silicone construction that meets hygienic requirements for food, pharmaceuticals, and cosmetics, while enabling multiple picks per second. EU food safety regulations mandate gripper materials that prevent microbial contamination during high-velocity packaging operations processing 10,000+ units per hour.

The robotic grippers market captures value as food processors integrate grippers that support primary, secondary, and tertiary packaging across flexible pouch formats, flow wrap configurations, and case-erecting systems. OnRobot's February 2021 VGP20 electric vacuum gripper delivers 90 percent operating cost savings compared with pneumatic alternatives while handling diverse product geometries, including irregular produce and consumer packaged goods. Clean-in-place compatibility and EHEDG European Hygienic Engineering and Design Group certification become procurement gating factors as multinational food companies standardise gripper specifications across global plant networks.

Restraint - High Precision Gripper Certification Costs and Extended Validation Cycles

Cleanroom certification for semiconductor-compatible grippers requires ISO Class 1 particle validation, which involves 6-12-month qualification cycles and costs $250K-$500K per gripper family across multiple OEM validation sites. Automotive OEMs mandate PPAP Level 3 approval processes that span 9-18 months, with destructive testing protocols consuming 20-30 prototype units per configuration.

Food/pharma applications require 3A sanitary standards and EHEDG Type EL Class I validation, which increases compliance costs by 3-5x compared with industrial grippers. These certification barriers delay market entry for new competitors and increase COGS by 25-35% for compliant designs, thereby constraining the addressable market for emerging suppliers lacking established qualification frameworks.

Supply Chain Dependencies on Rare-Earth Materials and Precision Components

Gripper actuators rely on neodymium magnets and shape memory alloys, subject to China's dominant supply chains, exhibiting 40 to 60 percent price volatility during geopolitical disruptions. Vacuum gripper venturi systems require specialised FKM seals, with 12- to 16-week lead times during capacity constraints. Soft-gripper silicone compounds are facing raw material shortages, affecting 20 to 25 percent of production schedules. These structural dependencies amplify 15 to 20 percent cost inflation during supply disruptions while constraining scalability for high-volume automotive and semiconductor programs requiring JIT delivery protocols.

Opportunity - Collaborative Robot (Cobot) Gripper Standardisation and Plug-and-Play Integration Platforms

Cobots are the fastest-adopting robot category, with Universal Robots commanding a 60 percent market share, creating demand for standardised gripper interfaces that enable rapid end-of-arm tooling exchange across multiple applications. SMC's March 2024 LEHR series electric grippers feature plug-and-play URCap software integration with Universal Robots, enabling 60-140 N gripping force configurations that can be deployed in under 30 minutes. OnRobot's April 2024 2FG14/3FG25 launch offers 25 kg payload capacity and universal mounting plates that support dozens of cobot models. The robotic grippers market captures immediate revenue as SMEs adopt gripper as a service models, leasing pre-certified end effectors with UR plus ecosystem certification.

This standardisation opportunity extends to software-defined grippers incorporating digital twin integration, Universal Robots and Siemens' January 2026 CES palletising system, and tactile sensor feedback, with Robotiq's January 2026 TSF 85 launch. Gripper OEMs developing ISO 9409 1 50 4 M6 compliant quick-change plates with proprietary force to torque monitoring, achieve 80 percent faster deployment versus custom integrations. Regional cobotics training centres and distributor demo programs accelerate adoption, as end users prioritise ROI within 12 months for flexible automation cells handling mixed-SKU palletising, machine tending, and kitting operations.

Soft Robotics Convergence with Agricultural Harvesting and Medical Applications

Soft grippers address unmet needs in delicate object manipulation across agriculture, JAIST, December 2025, ROSE gripper for strawberries and mushrooms, and medical device handling, MIT and Stanford, December 2025, vine-inspired gripper. These actuators mimic biological compliance using pneumatic silicone chambers, achieving gentle grasp forces below 0.5 N while supporting 15- to 20-kilogram payloads. Shape-memory alloy grippers at Saarland University, March 2025, consume 90 percent less energy than pneumatics, enabling cordless cobot deployments. The Robotic Grippers Market benefits from USDA ag tech grants and NIH medical robotics funding, which target 25 to 35 percent labor displacement in harvesting and sterile packaging.

Agricultural ROI accelerates as soft grippers achieve 95 percent pick success rates across irregular produce geometries, validated by KIMM's October 2022 elephant trunk gripper handling needles to boxes. Medical applications demand ISO 13485 certification and biocompatible materials, creating 3 to 5 times margin premiums versus industrial grippers. Government Farm-to-Table automation subsidies and hospital robot leasing programs provide immediate procurement funding for IP69 K-rated soft grippers supporting pharma primary packaging and surgical instrument handling, positioning compliant robotics as a dual-use technology that spans food safety and healthcare compliance requirements.

Category-wise Analysis

Product type Insights

Mechanical grippers are the dominant product category in the robotic grippers market, commanding 34.2% of the market in 2026 due to their robustness across automotive stamping lines and metal fabrication operations handling steel castings up to 500 kilograms. Parallel jaw configurations deliver consistent clamping force across a wide range of part geometries, with servo-electric actuation replacing pneumatics in high-duty-cycle applications. Kurt Workholding's May 2021 RV36 Quick Change Gripper features a patent-pending two-finger design that enables end effector exchange without body replacement. The 34.2 percent share reflects standardisation across Tier 1 suppliers, prioritising repeatability within ±0.1 millimetre for precision assemblies.

Vacuum grippers accelerate adoption in electronics assembly and packaging operations, handling non-porous surfaces at high takt times. OnRobot's VGP20 achieves a 20 kg payload with 90 percent cost savings versus pneumatics, while SCHUNK PPD, November 2023, enables force-to-speed adjustment via IO-Link for variable workpiece proximity. Vacuum technology supports wafer handling in Class 1 cleanrooms and primary food packaging that meets IP67 washdown requirements, positioning vacuum grippers for disruptive growth across the semiconductor back end and consumer packaged goods.

Industry Insights

Automotive commanding 22% of market share in 2026, Automotive commands leadership through high-volume welding cells and final assembly lines requiring multi-finger tooling for door panels, chassis components, and battery modules. In May 2024, BMW's 3D-printed bionic grippers achieve 30 percent weight savings when handling CFRP structures, while the Destaco eRDH Series, in June 2025, offers four teachable sensors for precision part location. The 22.0 percent share reflects OEM consolidation around qualified suppliers that meet IATF 16949 certification across global stamping, body-in-white, and powertrain assembly.

Food and beverage production accelerates with IP69K hygienic grippers, enabling primary packaging of irregular produce and ready meals. Festo HPSX, December 2025, handles multiple picks per second with food-grade silicone, while Destaco eRDH targets packaging lines with built-in jaw locking. Primary drivers include labour shortages across the dairy, bakery, and beverage sectors, which require 24-hour to 7-day operations with zero contamination risk, positioning food grippers for outsized growth relative to capital-intensive automotive applications.

Regional Insights

East Asia Robotic Grippers Market Trend

East Asia maintains 20% share through semiconductor dominance and automotive robotics leadership. Korea Institute, KIMM, launched the elephant trunk gripper in October 2022, combining pinch to suction mechanisms, while the JAIST ROSE gripper, in December 2025, addresses agricultural labour shortages with wrinkling-based grasping. China's semiconductor consumption drives procurement of vacuum grippers for wafer-level packaging, supported by the Made in China 2025 automation mandates. Japan's robotics leadership emphasises energy-efficient SMAs, Saarland and Hannover Messe collaboration, March 2025, consuming 90 percent less energy. Regulatory convergence around ISO 10218 facilitates cross-border OEM standardisation. Investment flows to cobot ecosystems with UR and Siemens digital twin palletising, CES January 2026, targeting logistics automation.

North America Robotic Grippers Market Trends

North America commands 35% of global robotic grippers through the CHIPS Act-fueled semiconductor resurgence and automotive electrification. U.S. fabrication capacity is projected to expand by 200 percent by 2032, with 500 billion dollars in private investment creating cleanroom gripper demand across Intel's Ohio, TSMC's Arizona, and Samsung's Texas fabs that process leading-edge logic and DRAM packaging. Automotive OEMs deploy 3D-printed bionic grippers; BMW Landshut and Munich expansion, May 2024; handling CFRP EV structures.

Regulatory tailwinds include OSHA collaborative robot standards that enable cobot deployment across SMEs. Investment trends favor venture-backed soft robotics, MIT and Stanford vine gripper, December 2025, targeting agricultural harvesting with USDA grant support. The competitive landscape is consolidated around OnRobot, Destaco, and SCHUNK North America, which supply UR+-certified tooling.

Europe Robotic Grippers Market Trends

Europe accounts for 25% through automotive premiumization and food-processing automation. EU semiconductor revenues grew 12.3% in 2022 to 51 billion euros, driving demand for precision grippers despite a 9.3% global market share. BMW 3D-printed grippers, May 2024, reduce CO2 emissions by 30 percent across Munich and Landshut, while Saarland SMA grippers, March 2025, target energy-intensive sectors. EHEDG hygiene standards mandate IP69K food grippers across Nestlé and Unilever packaging lines.

The regulatory framework includes the EU Machinery Directive 2006/42/EC enforcing cobot safety ratings. Investment trends favor Fraunhofer-backed soft robotics and VDA-qualified automotive tooling, with SCHUNK PPD, November 2023, enabling pneumatic retrofits. Competitive dynamics feature German precision engineering leadership.

Competitive Landscape

The global robotic grippers market is fragmented, with numerous players across various segments, including electric, pneumatic, and adaptive grippers. Leading companies such as SCHUNK, Festo, OnRobot, DESTACO, Robotiq, Universal Robotics, Destaco, and Applied Robotics dominate the market by offering innovative solutions tailored to diverse industrial applications. These players provide a wide range of products, from high-precision grippers for the automotive and electronics industries to soft, hygienic grippers for food and pharmaceutical sectors. The market's competitive nature is further driven by technological advancements, such as collaborative grippers and the integration of AI and digital twin technologies by companies like Siemens and Universal Robots. Despite the presence of large players, the market remains open for new entrants, ensuring continuous innovation and a dynamic competitive environment.

Key Developments:

- In January 2026, Universal Robots, Robotiq, and Siemens announced a collaboration to launch a smart palletising system at CES 2026. The system integrates Robotiq's PAL Ready palletising cell with Universal Robots’ UR20 robot arm, alongside Siemens’ Digital Twin Composer software. The system uses real-time digital twins and industrial AI to optimise gripper performance and improve palletising efficiency. The collaboration highlights the power of digital and physical innovation, with Siemens’ Industrial Edge hardware enabling real-time insights and optimisation, leading to improved operational flexibility and ROI.

- In January 2026, Robotiq Inc. launched the TSF-85 tactile sensor fingertips for its 2F-85 Adaptive Gripper, enabling robots to gain a "sense of touch." This innovative tactile sensing technology allows robots to interact more effectively with objects and tasks by providing high-frequency feedback, bridging the gap between AI and physical reality. The TSF-85 builds on years of research and has been deployed in over 23,000 grippers globally, enhancing robots' ability to generalise across diverse environments.

Companies Covered in Robotic Grippers Market

- SCHUNK

- OnRobot

- DESTACO

- Robotiq

- Soft Robotic Inc.

- Universal Robotics

- Applied Robotics

- Cellro B.V.

- Grabit, Inc.

- Festo

- Tünkers

- ATI industrial Automation

- Allegro Hand

- Manic Americas Inc.

- Ixtur

- SoftGripping

Frequently Asked Questions

The global Robotic Grippers Market is projected to be valued at US$ 1.3 Bn in 2026.

The Mechanical Grippers segment is expected to account for approximately 34.2% of the Global Robotic Grippers Market by product type in 2026.

The market is expected to witness a CAGR of 6.3% from 2026 to 2033.

The Robotic Grippers Market is driven by semiconductor manufacturing capacity expansion requiring sub-micron precision wafer handling, automotive electrification and lightweight materials assembly mandates necessitating high-accuracy grippers, and food processing hygiene standards demanding IP69 K-rated, corrosion-resistant designs for high-speed packaging lines.

Key market opportunities in the Robotic Grippers Market lie in collaborative robot gripper standardisation with plug-and-play integration platforms enabling rapid deployment and flexible automation, and the convergence of soft robotics for agricultural harvesting and medical applications supporting delicate handling, energy efficiency, and dual-use compliance.

Key players in the Robotic Grippers Market include SCHUNK, Festo, OnRobot, DESTACO, Robotiq, Universal Robotics, Destaco, and Applied Robotics.