- Medical Devices

- Disposable Robotic System Market

Disposable Robotic System Market Size, Share, and Growth Forecast, 2026 - 2033

Disposable Robotic System Market by Product Type (Disposable Surgical Robots, Disposable Endoscopic Robotic Systems, Disposable Catheter-based Robotic Systems, Others), Application (Minimally Invasive Surgery (MIS), Diagnostic Procedures, Interventional Procedures, Others), End User (Hospitals, Ambulatory Surgical Centres (ASCs), Speciality Clinics, Others) and Regional Analysis for 2026 - 2033

Disposable Robotic System Market Size and Trends Analysis

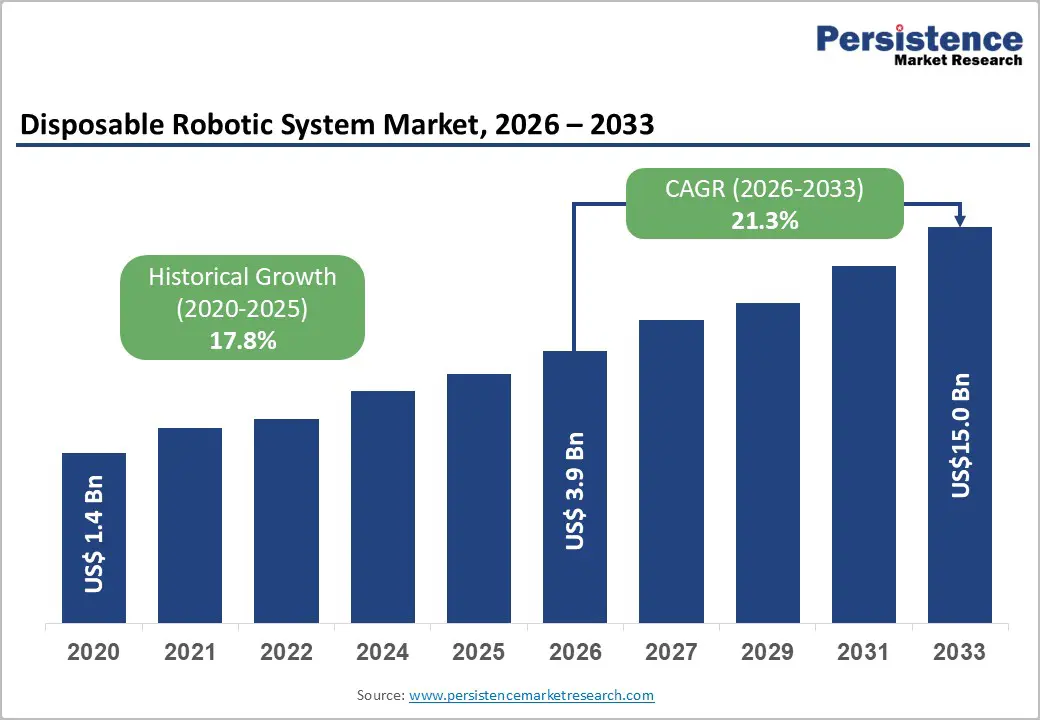

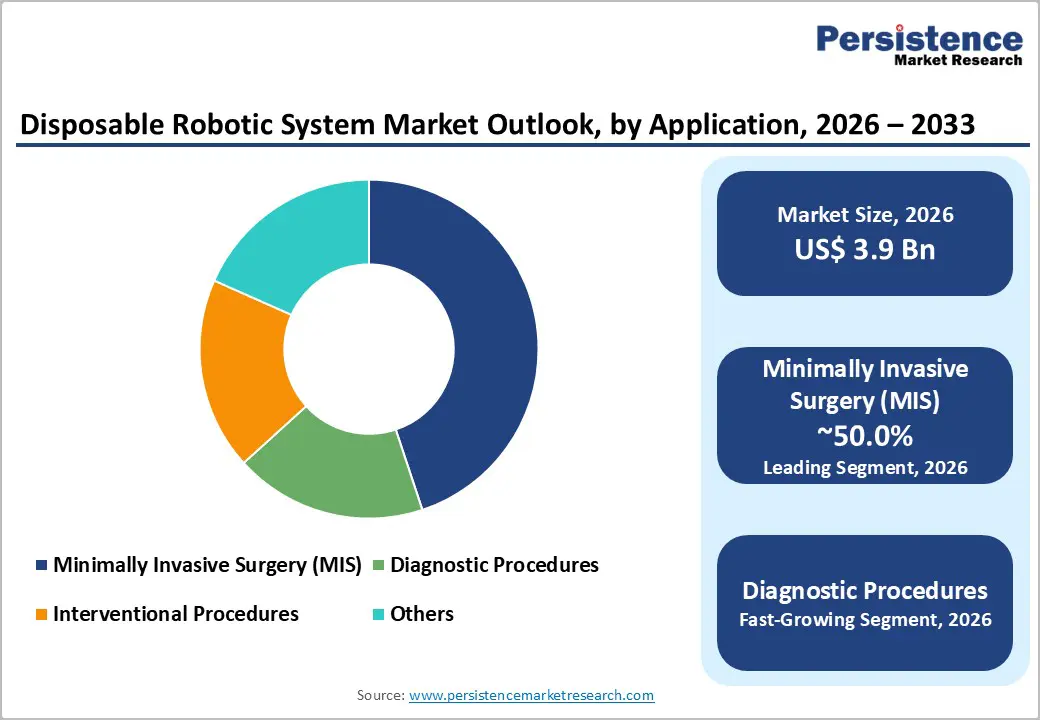

The Global Disposable Robotic System Market size was valued at US$3.9 billion in 2026 and is projected to reach US$15.0 billion by 2033, growing at a CAGR of 21.3% between 2026 and 2033. Market expansion reflects accelerating adoption of single-use, remotely operated robotic systems that fundamentally transform surgical economics, physician occupational safety, and patient access to advanced minimally invasive procedures.

The Market's exceptional growth trajectory, substantially exceeding the broader surgical robotics market, reflects paradigm-shifting advantages including elimination of capital equipment investments, reduction of physician radiation exposure by around 85 to 95 percent, rapid deployment enabling setup in under five minutes, and democratisation of robotic-assisted surgery across diverse facility types.

Key Industry Highlights:

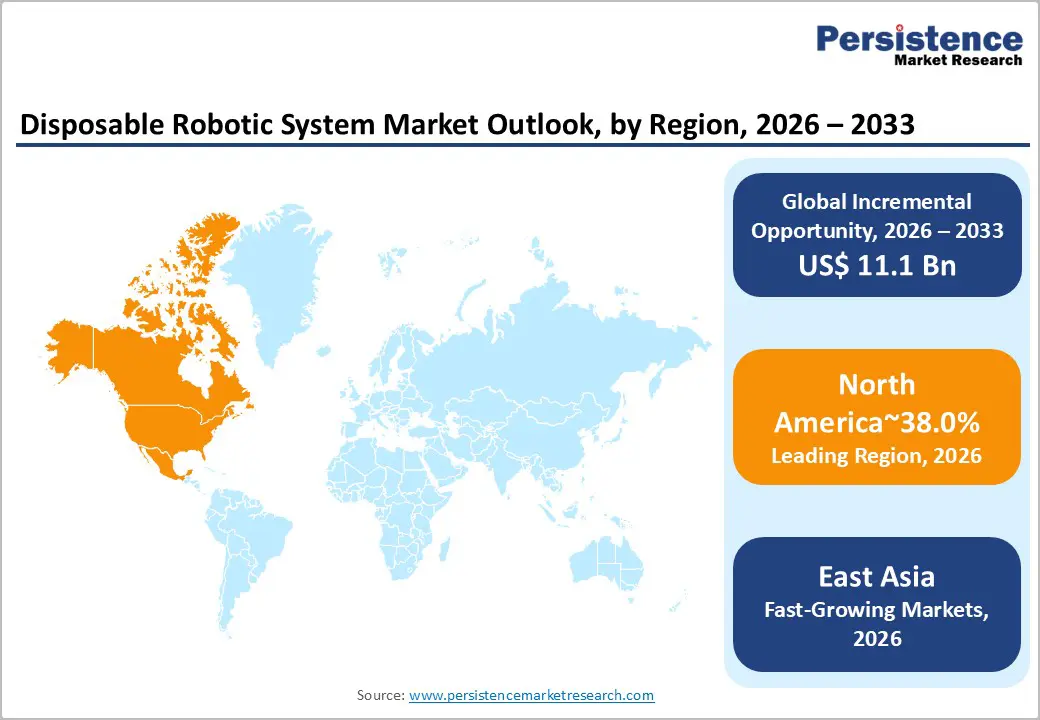

- Regional Leadership: North America leads the global Disposable Robotic System market with 38% share, driven by advanced healthcare infrastructure, early adoption of minimally invasive surgical robotics, and robust regulatory pathways supporting single-use platforms.

- Fastest-Growing Region: East Asia accounts for 20% share and represents the fastest-growing region, supported by rapid surgical robotics adoption in China, Japan, and South Korea, government healthcare modernisation, and growing middle-class demand for advanced medical technologies.

- Significant European Market: Europe holds 25% share, characterised by stringent medical device regulations, high adoption in well-funded academic medical centres, and increasing emphasis on cost-effective, modular disposable robotic systems.

- Leading Product Segment: Disposable surgical robots dominate with 45% share, driven by proven clinical efficacy, regulatory clearance, and direct substitution for reusable robotic platforms across general, urological, gynecological, and endovascular procedures.

- Fastest-Growing Product Segment: Disposable endoscopic robotic systems are the fastest-growing category, fueled by emerging applications in complex endoscopic, diagnostic, and therapeutic procedures requiring enhanced precision and visualisation.

| Key Insights | Details |

|---|---|

| Disposable Robotic System Market Size (2026E) | US$ 3.9 Bn |

| Market Value Forecast (2033F) | US$ 15.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 21.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 17.8% |

Market Dynamics

Growth Drivers

Minimally Invasive Surgery Paradigm and Patient Recovery Optimisation

Patient preference for minimally invasive surgical approaches has catalysed structural demand expansion within the Disposable Robotic System Market, driven by compelling clinical evidence demonstrating 40-50% faster recovery times, reduced postoperative complications, and diminished hospital resource consumption compared to traditional open surgical procedures.

Minimally invasive procedures currently represent approximately 70% of the global surgical robotics market, establishing a dominant positioning that disposable robotic systems directly address through enhanced accessibility and reduced procedural friction.

The Market benefits from this fundamental market shift as patients increasingly demand precision surgical outcomes achievable through remote manipulation capabilities while simultaneously avoiding the extended hospitalisation and recovery burdens associated with conventional open repair methodologies.

The ageing global population and escalating chronic disease prevalence, particularly cardiovascular, neurological, and peripheral vascular conditions requiring surgical intervention, have accelerated institutional adoption of surgical robotics. Hospitals recognise that robotic systems enhance surgical precision, reduce operative complications, and improve long-term patient outcomes while simultaneously addressing critical surgeon shortages affecting healthcare delivery globally. Disposable robotic systems amplify this advantage by eliminating equipment investment barriers that previously constrained adoption to well-capitalised academic medical centres, thereby expanding minimally invasive surgical access to ambulatory surgical centres, rural hospitals, and emerging market healthcare facilities within the Market.

Occupational Radiation Safety and Physician Wellness Protection

Physician radiation exposure represents a critical occupational health concern in endovascular and interventional procedures, with conventional manual catheterisation exposing surgical teams to chronic ionising radiation accumulation linked to elevated incidence of occupational cancers, cataracts, orthopaedic injuries, and reproductive health complications.

Disposable robotic systems fundamentally transform occupational safety profiles by enabling remote catheter and guidewire manipulation, reducing operator radiation exposure by 85 to 95 percent compared to manual interventional techniques while simultaneously eliminating the physical ergonomic strain associated with prolonged lead apron usage and repetitive positioning requirements. This occupational safety advantage represents a non-negotiable competitive differentiator within the Market, resonating powerfully with surgical teams and institutional risk management frameworks prioritising long-term clinician health preservation.

Clinical validation reinforces radiation protection benefits: Microbot Medical's LIBERTY system demonstrated 92% relative radiation reduction in pivotal trials, establishing quantifiable occupational health improvement that transcends traditional performance metrics to address fundamental workforce sustainability concerns. Healthcare institutions increasingly recognize that robotic system adoption, particularly single-use platforms eliminating reprocessing contamination risks, represents a strategic investment in clinician health preservation while simultaneously improving procedural efficiency, establishing a powerful institutional value proposition that accelerates adoption within the Market.

Market Restraining Factors

Manufacturing Complexity and Regulatory Approval Timelines

Development of single-use robotic systems requires advanced miniaturization, biocompatible materials science, sterility validation, and manufacturing scalability that impose substantial R&D investment and regulatory compliance burden within the Disposable Robotic System Market. FDA approval pathways demand comprehensive safety documentation, efficacy validation, and manufacturing consistency demonstration extending product development timelines across multiple clinical trial phases.

Quality assurance requirements mandate sophisticated manufacturing controls ensuring sterility, functionality verification, and performance consistency across large production batches, substantially increasing manufacturing costs and constraining production capacity expansion during market ramp phases within the Disposable Robotic System Market.

Key Market Opportunities

Endoscopic and Diagnostic Procedure Expansion into Minimally Invasive Domains

Endoscopic and diagnostic applications represent the fastest-growing segment within the Disposable Robotic System Market, addressing clinical opportunities in complex endoscopic submucosal dissection, diagnostic visualisation procedures, and interventional colonoscopy applications where disposable platform economics enable widespread procedural accessibility previously limited by capital constraints. Diagnostic procedures utilising robotic visualisation and enhanced precision can improve disease detection, reduce procedural complications, and enable therapeutic intervention during diagnostic procedures, creating integrated diagnostic-therapeutic value propositions.

Strategic manufacturers investing in endoscopic-specific robotic architectures addressing anatomical constraints specific to gastrointestinal, respiratory, and otolaryngologic applications can capture emerging market opportunities in procedure categories currently dominated by conventional endoscopic instruments. Development of specialised guidewire manipulation capabilities, enhanced visualisation integration, and miniaturised intervention tools designed for diagnostic procedure requirements can establish differentiation within the Market while addressing previously underserved diagnostic specialities lacking advanced precision instrumentation.

The diagnostic procedures segment demonstrates exceptional growth potential as healthcare systems increasingly prioritise precision diagnostics and early disease detection, establishing a substantial opportunity for disposable robotic systems addressing diagnostic procedure requirements within the Disposable Robotic System Market.

Hybrid Surgical Procedure Integration and Robotic-Endovascular Combination Platforms

Emerging opportunities exist for integrated surgical platforms combining robotic debranching procedures with endovascular stent graft deployment enabling complex hybrid interventions within single procedural sessions while leveraging both open surgical durability advantages and endovascular minimally invasive recovery benefits. Disposable robotic systems specifically architected for hybrid procedures can address complex aortic pathologies, challenging visceral artery reconstructions, and multi-level vascular interventions currently requiring multiple separate procedures and extended operative times.

Development of modular disposable robotic architectures enabling rapid conversion between surgical and endovascular operative modes can capture emerging hybrid procedure opportunities where traditional reusable robotic platforms demonstrate operational constraints. Within the Market, hybrid procedure development represents a high-margin opportunity addressing complex patient populations previously requiring multiple sequential operations, establishing a clinical value proposition justifying premium positioning while simultaneously improving patient outcomes through single-session comprehensive intervention.

Strategic investment in hybrid procedure validation and regulatory approval can establish a competitive moat within the Disposable Robotic System Market while addressing substantial unmet clinical demand.

Category-wise Analysis

Product Type Insights

Disposable surgical robot platforms command a dominant market share of around 45%, positioning within the Disposable Robotic System Market due to proven clinical efficacy, established regulatory pathways, and comprehensive physician familiarity with robotic-assisted surgical techniques adapted to single-use architectures.

The segment encompasses remote-operated systems designed for general surgical, urological, gynaecological, and endovascular applications, leveraging proven surgical principles translated into a disposable format. Established market leaders, including Microbot Medical, have achieved FDA regulatory clearance and demonstrated clinical success through pivotal trials, achieving 100% navigation success rates and zero device-related adverse events, establishing credibility foundations that accelerate institutional adoption.

The disposable surgical robot segment benefits from direct substitution opportunities within established surgical specialties currently utilizing reusable robotic platforms, enabling healthcare systems to transition to single-use architectures without comprehensive procedural retraining or workflow reconstruction.

Disposable endoscopic robotic systems represent fastest-growing product category within the Disposable Robotic System Market, driven by emerging applications in complex endoscopic submucosal dissection, advanced diagnostic procedures, and therapeutic endoscopic interventions requiring enhanced precision and visualization capabilities.

Application Insights

Minimally invasive surgical applications command dominant market positioning within the Disposable Robotic System Market, reflecting established clinical evidence supporting robotic-assisted minimally invasive approaches across diverse surgical specialties including urology, gynecology, general surgery, and vascular interventions. The MIS segment encompasses procedures traditionally performed through open surgical approaches where disposable robotic systems enable equivalent surgical outcomes with substantially improved patient recovery characteristics, reduced complications, and enhanced physician safety profiles.

The MIS segment's dominance reflects market maturity within broader surgical robotics, where approximately 70% of surgical robotics market revenue derives from minimally invasive applications currently dominated by reusable platforms. Disposable robotic systems directly substitute for established reusable technologies, offering compelling economic advantages and occupational safety improvements that drive institutional migration toward single-use architectures.

Diagnostic procedures represent fastest-growing application category within the Disposable Robotic System Market, driven by emerging recognition that enhanced diagnostic precision directly influences treatment planning and patient outcomes across multiple clinical domains. The segment encompasses endoscopic diagnostic visualization, advanced imaging-guided procedures, and precision tissue sampling applications where robotic manipulation enhances diagnostic accuracy while reducing patient trauma compared to conventional diagnostic approaches.

Regional Insights and Trends

North America Market Trend

North America commands 35% of the Global Disposable Robotic System Market, anchored by the United States' advanced healthcare infrastructure, robust medical device regulatory framework, and healthcare expenditure patterns supporting early-stage technology adoption.

The September 2025 FDA clearance of Microbot Medical's Liberty Endovascular Robotic System—the first fully disposable, single-use robotic platform for peripheral endovascular procedures—validated regulatory pathways for novel disposable designs while establishing clinical benchmarks including 100% navigation success rates, zero device-related adverse events, and 92% radiation exposure reduction in pivotal trials. Leading academic medical centers including New York University, Cleveland Clinic, University of Pennsylvania, and Cedars-Sinai Medical Center have operationalized robotic platforms across cardiovascular, general surgery, and orthopaedic departments, creating clinical training pipelines that normalize robotic assistance for graduating surgical residents. Johnson & Johnson MedTech's April 2025 completion of first-in-human OTTAVA Robotic Surgical System cases at Memorial Hermann-Texas Medical Center, targeting FDA De Novo authorisation for multi-speciality soft-tissue procedures, exemplifies continued innovation momentum from established medtech leaders complementing startup entrants.

East Asia Market Trend

East Asia captures 20% market share, driven by rapid surgical robotics adoption across China, Japan, and South Korea supported by government healthcare modernization initiatives, burgeoning middle-class populations demanding advanced medical technologies, and domestic medical device manufacturers challenging Western incumbents.

South Korea's Revo-i system, Asia's first domestically developed laparoscopic robotic platform approved in 2018, has completed over 1,800 procedures across 15 global installations, demonstrating technical competency while offering 30-40% cost advantages versus da Vinci systems. Japan's Hinotori platform, featuring unique 8-axis robotic arms and docking-free design, received Ministry of Health, Labour and Welfare approval in 2020 and has pioneered 5G-enabled telesurgery demonstrations validating remote operation feasibility. China's Toumai system achieved CE marking in 2023 and set a world record in November 2024 for intercontinental telesurgery spanning 12,000 kilometers between Shanghai and Casablanca, showcasing technical sophistication rivaling Western platforms.

The Disposable Robotic System Market benefits from East Asia's healthcare infrastructure investments, with China's Healthy China 2030 blueprint allocating substantial resources toward medical equipment modernization, Japan's ageing society driving surgical demand across geriatric-focused specialities, and South Korea's export-oriented medical device industry seeking differentiated technologies for global commercialisation.

Europe Market Trend

Europe accounts for 25% market share despite regulatory complexities and reimbursement fragmentation creating adoption friction across member states. The European surgical robotics market's growth trajectory reflects heterogeneous dynamics, with Scandinavia, Germany, United Kingdom, and France demonstrating higher penetration rates supported by well-funded public healthcare systems and academic medical centers prioritizing surgical innovation.

The Medical Device Regulation's 170+ page compliance framework, implemented since 2017, establishes stringent safety and efficacy standards, positioning Europe as one of the world's most rigorous regulatory environments for high-risk medical devices, including surgical robots. CMR Surgical's UK headquarters and European commercialisation strategy, culminating in 100+ Versius system installations and 30,000 plus procedures across 30 plus countries, exemplifies successful European market penetration by next-generation platforms emphasising modularity, portability, and cost-effectiveness.

Competitive Landscape

The global Disposable Robotic System market is consolidated in nature, dominated by a few key players who hold significant market share due to advanced technological capabilities, strong R&D pipelines, and extensive distribution networks. Intuitive Surgical leads the market with its well-established da Vinci® single-use instruments and continuous innovation in minimally invasive surgery systems. Medtronic and Stryker Corporation follow closely, leveraging modular and cost-effective disposable robotic solutions for hospitals and surgical centres. Smith & Nephew, Zimmer Biomet Holdings, and TransEnterix Surgical are also prominent, focusing on niche surgical applications and expanding their geographic presence.

The market is characterised by high entry barriers, significant regulatory requirements, and continuous innovation, making it difficult for smaller players to compete. Companies are increasingly investing in single-use robotics and smart instruments to address surgical efficiency, reduce cross-contamination risks, and meet growing demand in minimally invasive and interventional procedures. Emerging players like EndoWays and Medicaroid are exploring specialised robotic solutions, but overall market power remains concentrated among the leading firms.

Key Industry Developments

- In Sep 2025, Microbot Medical received FDA clearance for its Liberty Endovascular Robotic System, the first single-use, fully disposable robotic system for peripheral endovascular procedures. The system enables remote manipulation of guidewires and catheters, reduces clinician radiation exposure by 92%, and can be set up in under five minutes, marking a major step toward commercial adoption and expanded access to cost-effective robotic interventions.

- In May 2023, Microbot Medical announced that its LIBERTY® Robotic System surpassed 100 catheterisations in pre-clinical studies, achieving a 95% success rate in reaching pre-determined vascular targets with no intraoperative complications. The fully disposable system demonstrated consistent, safe, and reliable performance, reinforcing physician interest and supporting the company’s progress toward commercialisation and regulatory approvals, while aiming to reduce capital equipment needs, radiation exposure, and physician strain.

Companies Covered in Disposable Robotic System Market

- Intuitive Surgical

- Smith & Nephew

- Microdot Medical

- Medtronic

- EndoWays

- Stryker Corporation

- Zimmer Biomet Holdings

- TransEnterix Surgical

- Verb Surgical

- Medicaroid

Frequently Asked Questions

The global Disposable Robotic System Market is projected to be valued at US$ 3.9 Bn in 2026.

Minimally Invasive Surgery (MIS) Segment is expected to account for approximately 50% of the global Disposable Robotic System Market by Application in 2026.

The market is expected to witness a CAGR of 21.3% from 2026 to 2033.

The Disposable Robotic System Market is driven by the rising preference for minimally invasive surgeries enhancing patient recovery, coupled with occupational safety benefits for physicians through reduced radiation exposure and ergonomic strain, and expanded accessibility in hospitals and ambulatory centers.

Key opportunities in the Disposable Robotic System Market lie in expanding endoscopic and diagnostic procedures for minimally invasive interventions and developing hybrid robotic-endovascular platforms enabling single-session complex surgeries.

The key players in the Disposable Robotic System Market include Smith & Nephew, Zimmer Biomet Holdings, and TransEnterix Surgical.