- Testing, Inspection, & Certification

- OTA Testing Market

OTA Testing Market Size, Share, and Growth Forecast, 2025 - 2032

OTA Testing Market by Offering (Hardware (Chambers (Anechoic, Reverberation, Compact Range), Instrumentation (Signal Generators, Spectrum Analysers, Controllers)), Software and Analytics, Services (Testing and Certification Services, Consulting and Integration)), Technology (Telecom and Consumer Electronics, Automotive and Transportation, Industrial and Manufacturing IoT, Aerospace and Defense, Others), End-use, and Regional Analysis for 2025 - 2032

OTA Testing Market Size and Trend Analysis

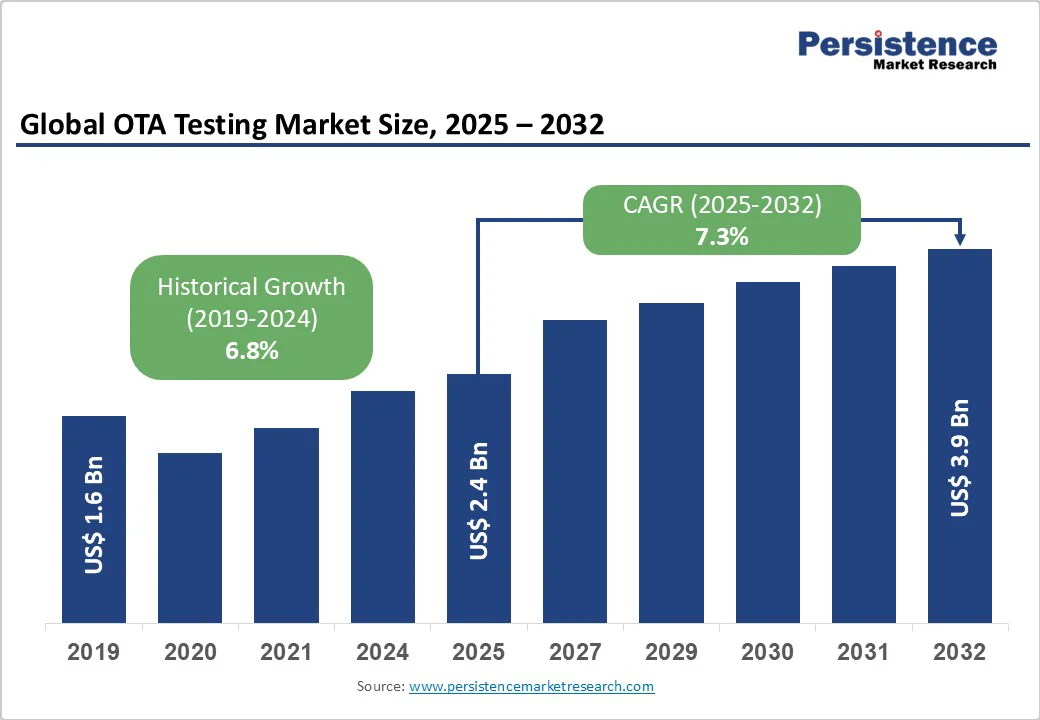

The global OTA testing market size is expected to be valued at US$2.4 billion in 2025 and reach US$3.9 billion by 2032, growing at a CAGR of 7.3% during the forecast period from 2025 to 2032.

The OTA testing market is witnessing robust growth, driven by the proliferation of 5G networks, IoT devices, and connected vehicles, where reliable wireless performance is essential.

OTA testing evaluates device antennas and systems in real-world conditions, ensuring compliance with standards for signal strength, interference resistance, and data throughput.

Key Industry Highlights

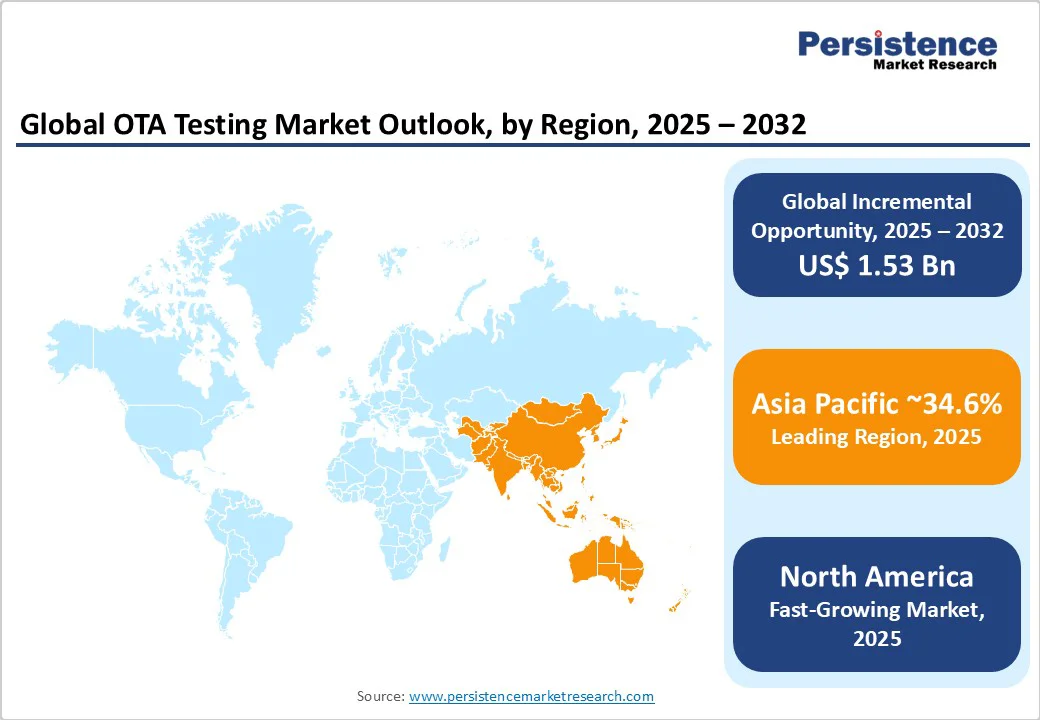

- Leading Region: Asia Pacific holds 34.6% market share of the OTA testing market in 2025, fueled by massive 5G deployments in China, Japan, and South Korea, alongside booming consumer electronics manufacturing.

- Fastest-growing Region: North America is the fastest-growing region, driven by innovation in automotive connectivity and IoT in the U.S. and Canada, backed by strong R&D investments.

- Investment Plans: China's 14th Five-Year Plan targets 80% 5G coverage by 2025, spurring OTA testing for telecom and industrial applications.

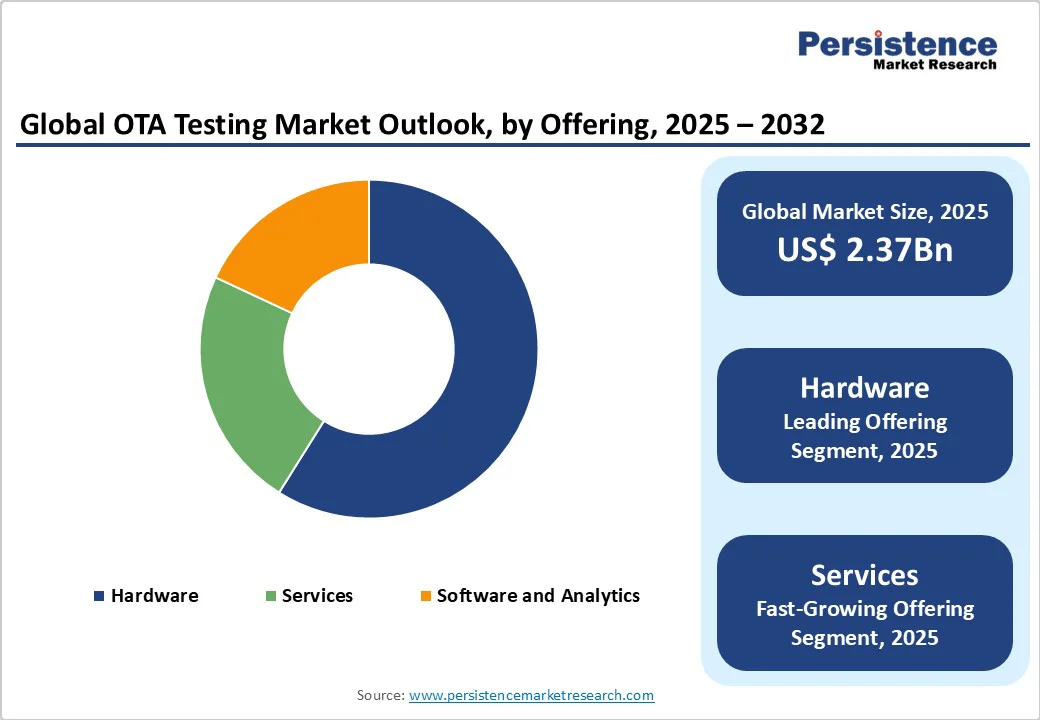

- Dominant Offering: Hardware, accounting for 58.8% of the OTA testing market share, due to demand for anechoic chambers and signal analyzers in high-volume testing.

- Leading End-use: Consumer Electronics, contributing over 37.6% of market revenue, propelled by smartphone shipments and wearable device proliferation.

| Key Insights | Details |

|---|---|

| OTA Testing Market Size (2025E) | US$ 2.4Bn |

| Market Value Forecast (2032F) | US$ 3.9Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.8% |

Market Dynamics

Driver: Proliferation of 5G and IoT Ecosystems Drives Market Expansion

The global OTA testing market is experiencing substantial growth due to the widespread adoption of 5G and IoT technologies worldwide. OTA testing is indispensable for validating antenna performance, MIMO configurations, and real-world signal propagation in 5G devices.

In the Asia Pacific, China's 5G base stations exceeded 3.92 million in 2024, boosting demand for OTA solutions in telecom infrastructure. The IoT ecosystem, expected to encompass 75 billion devices by 2025 per Statista, amplifies this trend, as connected sensors and edge devices require interference-resistant testing.

Companies such as Keysight Technologies reported revenue surge in OTA hardware sales in 2024, attributed to automotive and consumer applications. Regulatory pressures from the FCC and ETSI, combined with the need for seamless connectivity in smart factories and vehicles, cement OTA testing as a cornerstone driver through 2032.

Restraint: High Costs of Specialized Infrastructure and Skilled Expertise

The OTA testing market faces significant challenges due to the high costs associated with specialized infrastructure and the limited availability of skilled expertise. Building and maintaining advanced testing facilities, such as anechoic chambers and sophisticated measurement instruments, requires substantial capital investment, often restricting access to larger, well-funded players.

Additionally, regional regulatory variations such as differing FCC standards in the U.S. and CE requirements in Europe create added complexity and compliance costs for companies operating globally.

Although cloud-based OTA simulation platforms provide some cost-effective alternatives, they fall short in replicating the precise conditions of physical chambers, making them less suitable for critical applications such as aerospace and defense. These factors collectively hinder market penetration, particularly in regions with tighter budget constraints, slowing overall growth and innovation within the OTA testing industry.

Opportunity: Advancements in Automotive Connectivity and Smart Cities

The growing adoption of OTA updates in automotive and smart city infrastructures is unlocking significant growth potential for the OTA testing market. Smart city projects require rigorous testing of traffic sensors, urban IoT networks, and connected devices to ensure reliability and security.

Innovations, such as Rohde & Schwarz’s Vehicle-in-the-Loop systems, facilitate realistic over-the-air simulations for autonomous vehicles, supporting safer and more efficient transportation solutions that align with the EU’s Green Deal and U.S. infrastructure initiatives.

Leading companies, such as Anritsu, are advancing AI-powered OTA testing tools that enable predictive failure analysis, thereby enhancing maintenance and reducing downtime across these sectors. Government incentives and funding programs further stimulate demand for scalable, cost-effective OTA solutions.

As sustainability priorities shift computing closer to the edge, eco-friendly OTA testing methods provide manufacturers with opportunities to innovate while addressing environmental goals, positioning them to capture expanding market revenue through 2032.

Category-wise Insights

By Offering

- Hardware dominates with approximately 58.8% market share of the OTA testing market in 2025, driven by essential components such as anechoic chambers and spectrum analyzers for precise RF measurements. Critical for 5G mmWave and MIMO testing, hardware ensures accurate replication of real-world conditions in telecom and automotive applications. Leading firms, such as Rohde & Schwarz and ETS-Lindgren supply advanced chambers, supporting high-volume production in the Asia Pacific and North America, where regulatory compliance demands robust setups for consumer devices and IoT modules.

- Services are rapidly expanding due to the need for certification, consulting, and integration in complex deployments. Tailored for aerospace and healthcare, services address customization and post-deployment audits. Providers such as TÜV Rheinland and Intertek excel in providing end-to-end solutions, particularly in Europe and North America, where stringent standards, including FCC and RED directives, fuel demand for expert-led OTA validation.

By Technology

- Telecom and consumer electronics held the largest market share in 2025, at approximately 41.8%, driven by rapid 5G smartphone refresh cycles and the widespread deployment of Wi-Fi 7. OTA testing is critical for validating TRP/TIS performance across billions of devices annually, ensuring seamless global interoperability. Industry leaders such as Keysight and Anritsu supply advanced multi-band analyzers, which support dense urban networks, particularly throughout the Asia Pacific region.

- The automotive and transportation sectors surge ahead, driven by the integration of V2X and ADAS in electric vehicles. OTA solutions test latency-critical links for safety, aligning with SAE Level 3 autonomy. Bluetest AB and MVG innovate for dynamic scenarios, with adoption accelerating in North America and Europe, amid projections for 3.5 million self-driving vehicles by 2025.

By End-use

- Consumer electronics accounted for over 37.6% of the revenue share in 2025, driven by the rising demand for wearables and smart home devices that require Bluetooth and Wi-Fi certifications. OTA testing ensures seamless connectivity and performance for these devices. SGS and UL LLC lead compliance testing, supporting global shipments, particularly from major manufacturing hubs in the Asia Pacific region.

- Automotive is the fastest-growing end-use segment of the OTA testing market, driven by expanding connected car ecosystems and widespread OTA firmware updates. Rigorous testing ensures cybersecurity and performance under harsh conditions, critical for vehicle safety and reliability. Industry leaders such as Intertek and DEKRA provide comprehensive validation services. Rapid growth in the U.S. and China highlights increasing demand for dependable wireless testing and validation solutions.

Regional Insights

Asia Pacific OTA Testing Market Trends

The Asia Pacific region leads the OTA testing market, accounting for a 34.6% share, driven by the rapid expansion of 5G networks and robust electronics manufacturing hubs in China and India.

China’s Ministry of Industry and Information Technology (MIIT) reported approximately 4.25 million 5G base stations by December 2024, a surge of 870,000 from the previous year, fueling demand for OTA testing of mmWave devices and industrial IoT applications. India’s ambitious Production-Linked Incentive (PLI) scheme aims to achieve $300 billion in electronics manufacturing by 2025, underscoring the need for certification labs to ensure export quality and compliance.

Meanwhile, Japan and South Korea are at the forefront of automotive OTA testing, especially for Vehicle-to-Everything (V2X) communication, with major automakers such as Toyota and Hyundai heavily investing in connected vehicle technologies.

Leading OTA testing firms, such as Anritsu and Keysight, are expanding their facilities to support smart city pilot projects in Singapore. Rapid urbanization and sustained government subsidies solidify the Asia Pacific’s dominant position through 2032.

North America OTA Testing Market Trends

North America is emerging as the fastest-growing region in the OTA testing market, fueled by significant advancements in 5G technology and autonomous vehicle development in both the U.S. and Canada. The U.S. telecom industry heavily relies on OTA testing to secure CTIA certification, ensuring seamless connectivity and robust performance for millions of 5G users nationwide.

Market leaders such as Rohde & Schwarz and ETS-Lindgren have capitalized on this growth by providing comprehensive, integrated OTA solutions tailored for Advanced Driver Assistance Systems (ADAS), which are critical for the safety and reliability of autonomous vehicles.

Furthermore, recent U.S. infrastructure legislation has allocated $65 billion toward expanding broadband access, which in turn accelerates the validation and deployment of IoT devices.

The increasing adoption of AI-enhanced OTA analytics enables more precise testing and predictive insights, reinforcing North America’s dominant position in wireless technology validation. Collectively, these factors position the region for sustained leadership and innovation in OTA testing through 2032.

Europe OTA Testing Market Trends

Europe ranks as the second fastest-growing region in the OTA testing market, driven by stringent regulatory frameworks and a strong focus on green technology, particularly in Germany and France.

Germany’s robust automotive sector extensively utilizes OTA testing to meet Euro NCAP safety standards, ensuring advanced vehicle safety and connectivity. Meanwhile, France’s “5G for Industry” initiative accelerates the deployment of 5G-enabled smart factories, boosting industrial IoT applications that require rigorous OTA validation.

Key players such as TÜV Rheinland and Intertek lead innovation by developing sustainable OTA testing solutions that align with the European Green Deal, which earmarks €1 trillion for climate-neutral investments.

Furthermore, Europe’s emphasis on data privacy and security, reinforced by GDPR, drives the adoption of secure and compliant OTA testing practices. These factors collectively fuel consistent market growth, positioning Europe as a vital hub for sustainable and secure OTA validation through 2032.

Competitive Landscape

The global OTA testing market is highly competitive, dominated by comprehensive portfolios and global networks. Characterized as fragmented, it features multinational giants alongside regional specialists.

Leaders such as Keysight Technologies and Rohde & Schwarz command shares through innovation in 5G and automotive testing. Local firms such as CETECOM focus on Europe-specific compliance. Investments in AI-driven analytics and modular chambers intensify rivalry, spurred by 5G and IoT demands in telecom and consumer sectors.

Key Industry Developments

- April 2025: Anritsu and Microwave Vision Group launched a Wi-Fi 7 OTA system integrating MVG's multi-probe chambers with MT8862A testers, enabling efficient multi-link operation for consumer devices in the Asia Pacific. This joint offering enables manufacturers to test the Radio Frequency (RF) transmit and receive characteristics of Wi-Fi 7 devices by supporting features such as 320 MHz bandwidth, 4K QAM, and Multi-Link Operation, providing a stable and efficient platform for product development and compliance.

- March 2025; Keysight Technologies launched two new DCA-M sampling oscilloscopes capable of analyzing optical signals at speeds up to 240 Gbps per lane. These instruments were specifically designed for testing 1.6T optical transceivers used in AI data centers and next-generation optical interconnects. The oscilloscopes featured integrated clock recovery supporting baud rates up to 120 GBaud, simplifying testing procedures and reducing complexity.

Companies Covered in OTA Testing Market

- Anritsu

- Rohde & Schwarz

- Keysight Technologies ·

- ETS-Lindgren

- Bluetest AB

- TÜV Rheinland

- SGS Société Générale de Surveillance SA.

- MVG

- UL LLC

- Intertek Group plc

- Others

Frequently Asked Questions

The OTA Testing market is projected to reach US$2.37 Bn in 2025.

Proliferation of 5G and IoT ecosystems, and expanding applications in automotive connectivity are the key market drivers.

The OTA Testing market is poised to witness a CAGR of 7.3% from 2025 to 2032.

Advancements in automotive connectivity and smart cities are the key market opportunities.

Anritsu, Rohde & Schwarz, Keysight Technologies, and Intertek Group plc are key market players.