- Processed Food

- Potato and Yam Derivatives Market

Potato and Yam Derivatives Market Size, Share, and Growth Forecast, 2026 - 2033

Potato and Yam Derivatives Market By Source (Potato, Sweet Potato, Others), Derivative Type (Starch, Flakes & Dehydrated, Others), Application, Sales Channel, and Regional Analysis for 2026 - 2033

Potato and Yam Derivatives Market Size and Trends Analysis

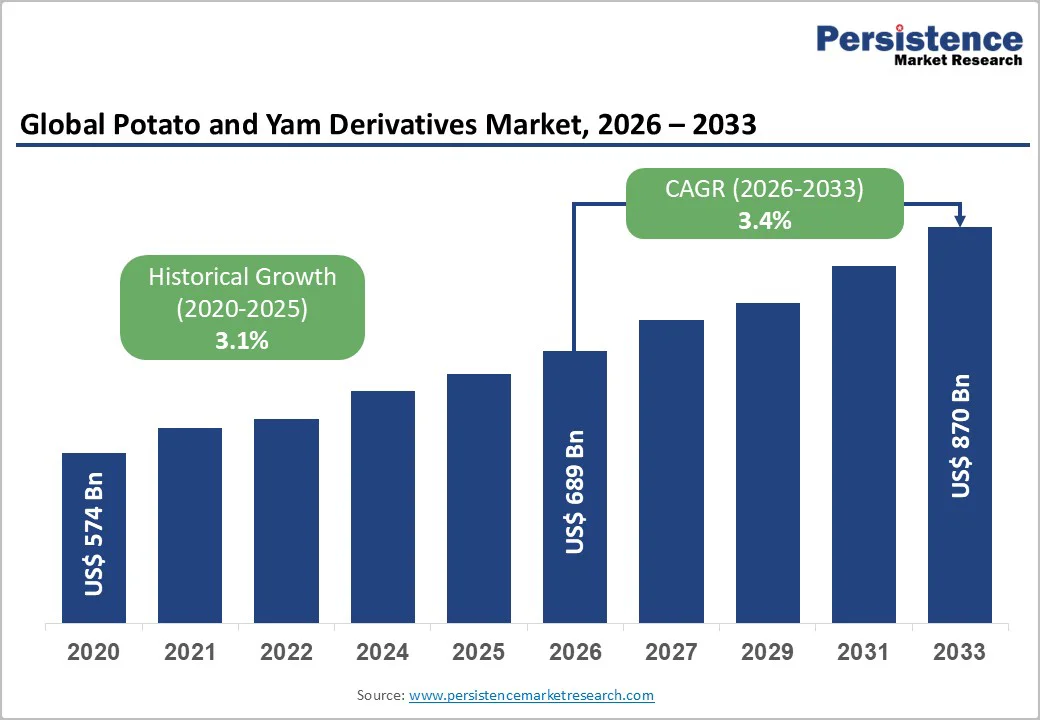

The global potato and yam derivatives market size is likely to be valued at US$689 Billion in 2026 and is expected to reach US$870 Billion by 2033, growing at a CAGR of 3.4% from 2026 to 2033, driven by growing consumption of processed foods and snacks, increased use of starches, flours, and proteins in industrial and food applications, demand growth in pet nutrition, and rising interest in biodegradable materials.

Supply-side improvements in yield and processing efficiency support volume growth while raw-material price volatility and substitution pressure from cassava or corn-based derivatives limit margin expansion.

Key Industry Highlights

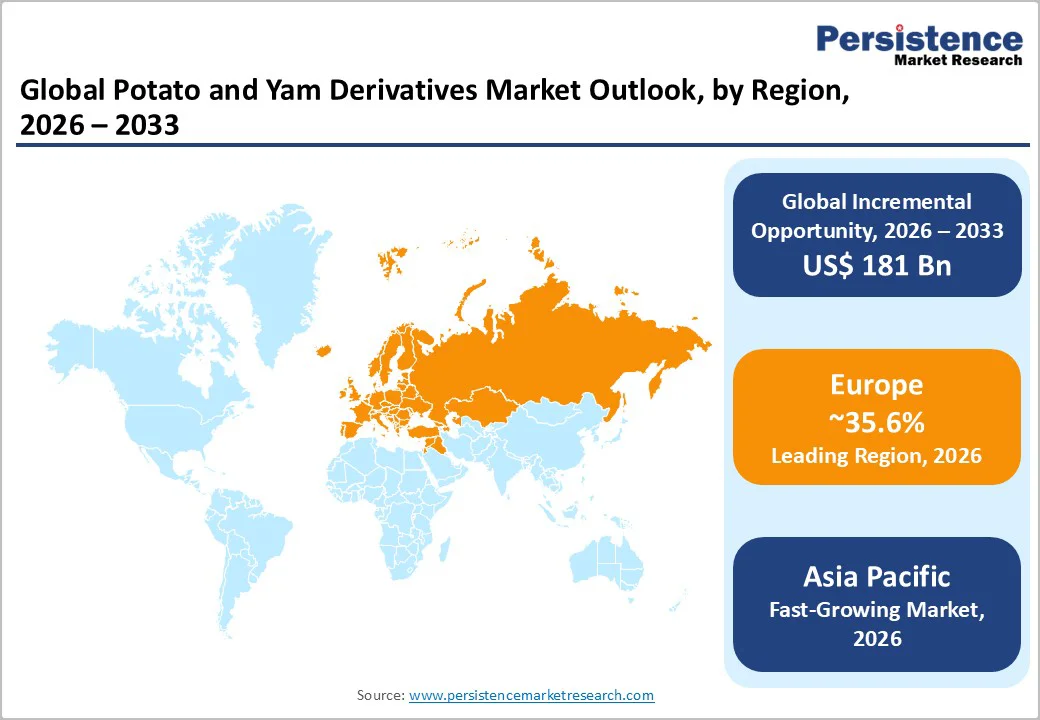

- Leading Region: Europe is anticipated to account for 35.6% of global potato and yam derivative demand in 2025, supported by advanced starch-processing infrastructure, strong clean-label adoption, and significant R&D investments in high-purity proteins and specialty starches.

- Fastest-growing Region: Asia Pacific is expected to expand, supported by increasing snack consumption, significant capacity additions in China and India, and growing adoption of starch in packaging, adhesives, and various industrial applications.

- Dominant Derivative Type: Starch is anticipated to lead the derivative type category with roughly 34.6% of the total market revenue in 2026, driven by extensive use in food processing, paper, textiles, adhesives, and biodegradable material formulations.

- Leading Application: Food applications are anticipated to account for an estimated 47% of total derivative consumption in 2026, reflecting strong demand from snacks, bakery, confectionery, and ready-to-eat foods that rely heavily on flakes, granules, modified starch, and dehydrated derivatives.

| Key Insights | Details |

|---|---|

| Potato and Yam Derivatives Market Size (2026E) | US$689 Bn |

| Market Value Forecast (2033F) | US$870 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Consumption of Convenience Snacks and Processed Foods

Global consumption of potato-based snacks, processed potatoes, and ready-to-eat foods continues to accelerate. The potato snacks category is expected to grow, indicating stable downstream demand for ingredients such as flakes, granules, dehydrated potato products, and functional starches.

This escalates offtake from both commodity derivative suppliers and producers of high-value starches and texturizers. Urban lifestyles, expanded retail penetration, and growing snack adoption across Asia Pacific and Latin America reinforce this trend. Ingredient producers benefit from consistent procurement cycles and incentives to invest in capacity expansion and product development.

Expansion of Specialty Applications Including Protein and Bio-Based Materials

Technical advances have moved potato-derived ingredients beyond traditional thickening roles. Purified potato proteins are gaining traction in pet food and human nutrition, supported by launches such as high-purity protein isolates introduced in 2024. Starch streams are increasingly used in bio-based polymers and biodegradable packaging.

These specialty applications attract higher margins and generate new demand channels. Ingredient manufacturers are prioritizing investments in purification systems, fractionation lines, and collaborative R&D with food and materials companies to capitalize on premium market opportunities.

Barrier Analysis - Raw-Material Price Instability and Yield Variability

Potato and yam crops are highly sensitive to weather, soil conditions, and seasonal disruptions. Variability in rainfall or temperature can lead to significant swings in yields and raw material availability. Input costs such as fertilizer, fuel, and labor have also experienced volatility.

Processors often face compressed margins during seasons with lower yields or elevated contract prices. Fluctuating production cycles discourage aggressive capacity expansion, particularly in regions where climatic risks are more pronounced.

Competition from Lower - Cost Alternative Starches and Regulatory Burdens

Potato and yam derivatives frequently compete with cheaper starch sources such as corn and cassava, particularly in price-sensitive applications like paper, textile, and adhesives manufacturing. This substitution risk limits pricing power in commodity-grade segments.

Regulatory compliance challenges add to the restraint profile. Food safety, traceability rules, pesticide-residue limits, and approvals for novel proteins or pet-food ingredients create cost burdens for processors developing high-purity or specialty-grade ingredients.

Opportunity Analysis - High-Purity Potato Protein for Human and Pet Nutrition

Potato protein offers strong digestibility, neutral flavor, and a favorable amino acid profile. Premiumization in pet food and interest in alternative plant proteins for human nutrition are strengthening commercial demand.

If potato protein captures even 0.5 to 1 percent of the total derivatives market value by 2030, the resulting opportunity amounts to several billion dollars in incremental revenue potential. Investments in protein purification technology, co-branding initiatives with pet-food producers, and marketing focused on sustainability and nutritional advantages can unlock substantial value.

Bio-Based Materials and Industrial Starch Upgrading

The global shift toward renewable and biodegradable materials is generating momentum for starch-based polymers, films, and packaging. Improved cross-linking, anti-retrogradation techniques, and composite formulations are improving performance, making potato and yam starches viable alternatives to petroleum-based materials.

If even 2 to 5% of starch volumes are redirected to higher-value bio-based industrial applications, processors can achieve significant margin expansion. Strategic opportunities include partnerships with packaging converters, technology licensing, and participation in pilot-scale circular-economy programs.

Category-wise Analysis

Derivative Type Insights

Starch is anticipated to dominate, representing roughly 34.6% of the global market revenue in 2026. Its leadership is supported by extensive use across food processing, paper manufacturing, textiles, and adhesive formulations. Potato starch production volumes consistently reach several million tonnes annually, reflecting its industrial scale and stable demand base.

Modified and pre-gelatinized starches are particularly important due to their functional versatility, including thickening, binding, and moisture-retention properties. Producers such as large European starch processors continue to expand capacity for specialty grades used in sauces, confectionery, and clean-label bakery items. Adoption in paper coatings, packaging adhesives, and bio-based polymer fillers further reinforces starch’s position as the market’s core volume driver.

Protein isolates, concentrates, and other specialty derivatives are expected to see the highest growth in 2026, driven by changing dietary trends and expanding industrial applications. Potato protein, valued for its amino acid profile and digestibility, is increasingly incorporated into sports nutrition powders, plant-based meat alternatives, and premium pet foods.

In Western Europe and North America, high-purity protein ingredients are tailored for extrusion-based meat analogues and allergen-free products. Specialty derivatives such as functional starches, clarified fibers, and enzymatically modified carbohydrates support natural emulsification, freeze-thaw stability, and low-viscosity thickening, with precision fractionation enabling high-value applications in beverages, nutraceuticals, and supplements.

Application Insights

Food applications are anticipated to dominate the market in 2026 with a share of 47%, led by snacks, bakery products, soups, sauces, and ready-to-eat meals. Growing global snack intake, driven by urbanization and expanding supermarket penetration, continues to elevate the use of flakes, granules, modified starch, and dehydrated ingredients.

Multinational snack brands integrate potato derivatives to improve crispiness, oil management, and texture stability in chips and extruded snacks. In bakery and convenience food manufacturing, dehydrated potato flakes and granules are used to enhance dough consistency, reduce preparation time, and maintain shelf stability.

Examples include instant mashed potato products, shelf-stable meal kits, and extrusion-based savory snacks that rely on consistent functional performance of potato derivatives.

Industrial applications for potato and yam derivatives are expected to expand at the fastest pace, driven by sustainability goals and the search for renewable materials. Starch-based adhesives, biodegradable polymers, and paper-coating formulations are gaining traction across the packaging, printing, and textile industries.

Bioplastics manufacturers are increasingly incorporating potato starch as a bio-filler or polymer backbone to improve biodegradability and reduce reliance on petroleum-derived resins. Paper producers in Europe and Asia are adopting modified starch coatings to enhance printability, water resistance, and material strength while complying with tightening environmental regulations.

Textile processors use starch for warp sizing, improving yarn performance during weaving, and reducing chemical load.

Regional Insights

North America Potato and Yam Derivatives Market Trends - Snack-Driven Innovation and Clean-Label Expansion

North America remains a key market for potato and yam derivatives, driven by high per-capita snack consumption, strong quick-service restaurant expansion, and a well-developed food-processing sector.

The U.S. leads the region, supported by major frozen potato processors and ingredient suppliers serving snacks, bakery, soups, sauces, and ready meals. Canada also contributes meaningfully as a major exporter, supported by integrated farming and processing operations.

Market growth is strengthened by rising demand for clean-label ingredients, including minimally processed starches, functional fibers, and specialty proteins aligned with natural formulation trends. Ingredient manufacturers are investing in advanced fractionation, enzymatic modification, and filtration technologies that deliver high-purity starches and functional components for plant-based foods, premium pet nutrition, and industrial adhesive applications.

Sustainability priorities further shape production strategies across the region, encouraging processors to adopt energy-efficient drying systems, water-recycling technologies, and waste-to-biogas solutions that reduce environmental impact.

Regulatory frameworks, particularly the Food Safety Modernization Act, influence sourcing, hazard controls, and processing standards. Labeling rules for non-GMO, natural, and allergen-free claims also guide how potato and yam derivatives are positioned for food and industrial manufacturers.

Europe Potato and Yam Derivatives Market Trends - Advanced Starch Technology and Circular Economy Focus

Europe is anticipated to account for an estimated 35.6% of global potato and yam derivative demand, due to its highly developed potato-processing ecosystem, diverse agricultural supply base, and long-standing leadership in starch innovation.

Countries including the Netherlands, France, Germany, Belgium, and Poland operate some of the world’s most advanced starch extraction and dehydration facilities. Innovation is central to Europe’s competitive positioning. Leading processors invest heavily in R&D for functional starch derivatives, enzymatically modified ingredients, and protein isolates suitable for beverages, plant-based foods, and infant nutrition.

Specialty flakes and granules designed for premium snacks and quick-preparation meals also maintain strong demand. Environmental policies across the EU are accelerating industrial uses of potato starch in biodegradable films, compostable packaging, paper coatings, and adhesive systems, reinforcing the region’s shift toward circular-resource models.

The regulatory landscape, shaped by EU food safety legislation, REACH chemical compliance rules, and packaging-waste directives, strongly influences product specifications and processing technologies.

Agricultural policies under the Common Agricultural Policy (CAP) affect raw-material pricing, contract farming, and acreage decisions.

Countries such as Spain and the U.K. are expanding capacities for dehydrated potato ingredients to meet rising demand from bakery, snacks, and convenience food manufacturers. Broad adoption of sustainability frameworks and traceability systems continues to strengthen Europe’s role as a high-value ingredient supplier with advanced quality and environmental standards.

Asia Pacific Potato and Yam Derivatives Market Trends - Advanced Starch Technology and Circular Economy Focus

Asia Pacific is expected to be the fastest-growing region in the potato and yam derivatives market, supported by large population bases, rapid urbanization, expanding retail distribution, and rising consumption of snacks, bakery items, and processed foods.

China remains the largest contributor, driven by the continued expansion of processing capacities for starch, flakes, dehydrated ingredients, and modified derivatives. Domestic manufacturers supply major snack brands, noodle companies, and instant-food producers that depend on consistent starch quality and cost efficiency.

India is experiencing rapid growth in the use of potato flakes and starch across snacks, curries, batters, and frozen foods as domestic processors scale capacity and invest in automation.

ASEAN markets, particularly Vietnam, Indonesia, and the Philippines, are emerging as competitive hubs for sweet potato and yam derivatives due to favorable climates, cost advantages, and growing export activity. Regional diversification is increasing as manufacturers expand supply chains and partner with food and industrial customers across Asia’s high-growth economies.

Regulatory reforms and investments in cold-chain systems are strengthening quality standards and improving raw-material availability, while rising interest in renewable materials boosts demand for bio-based starches across packaging, textiles, adhesives, paper manufacturing, and industrial applications.

Competitive Landscape

The global potato and yam derivatives market is moderately consolidated at the ingredient-supplier level, with a handful of major companies dominating starch and specialty ingredients due to high capital requirements and technological barriers. In contrast, the downstream dehydrated products segment is more fragmented, with numerous regional processors. Producers of frozen potato products also contribute significant scale and influence global demand for derivatives.

Key strategies include innovation in clean-label and specialty ingredients, vertical integration to secure raw-material supply, geographic expansion in the Asia Pacific, and investment in high-protein and bio-based industrial applications. Long-term partnerships with food and industrial manufacturers are critical for technology adoption and value-chain stability.

Key Industry Developments

- In May 2025, KMC partnered with a UK distributor to expand delivery of its clean-label potato starch solutions. This move supports broader adoption of functional and native potato starches in food manufacturing, particularly for companies looking for clean-label and allergen-free formulations.

- In August 2024, PoLoPo added a functional potato protein (patatin) to its commercial product lineup for the first time. This protein, native to potatoes, is positioned as a versatile, allergy-friendly ingredient with full essential amino acids, suitable for bakery, beverage, plant-based meat/dairy alternatives, and nutraceutical use.

Companies Covered in Potato and Yam Derivatives Market

- Avebe

- Emsland Group

- Roquette

- Tereos

- Ingredion

- Cargill

- ADM

- KMC

- Pepees Group

- Südstärke

- Novidon

- Lyckeby

- PPZ Trzemeszno

- McCain Foods

- Lamb Weston

- Simplot

- Idahoan Foods

- Basic American Foods

- BENEO

- AGRANA

Frequently Asked Questions

The global potato and yam derivatives market size is estimated to be US$689 Billion in 2026.

By 2033, the potato and yam derivatives market is projected to reach US$870 Billion.

Key trends include the rising use of clean-label starches, rapid adoption of potato proteins in plant-based and pet nutrition products, expanded industrial applications in biodegradable materials and adhesives, and technological advancements in starch modification and protein fractionation.

Starch is the leading derivative segment, accounting for approximately one-third of total market revenue due to its extensive use in food processing, paper, textiles, and adhesives.

The market is expected to grow at a CAGR of 3.4% from 2026 to 2033, supported by steady demand across food applications and rising adoption in industrial uses.

Major companies include Avebe, Emsland Group, Roquette, Ingredion, and Cargill.