- Food Ingredients & Additives

- Organic Oats Market

Organic Oats Market Size, Share, and Growth Forecast 2026 - 2033

Organic Oats Market by Product Type (Whole Oats Groats, Steel Cut Oats, Rolled Oats, Oat Flour), End- user (Retail, Food & Beverage Industry: Breakfast Cereals, Bakery & Confectionery, Beverages, Snacks and Savory, Others; Foodservice Industry, Others), Distribution Channel (Business to Business, Business to Consumer), and Regional Analysis, 2026 - 2033

Organic Oats Market Share and Trends Analysis

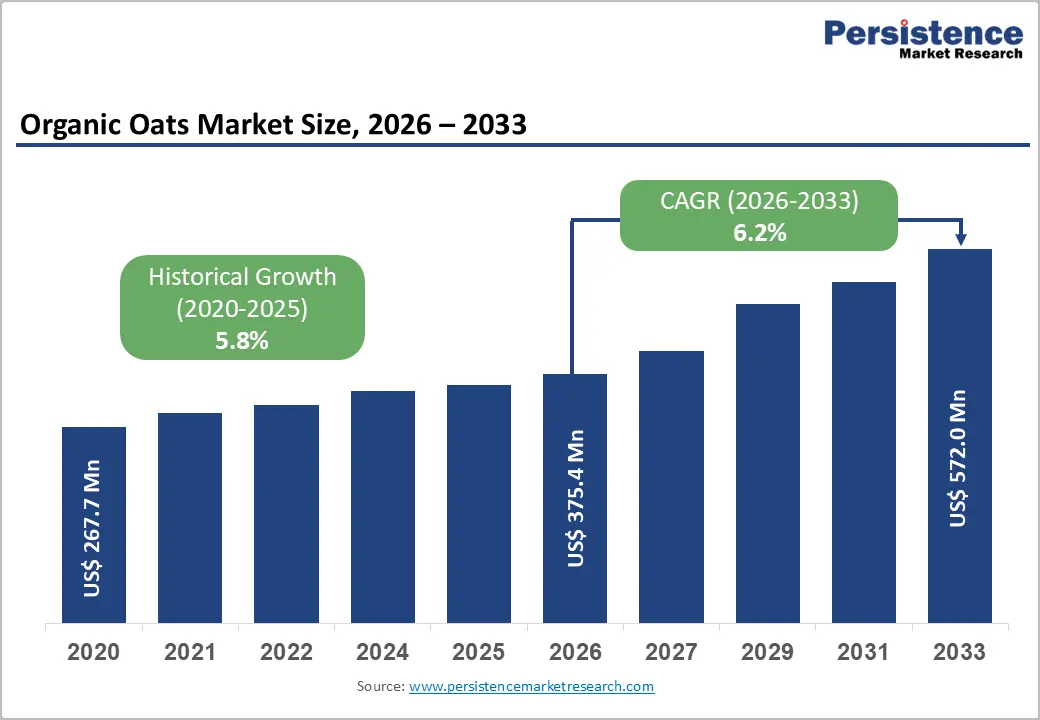

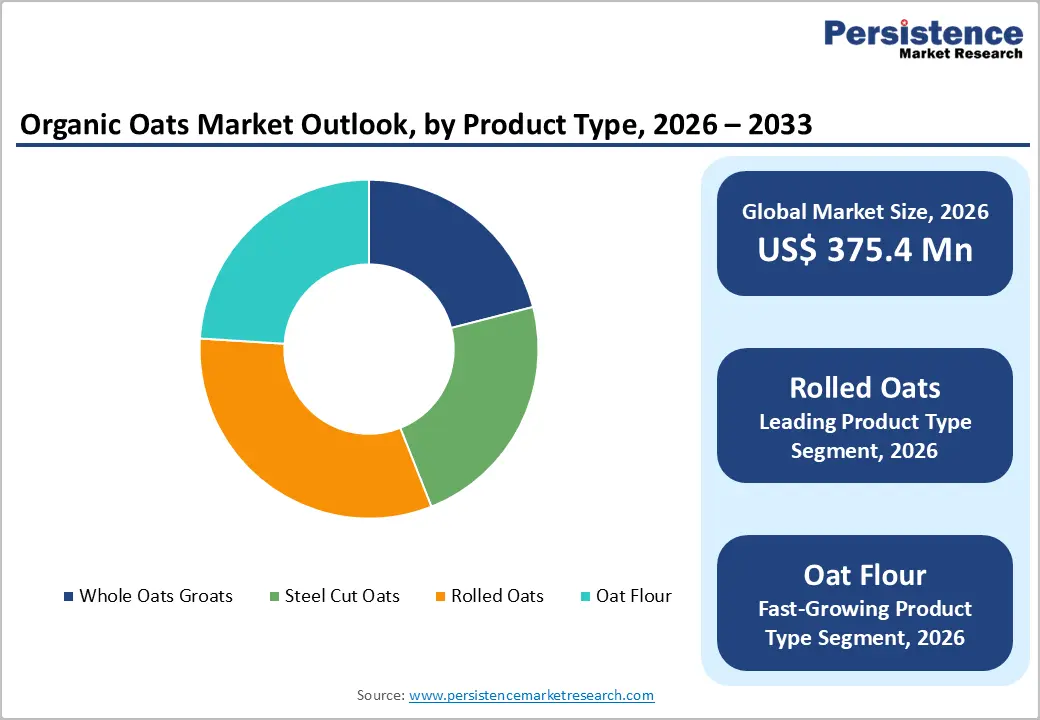

The global organic oats market size is expected to be valued at US$ 375.4 million in 2026 and projected to reach US$ 572.0 million by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This outlook aligns with broader organic food trends, where the global organic market reached about 106 billion euros in 2019 and has continued to expand, reflecting strong consumer preference for certified organic foods.

In the United States alone, certified organic product sales reached approximately US$ 69.7 billion in 2023, up 3.4% year-on-year, driven by categories such as organic breads, grains, and dry breakfast foods that are closely linked to oats consumption.

Key Industry Highlights:

- North America is the leading regional market for organic oats, with the United States organic sector reaching about US$ 69.7 billion in sales and organic grocery categories such as breads, grains, and dry breakfast foods showing robust growth, underpinning strong structural demand for organic oats across breakfast and snack applications.

- Asia Pacific is the fastest-growing region for organic oats, benefiting from expanding organic arable land, rising health and wellness awareness in markets such as China, Japan, and ASEAN, and rapid modernization of retail and e-commerce channels that increase access to organic cereals and oat-based products.

- Among product types, organic rolled oats dominate with an estimated 32% share in 2025, supported by their central role in hot cereal, overnight oats, muesli, granola, and snack bar formulations, and reinforced by continued growth in organic dry breakfast food sales worldwide.

- In end-use applications and channels, the food & beverage industry and B2B ingredient trade lead in organic oats consumption, as processors convert bulk organic oat groats, flakes, and flours into branded cereals, bakery items, beverages, and snacks, while B2C retail and e-commerce channels exhibit rapid growth off a smaller base.

- A key opportunity for market participants is to combine heart-health and whole-grain positioning with functional benefits (such as beta-glucan-linked cholesterol reduction), gluten-free or purity-protocol claims, and sustainable organic farming narratives, supported by innovation in oat-based beverages, bakery, and snack formats that command premium pricing.

| Key Insights | Details |

|---|---|

| Organic Oats Market Size (2026E) | US$ 375.4 million |

| Market Value Forecast (2033F) | US$ 572.0 million |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 5.8% |

Market Dynamics

Drivers - Health benefits of oats and rising preference for heart-healthy whole grains

A key driver of organic oats demand is the strong scientific and regulatory recognition of oats as a heart-healthy whole grain, particularly due to their content of soluble beta-glucan fiber. The European Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA) have both approved health claims stating that daily intakes of about 3 g of oat beta-glucan help lower blood LDL-cholesterol, thereby reducing cardiovascular disease risk. Meta-analyses of randomized controlled trials cited by EFSA indicate that consuming around 3 g of oat beta-glucan per day can reduce LDL-cholesterol by roughly 0.25 mmol/L, equivalent to around a 5-7% decrease. As consumers increasingly seek foods that combine preventive health benefits with convenience, organic oats are perceived as a minimally processed, fibre-rich, and nutrient-dense option that aligns with cholesterol-lowering and weight-management goals. This health halo supports premium positioning for certified organic rolled oats, steel cut oats, and oat-based products in retail and foodservice channels.

Expansion of organic farmland and organic cereals area worldwide

The steady expansion of organic agriculture globally has also strengthened the supply base for organic oats. According to FiBL and IFOAM - Organics International, organic farmland reached about 72.3 million hectares worldwide in 2019, with the global organic food market valued at roughly 106 billion euros and continuing to grow. Within this land base, organic cereal production is a major component: updated statistics for 2023 indicate that more than 5.7 million hectares of cereals were under organic management, representing about 0.8% of the world’s cereal area. Earlier FiBL analyses of organic cereals showed that oats accounted for roughly 12% of global organic cereal area, alongside wheat, barley, maize, rice, and rye, underscoring their importance in organic rotations and product portfolios. As governments in Europe, North America, and parts of Asia promote organic farming through subsidies and action plans, the increased availability of organic cereal raw materials including oats supports scaling of breakfast cereals, bakery, beverage, and snack applications that rely on certified organic oat ingredients.

Restraints - Premium pricing and affordability gaps versus conventional cereals and grains

Despite strong interest in organic products, premium pricing remains a significant restraint for the organic oats market, especially among price-sensitive consumers and in emerging economies. The Organic Trade Association (OTA) reports that U.S. certified organic sales reached about US$ 69.7 billion in 2023, with organic produce, grocery, and beverages all growing in value, but largely due to pricing rather than volume gains. Organic grocery sales including breads, grains, and dry breakfast foods grew around 4.1% to US$ 15.4 billion, while dry breakfast foods alone reached approximately US$ 1.8 billion in sales. These figures underscore both consumer willingness to pay more and the reality that organic remains a premium category. For some households, higher shelf prices for organic oats compared to conventional oats or other staple grains still act as a barrier, limiting volume growth and slowing penetration in mainstream segments.

Agronomic and supply-chain constraints for organic oat production

Another restraint is the relatively small share of global cereal land under organic management and the agronomic challenges of producing high-quality organic oats at scale. FiBL and IFOAM data indicate that, even with recent growth, organic cereals accounted for only about 0.8% of total cereal area in 2023, highlighting the limited base from which to expand supply. Historical analyses of organic cereal production in the mid-2010s similarly showed that oats made up around 12% of organic cereal area, but overall volumes remained modest compared with conventional cereal output. In regions like the European Union, official cereal balance sheets demonstrate that oats represent a relatively small share of total cereal production, which can make organic oat supply more vulnerable to adverse weather, disease pressure, or rotation constraints. These factors can translate into price volatility, occasional shortages for processors, and cautious capacity expansion along the value chain.

Opportunities - Growth of oat-based beverages and plant-based dairy alternatives

Rapid growth in oat-based beverages and plant-based dairy alternatives presents a major opportunity for organic oat processors and brands. The broader organic beverages category in the United States recorded sales of about US$ 9.4 billion in 2023, up 3.9% from the previous year, with functional, plant-forward drinks playing a prominent role in category expansion. Within this space, oat-based drinks have become one of the most visible segments, driven by consumer preferences for lactose-free, vegan, and environmentally friendly options that offer a creamy texture and favorable nutritional profile. As more brands launch organic oat milk, barista-style beverages, and drinkable oat-based blends, demand for certified organic oats especially oat flour and finely milled fractions continues to rise. This creates opportunities for oat millers and ingredient suppliers to develop tailored organic oat bases with specific viscosity, protein, and beta-glucan profiles optimized for beverage applications.

Premiumization, value-added formats, and clean-label bakery and snacks

The second major opportunity is the premiumization of organic oats through value-added formats in bakery, breakfast cereals, and snack categories. OTA and related trade analyses highlight strong performance of organic grocery staples: in the U.S., organic in-store bakery and fresh breads generated around US$ 3.1 billion, while dry breakfast foods including hot cereals and granola reached roughly US$ 1.8 billion in 2023, with growth rates near 8% in some subcategories. These trends favor organic rolled oats, steel cut oats, and oat flour used in artisanal breads, cookies, snack bars, and granolas that emphasize whole-grain content, fiber, and clean labels. Companies can further differentiate by promoting gluten-free purity protocols, regenerative or climate-smart farming stories, and innovative formats such as overnight oats, instant cups, high-protein blends, and savory oat-based snacks. As consumers look for versatile pantry staples that bridge breakfast and snacking occasions, organic oats are well-positioned to capture incremental value through such premium, convenience-oriented launches.

Category-wise Analysis

Product Type Insights

Rolled oats are the leading product type in the organic oats market, accounting for an estimated 32% share of global revenues in 2025. Their dominance reflects their versatility and familiarity: rolled oats form the base for traditional hot oatmeal, cold overnight oats, muesli, granola, and many snack bars and cookies, making them a staple across retail and foodservice channels. FiBL’s breakdown of global organic cereal area in earlier years showed that oats represented about 12% of organic cereal land, underscoring their importance within organic grain rotations and product portfolios. In the U.S., OTA notes that organic dry breakfast foods, where rolled oats are heavily represented, generated about US$ 1.8 billion in sales in 2023, growing faster than several other grocery categories. As more consumers adopt overnight oats routines, seek higher-fiber breakfasts, and experiment with plant-based baking, organic rolled oats are expected to maintain their leadership, even as oat flour and other formats gain traction.

Distribution Channel Insights

From a distribution-channel perspective, business-to-business (B2B) trade currently represents the leading route for organic oats, as large volumes of oats, oat flakes, and oat flour are sold to cereal, bakery, beverage, and snack manufacturers. Ingredient suppliers such as Richardson International report annual oat processing capacities exceeding 360,000 metric tonnes across multiple North American mills, with product lines covering whole groats, steel cut oats, flakes, brans, and flours for major retail and industrial brands. Similarly, Avena Foods positions itself as a leading producer of pure, uncontaminated, organic certified gluten-free oats, supplying ingredient customers worldwide through its Purity Protocol farm-to-table model. These capabilities highlight the scale of B2B flows that underpin organic oat use in branded products. At the same time, business-to-consumer (B2C) channels through supermarkets, health-food stores, and e-commerce are expanding rapidly as consumers buy organic oats directly for home cooking, but overall B2B remains the dominant channel by volume.

Regional Insights

North America Organic Oats Market Trends and Insights

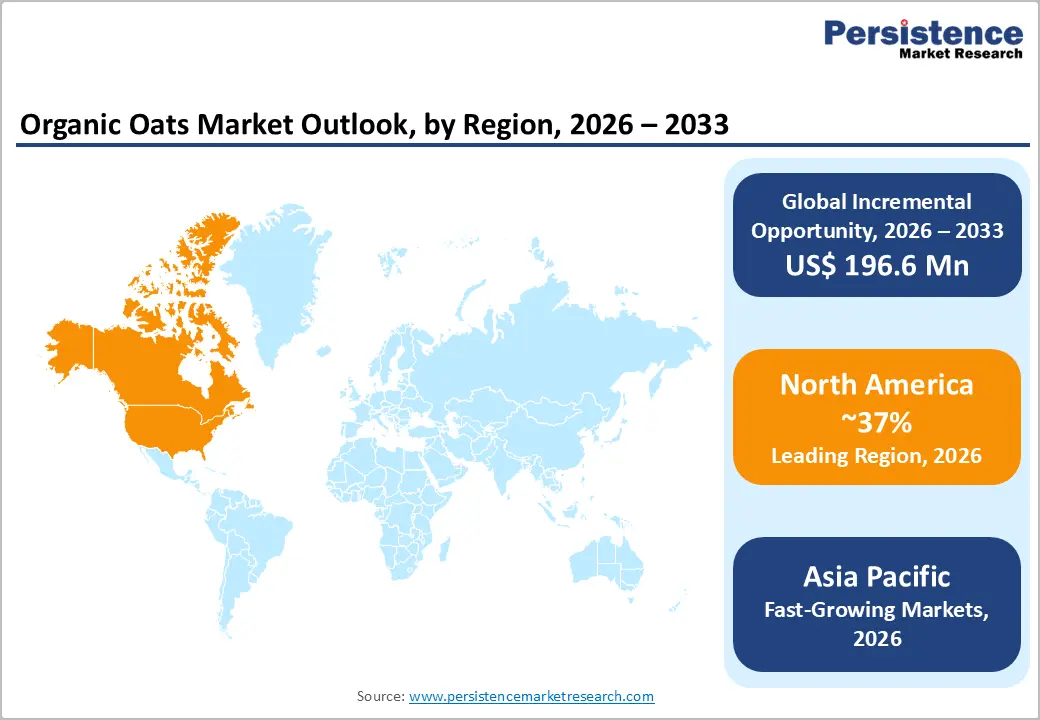

North America is the leading regional market for organic oats, accounting for an estimated 37% share of global organic oats revenues in 2025. The region’s leadership is underpinned by high per-capita cereal consumption, strong health and wellness awareness, and a mature organic certification and retail ecosystem. OTA reports that U.S. certified organic sales reached roughly US$ 69.7 billion in 2023, with organic grocery sales, including breads, grains, and breakfast foods, rising 4.1% to about US$ 15.4 billion. Within this, dry breakfast foods containing oats contributed around US$ 1.8 billion, highlighting the centrality of oats in organic breakfast and snacking patterns.

The regulatory framework in North America supports the continued expansion of the organic oats value chain. The USDA Organic program sets stringent standards for input use, traceability, and certification, while the FDA authorizes heart-health claims for oat beta-glucan, reinforcing consumer trust in oat-based products. Canada, a major oat producer, also plays a crucial role: companies such as Avena Foods and Richardson International operate dedicated facilities for pure, certified organic and gluten-free oats, serving ingredient and retail customers in North America, Europe, and beyond. Together, these factors create a robust innovation ecosystem in which multinational brands and specialized organic players continuously develop new oat-based cereals, snacks, and beverages.

Asia Pacific Organic Oats Market Trends and Insights

Asia Pacific is the fastest-growing regional market for organic oats, supported by rapid urbanization, rising disposable incomes, and an expanding base of health-conscious consumers. Data from FiBL and IFOAM show that Asia accounts for around 23% of global organic arable land, with significant areas dedicated to cereals, and that organic markets in countries such as China, Japan, and South Korea have recorded robust growth in recent years. In parallel, the regional snack and breakfast market is expanding quickly, as evidenced by regional analyses highlighting strong double-digit growth in demand for convenient, healthier, and mood-enhancing snacking options in Asia Pacific. Organic oats benefit from these dynamics as an ingredient in imported and locally manufactured breakfast cereals, granolas, snack bars, and increasingly in oat-based beverages tailored to local taste profiles.

Manufacturing and sourcing advantages further strengthen Asia Pacific’s role in the organic oats value chain. Several countries in the region are major producers and processors of conventional cereals and grains, and are gradually increasing certified organic acreage in response to domestic and export demand. Government nutrition and wellness campaigns in China, India, and ASEAN states often emphasize higher consumption of whole grains and plant-based foods, indirectly supporting interest in oats and other cereals. As cross-border e-commerce platforms, quick-commerce services, and premium supermarket chains proliferate in urban centers, organic oats and oat-based products are gaining shelf visibility and consumer awareness. This combination of supply-side expansion, retail modernization, and lifestyle shifts positions Asia Pacific as the fastest-growing regional market for organic oats over the forecast horizon.

Competitive Landscape

The organic oats market is characterized by a moderately consolidated yet competitive structure, where large-scale producers and processors coexist with numerous regional and niche players. Established participants leverage strong distribution networks, brand positioning, and diversified product portfolios, while smaller companies compete through organic certification, clean-label offerings, and specialty formats such as oat flour and gluten-free products. Competition is increasingly driven by product innovation, sustainability practices, and supply chain transparency, with companies investing in eco-friendly farming and sourcing.

Key Developments:

- In September 2025, Organic Valley expanded its plant-based portfolio by launching two new organic oat-based beverages Original and Creamy made from oats sourced directly from its family farms. The products emphasize a clean-label formulation, being free from gums, seed oils, and artificial additives, while offering improved taste and texture, including enhanced creaminess and frothability for beverages like coffee.

- In May 2026, Clearspring launched a new range of organic oat biscuits as its first entry into sweet, on-the-go snacks, featuring internationally inspired flavors such as miso maple, matcha, and sweet date. The products are made using organic Scottish wholegrain oats, are plant-based, high in fiber, and refined sugar-free, and focus on clean-label ingredients like coconut and olive oil instead of palm oil.

- In November 2025, Canadian brand Yumi expanded its international footprint by launching its organic overnight oats range in Australia, targeting health-conscious and time-poor consumers. The product is positioned as a ready-to-eat, grab-and-go breakfast, featuring soaked (not cooked) oats to retain higher levels of B-vitamins, antioxidants, and prebiotics, while offering low sugar (<6g) and ~210 calories per serving.

Companies Covered in Organic Oats Market

- Richardson International

- Quaker Oats Company

- Avena Foods

- Grain Millers, Inc.

- Bob’s Red Mill Natural Foods

- Fazer Mills

- Helsinki Mills Ltd.

- Ceres Organics

- Kialla Pure Foods

- NOW Foods

- Dutch Organic International Trade

- Nature's Path Foods

- Dancourt

- Saaten-Union GmbH

- Swedish Oat Fiber AB

Frequently Asked Questions

The global organic oats market size is expected to reach approximately US$ 375.4 million in 2026, rising from about US$ 267.7 million in 2020, and setting the stage for continued expansion to around US$ 572.0 million by 2033 at a forecast CAGR of roughly 6.2%.

Demand for organic oats is driven by the heart-health and cholesterol-lowering benefits of oat beta-glucan, growing consumer focus on whole-grain and high-fiber diets, expanding organic farmland and cereal production, and strong performance of organic grocery categories such as breads, grains, and dry breakfast foods that heavily incorporate oats.

North America currently leads the global organic oats market, supported by large and mature organic food markets in the United States and Canada, high per-capita cereal consumption, strong retail and certification infrastructure, and the presence of major oat processors and brands that anchor supply chains and product innovation.

A major opportunity lies in expanding value-added formats such as organic oat-based beverages, functional cereals, bakery, and snack products that leverage beta-glucan health claims, gluten-free or purity-protocol positioning, and regenerative or climate-smart farming stories, thereby capturing premium price points across both B2B and B2C channels.

Notable market participants include Richardson International, Quaker Oats Company, Avena Foods, Grain Millers, Inc., Bob’s Red Mill Natural Foods, Fazer Mills, Helsinki Mills Ltd., Ceres Organics, Kialla Pure Foods, NOW Foods, Dutch Organic International Trade, Nature's Path Foods, Dancourt, Saaten-Union GmbH, and Swedish Oat Fiber AB, along with other regional brands active in organic oat ingredients, cereals, and beverages.