- Pharmaceuticals

- Oral Vaccines Market

Oral Vaccines Market Size, Share, and Growth Forecast, 2026 - 2033

Oral Vaccines Market By Vaccines Type (Live Attenuated Vaccines, Others), Application (Infectious Diseases, Others), Distribution Channel (Hospitals, Clinics, Online Pharmacies, Others), End-user (Pediatrics, Adults, Geriatrics), and Regional Analysis for 2026 - 2033

Oral Vaccines Market Size and Trends Analysis

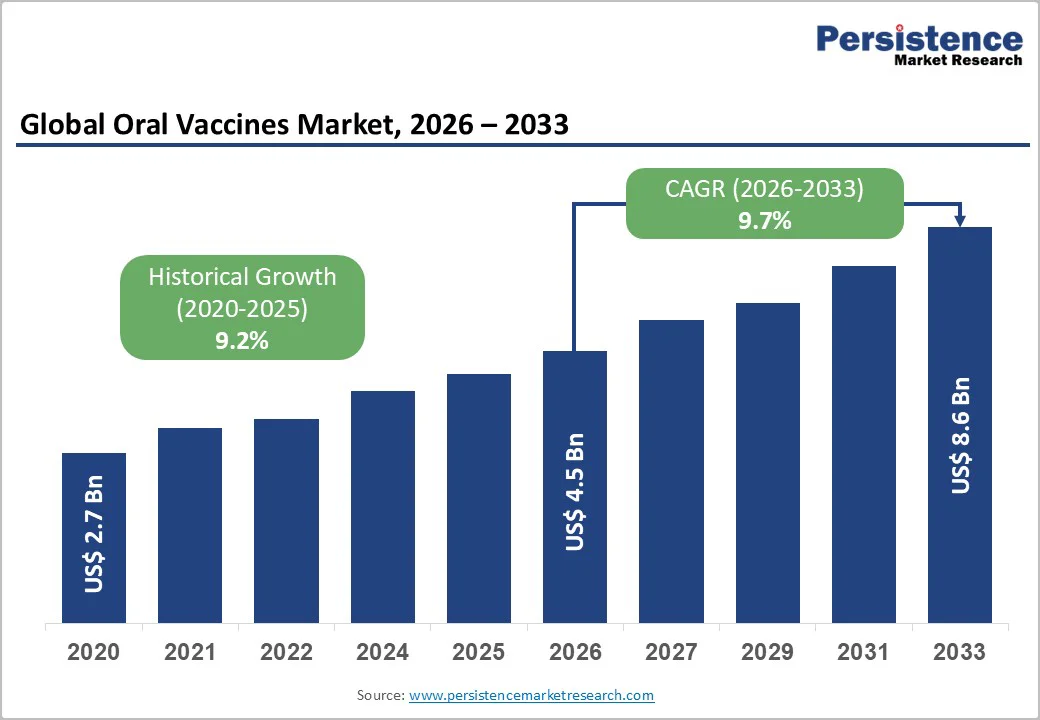

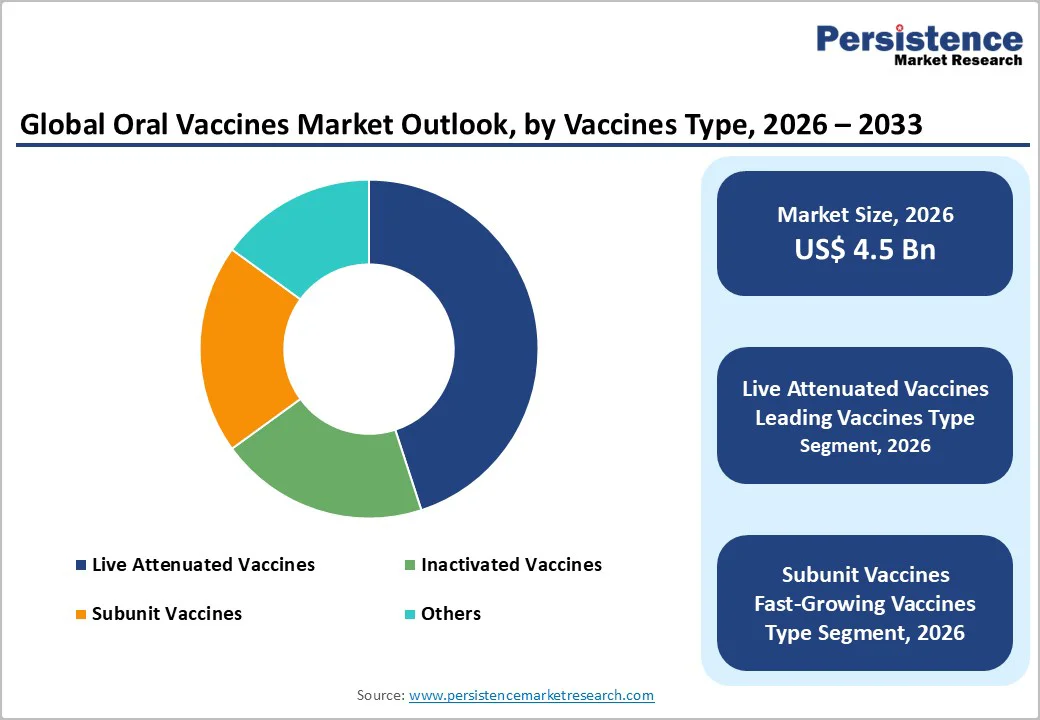

The global oral vaccines market size is likely to be valued at US$4.5 billion in 2026, and is expected to reach US$8.6 billion by 2033, growing at a CAGR of 9.7% during the forecast period from 2026 to 2033, driven by the increasing prevalence of needle-free immunization preferences, rising demand for easy-to-administer vaccines in infectious diseases, and advancements in mucosal delivery technologies.

Growing demand for accessible, stable vaccines, especially for pediatrics, is accelerating the adoption of oral vaccines across demographics. Advances in live attenuated and subunit formulations are further boosting uptake by offering more stable, effective options. Increasing recognition of oral vaccines as critical for health equity in low-resource regions remains a major driver of market growth.

Key Industry Highlights:

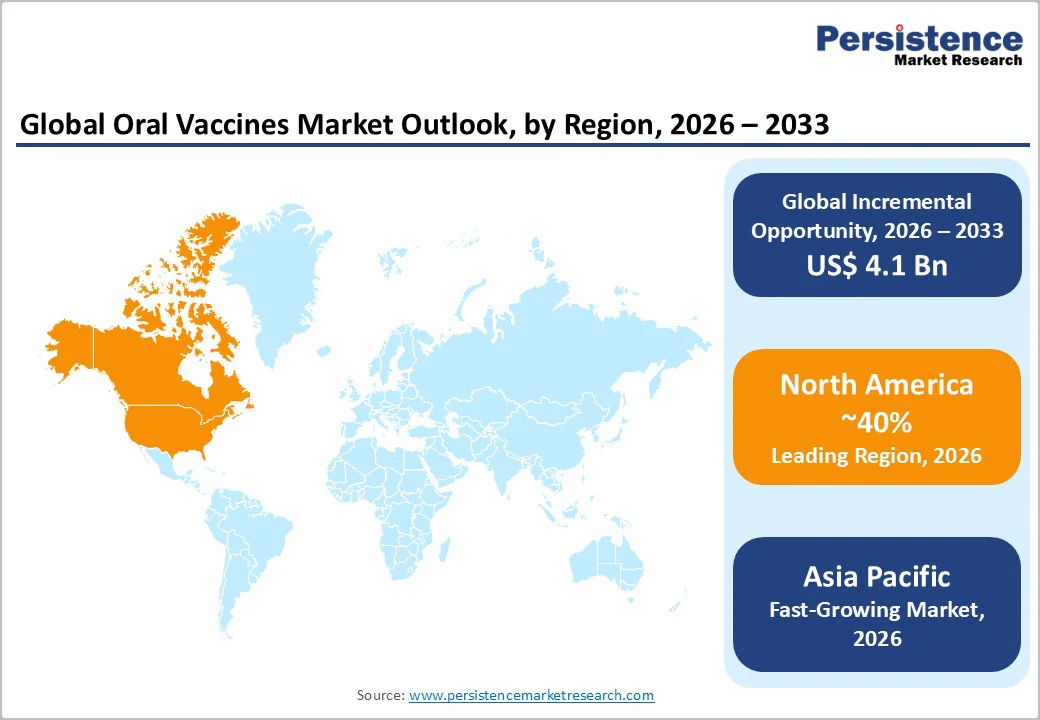

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by advanced vaccine R&D, high prevalence of pediatric immunization, and strong regulatory support in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by increasing vaccination programs, rising awareness of mucosal vaccines, and growing investments in biotech in India and China.

- Dominant Vaccines Type: Live attenuated vaccines, to hold approximately 45% of the market share, as they generate strong, long-lasting immunity by closely mimicking natural infections.

- Leading Application: Infectious diseases account for over 60% of the market revenue, due to high prevalence, ongoing outbreaks, and widespread immunization programs.

- Leading Distribution Channel: Hospitals, contributing nearly 50% of the market revenue, due to their advanced infrastructure, trained staff, and capacity to handle complex or high-risk vaccinations.

- Leading End-user: Pediatrics, with approximately 35% share, due to children requiring routine immunizations as part of national vaccination schedules, ensuring consistent demand.

| Key Insights | Details |

|---|---|

|

Oral Vaccines Market Size (2026E) |

US$4.5 Bn |

|

Market Value Forecast (2033F) |

US$8.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Needle-Free Immunization Preferences and Demand For Easy-To-Administer Vaccines

The rising preference for needle-free immunization is quickly becoming a major opportunity for vaccine developers, driven by growing patient demand for comfort, convenience, and reduced pain. Traditional injections often create fear, especially among children and needle-phobic adults, leading to missed vaccinations and lower compliance rates. Needle-free technologies, including oral vaccines, nasal sprays, microneedle patches, jet injectors, and dissolvable thin films, address these concerns by offering a painless or minimally invasive alternative. These formats simplify administration, reduce the need for trained healthcare workers, and are particularly effective during mass immunization programs or emergency responses where rapid deployment is critical.

Needle-free vaccines significantly lower the risk of needlestick injuries, cross-contamination, and improper disposal, which remain major concerns in healthcare settings. They also support improved cold-chain stability and easier storage, especially for oral and film-based vaccines, making them ideal for low-resource or remote regions. As global health organizations push for wider vaccination coverage and user-friendly delivery methods, demand continues to expand across infectious diseases, travel vaccines, and emerging pathogens.

High Development and Stability Costs

High development and stability costs present a significant barrier for companies advancing next-generation vaccines and novel drug-delivery systems. Developing innovative formulations such as needle-free, oral, intranasal, or microneedle-based vaccines requires extensive research, specialized excipients, and advanced manufacturing technologies that are far more expensive than traditional injectable platforms. Stability is an even greater challenge: many modern biologics, mRNA constructs, and protein-based vaccines are sensitive to temperature, humidity, and light, requiring rigorous optimization to ensure they remain potent throughout storage and distribution. Achieving long-term stability often involves costly formulation trials, sophisticated analytical testing, and the use of high-grade stabilizers, which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for stability data, shelf life, and batch consistency requires multiple stability studies under various conditions and across several production batches. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled environments, specialized equipment, and quality-assurance systems, further driving up overall costs. For smaller biotech companies, these challenges can limit pipeline expansion or delay commercialization.

Advancements in Thermostable and Mucosal Delivery Platforms

Advancements in thermostable and mucosal vaccine delivery platforms are transforming the global immunization landscape by addressing two major challenges, cold-chain dependence and needle-based administration barriers. Thermostable vaccines are engineered to maintain potency at higher temperatures, reducing reliance on refrigeration and enabling safe distribution in remote, resource-limited, or emergency settings. Innovations, such as freeze-dried formulations, lipid-based stabilizers, protein engineering, and viral-vector optimization, significantly improve shelf life and reduce spoilage, lowering logistical costs for healthcare systems and humanitarian campaigns.

Progress in mucosal delivery platforms, including intranasal sprays, oral films, buccal tablets, and gut-targeted capsules, supports more natural immune activation by stimulating mucosal immunity, the body’s first line of defense against respiratory and gastrointestinal pathogens. These formats eliminate needles, enhance patient compliance, and allow self-administration without trained professionals, making them highly suitable for mass vaccination programs. New technologies such as nanoparticle carriers, mucoadhesive polymers, and VLP-based oral vaccines further enhance antigen uptake and immune response.

Category-wise Analysis

Vaccines Type Insights

Live attenuated vaccines are anticipated to dominate the market, accounting for approximately 45% of the market share in 2026. Its dominance is driven by robust immunity, cost-effectiveness, and stability, making it preferred for infectious disease control. Live attenuated vaccines provide gut protection, ensure efficacy, and contribute to herd immunity, making them suitable for large-scale vaccination campaigns. For example, companies such as IOS produce live attenuated vaccines for poultry and livestock, protecting against gastrointestinal infections while supporting mass immunization programs that are both scalable and effective.

Subunit vaccines represent the fastest-growing segment, due to their precision and expanding use in cancer immunotherapies. Their strong safety profile makes them ideal for targeted immune responses, reducing adverse effects. Continuous innovations in advanced adjuvants are further strengthening their efficacy, driving rapid adoption across North America and Europe, where demand for next-generation, high-specificity vaccines is accelerating. For example, pharmaceutical companies are developing subunit vaccines targeting oncogenic viruses and tumor-specific antigens, enabling safer and highly specific immunotherapy options for cancer patients in advanced healthcare markets.

Application Insights

Infectious diseases lead the market, holding approximately 60% of the share in 2026, driven by persistent endemic threats, large immunization programs, and strong global demand for preventive vaccines. Their dominance continues as countries expand vaccination for influenza, RSV, dengue, and HPV. Rising RSV vaccine adoption and expanded dengue immunization campaigns highlight the growing focus on infectious-disease protection. For example, pharmaceutical companies such as GlaxoSmithKline (GSK) supply vaccines such as Shingrix and Dengvaxia for large-scale immunization programs, reducing disease incidence and supporting national vaccination strategies across multiple regions.

Cancer is the fastest-growing segment, due to strong momentum in immunotherapy and expanding inclusion of cancer vaccines in clinical trials. The growing shift toward convenient oral and mucosal delivery platforms, along with better patient tolerance, accelerates the adoption. Advancements in personalized mRNA cancer vaccines and continued progress of therapeutic HPV-related cancer vaccines entering late-stage trials drive market growth. For example, companies such as Moderna and BioNTech are developing personalized mRNA cancer vaccines targeting tumor-specific antigens, enabling highly tailored immunotherapies and showing promising results in clinical studies for melanoma and HPV-associated cervical cancer.

Distribution Channel Insights

Hospitals are expected to dominate the market, contributing nearly 50% of revenue in 2026, due to remaining the primary hubs for vaccination, advanced immunotherapy administration, and management of complex cases requiring physician oversight. Their strong infrastructure, trained staff, and ability to handle high-risk or specialized vaccines drive higher patient volume. Hospitals are leading RSV and HPV vaccination rollouts as well as administering emerging cancer vaccine trials. For example, large healthcare systems such as Mayo Clinic routinely conduct RSV and HPV immunization programs while also participating in clinical trials for personalized cancer vaccines, ensuring patients receive specialized, supervised care with high safety standards.

Clinics represent the fastest-growing segment, driven by their strong community presence and expanding role in primary care vaccination. They offer convenient, quick, and accessible immunization services, attracting patients who prefer local, low-wait-time settings. Increased outreach programs, preventive-care focus, and wider availability of routine and travel vaccines further accelerate patient flow, boosting rapid adoption across both urban and semi-urban areas. For example, community clinics such as CVS MinuteClinic in the U.S. provide walk-in vaccination services for influenza, HPV, and travel vaccines, making immunizations more accessible to local populations while reducing pressure on hospitals.

End-user Insights

The pediatrics segment is likely to dominate the market, with approximately 35% share in 2026, due to the high volume of routine childhood immunizations and strong global emphasis on early disease prevention. Regular vaccination schedules, school-entry requirements, and widespread access to pediatric care drive consistent demand. Rising focus on vaccines for RSV, HPV, and influenza in children further strengthens pediatric market leadership. For example, pediatric hospitals and clinics such as Boston Children’s Hospital administer routine immunizations, including RSV, influenza, and HPV vaccines, ensuring high coverage in children while supporting early preventive healthcare initiatives.

Geriatrics is the fastest-growing field, driven by the rising need for boosters, vulnerability to severe infections, and expanding adoption of age-specific vaccines. Improved safety profiles, tailored dosing, and stronger immunogenicity for older adults support rapid uptake. The growing use of influenza, pneumococcal, RSV, and shingles vaccines among aging populations further accelerates market growth. For example, senior-focused clinics and programs such as Kaiser Permanente’s senior vaccination initiatives provide targeted influenza, pneumococcal, and shingles vaccines, protecting older adults and reducing the risks of severe infectious diseases in aging populations.

Regional Insights

North America Oral Vaccines Market Trends

North America is projected to account for nearly 40% of the global oral vaccines market in 2026, driven by the region’s advanced healthcare infrastructure, strong research and development capabilities, and high public awareness of immunization benefits. Healthcare systems in the U.S. and Canada provide extensive support for vaccination programs, ensuring wide accessibility of oral vaccines across pediatric, adult, and geriatric populations. Increasing demand for needle-free, convenient, and easy-to-administer vaccines is further accelerating adoption, as these formats improve patient compliance and reduce barriers associated with traditional injections.

Innovation in oral vaccine technology, including stable formulations, improved antigen delivery, and targeted mucosal immunity, is attracting significant investment from both public and private sectors. Government initiatives and public health campaigns continue to promote vaccination against endemic infectious diseases, seasonal influenza, and emerging pathogens, creating sustained market demand. The growing focus on adult and booster immunizations, particularly for respiratory and gastrointestinal diseases, is expanding the target population for oral vaccines.

Europe Oral Vaccines Market Trends

Europe is projected to lead with a market share of 25% in 2026, driven by increasing awareness of vaccination benefits, strong healthcare systems, and government-led immunization programs. Countries such as Germany, France, and the U.K. have well-established public health frameworks that support routine immunizations and encourage adoption of innovative vaccine delivery methods, including oral vaccines. These non-invasive formulations are particularly appealing for pediatric populations, needle-averse adults, and geriatric patients, improving compliance and coverage rates.

Technological advancements in oral vaccine development, such as enhanced stability, mucosal-targeted delivery, and improved antigen formulations, are further boosting market potential. European health authorities are increasingly supporting research and clinical trials for oral vaccines against both endemic and emerging infectious diseases, strengthening market confidence. The growing emphasis on convenient, self-administered immunization options is aligned with the region’s focus on preventive healthcare and reducing hospital visits. Public awareness campaigns and vaccination drives are expanding reach in both urban and rural areas, while pharmaceutical companies are investing in adjuvants and novel formulations to increase efficacy.

Asia Pacific Oral Vaccines Market Trends

Asia Pacific is likely to be the fastest-growing market for oral vaccines in 2026, driven by rising healthcare awareness, increasing government initiatives, and expanding immunization programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting vaccination campaigns to address endemic infectious diseases and emerging pathogens. Oral vaccines are particularly attractive in these regions due to their needle-free administration, ease of distribution, and suitability for large-scale immunization drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-administer oral vaccines, which can withstand challenging storage conditions and minimize cold-chain dependence. These innovations are critical for reaching remote areas and improving overall vaccination coverage. Growing demand for pediatric, adult, and booster immunizations is contributing to market expansion. Public-private partnerships, increased healthcare expenditure, and rising investment in vaccine research and manufacturing capacity are further accelerating growth. The convenience of oral delivery, combined with improved patient compliance and reduced risk of needlestick injuries, positions oral vaccines as a preferred choice.

Competitive Landscape

The global oral vaccines market features competition between established pharmaceutical leaders and emerging biotech firms. In North America and Europe, Sanofi and GSK lead through strong R&D, distribution networks, and healthcare ties, bolstered by innovative formulations and immunization programs. In Asia Pacific, Oravax Medical advances with localized solutions, enhancing accessibility. Mucosal needle-free delivery boosts compliance, cuts injection risks, and enables mass campaigns across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand pipelines, and speed commercialization. Thermostable formulations solve storage issues, aiding penetration in resource-limited areas.

Key Developments

- In August 2025, the University of Oxford, in collaboration with Upperton Pharma Solutions, launched a strategic initiative after securing funding from the first VaxHub Sustainable Platform Funding Call to advance an oral formulation of Adenovirus-vectored vaccines. Led by Professor Dame Sarah Gilbert, the project aims to overcome the limitations of intramuscular delivery by enabling mucosal immunity, enhancing vaccine stability, simplifying distribution, and supporting self-administration, positioning oral vaccines as a scalable, patient-friendly alternative for future immunization programs.

- In May 2025, Bharat Biotech announced that its oral cholera vaccine Hillchol successfully completed Phase III clinical trials in India (1,800 participants), demonstrating non-inferiority versus the existing licensed vaccine (Shanchol) for both Ogawa and Inaba serotypes, along with a strong safety profile.

Companies Covered in Oral Vaccines Market

- Sanofi

- GSK

- IOS

- Takeda Pharmaceuticals

- Soligenix

- Liquidia Technologies

- Elasmogen

- Oravax Medical

- Rapid Dose Therapeutics

- AVRO Life Science

- Prokarium Ltd

- Matinas Biopharma

- ACM Biolabs

Frequently Asked Questions

The global oral vaccines market is projected to reach US$4.5 billion in 2026.

The rising prevalence of needle-free immunization preferences and demand for easy-to-administer vaccines are key drivers.

The oral vaccines market is poised to witness a CAGR of 9.7% from 2026 to 2033.

Advancements in thermostable and mucosal delivery platforms are key opportunities.

Sanofi, GSK, Takeda Pharmaceuticals, Oravax Medical, and Prokarium Ltd are the key players.