- Pharmaceuticals

- U.S. Oral Clinical Nutrition Supplement Market

U.S. Oral Clinical Nutrition Supplement Market Size, Share, and Growth Forecast, 2025 - 2032

U.S. Oral Clinical Nutrition Supplement Market By Form (Liquid, Semi-solid, Powder), Clinical Indication (Malnutrition, Oncology, Surgical/Perioperative Nutrition, Others), Sales Channel (Online Sales, Retail Sales, Institutional Sales), and Regional Analysis for 2025 - 2032

U.S. Oral Clinical Nutrition Supplement Market Size and Trends Analysis

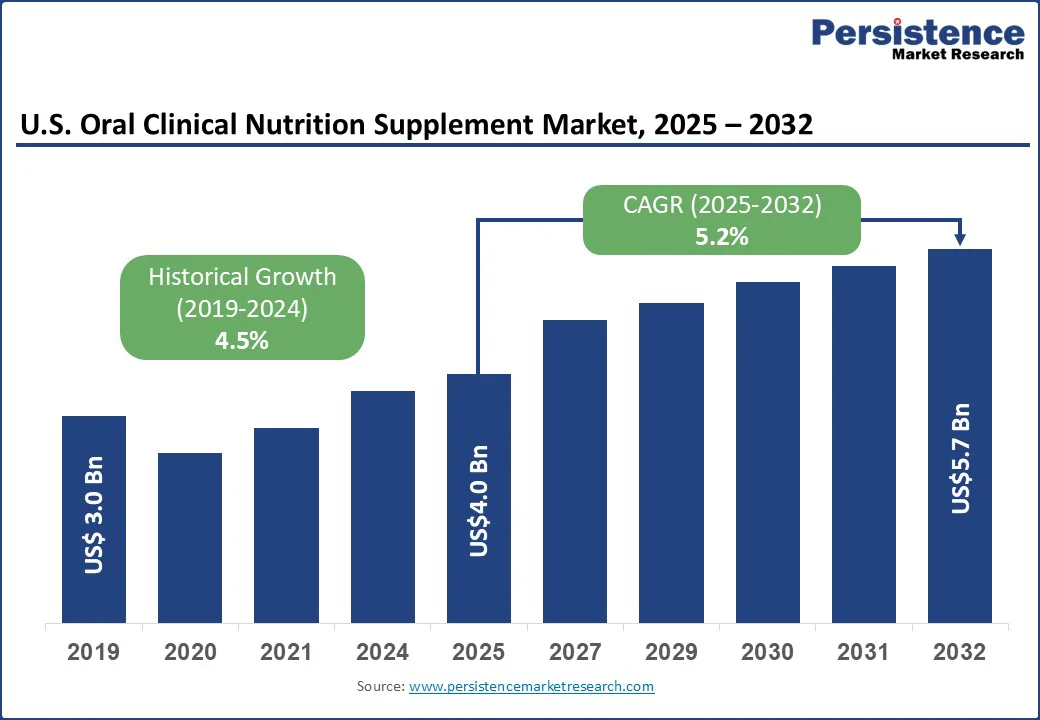

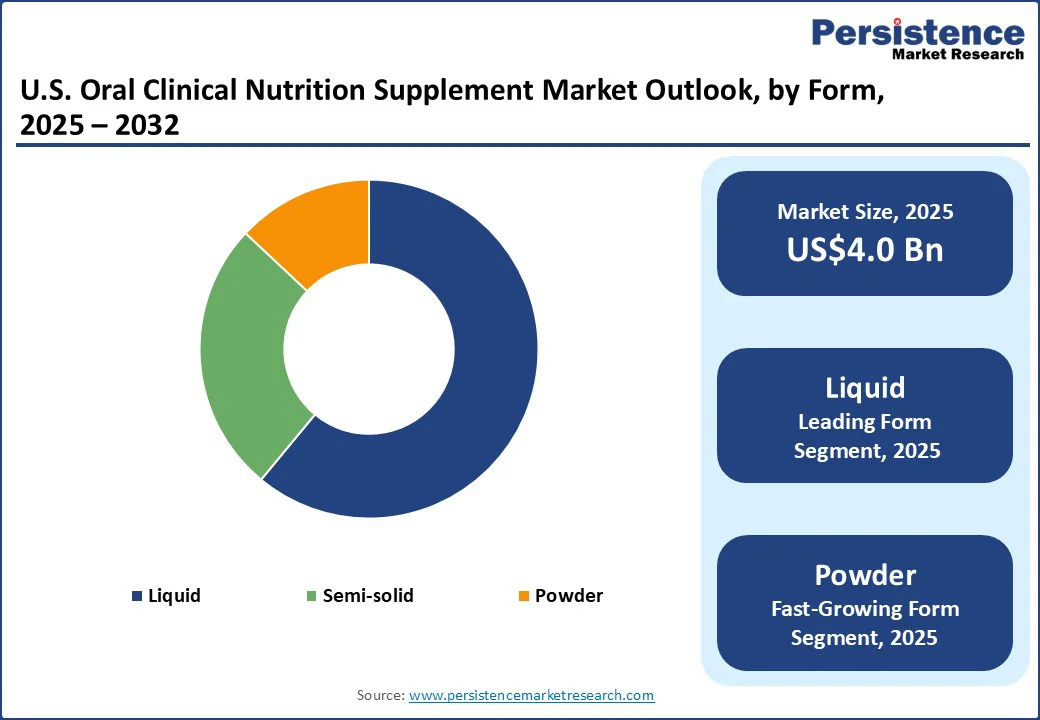

The U.S. oral clinical nutrition supplement market size is likely to be valued at US$4.0 Bn in 2025 and is expected to reach US$5.7 Bn by 2032, growing at a CAGR of 5.2% during the forecast period from 2025 to 2032, supported by an aging population, rising chronic disease burden, and greater focus on medical nutrition in patient recovery.

Key Industry Highlights:

- Fastest-Growing Form: Powdered supplements, expanding rapidly due to affordability, ease of storage, and growing adoption for home-based care and chronic disease management.

- Form Leader: Liquid supplements dominate the U.S. oral clinical nutrition supplement market with over 61.6% share in 2025, widely used in hospitals, elderly care, and for patients with swallowing difficulties.

- Dominant Distribution Channel: Institutional sales account for ~50.7% of market share in 2025, driven by hospitals, long-term care facilities, and clinical prescriptions.

- Emerging Opportunity: Online sales growth, fueled by digital health platforms, subscription models, and increasing patient preference for home delivery and personalized nutrition solutions.

| Key Insights | Details |

|---|---|

| U.S. Oral Clinical Nutrition Supplement Market Size (2025E) | US$4.0 Bn |

| Market Value Forecast (2032F) | US$5.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

High Prevalence of Chronic Diseases in the U.S.

Chronic disease prevalence is one of the strongest drivers of the U.S. oral clinical nutrition supplement market, as more Americans require long-term nutritional support to manage illness and recovery. According to the CDC, in 2023, about 76.4% of U.S. adults had at least one chronic condition, and 51.4% lived with two or more.

Even younger adults are impacted, with nearly 60% of those aged 18-34 reporting at least one chronic illness, while the figure rises to 93% in seniors aged 65 and above.

Obesity, which affects 40.3% of adults, and diabetes, impacting more than 38 million Americans, further compound nutritional risks, often leading to sarcopenia, malnutrition, or poor surgical recovery.

Chronic conditions drive nearly 90% of the nation’s US$4.1 Tn healthcare spending, making supportive therapies such as oral nutrition supplements essential. These products help improve patient outcomes, reduce complications, and are increasingly integrated into chronic disease management pathways.

Palatability & Compliance Issues Acts a Barrier for Adoption for Diet-sensitive Patients

Palatability and patient compliance act as critical restraints to the U.S. oral clinical nutrition supplement market. Although average adherence is relatively high, at around 78%, with variability ranging from 37% to 100%, factors such as flavor, texture, and sensory appeal largely determine intake levels. Trials show patients strongly prefer milk-based flavors (pleasantness ~6.2/10) over fruit-juice or savory versions, with 81.6% selecting milk-based options when offered.

Chocolate flavors, for instance, led to daily consumption of nearly 2 units per day, outperforming vanilla and strawberry variants. Meanwhile, chemotherapy-induced taste alterations, such as metallic or off-flavors in juice-based products, negatively affect palatability, whereas strawberry formulations maintain consistent acceptance even during treatment.

These findings highlight how sensory challenges directly impair adherence, reducing the effectiveness of oral nutrition therapy, especially among vulnerable populations in clinical settings.

Personalized & Disease-Specific Formulations

The growing prevalence of chronic and specialized health conditions presents a major opportunity for personalized and disease-specific oral clinical nutrition supplements in the U.S. Millions of Americans are living with conditions such as cancer, diabetes, and chronic kidney disease, many of whom have unique nutritional needs that standard supplements cannot fully address.

Cancer patients often require high-protein, energy-dense formulations to counteract weight loss and muscle wasting, while individuals with diabetes benefit from low-sugar, controlled-carbohydrate products.

Patients with renal or gastrointestinal disorders require electrolyte- and nutrient-adjusted supplements to support organ function without overloading compromised systems. Despite the high burden of these conditions, many patients struggle to find tailored solutions, highlighting a significant gap in the market.

By developing formulations customized to specific diseases, manufacturers can improve patient adherence, optimize clinical outcomes, and expand U.S. oral clinical nutrition supplement market penetration. This opportunity aligns with the broader trend toward personalized medicine and preventive healthcare, making disease-specific oral nutrition a key growth area.

Category-wise Analysis

Form Insights

Liquid clinical nutrition supplements are leading the U.S. oral clinical nutrition supplement market due to their ease of use, faster absorption, and higher patient compliance compared to other formats.

Studies indicate that patients are more likely to accept a nutrition therapy program if the oral nutritional supplement (ONS) has a good taste and minimal adverse reactions. For instance, a study found that respondents were 93.73% more likely to accept a nutrition therapy program when adverse reactions were minimal compared to when they occurred frequently.

Additionally, the flavor of the supplement plays a significant role in patient acceptance, with "good taste" being a highly valued attribute.

These factors contribute to the preference for liquid forms, which are ready-to-use, require no mixing, and are easier to swallow, especially for patients with swallowing difficulties or those undergoing treatments such as chemotherapy. Consequently, liquid supplements are increasingly prescribed in clinical settings, leading to higher adherence rates and better nutritional outcomes.

Clinical Indication Insights

Malnutrition is the leading clinical indication driving the U.S. market due to its high prevalence among hospitalized and elderly populations. According to recent studies, nearly one in three hospitalized patients in the U.S. is at risk of malnutrition, with older adults particularly affected due to frailty, chronic illnesses, and reduced appetite.

Malnutrition is associated with longer hospital stays, higher readmission rates, and increased healthcare costs, creating a strong need for nutritional intervention. Oral clinical nutrition supplements provide a convenient, nutrient-dense solution to address protein-energy deficits, support recovery, and improve overall health outcomes.

The high clinical focus on prevention and treatment of malnutrition makes this indication the primary driver of product adoption across hospitals, long-term care facilities, and home-based care settings.

Competitive Landscape

The U.S. oral clinical nutrition supplement market is competitive, led by global giants such as Abbott, Nestlé Health Science, Danone Nutricia, Fresenius Kabi, and B. Braun. These companies focus on disease-specific, high-protein, and plant-based formulations, while emerging players innovate in taste, texture, and convenient packaging to improve adherence, targeting hospitals, elderly care, and home-based nutrition markets.

Key Industry Developments

- In June 2024, Nestlé Health Science launched a comprehensive GLP-1 Nutrition Support Platform in the U.S. This platform aims to assist individuals on their weight management journey, particularly those using GLP-1 medications such as Ozempic and Wegovy.

- In June 2024, Nestlé Health Science announced the acquisition of global rights to VOWST® (fecal microbiota spores, live-brpk) capsules from Seres Therapeutics. This strategic move grants Nestlé full control over the development, commercialization, and manufacturing of VOWST worldwide.

Companies Covered in U.S. Oral Clinical Nutrition Supplement Market

- Abbott Laboratories

- Nestlé Health Science

- Danone Nutricia

- Fresenius Kabi

- B. Braun Melsungen AG

- Perrigo Company plc

- Reckitt Benckiser Group plc

- Medtrition Inc.

- Hormel Health Labs

- Kate Farms

- Ajinomoto Cambrooke

- Aymes Nutrition

Frequently Asked Questions

The U.S. oral clinical nutrition supplement market is projected to be valued at US$4.0 Bn in 2025.

Aging population, chronic diseases, home healthcare growth, product innovation, and insurance integration drive market demand.

The U.S. oral clinical nutrition supplement market is poised to witness a CAGR of 5.2% between 2025 and 2032.

Personalized formulations, home-based care, plant-based products, digital health integration, and preventive nutrition drive growth opportunities.

Major players in the U.S. oral clinical nutrition supplement market are Abbott Laboratories, Nestlé Health Science, Danone Nutricia, Fresenius Kabi, B. Braun Melsungen AG, and Perrigo Company plc.