- Medical Devices

- Oral Wound Dressing Market

Oral Wound Dressing Market Size, Share, and Growth Forecast, 2026 – 2033

Oral Wound Dressing Market by Content Type (Collagen, Oxidized regenerated cellulose, Others), Application (Minor oral wounds, Closure of grafted sites, Repair of Schneiderian membrane), End-user (Hospitals, Dental Clinics), and Regional Analysis 2026 – 2033

Oral Wound Dressing Market Size and Trends Analysis

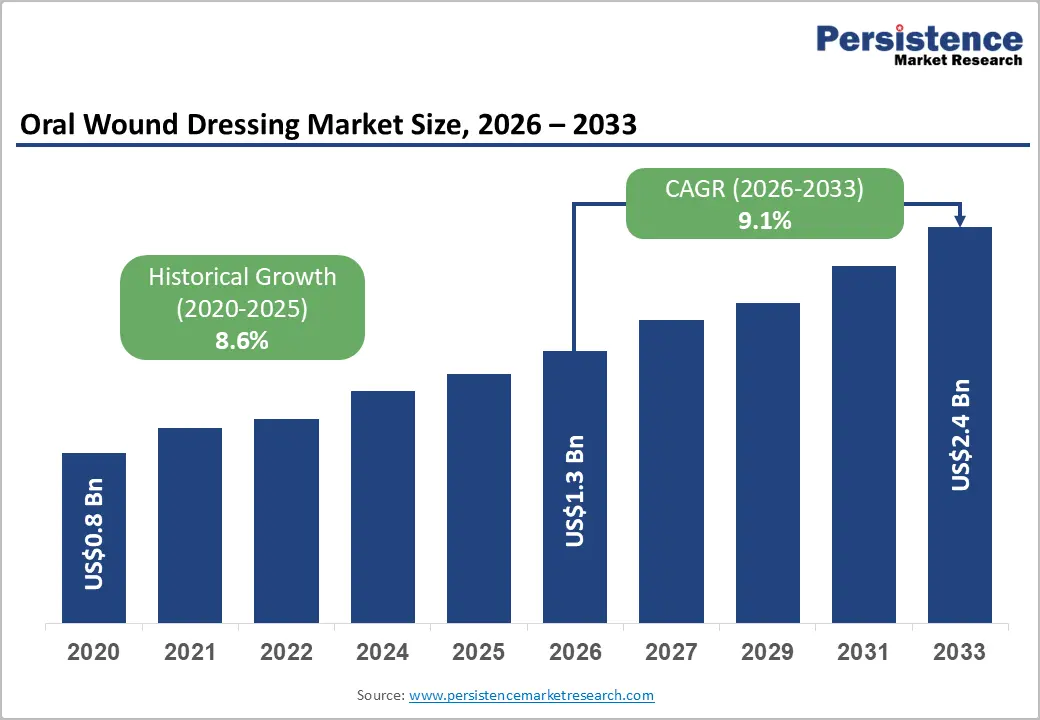

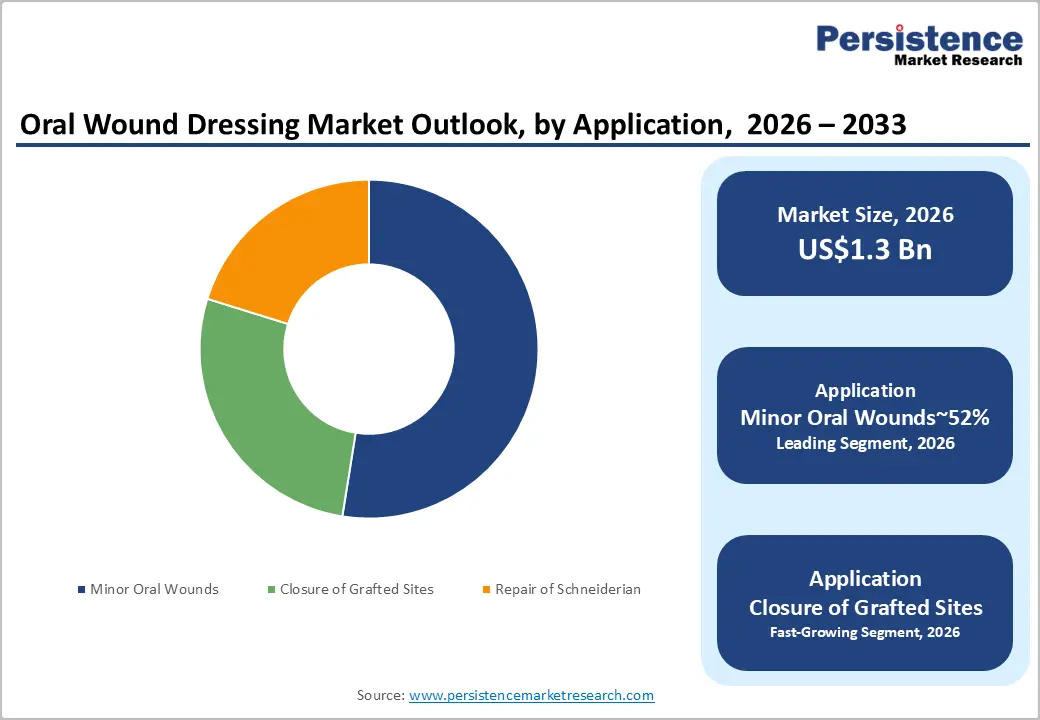

The global oral wound dressing market size is likely to be valued at US$1.3 billion in 2026 and is expected to reach US$2.4 billion by 2033, growing at a CAGR of 9.1% during the forecast period from 2026 to 2033, driven by increasing dental implant procedures that consistently accelerate structural product procurement across multiple care settings.

Rising surgical volumes directly necessitate advanced regenerative clinical materials securing optimal patient recovery. This escalating clinical demand reliably ensures sustained category momentum throughout the forecast horizon. Agencies strongly encourage continuous modernization across specialized therapeutic delivery environments globally.

Key Industry Highlights:

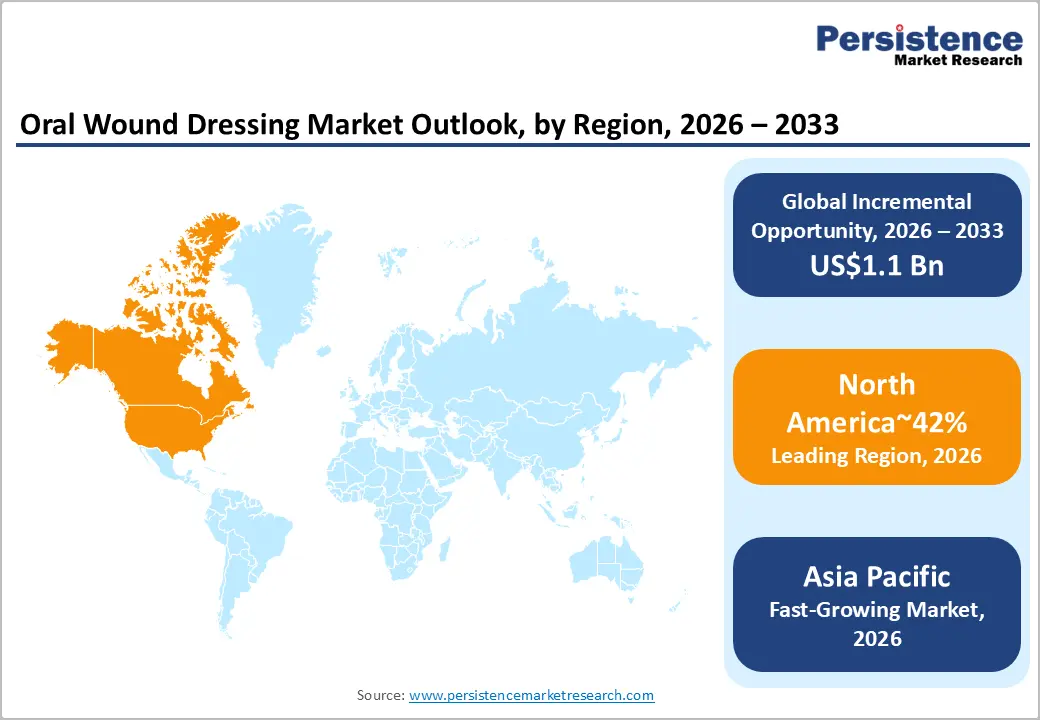

- Leading Region: North America is projected to lead, accounting for approximately 42% share in 2026, supported by deeply entrenched advanced healthcare infrastructure networks and high elective procedural volumes.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by rapid private healthcare infrastructure buildouts and massive middle-class demographic expansions.

- Leading Content Type: Collagen is expected to lead, accounting for approximately 29% share in 2026, anchored by exceptional natural physiological tissue compatibility and rapid cellular migration properties.

- Leading Application: Minor oral wounds are anticipated to dominate, accounting for approximately 52% share in 2026, anchored by overwhelmingly high routine clinical incident frequencies and standard extraction protocols.

| Key Insights | Details |

|---|---|

| Oral Wound Dressing Market Size (2026E) | US$1.3 Bn |

| Market Value Forecast (2033F) | US$2.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.6% |

DRO Analysis

Driver Analysis –Expansion of Ambulatory Care Networks Reshaping Hemostatic Material Demand

The rapid expansion of ambulatory care networks is fundamentally restructuring procurement dynamics for surgical consumables across decentralized treatment environments. Independent outpatient practices are increasingly performing complex maxillofacial and dental procedures traditionally confined to hospital settings, redistributing demand across fragmented clinical nodes. Outpatient facilities prioritize versatile, easy-to-handle consumables that integrate seamlessly into chairside interventions, reducing procedural complexity and minimizing reliance on centralized inventory systems. Consequently, demand patterns are shifting toward scalable, multi-indication hemostatic solutions compatible with varied clinical settings. These structural changes collectively broaden market participation while reinforcing the importance of logistical agility.

Distributed care delivery intensifies requirements for infection control, sterility assurance, and predictable clinical performance across diverse practice environments. Absorbable hemostatic materials with consistent degradation profiles and minimal handling complexity are gaining preference, enabling faster patient throughput and optimized resource utilization. Manufacturers are aligning product design with outpatient workflow efficiencies, incorporating biocompatible materials and simplified application mechanisms to reduce training burdens. These dynamics stabilize demand visibility and reinforce recurring consumption patterns, supporting sustained revenue generation across the hemostatic materials segment.

Implantology Expansion and Protocol Standardization: Elevating Hemostatic Biomaterial Demand

The accelerating adoption of dental implantology is structurally increasing demand for advanced hemostatic dressings designed for graft stabilization and infection control. Rising procedural volumes across restorative dentistry workflows are embedding biomaterial usage into routine clinical protocols, particularly in grafted and surgically manipulated sites. This shift compels providers to prioritize materials that ensure rapid clot formation, membrane stabilization, and predictable healing trajectories under time-constrained outpatient conditions. As implant procedures scale across urban and peri-urban clinical networks, procurement patterns increasingly favor standardized, high-performance consumables compatible with repeatable surgical outcomes. These dynamics reinforce a transition from discretionary usage toward protocol-driven integration of hemostatic biomaterials within implant workflows.

The formalization of osseointegration protocols mandates consistent soft tissue management through protective membranes and engineered scaffolds. Clinical guidelines increasingly displace traditional healing approaches, emphasizing biomaterials that support aesthetic outcomes and keratinized tissue regeneration. Manufacturers are responding with collagen-based matrices and resorbable dressings tailored for implant interfaces, aligning with practitioner demand for predictable clinical performance. The convergence of protocol rigor, aesthetic expectations, and material innovation is driving sustained utilization and recurring inventory cycles within the premium hemostatic biomaterials segment.

Restraint Analysis – Biomaterial Sourcing Constraints Limiting Scalable Production Efficiency

Stringent xenograft purification standards significantly constrain the availability of compliant biological raw materials globally. Regulatory frameworks impose strict oversight on animal tissue sourcing and processing methodologies. These compliance requirements extend validation timelines and delay throughput across manufacturing operations. Limited input availability restricts manufacturers from achieving consistent production scale efficiencies. Consequently, supply volatility introduces uncertainty across downstream distribution and clinical utilization channels. These structural frictions collectively suppress responsiveness to rising demand within biomaterial-intensive surgical segments.

The complex processing techniques elevate operational costs and extend production timelines. Advanced crosslinking and sterilization protocols require specialized infrastructure and technical expertise deployment. Validation procedures across multiple jurisdictions further intensify compliance burdens and approval timelines. Production interruptions directly affect distribution continuity and weaken service reliability for clinical providers. Cost structures remain elevated due to stringent quality assurance and traceability requirements. These inefficiencies reduce margin flexibility and constrain competitive pricing strategies within the market. Collectively, sourcing limitations and processing complexity hinder rapid capacity expansion and scalability.

Raw Material Volatility Disrupting Hemostatic Supply Stability

Volatility in collagen and cellulose sourcing disrupts consistent production planning for hemostatic materials globally. Dependence on geographically concentrated raw material streams exposes manufacturers to supply-side shocks and pricing fluctuations. Input cost instability directly compresses margins, particularly within price-sensitive healthcare procurement environments. These fluctuations complicate long-term contracting and reduce predictability across procurement and inventory cycles. Manufacturers face constrained flexibility in scaling output amid uncertain raw material availability conditions. Consequently, production planning remains reactive, limiting the ability to meet expanding clinical demand consistently. This structural instability dampens confidence across distribution networks and slows category-wide growth momentum.

Procurement strategies increasingly incorporate diversification and buffer inventory to mitigate disruptions. However, stockpiling introduces working capital pressures and does not fully offset supply inconsistencies. End-users respond by rationing advanced hemostatic dressings, prioritizing critical procedures over routine applications. This selective utilization weakens overall consumption intensity across outpatient and surgical care settings. Persistent volatility also influences product mix decisions, favoring cost-stable alternatives over premium biomaterials. Regulatory and quality constraints further restrict the rapid substitution of raw material inputs. These dynamics constrain utilization rates and limit scalable expansion within the hemostatic materials market.

Opportunity Analysis – Bioactive Scaffold Integration

Emerging tissue engineering paradigms are redefining regenerative healing through integration of bioactive scaffold technologies. Incorporation of growth factors within structural membranes enhances cellular signaling and accelerates tissue regeneration. These innovations shift biomaterials from passive barriers toward active participants in physiological repair processes. Clinicians increasingly demand solutions that stimulate predictable healing while reducing postoperative complications and recovery variability. This evolution elevates product differentiation and supports premium positioning across advanced surgical and dental applications. The bioactivity integration is expanding the functional scope and value proposition of hemostatic biomaterials.

The manufacturers are investing in biomimetic design and controlled delivery systems to optimize therapeutic outcomes. Advanced formulations incorporating microsphere-based carriers and engineered matrices enhance localized bioavailability of regenerative agents. These technologies enable targeted tissue interaction while maintaining structural integrity and resorption predictability. Clinical adoption is reinforced by improved procedural efficiency and superior healing consistency across diverse patient profiles. This merging of material science and regenerative medicine is unlocking high-value clinical niches and expanding market segmentation opportunities.

Personalized Regenerative Solutions Enabling Precision Biomaterial Adoption

Advancements in three-dimensional bioprinting of collagen are enabling the development of patient-specific regenerative dressings. These technologies allow precise anatomical conformity, improving graft stability and localized healing outcomes significantly. Integration with digital dentistry workflows strengthens alignment between diagnostic imaging and scaffold fabrication processes. Patient-centric treatment planning is accelerating adoption across implantology and complex oral reconstruction procedures. Regulatory acceptance of customized biologics is gradually reducing barriers to commercialization and clinical deployment. This convergence enhances differentiation by shifting biomaterials toward precision-engineered therapeutic solutions. Consequently, personalized scaffolds expand clinical applicability while supporting premium pricing and specialized care pathways.

Integra LifeSciences, through its Gentrix platform, is advancing regenerative matrix technologies and driving the evolution of next-generation treatment platforms. Healthcare providers are increasingly forming strategic partnerships within implantology-focused centers to enhance clinical capabilities. Manufacturers are transitioning toward platform-based regenerative solutions that enable scalable customization. Production approaches are incorporating digital design tools, advanced fabrication technologies, and optimized biocompatible materials, increasing both sophistication and efficiency. Although these advancements introduce greater operational complexity, they also create strong technological advantages for early adopters. Clinicians benefit from enhanced procedural consistency and fewer intraoperative adjustments. Overall, these developments are improving product differentiation and opening new opportunities within specialized regenerative care segments.

Category–wise Analysis

Content Type Insights

Collagen is expected to lead, accounting for approximately 29% share in 2026, anchored by natural physiological tissue compatibility. Innate biochemical properties actively facilitate rapid cellular migration patterns. Zimmer Biomet with Zimmer CollaPlug effectively leverages these inherent advantages. Practitioners highly value predictable resorption during complex reconstructive procedures. Integra LifeSciences with HeliTape delivers consistent localized hemostatic control.

Coloplast with BioPatch and Integra LifeSciences with Gentrix reinforce this dominance through antimicrobial matrices proven in implant procedures. Specialized crosslinking techniques further enhance specific baseline material durability. Surgeons universally prefer materials mimicking endogenous structural connective tissues. Such structural familiarity continuously guarantees formidable ongoing commercial procurement.

Oxidized regenerated cellulose is anticipated to be the fastest-growing segment, driven by superior, rapid hemostatic deployment capabilities. Advanced structural weaving techniques significantly improve critical intraoperative handling. Surgeons frequently require instantaneous bleeding cessation across compromised surgical sites. Johnson & Johnson, with Surgicel, provides proven localized efficacy. Medtronic with Opcima and Johnson & Johnson with Promogran exemplify transitions to precise ORC platforms for Schneiderian applications.

Escalating acute procedural volumes consistently accelerate specific material procurement. Biodegradable characteristics eliminate secondary traumatic removal procedure. Data-integrated variants enhance audit compliance in clinics. Utilization gains traction as procedural complexities rise, expanding ecosystem roles.

Application Insights

Minor oral wounds are projected to lead, accounting for approximately 52% share in 2026, supported by overwhelmingly high routine clinical incident frequencies. Standard extraction protocols universally necessitate immediate postoperative site stabilization. Routine localized trauma consistently generates massive aggregate consumable demand. Curatick with Curatick Oral Wound Dressing directly addresses these daily requirements. Accessible protective barriers profoundly improve baseline patient recovery experiences.

Forward Science with PerioStm simplifies non-pharmacological mucosal irritation management. General dentistry practices constantly replenish these specific fundamental baseline supplies. Preventive interventions inherently rely upon reliable, accessible physical barrier systems. This immense continuous throughput intrinsically guarantees unparalleled commercial volume leadership.

Closure of grafted sites is set to be the fastest-growing segment, driven by surging advanced implantology procedural adoption rates. Sophisticated bone augmentation techniques strictly mandate absolute flap tension reduction. Clinicians constantly seek specialized matrices to prevent debilitating premature suture failures. Geistlich Pharma with Geistlich Select REGENFAST significantly enhances specific vertical tissue stability. These robust biological interfaces tangibly optimize complex reconstructive integration phases.

Nobel Biocare Services with Creos Xenoprotect ensures profound guided bone regeneration. Such critical performance alignments aggressively accelerate niche-targeted product penetration. Aesthetic clinical demands increasingly dictate flawless soft tissue contouring architectures. Consequently, these intricate restorations persistently command premium biological material integration.

Regional Insights

North America Oral Wound Dressing Market Trends

North America is likely to remain the leading regional market, accounting for approximately 42% share in 2026, supported by deeply entrenched advanced healthcare infrastructure networks. Extensive dental insurance penetration reliably sustains high elective procedural volumes. Regional practitioners consistently pioneer novel, complex tissue regeneration surgical methodologies. Premium biological matrices command overwhelming preference across these affluent demographics. Stringent regulatory oversight continuously guarantees exceptionally high biological material quality. Consequently, immense aggregate purchasing power firmly stabilizes robust regional leadership.

The U.S. continues to anchor regional momentum through sustained advanced biological research funding. Domestic therapeutic enterprises aggressively develop sophisticated proprietary tissue engineering platforms. Integra LifeSciences with HeliTape benefits directly from localized, streamlined distribution networks. Favorable federal reimbursement pathways significantly encourage complex reconstructive surgical frequency. Zimmer Biomet, with Zimmer CollaPlug, extensively permeates these vast domestic institutional supply chains. This continuous institutional investment powerfully insulates prevailing domestic commercial trajectories.

Europe Oral Wound Dressing Market Trends

Europe remains on track to remain a mature and structurally stable regional market, approximating a significant overall share, with demand primarily anchored in mandatory rigorous compliance upgrades. Universal healthcare models fundamentally ensure a steady baseline routine consumable procurement. Aging regional populations consistently require extensive restorative maxillofacial surgical interventions. Providers heavily prioritize clinically validated materials demonstrating exceptional long-term efficacy. Strict centralized safety directives inherently slow radical experimental technology adoption. This balanced operational ecosystem reliably generates predictable, steady commercial revenues.

Germany is projected to maintain absolute central dominance, utilizing superior localized precision manufacturing infrastructure. Domestic engineering standards mandate unparalleled excellence across all medical device production. Geistlich Pharma with Geistlich Select REGENFAST heavily penetrates these specialized high-tier dental networks. Robust national insurance frameworks adequately support expensive advanced biomaterial utilization. Baxter with PerClot aligns with these through hemostatic precision. Expansion sustains amid procedure standardization.

Asia Pacific Oral Wound Dressing Market Trends

Asia Pacific continues to register the fastest growth trajectory, as unprecedented private healthcare infrastructure buildouts fiercely accelerate broader specialized market expansion. Explosive middle-class demographic expansions dramatically elevate baseline aesthetic dental expectations. Emerging metropolitan centers aggressively construct highly modernized decentralized outpatient facilities. These structural developments organically create massive, completely untapped commercial populations. Cost-effective regenerative solutions inherently capture massive initial regional market penetration. Accordingly, escalating disposable incomes reliably fuel continuous aggressive category acceleration.

India leads regional acceleration through government-backed dental expansions under health schemes. Investments target ambulatory ORC adoption for grafts. ConvaTec with AQUACEL leverages affordability strategies. Procurement intensifies with rising implant demand. China is poised to command extreme localized expansion, given massive targeted strategic technological investments. Governmental health initiatives purposefully subsidize the construction of immense modern therapeutic facilities.

Curatick with Curatick Oral Wound Dressing directly captures these explosive localized volume requirements. Domestic practitioners rapidly integrate sophisticated Western surgical methodologies into routine practice. Forward Science with PerioStm successfully targets these rapidly modernizing professional clinical networks. This synchronized national modernization consistently ensures phenomenal exponential volume trajectories.

Competitive Landscape

The global oral wound dressing market remains fragmented, with numerous providers competing across material tiers rather than consolidated dominance. This structure arises from specialized niches in content types such as collagen and ORC, allowing mid-sized players to capture clinic segments through targeted innovations. Leading corporations inherently dictate prevailing surgical standards utilizing profound clinical evidence. These dominant entities successfully leverage vast integrated global distribution infrastructures. Geistlich Pharma with Geistlich Mucograft establishes definitive premium regenerative tissue benchmarks. Institutions implicitly trust organizations demonstrating decades of pristine safety records. Zimmer Biomet with Zimmer CollaPlug dominates routine foundational hemostatic supply networks. Integra LifeSciences with HeliTape anchors essential centralized hospital procurement contracts

Elite manufacturers purposefully concentrate immense resources on bioactive formulation enhancements. Forward Science with PerioStm exemplifies this distinct lateral technological innovation strategy. Conversely, value-tier participants exclusively target massive price-sensitive emerging geographical territories. Curatick with Curatick Oral Wound Dressing executes highly effective, accessible volume penetration. Strategic acquisitions increasingly consolidate disparate specialized product lines under singular umbrellas. Multinational conglomerates aggressively absorb nimble, innovative startups, acquiring novel intellectual property. This continuous consolidation structurally elevates baseline competitive intensity across every segment.

Key Industry Developments:

- In January 2026, SCTIMST unveiled and licensed CholeDerm, an acellular dermal dressing derived from animal gall bladders, to Alicorn Medical. This commercialization of bio-derived materials highlights the market's increasing move toward regenerative therapies and eco-friendly, animal-sourced wound healing matrices.

- In November 2025, Mölnlycke established its first manufacturing site in Changshu, China, spanning 10,000 m². This move aims to localize production in the high-growth Asia Pacific region, enhancing supply chain resilience and proximity to the world's largest diabetic patient populations.

Companies Covered in Oral Wound Dressing Market

- Geistlich Pharma

- Zimmer Biomet

- Integra LifeSciences

- Johnson & Johnson

- 3M Company

- Medtronic

- Baxter

- Smith & Nephew

- ConvaTec

- Coloplast

- Molnlycke

- Nobel Biocare Services

- Collagen Matrix, Inc.

- Axio Biosolutions

- Forward Science

- Novabone

Frequently Asked Questions

The global oral wound dressing market size is expected to reach US$1.3 billion in 2026. The market is projected to expand significantly, reaching US$2.4 billion by 2033. This substantial trajectory represents a robust overall commercial expansion period.

The primary market driver remains the consistent acceleration of global advanced dental implant procedures. These complex surgeries unconditionally require superior biological healing substrates, preventing critical postoperative complications.

The oral wound dressing market is anticipated to experience a strong 9.1% CAGR throughout the forecast period. Such acceleration powerfully highlights intensifying global reliance upon sophisticated regenerative medical technologies.

North America confidently leads the global landscape, anticipating approximately 42% total market share in 2026. This dominant regional positioning intrinsically stems from deeply entrenched sophisticated healthcare funding mechanisms.

Leading industry participants include prominent multinational entities such as Geistlich Pharma, Zimmer Biomet, and Integra LifeSciences. These established corporations decisively govern global technological standards through continuous, relentless scientific formulation innovations. Emerging localized manufacturers also critically supply specialized synthetic products addressing specific regional economic constraints.