- Medical Devices

- U.S. Intraoral Scanners Market

U.S. Intraoral Scanners Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

U.S. Intraoral Scanners Market by Type (Wired, Wireless), Modality (Standalone, Portable), Application (Orthodontics, Prosthodontics, Implantology, Periodontics, Others), End User (Dental Clinics, Hospitals, Research Institutes, Others), Analysis from 2025 to 2032

U.S. Intraoral Scanners Market Share and Trends Analysis

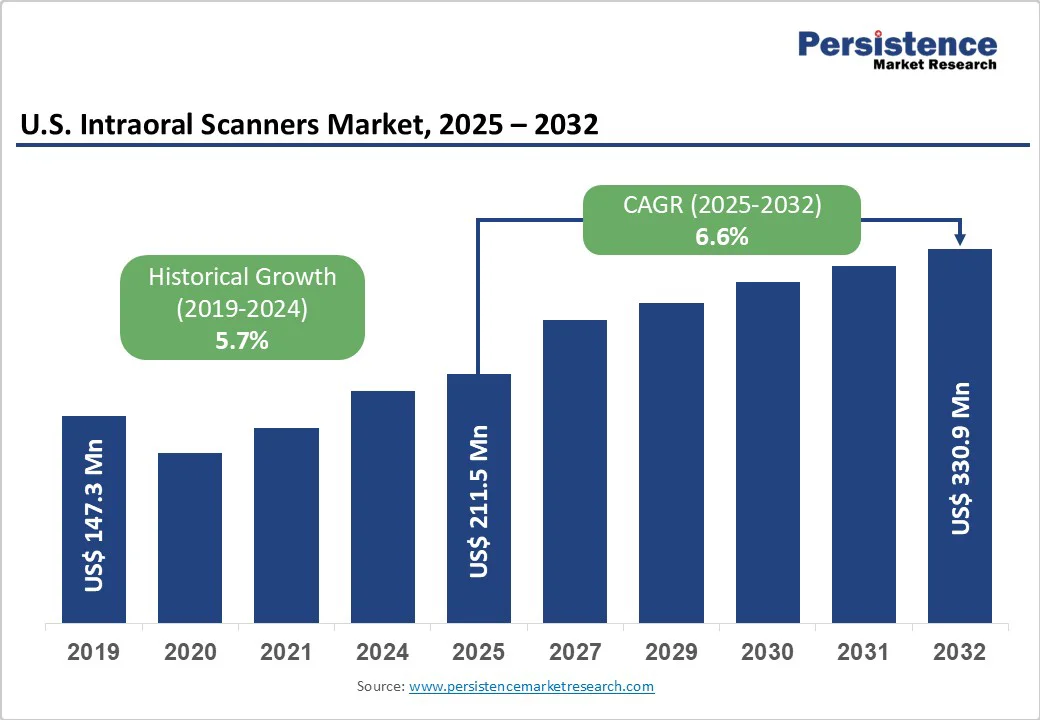

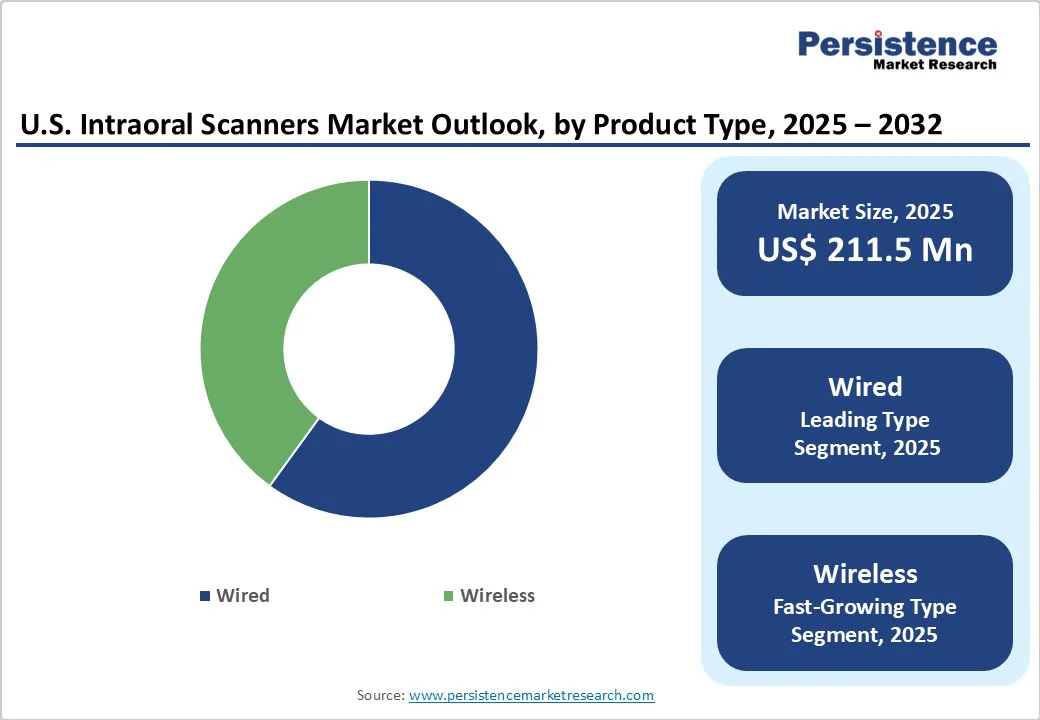

The U.S. intraoral scanners market size is expected to be valued at US$211.5 million in 2025 and is projected to reach US$330.9 million by 2032, growing at a CAGR of 6.6% during the forecast period from 2025 to 2032. The U.S. intraoral scanner industry is driven by the rising adoption of digital dentistry, demand for clear aligners, and the need for accurate and efficient impressions.

Growing dental disorders, a large orthodontist presence, and patient comfort preferences all contribute to increased uptake. Trends include wireless and AI-enabled scanners, CAD/CAM workflows, cloud-based integration, and training programs enhancing accessibility across clinics, hospitals, and institutes.

Key Industry Highlights:

- Fastest-Growing Type: Wireless and AI-enabled intraoral scanners are expanding rapidly due to enhanced imaging accuracy, faster workflow, and growing adoption in orthodontics, prosthodontics, and implantology.

- Application Leader: Orthodontics accounts for about 36.5% of the U.S. intraoral scanners market in 2025, driven by the growing demand for clear aligners, precise digital impressions, and efficient treatment planning. High adoption is supported by AI-assisted scanning, real-time monitoring, and seamless integration with CAD/CAM workflows, which improve patient comfort, reduce chair time, and enhance overall treatment accuracy.

- Dominant End-user: Dental clinics account for approximately 60.3% of the market in 2025, fueled by high patient volume, demand for digital impressions, and integration with lab and chairside systems.

- Emerging Opportunity: Portable hand-held scanners, cloud-based integration, and AI-assisted diagnostic features are gaining attention, driven by workflow efficiency, patient comfort, remote collaboration, and improved treatment planning.

| U.S. Intraoral Scanners Market Attribute | Key Insights |

|---|---|

| U.S. Intraoral Scanners Market Size (2025E) | US$211.5 Mn |

| Market Value Forecast (2032F) | US$330.9 Mn |

| Projected Growth (CAGR 2025 to 2032) | 6.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.7% |

Market Dynamics

Driver - Artificial Intelligence and Machine Learning Technology Integration Surges in the Market

The integration of artificial intelligence and machine learning in dental imaging and intraoral scanning is accelerating in the U.S., driven by FDA clearances and academic validations. As of August 2024, the FDA has authorized 950 AI/ML-enabled medical devices, up from just six in 2015, a significant increase reflecting both regulatory and technological readiness.

In dentistry specifically, products like Denti.AI Detect, cleared in October 2023, demonstrated a 26% increase in treatment-opportunity detection by aiding dentists in identifying caries, periapical lesions, and bone loss from intraoral X-rays.

Experimental studies of intraoral scanners also show improved precision and reduced errors when AI fills mesh defects in full-arch scans. This convergence of regulatory approvals, clinical evidence, and device innovation underscores AI’s role as a key driver of the U.S. intraoral scanning market.

Restraints - Data Privacy Concerns and Regulatory Hurdles

Data privacy concerns and regulatory hurdles present significant restraints in the U.S. intraoral scanners market. The integration of digital imaging technologies requires strict adherence to the Health Insurance Portability and Accountability Act (HIPAA), which mandates the secure handling of patient data. Inadequate compliance with these standards can result in legal repercussions and a loss of patient trust.

The Food and Drug Administration (FDA) regulates dental devices under 21 CFR Part 872, ensuring that products meet safety and efficacy standards. Devices must undergo rigorous testing and validation processes, which can delay time-to-market and increase development costs. For instance, the TRIOS 5 intraoral scanner underwent FDA 510(k) clearance, demonstrating the extensive regulatory requirements.

Moreover, the evolving nature of digital dentistry and AI integration introduces challenges in standardization and clinician training. A 2025 study highlighted concerns over algorithmic bias and the need for standardized protocols in AI applications within dentistry.

These factors collectively contribute to a complex regulatory landscape, which may hinder the widespread adoption and integration of intraoral scanners in dental practices.

Opportunity - Patient-centric Features and Applications Development

The development of patient-centric features and applications represents a significant opportunity in the U.S. intraoral scanner market, enhancing user experience and accelerating adoption in dental practices. Patient-friendly features, such as real-time imaging, guided scanning, and AI-based feedback, simplify the scanning process, making it more comfortable and engaging for patients.

These advancements not only improve patient satisfaction but also empower dentists with enhanced diagnostic accuracy, resulting in personalized and efficient treatment planning. Additionally, applications that support remote monitoring and virtual consultations expand access to care and strengthen patient-practitioner communication.

As patient demand grows for accessible, less invasive treatments, the adoption of intraoral scanners with these patient-centered functionalities offers a competitive advantage, driving growth in the U.S. market.

Category-wise Analysis

By Type, Wired dominates the Intraoral Scanners Market

Wired led the market with 68.7% share in 2025, due to their reliability, consistent power supply, and established integration into existing dental workflows. These devices are often preferred in clinical settings where uninterrupted performance and data security are paramount.

For instance, the iTero Element series, a widely used wired scanner, is recognized for its speed and accuracy in capturing detailed digital impressions. Additionally, wired systems are less susceptible to connectivity issues, ensuring stable data transmission during procedures.

While wireless models offer enhanced mobility, their adoption is limited by concerns over battery life, potential interference, and the need for robust wireless infrastructure. Therefore, the reliability and performance of wired intraoral scanners make them a preferred choice in many U.S. dental practices.

By Application, Orthodontics are Gaining Traction due to Portability, Reliability, Quick Deployment, and Independent Power Supply

Orthodontics leads the U.S. market due to the growing demand for precise, efficient, and patient-friendly digital impressions used in treatments like clear aligners and braces. Approximately 5% of U.S. dentists are orthodontists, representing over 200,000 practitioners nationwide.

FDA-cleared devices, such as the iTero Element 5D, enable accurate digital impressions, real-time monitoring, and seamless integration with CAD/CAM workflows. These technologies reduce chair time, improve patient comfort, and enhance treatment outcomes, which drives adoption.

Combined with the increasing popularity of clear aligner therapy and growing dental awareness, orthodontics remains the leading application segment for intraoral scanners in the U.S., accounting for the largest share of usage in both clinics and specialty practices.

Competitive Landscape

The U.S. intraoral scanners market is highly competitive, led by players such as Align Technology, Dentsply Sirona, Carestream Dental, Envista Holdings, and IOS Technologies. These companies focus on scanner accuracy, high-speed image capture, wireless or cart-based designs, and seamless integration with CAD/CAM and dental lab workflows.

Emerging players emphasize affordability, portable hand-held solutions, AI-enabled lesion detection, and user-friendly interfaces to cater to dental clinics, hospitals, and academic institutes, targeting both general practitioners and specialists in orthodontics, prosthodontics, and implantology.

Key Industry Developments:

- In March 2025, Carestream Dental unveiled the next-generation CS 8200 3D Advance Edition, featuring enhanced imaging capabilities, improved 3D diagnostics, and streamlined workflows. The upgraded system aimed to provide dental professionals with higher precision, faster scanning, and better integration with digital treatment planning tools, supporting efficient and accurate patient care.

- In September 2024, Dentsply Sirona introduced Primescan® 2 powered by DS Core, marking the launch of the first cloud-native intraoral scanning solution. The device enabled seamless cloud integration, improved data management, and enhanced workflow efficiency for dental practices, supporting advanced digital impressions and CAD/CAM applications.

- In September 2024, Dentsply Sirona launched Primescan 2, the first-ever cloud-based intraoral scanner. The device enabled dental practices to capture precise digital impressions while securely storing and managing data in the cloud, thereby enhancing workflow efficiency and facilitating seamless integration with CAD/CAM systems for improved treatment planning and patient care.

Companies Covered in U.S. Intraoral Scanners Market

- Dentsply Sirona

- Align Technology

- Carestream Dental

- Medit Corp.

- Envista Holdings Corporation

- IOS Technologies, Inc.

- Acteon Group Ltd.

- 3Shape

- DEXIS

- Planmeca USA

- Cad-Ray

- Renew Digital

- Benco Dental

- Brontes Technologies

- Others

Frequently Asked Questions

The U.S. intraoral scanners Market is projected to be valued at US$ 211.5 Mn in 2025.

Rising digital dentistry adoption, clear aligner demand, need for accurate impressions, patient comfort, AI integration, and efficient CAD/CAM workflows drive growth.

The U.S. market is poised to witness a CAGR of 6.6% between 2025 and 2032.

AI-enabled scanners, wireless portability, cloud integration, CAD/CAM workflows, orthodontics growth, expanding dental clinics, and rising cosmetic dentistry adoption present key opportunities.

Major players in the U.S. are Dentsply Sirona, Align Technology, Carestream Dental, Medit Corp., Envista Holdings Corporation, IOS Technologies, Inc., and Others.