- Testing, Inspection, & Certification

- Global Monolithic Microwave Integrated Circuits Market

Global Monolithic Microwave Integrated Circuits Market Size, Share, and Growth Forecast 2026 – 2033

Monolithic Microwave Integrated Circuits Market by Component (Power Amplifiers, Power Amplifiers, Attenuators, Switches, Phase Shifters, Mixers, and Others), Material Type (Gallium Arsenide, Gallium Arsenide, Gallium Arsenide, and Others), Technology (Gallium Arsenide, Gallium Arsenide, pHEMT, E-pHEMT, mHEMT, mHEMT, and MOS), and Regional Analysis

Monolithic Microwave Integrated Circuits Market Size and Share Analysis

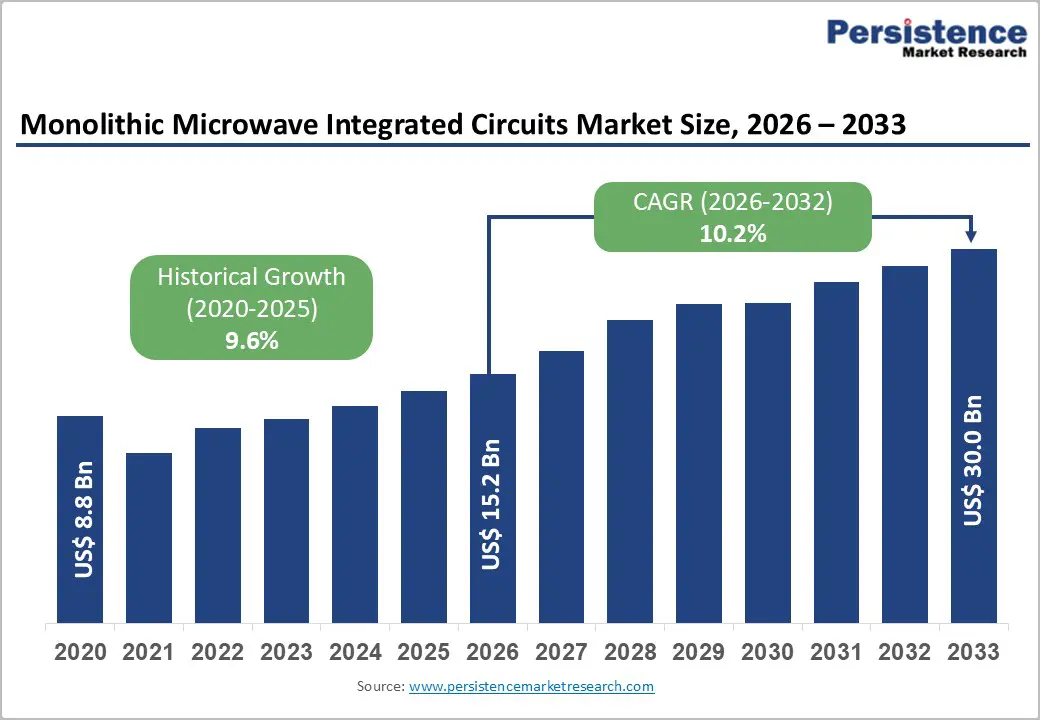

The global Monolithic Microwave Integrated Circuits Market size was valued at US$ 15.2 Bn in 2026 and is projected to reach US$ 30.0 Bn by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

Market expansion is driven by explosive 5G and 6G network rollout requiring advanced RF front-end modules, power amplifiers, and beamforming solutions at millimeter-wave frequencies establishing critical infrastructure modernization catalyst. Accelerating satellite communications expansion including mega-LEO constellation deployment, high-throughput satellite integration, and Ka-band applications (26.5-40 GHz frequency range) demanding specialized MMIC components creates unprecedented growth opportunity for power amplifier and low-noise amplifier manufacturers.

Key Market Highlights

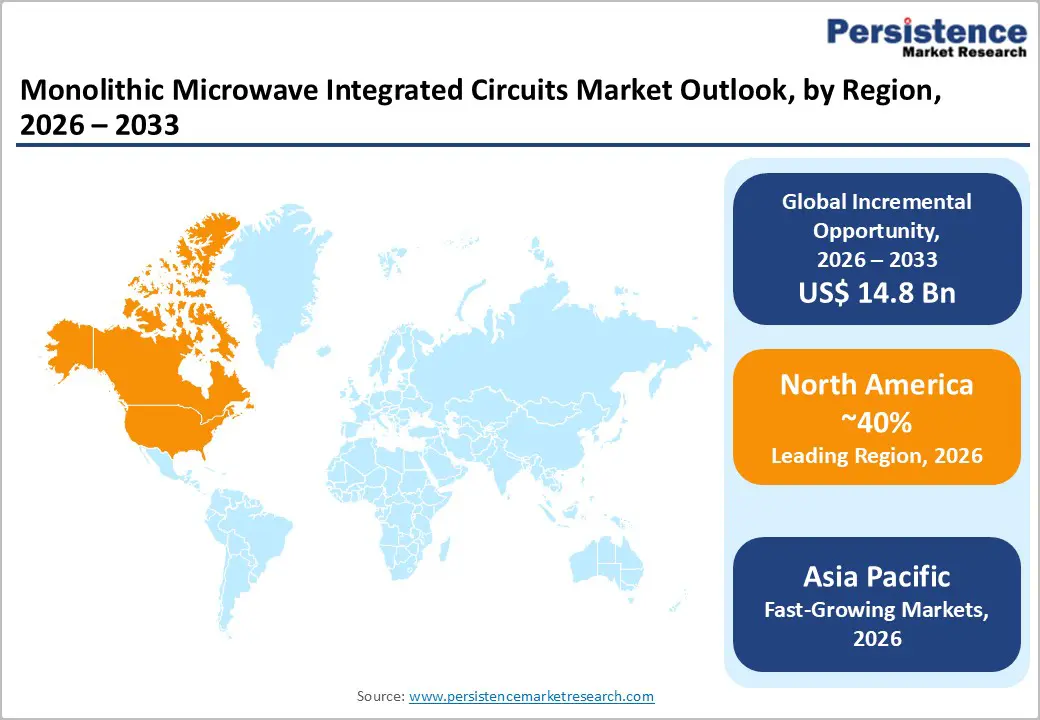

- Leading Region: North America maintains market leadership anchored by United States RF semiconductor design ecosystem dominance, military and aerospace application focus, government space program funding, and major MMIC supplier headquarters including Qorvo, MACOM, Analog Devices, Infineon, and Skyworks.

- Fastest Growing Region: Asia-Pacific commands fastest expansion driven by China manufacturing dominance with 60% global capacity, India's space program MMIC development, rapid urbanization requiring massive telecommunications infrastructure, and government digital transformation initiatives across emerging economies.

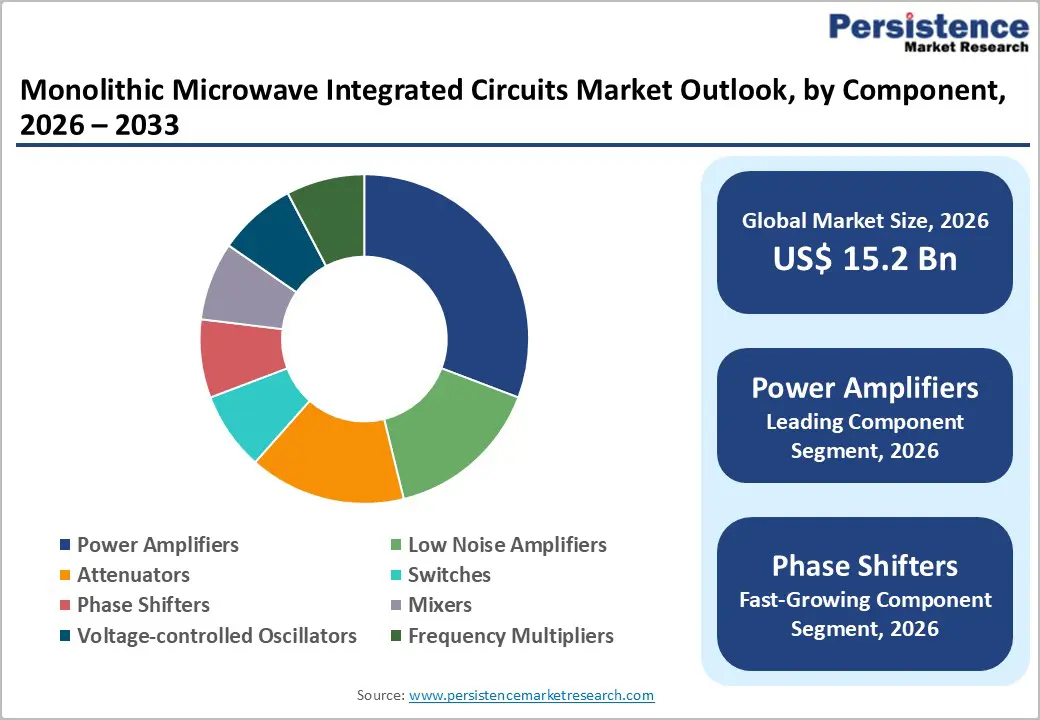

- Dominant Component: Power amplifiers command market dominance with 45% share, driven by fundamental RF system architecture requirement, 77 GHz automotive radar application volume ramp, Ka-band satellite communications specialization, and defense/aerospace premium application positioning.

- Fastest Growing Material Type: Gallium Nitride (GaN) HEMT technology experiencing fastest growth momentum at 15% annual rates, propelled by superior performance characteristics including 3.3 MV/cm breakdown field, >900 cm²/Vs mobility, GaN-on-Si cost reduction pathway, automotive radar deployment acceleration, and 2025 production volume targets.

- Key Market Opportunity: Satellite communications mega-LEO constellation expansion and 5G/6G convergence infrastructure requiring specialized MMIC components for power amplifiers, beamforming systems, and receiver architectures, creating multi-billion-unit addressable market opportunity for regional manufacturers and fabless design companies.

| Key Insights | Details |

|---|---|

| Global Monolithic Microwave Integrated Circuits Market Size (2026E) | US$ 15.2 Bn |

| Market Value Forecast (2033F) | US$ 30.0 Bn |

| Projected Growth CAGR(2026-2033) | 10.2% |

| Historical Market Growth (2020-2025) | 9.6% |

Market Dynamics

Market Growth Drivers

5G and 6G Network Expansion Driving RF Front-End Module and Millimeter-Wave Component Demand

Unprecedented 5G network rollout expansion and emerging 6G development programs creating critical demand for advanced MMIC components particularly RF power amplifiers, low-noise amplifiers, and phase shifters operating at millimeter-wave frequencies. 5G frequency band standards including N257 (26.5-29.5 GHz) and N258 (24.25-27.5 GHz) requiring specialized MMIC LNA designs with measured linear gain 18.2-20.3 dB and noise figure 2.5-3.1 dB establishing rigorous performance specifications driving innovation and manufacturing investment. 6G development programs emphasizing AI-driven resource optimization, spectrum sharing, and mobility support up to 1000 km/h create next-generation MMIC requirements for enhanced processing speed, integration density, and thermal performance.

Phased array beamforming systems adoption requiring precise phase control and RF signal routing drive specialized MMIC switch, mixer, and phase shifter component demand. Rollout of advanced cellular infrastructure particularly in Asia-Pacific region with China and India leading telecommunication investment, establishing sustained demand growth supporting market expansion momentum through forecast period.

Satellite Communications Mega-Constellation Expansion and Inter-Satellite Link Integration

Explosive satellite communications market expansion driven by mega-LEO constellation deployment with reduced per-unit costs through mass production creates exceptional MMIC market opportunity particularly for power amplifiers operating at Ka-band frequencies (26.5-40 GHz) enabling satellite data transmission. LEO mega-constellations providing global broadband coverage, IoT connectivity, and low-latency communications requiring high-throughput satellite (HTS) MMIC integration including beamforming, RF power amplification, and receiver components. Inter-satellite link (ISL) advancement particularly optical ISL technology requiring supporting RF components for seamless terrestrial-satellite network integration drives specialized MMIC development.

Government and private sector investment in space programs including India's DRDO MMIC satellite radar imaging deployment (2022) and China's IC manufacturing expansion establish regional manufacturing capacity acceleration. Ka-band application expansion beyond traditional telecom into emerging 5G/6G convergence infrastructure establishing new application categories, sustaining market growth momentum through forecast period.

Market Restraints

Complex Material Supply Chain and Export Control Vulnerabilities

Critical raw material constraints particularly indium and phosphorus availability subject to China's expanded export controls on indium-bearing compounds implemented in 2024 creates supply uncertainty and cost volatility affecting InP-based MMIC production. Indium Phosphide wafer market dependency on limited suppliers and geographic concentration combined with mechanical fragility constraining wafer size scaling beyond 6 inches limits manufacturing throughput and cost optimization. Western wafer maker qualification of alternative gallium and phosphorus suppliers extending procurement lead times and increasing operational complexity for MMIC manufacturers.

High-Temperature Management and Thermal Performance Limitations

Power density demands in modern MMIC designs requiring thermal conductivity optimization particularly in GaN-on-Si platforms create engineering complexity managing substrate parasitic conduction and RF losses. Thermal dissipation challenges in high-power amplitude applications limiting sustained operation without performance degradation particularly in satellite and defense applications requiring reliability. Trade-off between performance optimization and manufacturability constraining design flexibility and cost reduction opportunities.

Market Opportunities

Gallium Nitride (GaN) Technology Adoption and GaN-on-Silicon Cost Reduction Acceleration

GaN HEMT technology maturation with demonstrated performance superiority including 3.3 MV/cm breakdown field, >900 cm²/Vs electron mobility, and 10 A current handling capacity establishing next-generation power amplifier and receiver architecture foundation. Migration to 200 nm silicon platform utilizing CMOS-compatible fabrication tools reducing manufacturing costs significantly while enabling integrated circuit technology leverage supporting cost-competitive GaN-on-Si MMIC production.

Infineon partnership delivering 77 GHz GaN power amplifiers for automotive radar with full production target by 2025 establishing volume manufacturing milestone validating commercial viability. GaN-CMOS integration enabling E-mode/D-mode CMOS-like circuit technology with negligible static power consumption creating premium efficiency positioning for defense and satellite applications. Automotive radar sensor expansion beyond traditional OEM adoption into aftermarket and advanced driver-assistance system (ADAS) integration creating volume growth opportunity, establishing sustained demand expansion through forecast period.

Emerging Applications in Advanced Sensing, AI-Driven Optimization, and Future Network Integration

Millimeter-wave sensing applications including simultaneous communication and sensing (JCAS) emerging as critical 6G technology requiring integrated MMIC transceiver capability. Phased array radar evolution toward electronically steerable architectures for automotive, aerospace, and defense applications demanding higher integration density and beam-steering precision from MMIC component suppliers. AI and machine learning integration enabling intelligent RF front-end design and adaptive power management creating differentiation opportunity for technologically advanced MMIC manufacturers.

Internet of Things (IoT) expansion requiring low-power RF receiver and transceiver MMIC solutions. Space economy acceleration with emerging commercial space stations, in-orbit manufacturing, and satellite servicing creating new MMIC application categories, establishing next-generation market expansion opportunity through forecast period.

Category-wise Insights

Component Analysis

Power amplifiers command dominant market position with estimated 45% share driven by fundamental RF system architecture requirement for signal transmission across all wireless standards. Automotive radar application dominance with 77 GHz power amplifier specifications driving 2025 production volume ramp (Infineon partnership) establishes high-volume segment growth. Ka-band satellite communication power amplifiers including Qorvo's QPA1724 demonstrating twice competitor power output at 17.3-21.2 GHz frequency range establish premium segment commanding higher pricing. 5G and 6G infrastructure buildout requiring distributed power amplifier deployment across base station phased arrays and RF front-end modules create multi-billion-unit addressable opportunity.

Defense and aerospace power amplifier specialization with military-grade reliability requirements and classified applications command premium pricing supporting highest-margin segment. Efficiency optimization emphasis particularly Doherty and outphasing power amplifier architectures enabling improved linearity and bandwidth sustain competitive differentiation, maintaining power amplifier market leadership throughout forecast period.

Material Type Analysis

Gallium Arsenide materials command estimated 45-50% market share reflecting most mature and extensively established compound semiconductor technology with 5-6 times silicon electron mobility enabling high-frequency operation. Proven manufacturing infrastructure across six-inch wafer processing at established suppliers including Qorvo, Skyworks, MACOM, and international foundries establish cost-competitive production capability. Bandgap characteristics (1.43 eV vs silicon 1.1 eV) with direct bandgap property enabling superior noise performance for low-noise amplifier applications justifying continued dominance particularly in receiving system architecture.

Satellite data transmission, mobile communications, and GPS navigation representing legacy high-volume applications with established manufacturing ecosystem supporting cost optimization and yield improvement. GaAs HEMT and pHEMT technology maturity with decades of device characterization and design methodology optimization enable rapid prototyping and reduced time-to-market for new applications, sustaining market leadership position through forecast period.

Technology Analysis

HEMT (High Electron Mobility Transistor) technology variants command estimated 55-65% market share driven by superior frequency response, high-power handling, and low-noise characteristics compared to traditional MESFET technology. pHEMT (Pseudomorphic HEMT) maturity with strained-layer technology optimization enabling enhanced electron mobility and transconductance establish standard-baseline performance. E-pHEMT (Enhancement-mode pHEMT) adoption accelerating integration density and circuit function consolidation by eliminating separate depletion-mode bias networks.

GaN HEMT rapid growth representing emerging technology adoption with performance advantages including high breakdown voltage tolerance, superior thermal conductivity, and integrated circuit capability establishing fastest-growing segment with 15% annual growth rates. mHEMT (Metamorphic HEMT) specialization for dual-band and wideband applications enabling broader frequency coverage from single MMIC design. HBT (Heterojunction Bipolar Transistor) technology maintaining specialized application niche for power amplifier applications requiring exceptional linearity, establishing market segmentation with technology-specific positioning through forecast period.

Regional Insights

North America Monolithic Microwave Integrated Circuits Trends

North America maintains technology leadership position anchored by United States RF semiconductor design and manufacturing ecosystem dominance. Major MMIC suppliers including Qorvo, MACOM, Analog Devices, Infineon, and Skyworks maintaining headquarters and primary R&D centers in North America establish innovation capacity leadership supporting next-generation technology development.

Rising defense expenditure and government space program expansion including mega-LEO constellation policy support drive substantial MMIC investment particularly for classified military applications. Automotive radar adoption leadership particularly in advanced driver-assistance system (ADAS) and autonomous vehicle development supporting high-volume consumer electronics MMIC demand.

Europe Monolithic Microwave Integrated Circuits Trends

Europe maintains advanced manufacturing ecosystem with Germany commanding industrial electronics specialization and United Kingdom maintaining design capability strength. Established MMIC suppliers including OMMIC and United Monolithic Semiconductors providing European-based manufacturing capacity supporting regulatory compliance and supply chain resilience.

European 5G and 6G initiative leadership driving telecommunications infrastructure modernization supporting sustained MMIC demand growth. Regulatory harmonization initiatives promoting consistent performance standards across EU member states reducing fragmentation and simplifying commercialization of cross-border MMIC solutions.

Asia Pacific Monolithic Microwave Integrated Circuits Trends

Asia-Pacific commands fastest regional growth at 15% CAGR driven by China establishing global manufacturing dominance with over 60% of large manufacturers integrating advanced analytics solutions for supply chain optimization. China's strategic MMIC manufacturing investment including WIN Semiconductors and emerging domestic manufacturers establishing cost-competitive production capacity supporting regional market expansion.

India's DRDO MMIC satellite radar imaging deployment (2022) establishing indigenous capability development supporting space program independence. Rapid urbanization and massive population demographics driving massive cellular infrastructure expansion requiring sustained MMIC component supply for 5G/6G rollout. Government digital transformation initiatives and private sector investment in telecommunications infrastructure modernization establishing multi-year demand growth trajectory, ensuring sustained Asia-Pacific market leadership through forecast period.

Competitive Landscape for the Mo nolithic Microwave Integrated Circuits Market

The Monolithic Microwave Integrated Circuits market exhibits moderate consolidation dominated by tier-one global technology companies including IBM, Google, Oracle, and Salesforce commanding substantial enterprise market share through comprehensive platform portfolios, established customer relationships, and enterprise support capabilities. Specialized analytics platforms including Mixpanel, Amplitude, Heap, and Fullstory establishing competitive positions through superior user experience, ease-of-setup, and domain specialization particularly in e-commerce and SaaS segments.

Vertical-specific Component providers capturing niche market segments with deep Technology expertise serving healthcare, BFSI, and retail verticals with compliance-first, Technology-tailored platforms. R&D-driven competition emphasizing AI/ML integration, real-time capabilities, and mobile-first architectures creating continuous innovation cycle supporting sustained market dynamism.

Key Market Developments

- In November 2024, MACOM acquired ENGIN-IC, a fabless semiconductor company specializing in advanced Gallium Nitride MMICs, strengthening GaN MMIC design capabilities and enabling accelerated market share gain in emerging GaN technology segment particularly for next-generation power amplifier and receiver applications.

- In June 2024, Qorvo introduced three new RF MCMs specifically designed for advanced radar systems, leveraging proprietary packaging and process technology to deliver compact size, superior performance, lower noise, and reduced power consumption optimized for modern phased array and multifunction radar systems.

Companies Covered in Global Monolithic Microwave Integrated Circuits Market

- Analog Devices

- Infineon Technologies

- NXP Semiconductor

- Qorvo

- MACOM

- Skyworks Solutions

- Mini-Circuits

- Broadcom

- Maxim Integrated

- OMMIC

- WIN Semiconductors

- Custom MMIC Design Services

- United Monolithic Semiconductors

- Microarray Technologies

- VectraWave

Frequently Asked Questions

The global Monolithic Microwave Integrated Circuits Market is projected to reach US$ 30.0 billion by 2033, expanding from US$ 15.2 billion in 2026 at a CAGR of 10.2%, driven by 5G/6G network expansion, satellite communications mega-constellation deployment, automotive radar proliferation, and Gallium Nitride technology cost reduction through GaN-on-Si platform migration.

Market demand growth is driven by multiple converging factors including 5G and 6G network rollout requiring advanced RF front-end modules, satellite mega-LEO constellation expansion with Ka-band communications, automotive sector vehicle electrification and autonomous vehicle development requiring 77 GHz radar systems, Gallium Nitride performance advantages with 3.3 MV/cm breakdown field and >900 cm²/Vs mobility, and cost reduction through GaN-on-Si technology platform migration supporting volume production.

Power amplifiers command market leadership with estimated 40-45% market share, driven by fundamental RF system transmission requirement, automotive radar 77 GHz adoption with 2025 production volume targets, Ka-band satellite communications specialization with twice-competitor power output capability, and defense/aerospace premium application positioning commanding highest pricing.

North America maintains market leadership anchored by United States RF semiconductor design ecosystem dominance, military and aerospace application focus with substantial defense expenditure, government space program funding, and major MMIC supplier headquarters including Qorvo, MACOM, Analog Devices, Infineon, and Skyworks concentrating technology development and manufacturing capacity.

Major market opportunities include satellite mega-LEO constellation expansion requiring specialized power amplifiers and beamforming systems creating multi-billion-unit addressable market; 5G/6G infrastructure buildout requiring distributed RF components; GaN-on-Si cost reduction enabling volume production; automotive radar sensor expansion beyond OEM adoption into aftermarket ADAS; AI-driven RF front-end optimization; and emerging millimeter-wave sensing applications for simultaneous communication and sensing (JCAS) supporting next-generation network integration.

Leading market players include Qorvo commanding market leadership through RF MCM radar solutions and Skyworks merger creating $22 billion entity; MACOM establishing GaN MMIC specialization through ENGIN-IC acquisition; Analog Devices maintaining comprehensive RF power semiconductor portfolio; Infineon leading automotive radar GaN PA development with 2025 production targets; and Skyworks Solutions achieving six-inch processing line capacity supporting volume production across consumer and enterprise electronics applications.