- Specialty & Fine Chemicals

- Metal Finishing Chemicals Market

Metal Finishing Chemicals Market Size, Share, and Growth Forecast 2025 - 2032

Metal Finishing Chemicals Market by Product Type (Plating Chemicals, Cleaning & Degreasing Chemicals, Conversion Coatings, Anodizing Chemicals, Polishing & Buffing Compounds, and Activation & Pretreatment Chemicals), Metal Type (Steel & Iron, Aluminum, Copper & Alloys, Zinc & Alloys, Magnesium, and Nickel & Precious Metals), Technology, Industry, and by Regional Analysis, 2025 - 2032

Metal Finishing Chemicals Market Size and Trend Analysis

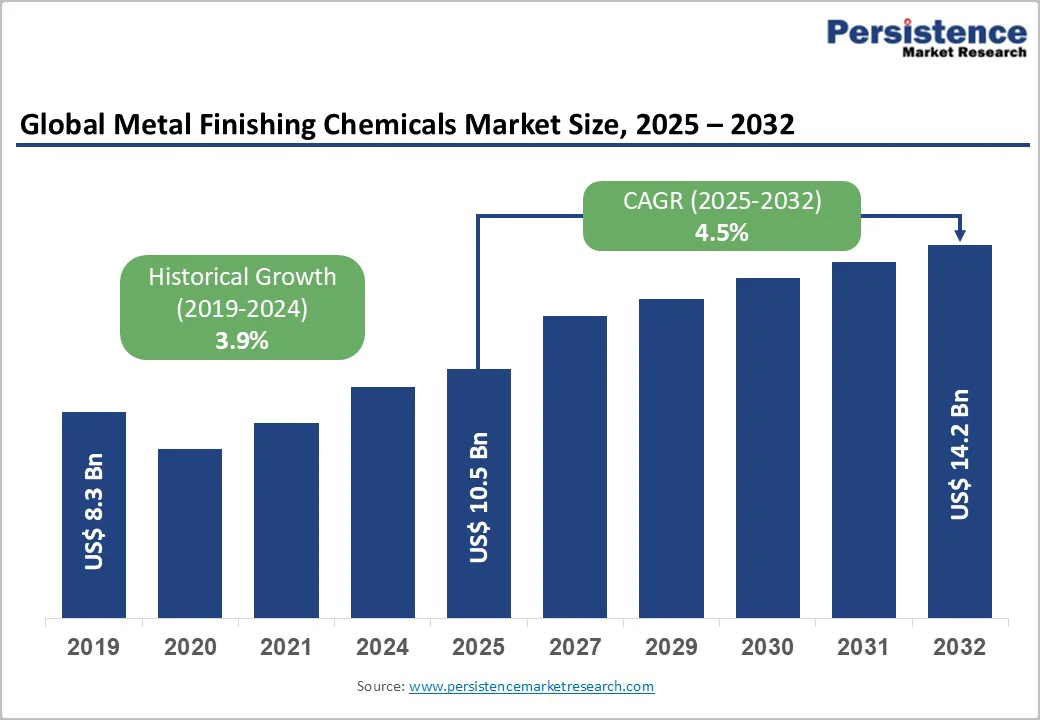

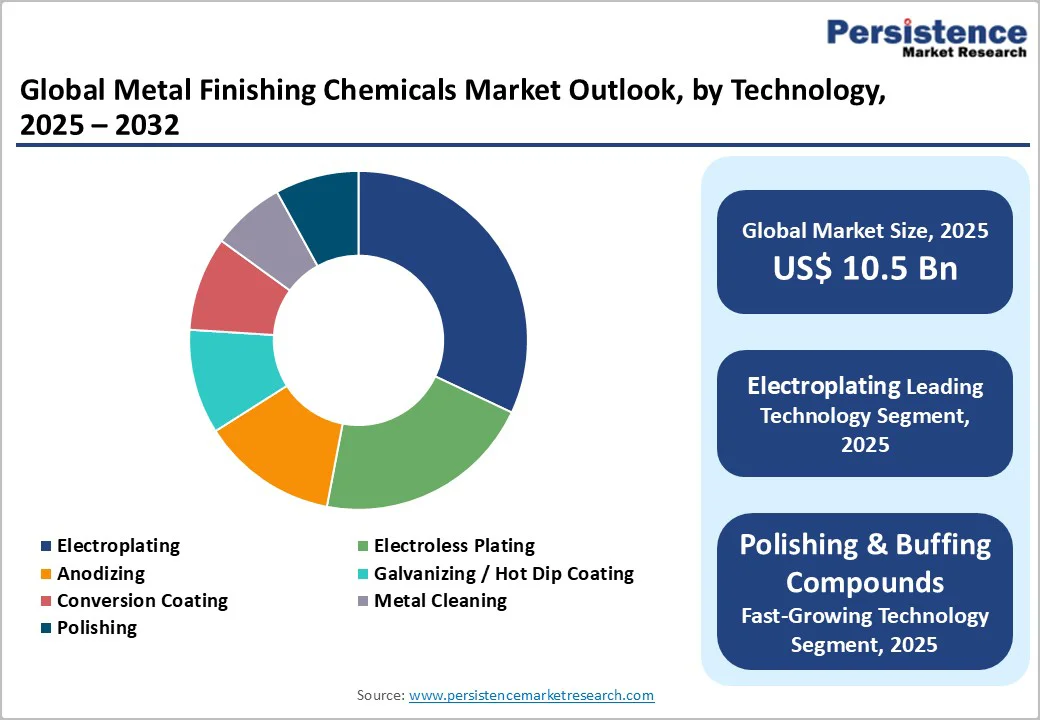

The global metal finishing chemicals market size is valued at US$ 10.5 billion in 2025 and is projected to reach US$ 14.3 billion, growing at a CAGR of 4.5% between 2025 and 2032.

The market expansion is primarily propelled by surging demand from the automotive and electronics sectors, where enhanced corrosion resistance and aesthetic finishes are essential for component longevity.

Key Market Highlights

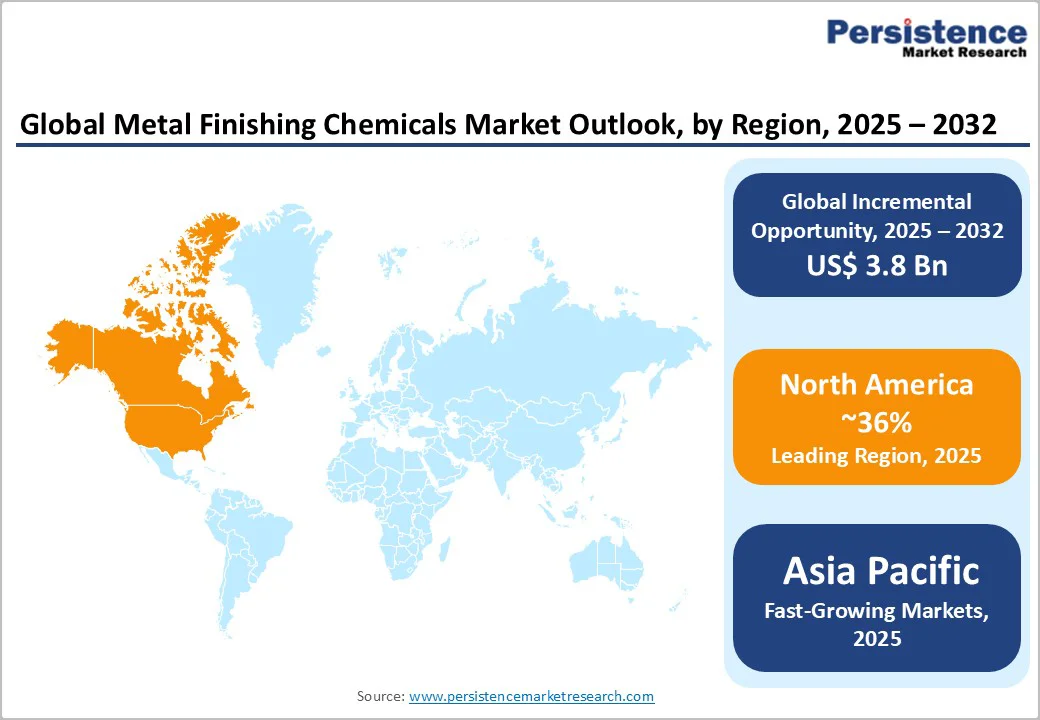

- Leading Region: North America leads the metal finishing chemicals market with siring share of 36%, due to advanced automotive and aerospace sectors, supported by stringent EPA regulations ensuring high-quality, compliant finishes.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing region with a significant CAGR of 5.7%, driven by China's manufacturing boom and India's infrastructure push, projecting robust demand for plating solutions.

- Leading segment: Electroplating dominates technology segments with 32% share, offering precise corrosion protection vital for electronics and automotive durability worldwide.

- Fastest-Growing Segment: Cleaning chemicals represent the fastest-growing product segment with significant CAGR of 5.3%, fueled by eco-regulations and electronics expansion requiring contaminant-free surfaces.

- Key Opportunity: Sustainable bio-based formulations offer key opportunities, aligning with global green policies to capture demand in aerospace and renewables for low-toxicity coatings.

| Key Insights | Details |

|---|---|

| Metal Finishing Chemicals Market Size (2025E) | US$ 10.5 Bn |

| Market Value Forecast (2032F) | US$ 14.3 Bn |

| Projected Growth CAGR (2025 - 2032) | 4.5% |

| Historical Market Growth (2019 - 2024) | 3.9% |

Market Dynamics

Drivers - Growing Vehicle Production and EV Adoption are Driving Strong Demand for High-Performance Metal Finishing Chemicals

The rapid expansion of the global automotive industry continues to significantly boost the metal finishing chemicals market, as car manufacturers increasingly rely on advanced finishing solutions for corrosion protection, improved durability, and better aesthetics. With global vehicle production surpassing 90 million units in 2024 according to OICA, the need for high-performance finishes on steel and aluminum components has grown considerably.

This requirement is even stronger in the electric vehicle segment, where lightweight parts must remain both strong and corrosion-resistant to ensure long battery life and optimal safety. Metal finishing chemicals also help reduce long-term maintenance costs by up to 30%, as noted by the SAE, due to better surface durability.

The use of advanced plating technologies supports global emission reduction goals and fuel-efficiency standards, positioning the market for continuous expansion amid accelerating electrification trends.

Rapid Innovation in Electronics and Semiconductor Manufacturing is Boosting the need for Precise, High-Reliability Finishing Chemicals

Ongoing technological advancements in electronics manufacturing are another powerful growth driver for the metal finishing chemicals market. These chemicals play a crucial role in achieving high-precision plating for circuit boards, connectors, and microcomponents, ensuring better conductivity, reliability, and performance.

With global semiconductor sales crossing US$ 500 billion in 2024 per the SIA, the demand for chemicals such as electroless nickel has surged due to their ability to reduce wear and enhance surface uniformity.

These finishes help improve signal integrity, heat dissipation, and device lifespan-key factors for high-density electronics used in 5G networks, AI systems, and smart consumer products.

Innovations in smaller and more complex electronic components have further pushed manufacturers to adopt high-quality finishing technologies, reducing failure rates by nearly 25%. Rising electronics production across Asia Pacific continues to strengthen market demand and global supply chain resilience.

Restraints - Tight Global Regulations on Hazardous Substances are Increasing Compliance Costs and Slowing Traditional Chemical Adoption

Increasingly strict environmental regulations remain a significant restraint on the metal finishing chemicals market, as governments worldwide enforce limits on hazardous substances such as hexavalent chromium.

Under the European Union’s REACH regulations, many conventional chemical formulations are being phased out, impacting more than 70% of companies operating within the region. Compliance requirements have raised waste management and operational costs by approximately 20%, forcing manufacturers to shift toward safer, eco-friendly alternatives.

In the United States, the EPA enforces similar rules that further restrict emissions and chemical usage, making it challenging for cost-sensitive industries to adapt quickly. These regulatory pressures often slow down innovation cycles, disrupt production lines, and increase the complexity of sourcing approved materials. As a result, companies face limitations in adopting traditional finishing technologies, which ultimately slows market expansion in regions with stringent compliance frameworks.

Volatile Metal Prices and High Manufacturing Expenses are Limiting Market Growth, Especially for Small-Scale Producers

Rising production costs for specialized metal finishing chemicals present a notable challenge, largely due to fluctuations in prices of key raw materials like nickel and chromium. According to the LME, costs for these metals increased by around 15% in 2024, directly affecting manufacturing expenses across the industry. Producers investing in sustainable and advanced chemical formulations also face higher R&D spending, further increasing operational burdens.

Smaller manufacturers, in particular, struggle to maintain profitability because they lack economies of scale, resulting in higher product prices that can discourage adoption in developing markets. Additionally, global supply chain disruptions, rising energy costs, and material shortages put extra pressure on production timelines and pricing structures.

These financial constraints slow market penetration across various Industry sectors such as automotive, construction, and industrial machinery, ultimately affecting overall market competitiveness.

Opportunity - Rising Sustainability Initiatives are Creating Strong Opportunities for Eco-Friendly and Bio-Based Metal Finishing Solutions

The growing shift toward eco-friendly and bio-based metal finishing chemicals presents a major growth opportunity for manufacturers. As global industries adopt greener practices to comply with sustainability mandates, demand for alternatives like trivalent chromium and other low-toxicity coatings has risen sharply.

The UNEP reports a 40% increase in global investments related to green chemistry since 2020, signaling strong momentum toward sustainable manufacturing. These eco-based solutions offer comparable performance to traditional chemicals while reducing environmental impact, making them highly attractive for automotive, aerospace, and electronics industries.

Automakers seeking low-VOC and recyclable coatings can achieve better environmental ratings, potentially increasing their market share by 20% by 2030 as per EU sustainability goals. Companies embracing innovation in bio-based formulations can strengthen their competitive positioning, lower long-term liabilities, and meet the rising demand for safer, high-performance finishing solutions.

Growth in Aerospace and Renewable Energy Sectors is Increasing Demand for Advanced, High-Durability Metal Finishing Chemicals

The increasing use of metal finishing chemicals in the aerospace and renewable energy sectors represents a strong market opportunity. The IATA forecasts a 4.3% annual increase in global passenger traffic through 2032, driving the need for lightweight aircraft components with superior fatigue, corrosion, and heat resistance. Advanced anodizing and plating chemicals help improve the durability of Aluminium structures used in aircraft frames and engine parts.

Meanwhile, the renewable energy sector, particularly wind energy, is accelerating quickly, with global wind turbine installations expected to reach 1,200 GW by 2025, according to the GWEC. Offshore wind components require highly durable anti-corrosion coatings to withstand harsh marine environments, which boosts demand for specialized plating technologies.

Manufacturers focusing on high-strength, lightweight, and eco-friendly formulations can capture long-term contracts, supported by policy incentives such as the U.S. Inflation Reduction Act, enhancing growth in these profitable sectors.

Category-wise Analysis

By Product Type Insights

Plating chemicals dominate the product type segment with nearly 40% market share, mainly because they are essential for electroplating processes that improve corrosion resistance and electrical conductivity. These chemicals are widely used across automotive and electronics industries to ensure uniform metal coating on materials such as steel and copper.

According to NAMF standards, plating chemicals can reduce component wear by about 35%, extending product lifespan. Ongoing innovations such as cyanide-free and eco-friendly formulations further support demand in regulated markets.

By Metal Type Insights

Aluminum leads the metal type segment with around 31% share, primarily due to its use in lightweight applications for automotive, transportation, and construction industries. Metal finishing chemicals used in anodizing help strengthen aluminum’s oxide layer, offering better protection and longer durability.

The Aluminum Association highlights rising use in electric vehicles, where lightweight materials improve energy efficiency by nearly 15%. Aluminum’s recyclability, versatility, and global output surpassing 65 million tons annually according to the IAI contribute to its strong position in the market.

By Technology Insights

Electroplating holds approximately 32% of the technology segment, driven by its accuracy in applying uniform protective coatings on metal surfaces. This technology is widely used in electronics and automotive components to improve corrosion resistance and surface strength.

Tests by the ASTM show that electroplated surfaces offer up to 50% better adhesion strength, enhancing overall durability. The increasing use of automation in electroplating processes supports consistent quality, high-volume production, and cost efficiency, making it a preferred technology across multiple industries.

By Industry Analysis

The automotive industry leads with about 35% share, as metal finishing chemicals are essential for protecting engine parts, structural components, and body panels from corrosion and wear. These finishes help manufacturers comply with global quality and safety standards.

According to OICA, treated components can extend vehicle life by nearly 20%, improving long-term durability. With over 80 million vehicles produced annually worldwide, the sector continues to create strong and stable demand for plating, cleaning, and protective finishing solutions.

Regional Insights

North America Metal Finishing Chemicals Market Analysis

North America continues to lead the global metal finishing chemicals market, supported by a well-established automotive, aerospace, and defense manufacturing infrastructure.

The U.S. especially benefits from significant investments by organizations such as NASA and the DoD, which together contribute over US$ 100 billion toward advanced materials and engineering innovations. These investments encourage the adoption of state-of-the-art plating and coating technologies in defense and space applications.

Regulatory frameworks such as the EPA Clean Air Act promote the use of eco-friendly metal finishing solutions, including trivalent chromium and low-VOC chemicals, which help reduce emissions by nearly 40%. In Canada, growth in electronics manufacturing and semiconductor finishing is supported by favorable trade agreements like USMCA, strengthening North America’s overall market position as a hub for advanced and sustainable metal finishing technologies.

Europe Metal Finishing Chemicals Market Analysis

Europe’s metal finishing chemicals market is shaped largely by strict regulatory frameworks that promote sustainability and quality compliance. Countries such as Germany, France, the U.K., and Spain follow the EU’s REACH and RoHS directives, pushing manufacturers toward safer chemical formulations and greener production methods.

The ECHA’s 2025 proposals for limited exemptions on hexavalent chromium allow certain electroplating processes to continue under tighter emission controls, supporting nearly 25% of the region’s plating operations. Germany’s automotive giants, including Volkswagen, continue to invest heavily in low-VOC and high-durability finishing solutions to meet EU Green Deal goals, which aim to reduce industrial pollution by 55% by 2030.

France and Spain, home to strong aerospace manufacturing activities, rely on advanced anodizing techniques to improve aircraft structure durability. The U.K.’s post-Brexit alignment with EU standards ensures market stability and uninterrupted supply chains.

Asia Pacific Metal Finishing Chemicals Market Analysis

Asia Pacific remains the fastest-growing regional market, driven by large-scale manufacturing in China, Japan, India, and ASEAN countries. China’s industrial expansion, supported by annual steel output exceeding 1 billion tons according to the WSA, drives strong demand for cleaning and plating chemicals used across automotive, construction, and electronics industries.

India’s “Make in India” initiative continues to accelerate local vehicle production, rising 12% in 2024 per SIAM, boosting demand for high-quality metal finishing processes.

Japan’s precision manufacturing sector, especially in consumer electronics and automotive components, relies heavily on electroless plating technologies, supported by METI subsidies for adopting greener chemical solutions.

ASEAN countries like Thailand, Indonesia, and Vietnam benefit from low production costs and expanding export manufacturing, contributing to a stable 6% CAGR driven by industrial growth, infrastructure development, and supportive government policies.

Competitive Landscape

The global metal finishing chemicals market features a moderately consolidated structure, with top players controlling about significant share through strategic expansions and R&D investments. Companies focus on mergers, like acquisitions of specialty chemical firms, to enhance portfolios in sustainable formulations.

Key differentiators include eco-compliant innovations, such as water-based cleaners, while emerging models emphasize circular economy practices like chemical recycling. This landscape encourages collaboration with Industrys for customized solutions, driving growth in high-tech segments.

Key Market Developments:

- In May, 2025: The ECHA proposed controlled exemptions for hexavalent chromium in electroplating, enabling industries to maintain coating performance while shifting toward safer, compliant alternatives. This update supports smoother regulatory adaptation for EU manufacturers.

- In July, 2024: The EPA released enhanced sustainability guidelines encouraging trivalent chromium adoption, helping U.S. metal finishing facilities cut hazardous waste generation by nearly 30% through safer chemical substitutions and improved waste management practices.

- In March, 2024: The IEA reported that advanced anodizing and protective coating chemicals significantly improve EV battery housing durability, prompting major investments in Asia Pacific production hubs to support growing electric vehicle demand.

Companies Covered in Metal Finishing Chemicals Market

- Advanced Chemical Company

- Atotech Deutschland GmbH

- Coral Chemical Co.

- C. Uyemura & Co. Ltd.

- Lonza Group

- McGean Specialty Chemicals Group

- Quaker Chemicals Corp.

- Chemetall, Elementis

- DOW Chemicals

- Platform Specialty Products Corporation

- Houghton International Inc.

- NOF Corporation

- HENKEL AG

- BASF Corporation

- PPG Industries, Inc.

Frequently Asked Questions

The market is expected to reach US$ 14.3 Bn by 2032, growing from US$ 10.5 Bn in 2025 at a CAGR of 4.5%, driven by automotive and electronics demand.

Key drivers include automotive sector expansion and electronics manufacturing growth, with global vehicle production over 90 million units and semiconductor sales at US$ 500 billion in 2024 fueling need for corrosion-resistant finishes.

Electroplating leads with a 42% share, providing precise coatings for enhanced conductivity and durability in electronics and automotive applications.

North America leads due to its advanced manufacturing in automotive and aerospace, supported by EPA regulations and investments exceeding US$ 100 billion in materials R&D.

The shift to sustainable bio-based formulations offers growth, aligning with EU Green Deal and UNEP goals to reduce toxicity, capturing 20% more share in aerospace by 2030.

Major Players include Atotech Deutschland GmbH, Chemetall, HENKEL AG, BASF Corporation, and PPG Industries, Inc., focusing on eco-innovations and global expansions.