- Smart Packaging

- Metallized Paper Market

Metallized Paper Market Size, Share, and Growth Forecast, 2026 - 2033

Metallized Paper Market by Product Type (Lamination, Vacuum Lamination, Others), Thickness (51-100 GSM, Above 150 GSM, Others), Application, End-use Industry, and Regional Analysis for 2026 - 2033

Metallized Paper Market Size and Trends Analysis

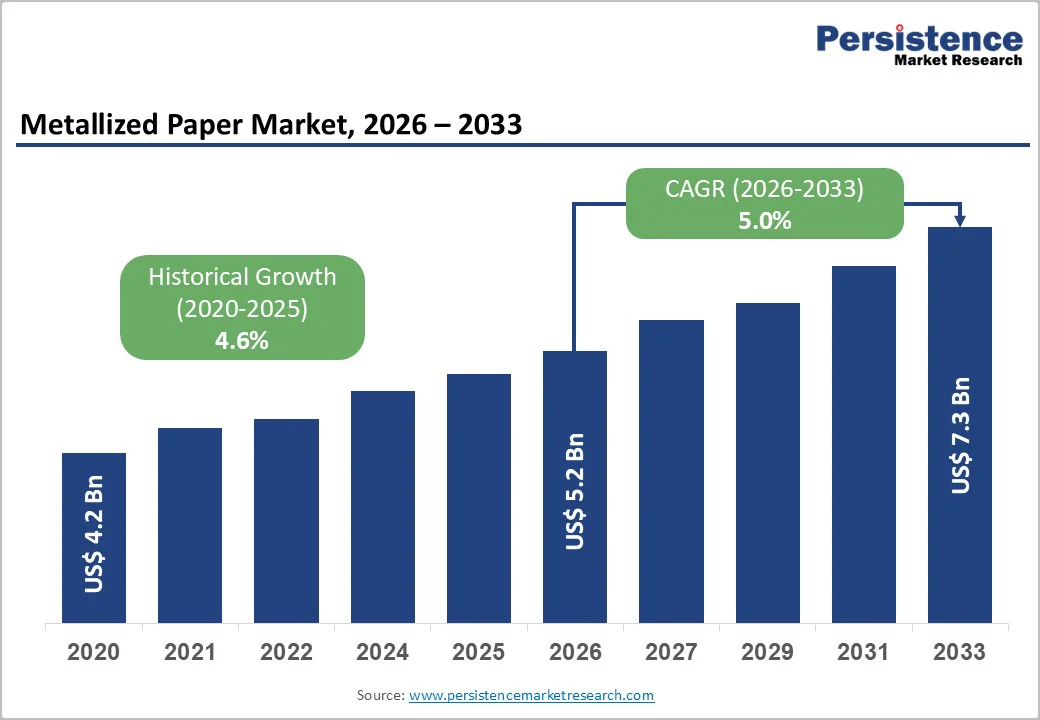

The global metallized paper market size is likely to be valued at US$5.2 billion in 2026 and is expected to reach US$7.3 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033, driven by rising demand for high-barrier and visually premium packaging in food & beverage and personal care applications, growing adoption of flexible packaging formats, and advancements in vacuum metallization technologies that enhance barrier performance while reducing material weight.

Strict retail aesthetic standards and a shift toward paper-based metallic finishes are replacing heavier aluminum foils. Growth is driven by product premiumization and expanded metallizing capacity, while aluminum price volatility and recycling challenges constrain adoption.

Key Industry Highlights

- Leading Region: North America is projected to account for 36.5% of the global metallized paper market, supported by strong demand from premium food, beverage, and personal care packaging, along with advanced converting and metallizing infrastructure.

- Fastest-growing Region: Asia Pacific, driven by expanding packaged food consumption, rising middle-class populations, and large-scale capacity additions across China, India, and Southeast Asia.

- Investment Plans: Packaging manufacturers are actively investing in vacuum metallization, coating, and slitting capacity, with a strong focus on recyclable and low-metal metallized paper solutions, particularly in North America and Europe, to align with sustainability regulations and brand-owner commitments.

- Dominant Product Type: Lamination is anticipated to account for approximately 56.2% of the market, driven by its extensive use in high-speed packaging operations, superior machinability, and reliable barrier performance across flexible packaging, labels, and decorative overwrap applications.

- Leading Application: Flexible packaging is estimated to be nearly 42.7% of demand, supported by high consumption volumes in food and beverage packaging and growing adoption of paper-forward metallized solutions for shelf differentiation.

| Key Insights | Details |

|---|---|

| Metallized Paper Market Size (2026E) | US$5.2 Bn |

| Market Value Forecast (2033F) | US$7.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growth in Packaged Food & Beverage and Premium Labeling Demand

Rising consumption of packaged food and beverages, coupled with retail premiumization trends, is increasing demand for visually distinctive and shelf-enhancing packaging materials such as metallized paper. The metallized layer delivers reflective finishes and improved light and moisture barrier properties compared with uncoated paper, supporting both functional protection and brand differentiation.

Flexible and single-serve packaging formats, including snack pouches, coffee sachets, and lidding materials, continue to expand at a faster pace than rigid formats. This shift is translating into higher conversion volumes for metallized paper across labels and flexible packaging applications, encouraging sustained investments in metallizing equipment and downstream converting capacity.

Technology Advances in Vacuum Metallization and Coating Processes

Advancements in vacuum metallization, barrier coating technologies, and adhesive and primer chemistries are enabling metal deposition on thinner and lower-cost paper substrates while improving adhesion and barrier performance. These innovations reduce reliance on full aluminum foil lamination in several applications, allowing lighter packaging structures with comparable shelf-life performance for many dry and semi-dry products.

Converters benefit from material down-gauging, lower transportation costs, and improved sustainability profiles without compromising product protection. Ongoing upgrades to metallizing lines and the introduction of high-barrier metallized grades are directly supporting the projected market growth rate over the forecast period.

Regulatory and Retailer Pressure for Recyclable, Paper-Forward Packaging

Increasing regulatory focus on packaging sustainability and retailer commitments to circular economy targets are accelerating demand for paper-forward packaging designs. Metallized paper solutions that meet aesthetic and barrier requirements while reducing overall material complexity are gaining traction.

Suppliers are developing structures with lower metal loading and designs that facilitate separation during recycling. When engineered for recyclability, metallized paper can replace traditional foil laminates in selected applications, creating a medium-term growth pathway as collection, sorting, and recycling infrastructure continues to improve.

Barrier Analysis - Aluminum Price Volatility and Cost Pressures

Fluctuations in aluminum pricing have a direct impact on metallizing costs, affecting metal targets, energy consumption, and overall processing expenses. Periodic price increases can compress margins for converters and slow adoption in cost-sensitive segments such as commodity food packaging.

A sustained increase in aluminum prices can materially raise raw-material costs per square meter, forcing manufacturers to pass costs downstream or shift toward alternative barrier coatings. As a result, brand owners may delay packaging format transitions during periods of pricing instability.

Recycling Complexity of Multilayer Structures

Metallized paper products that are laminated with polymers or foils can present challenges for recycling systems. In many cases, metallized layers are treated as contaminants unless they are easily separable, increasing compliance costs under extended producer responsibility frameworks.

Stricter regulatory measures could reduce demand for non-recyclable metallized laminates or increase the total cost of ownership for brand owners. While recyclable and mono-material designs mitigate this risk, they often require investment in new materials, processing methods, and specialized adhesives.

Opportunity Analysis - Expansion in Personal Care and Premium Beverage Labeling

Personal care and premium beverage brands are increasingly using high-value labels and decorative wraps to reinforce brand identity and perceived quality. As the fastest-growing end-use segment, personal care offers strong potential for higher-margin metallized paper products.

Converting this demand into premium label materials with enhanced gloss, printability, and tactile appeal can significantly improve average selling prices for suppliers. If growth in this segment continues at an accelerated pace, it represents a substantial incremental revenue opportunity within the overall market by 2033.

Down-Gauging and Mono-Material Innovation

There is a growing demand for metallized paper solutions that enable material down-gauging while maintaining barrier and print performance. These products address both cost efficiency and sustainability objectives. Replacing a portion of traditional foil-laminated structures with down-gauged metallized paper could unlock meaningful incremental market value over the forecast period.

Strategic investment in research partnerships, pilot metallizing lines, and life-cycle assessment validation can accelerate adoption and improve qualification with large retailers and brand owners.

Category-wise Analysis

Product Type Insights

Laminated metallized paper is anticipated to hold a 56.2% market share, due to its extensive adoption in high-speed and high-volume packaging operations across food, beverage, and tobacco applications. These structures typically combine metallized paper with polymer films such as polyethylene or polypropylene, enhancing tensile strength, seal integrity, and moisture resistance while preserving metallic aesthetics.

The format is widely used in lidding materials, wrap-around labels, and decorative overwraps for confectionery, snacks, instant beverages, and cigarette packaging, where consistent barrier performance and machinability are critical. From a brand perspective, laminated metallized paper is preferred by large consumer goods manufacturers seeking reliable performance on automated packaging lines with minimal downtime.

Its compatibility with gravure and flexographic printing allows brand owners to maintain a consistent visual identity across product portfolios. Expansion of ready-to-eat food brands and premium confectionery lines in both developed and emerging markets continues to reinforce demand for laminated formats, particularly where shelf-life stability and visual differentiation are equally prioritized.

Vacuum metallization is likely to be the fastest-growing segment as advancements in deposition technology allow the application of ultra-thin metallic layers with improved adhesion, uniformity, and optical performance.

This process significantly reduces metal usage compared to traditional foil lamination while delivering comparable reflectivity and barrier properties for light, oxygen, and moisture in selected applications. As a result, vacuum-metallized paper is increasingly adopted in premium packaging and labeling where weight reduction and sustainability considerations are becoming more prominent.

Growth in this segment is supported by premium beverage brands, cosmetics manufacturers, and specialty food producers seeking metallic finishes without the cost burden or recycling limitations of thicker foil-based laminates.

Brand expansion strategies focused on limited-edition packaging, seasonal launches, and premium sub-brands are accelerating the adoption of vacuum-metallized paper, particularly in labels and decorative wraps. The segment also benefits from improved compatibility with recycling systems when designed with lower metal loading, aligning with evolving sustainability targets.

Application Insights

Flexible packaging is expected to be the largest application segment, accounting for approximately 42.7% of total metallized paper demand.

Its leadership is driven by widespread use in food and beverage packaging, including snacks, bakery products, powdered beverages, and confectionery items that require protection from light and moisture while maintaining visual appeal. Metallized paper in flexible formats offers a distinctive balance between a paper-like texture and premium metallic finishes, making it attractive for brands aiming to differentiate products on retail shelves.

Large-scale brand owners continue to expand flexible packaging formats due to their lower material consumption, reduced transportation costs, and adaptability to various pack sizes.

Growth in single-serve, portion-controlled, and on-the-go consumption formats has further increased demand for metallized paper-based flexible packaging. As brands seek alternatives to plastic-heavy laminates, metallized paper solutions that meet functional and aesthetic requirements are increasingly incorporated into new product launches and regional portfolio expansions.

Labels are projected to be the fastest-growing application segment, supported by rising demand for high-impact branding and product authentication. Metallized paper labels are widely used in premium beverages, personal care products, specialty foods, and household goods, where shelf differentiation and brand recognition play a decisive role in purchasing decisions.

The metallic sheen enhances visual depth, color vibrancy, and print effects, enabling brands to communicate premium positioning more effectively.

Growth in this segment is closely linked to brand expansion strategies such as SKU diversification, regional market entry, and limited-edition product releases.

The rapid growth of e-commerce has also increased the importance of visually distinctive labeling that maintains brand integrity across digital and physical retail channels. Metallized labels further support functional requirements such as tamper evidence and anti-counterfeiting, making them a preferred choice for high-value and brand-sensitive products.

Regional Insights

North America Metallized Paper Market Trends-Premium Retail Demand and Domestic Capacity Expansion

North America is likely to account for approximately 36.5% of the market, with the U.S. acting as the primary growth engine. Strong consumer spending power, a highly developed retail ecosystem, and sustained demand for premium food, beverage, and personal care products continue to support consistent consumption.

Metallized paper is widely used across snack packaging, beverage labels, tobacco wraps, and personal care cartons, where visual differentiation and shelf impact remain critical. The region’s advanced printing and converting infrastructure allows rapid commercialization of specialty and short-run packaging formats, supporting frequent product refresh cycles.

Sustainability initiatives and extended producer responsibility frameworks are reshaping material selection across the U.S. and Canada. Several large packaging suppliers operating in North America have expanded their recyclable and paper-forward packaging portfolios, including metallized paper grades designed for reduced metal content and improved recyclability.

Investments in domestic metallizing, slitting, and coating capacity by multinational packaging companies have shortened lead times and reduced reliance on imports. These developments strengthen regional supply resilience while enabling brand owners to adopt premium metallized designs that align with evolving sustainability commitments.

Europe Metallized Paper Market Trends - Regulation-Led Recyclable Innovation for Luxury Packaging

Europe represents a structurally important market characterized by stringent environmental regulations and strong demand for premium and luxury packaging solutions. Germany, France, the U.K., and Spain remain the core consumption centers, supported by advanced converting capabilities, strong beverage and confectionery industries, and a well-established luxury goods sector.

Metallized paper is widely adopted in labels, decorative wraps, and specialty cartons, particularly in premium spirits, confectionery, and cosmetics packaging, where visual appeal and brand heritage are central to consumer perception.

Regulatory harmonization across the European Union emphasizes recyclability, material reduction, and circular design, accelerating the shift toward compliant metallized paper solutions. Several European packaging groups have invested in low-metal and recyclable metallized paper grades to meet these requirements, often integrating life-cycle assessment data into product development.

The region has also seen collaboration between material suppliers and brand owners to redesign packaging formats for improved recyclability without compromising aesthetics. These efforts reinforce Europe’s position as a technology and sustainability benchmark for metallized paper innovation.

Asia Pacific Metallized Paper Market Trends - High-Volume Manufacturing Scale and Emerging Market Adoption

Asia Pacific is likely to be the fastest-growing regional market, driven by rising packaged food consumption, expanding middle-class populations, and rapid urbanization. China and India function as both major consumption markets and production hubs, supported by large-scale investments in metallizing, coating, and converting capacity.

Domestic packaging companies in these countries continue to scale operations to meet demand from food, beverage, tobacco, and personal care brands, while also supplying export markets in Southeast Asia, the Middle East, and Africa.

Southeast Asian markets, including Indonesia, Vietnam, and Thailand, are witnessing increased adoption of metallized paper in cost-sensitive packaging applications as brands upgrade from basic printed paper to higher-value decorative formats.

Regional players and multinational packaging groups with operations in Asia Pacific have expanded capacity to support flexible packaging and label demand, benefiting from lower manufacturing costs and proximity to fast-growing consumer markets.

These manufacturing and cost advantages position Asia Pacific as a critical driver of global volume growth, while ongoing quality improvements are enabling wider adoption of metallized paper in premium and export-oriented applications.

Competitive Landscape

The global metallized paper market shows moderate concentration. A group of large multinational packaging companies and regional specialty film manufacturers account for a substantial portion of the total supply, while numerous smaller converters serve localized demand. Competition is primarily based on technological capability, product differentiation, cost efficiency, and sustainability performance.

Recent strategic activity includes expansion of metallizing and slitting capacity in key markets, increased investment in recycling and circular-economy projects, and the introduction of specialty metallized grades targeting premium packaging and technical applications. These developments reflect a focus on regional supply optimization, sustainability compliance, and portfolio diversification.

Leading players emphasize innovation in high-barrier and printable metallized products, regional capacity expansion for just-in-time supply, and development of recyclable or mono-material solutions. Vertical integration and close collaboration with converters and brand owners remain central to maintaining competitive advantage.

Key Industry Developments

- In 2025, Lecta expanded its Metalvac product range with the launch of Metalvac Seal Oxygen Barrier metallized paper, designed to improve industrial efficiency and sustainability performance in high-barrier packaging applications.

- In February 2025, Koehler Paper deployed its “Koehler NexPlus Advanced” flexible packaging paper in commercial packs for convenience meal products, demonstrating enhanced oxygen, mineral oil, and grease barrier properties for ready-to-eat food applications.

Companies Covered in Metallized Paper Market

- AR Metallizing

- Amcor

- Mondi

- Uflex

- Cosmo First

- Jindal Poly Films

- Polyplex Corporation

- Lecta Group

- Innovia Films

- Huhtamaki

- Sealed Air

- Koehler Paper

- Glatfelter

- Brigl & Bergmeister

- UPM Specialty Papers

- Sappi

- Stora Enso

- Avery Dennison

- Transcontinental

- Kuraray

Frequently Asked Questions

The global metallized paper market is projected to be valued at US$5.2 billion in 2026.

By 2033, the metallized paper market is expected to reach US$7.3 billion, supported by steady demand across packaging and labeling applications.

Key trends include growing adoption of paper-forward and recyclable packaging, rising demand for premium labels and decorative packaging, increased use of vacuum metallization for lightweight barrier solutions, and capacity expansions in Asia Pacific to support both domestic consumption and exports.

Lamination is the leading segment, accounting for approximately 56.2% of total market share, due to its widespread use in high-speed flexible packaging, lidding, and decorative overwrap applications.

The market is projected to grow at a CAGR of 5.0% between 2026 and 2033.

Major players with strong product portfolios include Amcor, Mondi, Uflex, Cosmo First, and Jindal Poly Films.