- Metals & Minerals

- Lithium Metal (99.9%) Market

Lithium Metal (99.9%) Market Size, Share, and Growth Forecast 2026 - 2033

Lithium Metal (99.9%) Market by Origin (Salt Lake Brine, Lithium Ores/Hard Rock Mining, Recycled Lithium), Grade (Battery Grade, Industrial Grade, Ultra-High Purity), End-User (Primary Batteries, Electric Vehicle (EV) Batteries, Aerospace & Defense, Pharmaceuticals & Medical, Synthetic Polymers, Others), by Regional Analysis, 2026 - 2033

Lithium Metal (99.9%) Market Size and Trend Analysis

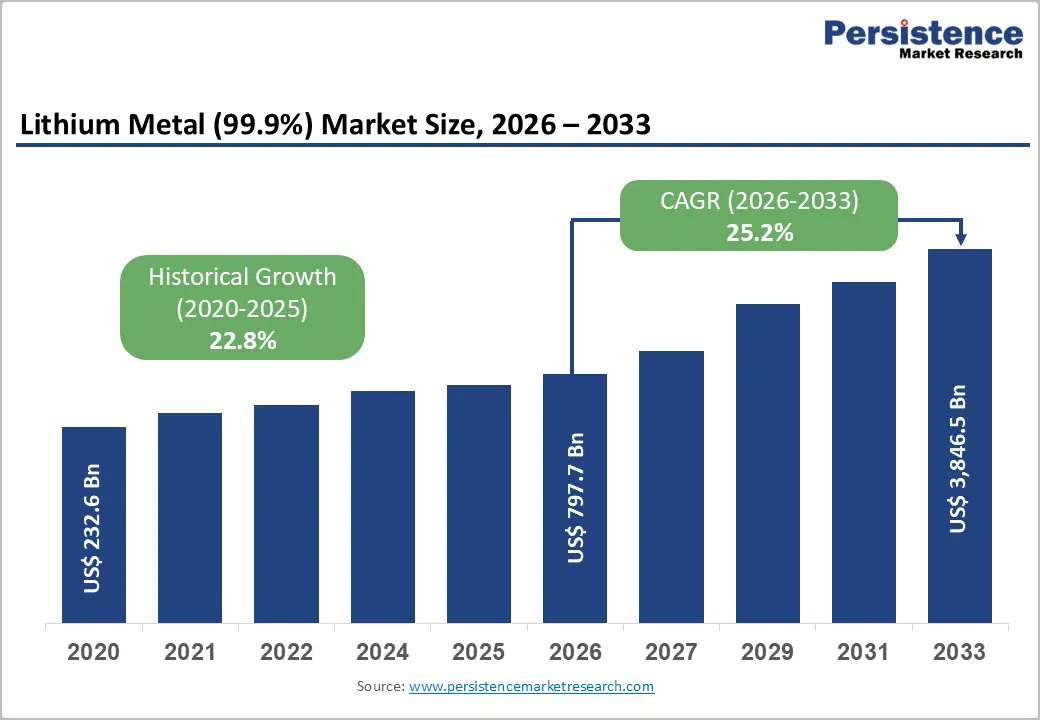

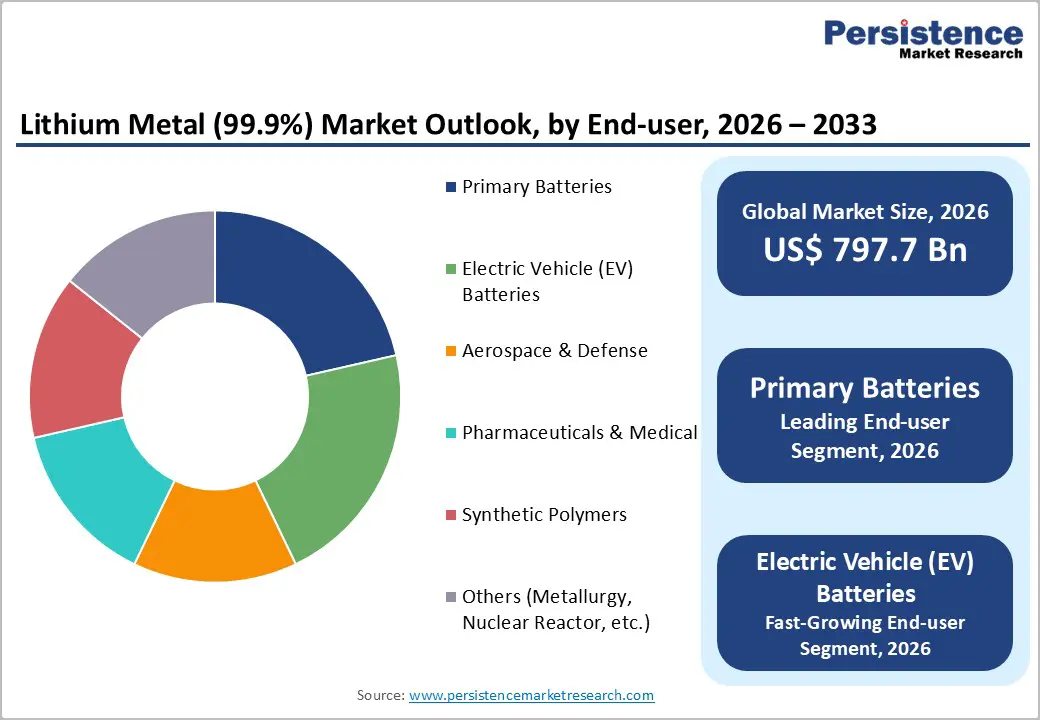

The global Lithium Metal (99.9%) market size is expected to be valued at US$ 797.7 billion in 2026 and projected to reach US$ 3,846.5 billion by 2033, growing at a CAGR of 25.2% between 2026 and 2033.

The market's exceptional trajectory is primarily fueled by the accelerating global shift toward electrified transportation and grid-scale energy storage, which has dramatically elevated demand for high-purity lithium metal as a critical anode material in next-generation solid-state batteries. Surging electric vehicle adoption, with global EV sales surpassing 14 million units in 2023 according to the International Energy Agency (IEA), combined with ambitious government decarbonization targets, manufacturing incentives, and robust gigafactory investments, is reinforcing a sustained multi-decade demand cycle for lithium metal across industrial, defense, and energy applications worldwide.

Key Industry Highlights

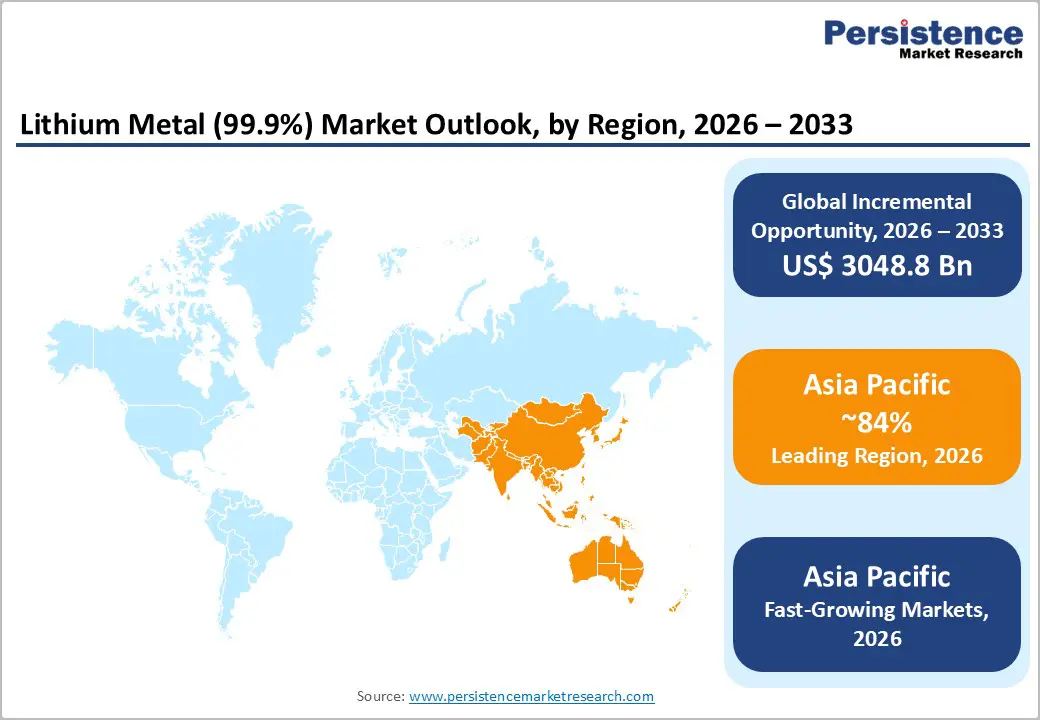

- Leading Region: Asia Pacific leads the global Lithium Metal (99.9%) market with approximately 84% share in 2025, underpinned by China's dominant lithium processing infrastructure, massive battery gigafactory capacity, and integrated downstream EV manufacturing ecosystem.

- Fastest Growing Region; Asia Pacific is also the fastest growing region, projected at a CAGR of 27% (2026–2033), driven by India's emerging PLI-backed battery manufacturing base, ASEAN's rapid EV adoption, and continued capacity expansion by Chinese producers.

- Dominant Segment: Battery Grade lithium metal dominates the Grade category with approximately 51% market share in 2025 and is the fastest growing grade segment at 30% CAGR, reflecting the explosive global expansion of EV and energy storage battery manufacturing.

- Fastest Growing Segment: Electric Vehicle (EV) Batteries represent the fastest growing end-use application, projected at a CAGR of 45% from 2026 to 2033, driven by global EV policy mandates and the anticipated commercial rollout of lithium metal anode-based solid-state batteries by 2027–2030.

- Key Opportunity: The key market opportunity lies in Recycled Lithium, growing at 31% CAGR, as the EU Battery Regulation 2023/1542, rising end-of-life EV battery volumes between 2025–2030, and cost-competitive closed-loop economics collectively attract substantial capital investment into battery recycling infrastructure globally.

| Key Insights | Details |

|---|---|

|

Lithium Metal (99.9%) Market Size (2026E) |

US$ 797.7 Billion |

|

Market Value Forecast (2033F) |

US$ 3,846.5 Billion |

|

Projected Growth CAGR (2026–2033) |

25.2% |

|

Historical Market Growth (2020–2025) |

22.8% |

Market Dynamics

Drivers - Rapid Growth in Electric Vehicle Production and Battery Manufacturing

The accelerating adoption of EVs remains the most significant driver for the lithium metal market. Lithium metal is increasingly used in advanced battery chemistries, including lithium metal and solid-state batteries, which offer higher energy density and longer driving ranges compared to conventional lithium-ion batteries. According to the International Energy Agency (IEA), global EV sales topped 17 million units in 2024, rising by more than 25%. Just the additional 3.5 million cars sold in 2024, compared to 2023, outnumber total electric car sales for the whole of 2020. Government-led decarbonization policies and zero-emission vehicle mandates across major economies are compressing long-term battery demand into a shorter timeframe.

The U.S. Department of Energy (DOE) targets a 50% EV sales share by 2030, while the European Commission’s “Fit for 55” package mandates a 100% reduction in CO2 emissions from new passenger cars by 2035. These regulations are catalyzing large-scale investments in battery gigafactories, directly increasing demand for high-purity lithium metal. Lithium demand for batteries is expected to more than quadruple from 720,000 metric tons in 2022 to around 3.1 million metric tons by 2030, underscoring the need for high-purity feedstock such as 99.9% lithium metal. Mineral statistics show that global lithium mine production rose to roughly 180,000–240,000 metric tons between 2023 and 2024, reflecting rapid upstream expansion in response to battery demand.

Expanding Defense, Aerospace, and Industrial Primary Battery Demand

Beyond the EV sector, defense, aerospace, and industrial primary battery applications are emerging as a significant incremental demand channel for 99.9% purity lithium metal. Lithium primary batteries, employed in guided munitions, soldier-worn electronics, emergency locator transmitters, and space power systems, require ultra-high purity metal to satisfy stringent energy density and operational reliability standards. The U.S. Department of Defense (DoD) has consistently increased procurement of advanced lithium battery systems as part of its force modernization programs. The Stockholm International Peace Research Institute (SIPRI) reported global defense expenditure reaching a record US$ 2.44 trillion in 2023, with advanced battery procurement identified as a rapidly growing cost center. Furthermore, NASA's Artemis lunar program and commercial deep-space missions are actively evaluating lithium metal power configurations, underscoring the sustained multi-sector demand underpinning market growth.

Restraints - Geopolitical Concentration and Supply Chain Vulnerabilities

The lithium metal supply chain is critically concentrated in a limited number of nations, creating systemic vulnerability to supply disruptions and price volatility that restrain market expansion. According to the U.S. Geological Survey (USGS) Mineral Commodity Summaries 2024, Chile and Australia collectively account for over 70% of global lithium mine production. Processing capacity is even more concentrated, with China controlling approximately 60% of global lithium refining. Chile's partial nationalization of its lithium industry in 2023 and ongoing tensions surrounding Democratic Republic of Congo's cobalt supply demonstrated how politically sensitive critical mineral supply chains remain. Such structural vulnerabilities amplify cost uncertainty for downstream manufacturers and restrict their ability to execute long-term capacity planning, dampening investment confidence in lithium metal-intensive technologies.

Reactivity, Safety, and Regulatory Compliance Costs

Lithium metal's inherently high chemical reactivity creates substantial safety, storage, and logistics challenges that elevate operational costs and limit the pace of market penetration. Lithium metal reacts violently with moisture and atmospheric gases, necessitating specialized inert-atmosphere handling, transport, and storage infrastructure. The United Nations Model Regulations on the Transport of Dangerous Goods classify lithium metal as a Class 4.3 dangerous substance, imposing stringent documentation, packaging, and carrier requirements that significantly increase logistics costs. Regulatory bodies including the U.S. Occupational Safety and Health Administration (OSHA) and the European Chemicals Agency (ECHA) impose increasingly rigorous workplace safety standards for lithium metal handling, raising compliance burdens for producers and end-users alike and acting as a meaningful barrier to entry for new market participants.

Opportunity - Commercialization of Solid-State Battery Technology

The imminent commercial rollout of solid-state battery (SSB) technology represents the single largest near-term opportunity for the lithium metal market. Unlike conventional lithium-ion cells, solid-state batteries utilize lithium metal directly as the anode, eliminating graphite and delivering significantly superior energy density, faster charging, and enhanced safety. Toyota Motor Corporation has announced plans to begin solid-state EV battery production by 2027–2028, while Volkswagen Group (through its equity stake in QuantumScape) and Hyundai Motor Group have committed multi-billion dollar investments targeting SSB commercial availability by 2030. According to the U.S. Department of Energy (DOE), solid-state cells could achieve energy densities exceeding 500 Wh/kg, roughly double current lithium-ion benchmarks. This technology transition is expected to meaningfully increase per-unit lithium metal consumption, creating a structural demand uplift that will further accelerate the market's already elevated forecast CAGR of 25.2% through 2033.

Recycled Lithium as a Scalable Low-Carbon Supply Vector

The recycled lithium segment, projected to grow at a CAGR of 31% between 2026 and 2033, the fastest across all Origin categories, presents a transformative opportunity for producers and technology companies developing closed-loop battery supply chains. Tightening circular economy legislation, most notably the European Union Battery Regulation (EU) 2023/1542, which mandates a minimum 80% lithium recycling efficiency by 2031, is compelling manufacturers to establish and invest in end-of-life battery recovery infrastructure. Companies including Li-Cycle Holdings, Umicore N.V., and Redwood Materials are scaling hydrometallurgical lithium recovery technologies capable of producing battery-grade and ultra-high purity output. Critically, the first large wave of EV battery packs from vehicles sold during 2015–2020 is approaching end-of-life between 2025 and 2030, creating a rapidly growing pipeline of recyclable lithium feedstock. This convergence of regulatory mandates, maturing technology, and feedstock availability will unlock a substantial, structurally sustainable new supply channel for market participants.

Category-wise Analysis

Origin Insights

Lithium Ores/Hard Rock Mining dominates the global Lithium Metal (99.9%) market by origin, commanding approximately 94% market share in 2025. This dominance reflects the segment's structural advantages in production scale, chemical consistency, and geographic accessibility across major supply hubs. Australia's Pilbara region, home to Pilbara Minerals' Pilgangoora project and Albemarle Corporation's Greenbushes operation, the world's largest hard rock lithium mine, collectively underpins global spodumene concentrate supply. Hard rock deposits yield high-grade spodumene with 6–7% Li2O content, which can be processed into battery-grade and ultra-high purity lithium metal with significantly greater chemical predictability and consistency than brine-based sources. The Australian Government's Critical Minerals Strategy 2023–2030 and associated downstream processing incentives further consolidate this segment's leadership, while the segment's faster mine ramp-up timelines and established logistics infrastructure continue to make it the preferred origin for global lithium metal refiners.

Grade Insights

Battery grade lithium metal holds the leading position within the Grade category, commanding approximately 51% market share in 2025 and simultaneously representing the fastest growing grade segment at a projected CAGR of 30% through 2033. This segment's dominance is driven by the explosive global expansion of lithium-ion and next-generation solid-state battery manufacturing. Battery-grade specifications require 99.9% or higher purity lithium metal with strictly controlled impurity profiles for elements including sodium, potassium, calcium, and iron, as mandated by International Electrotechnical Commission (IEC) and proprietary cell maker qualification standards. China's battery manufacturing ecosystem, anchored by Contemporary Amperex Technology Co., Limited (CATL) and BYD, consumes over 70% of global lithium battery cell production capacity. Investment programs such as the U.S. Advanced Battery Manufacturing initiative and the European Battery Alliance continue to fund new battery-grade lithium refining capacity, cementing this segment's preeminent position globally.

End-user Insights

Primary batteries represent the leading end-user segment with approximately 27% market share in 2025, supported by decades of stable demand from military, medical device, consumer electronics, and industrial instrumentation applications. Lithium primary chemistries, notably lithium thionyl chloride (LiSOCl2) and lithium manganese dioxide (LiMnO2), are valued for their exceptional shelf life of up to 20 years, wide operating temperature range of −55°C to +85°C, and high volumetric energy density. The U.S. military is the world's single largest consumer of lithium primary batteries, sourcing large volumes for guided munitions, soldier-worn electronics, and emergency positioning systems. Proliferating industrial IoT sensor deployments and smart metering rollouts, driven by IEC standards for advanced metering infrastructure, are sustaining incremental primary battery demand. Specialized producers including Electrochem (a Integer Holdings company) and Tadiran Batteries supply ultra-high purity lithium metal-based primary batteries for critical and high-reliability applications globally.

Regional Insights

North America Lithium Metal (99.9%) Market Trends and Insights

North America's lithium metal market is being dynamically reshaped by domestic energy security imperatives and accelerating electric vehicle ecosystem development. The U.S. Inflation Reduction Act (IRA) of 2022 established powerful incentives for critical mineral processing and battery manufacturing, with Advanced Manufacturing Production Credits incentivizing domestic lithium refining capacity investment. The U.S. Department of Energy's National Blueprint for Lithium Batteries 2021–2030 explicitly targets lithium metal anode technologies for next-generation batteries, channeling research funding to institutions including Argonne National Laboratory and Oak Ridge National Laboratory. As of 2024, Albemarle Corporation operates the Silver Peak brine facility in Nevada, the only producing lithium operation in the continental United States, while new hard rock projects in North Carolina (Piedmont Lithium) and Arkansas are in advanced development stages.

Canada is emerging as a strategic supply chain partner through its Canadian Critical Minerals Strategy, supporting lithium exploration and processing investments in Ontario, Quebec, and the Northwest Territories. The region's world-class innovation ecosystem, spanning MIT, the University of Texas at Austin, and Stanford University, is advancing solid-state electrolyte and lithium metal anode research, positioning North America as a technology leader even as primary production capacity is built out. Defense procurement programs administered by the U.S. DoD further anchor non-EV demand for high-purity lithium metal across the region.

Europe Lithium Metal (99.9%) Market Trends and Insights

Europe's lithium metal market is being rapidly shaped by an aggressive regulatory and industrial policy framework aimed at securing indigenous battery supply chains. The European Battery Alliance (EBA), operating under the European Commission, is coordinating a fully integrated European battery value chain roadmap covering lithium extraction, refining, cell manufacturing, and recycling by 2030. The EU Critical Raw Materials Act (CRMA), enacted in 2024, designates lithium as a strategic raw material and mandates that at least 10% of the EU's annual critical mineral consumption be domestically sourced by 2030, accelerating lithium mining projects in Portugal, Czech Republic, and Finland. The EU Battery Regulation 2023/1542 further mandates minimum 80% lithium recycling efficiency by 2031, spurring significant investment in battery recycling infrastructure across the continent.

Germany leads European EV-driven lithium demand as the continent's largest automotive manufacturing nation, with Volkswagen Group, BMW AG, and Mercedes-Benz Group committed to full fleet electrification. Northvolt AB, the Swedish battery manufacturer, is scaling gigafactory capacity at its Ett facility in Skellefteå, while France and Spain are advancing domestic EV battery strategies under their respective national industrial programs. The United Kingdom's Faraday Institution is delivering solid-state battery research breakthroughs, collectively driving Europe's growing appetite for battery-grade and ultra-high purity lithium metal.

Asia Pacific Lithium Metal (99.9%) Market Trends and Insights

Asia Pacific commands approximately 84% of the global lithium metal (99.9%) market in 2025 and is concurrently the fastest growing region, projected to expand at a CAGR of 27% from 2026 to 2033. China is the uncontested epicenter of global lithium metal supply and demand, accounting for approximately 70–75% of global lithium chemical refining capacity through vertically integrated producers including Ganfeng Lithium Co., Ltd., Tianqi Lithium Corporation, and Chengxin Lithium Group Co., Ltd. The Chinese government's 14th Five-Year Plan and New Energy Vehicle (NEV) industry policy explicitly mandate expanded battery manufacturing and critical minerals processing, ensuring China's continued dominance across the lithium value chain and sustaining the region's structural market leadership.

Japan and South Korea contribute significantly through world-class battery technology companies, Panasonic Holdings, Samsung SDI, and LG Energy Solution, which collectively represent major battery-grade lithium metal consumption centers. India is emerging as a high-growth market, with the Production-Linked Incentive (PLI) Scheme for Advanced Chemistry Cell (ACC) Batteries attracting over US$ 2 billion in committed investments as of 2024, per the Ministry of Heavy Industries, Government of India. Australia anchors regional supply as the world's largest hard rock lithium producer, with Pilbara Minerals, Mineral Resources Limited, and IGO Limited expanding mine output to satisfy surging downstream Asian demand.

Competitive Landscape

The lithium Metal (99.9%) market demonstrates a moderately consolidated structure, with a limited number of established producers accounting for a significant share of global supply. Competition is primarily driven by companies with strong integration across the lithium value chain, from upstream resource development to refining and high-purity lithium metal production. Market participants are increasingly focusing on securing long-term access to lithium resources through strategic mining investments, joint ventures, and supply agreements to ensure stable raw material availability.

Business strategies across the industry emphasize capacity expansion, technological advancement, and supply chain integration to support the rapidly growing battery and energy storage sectors. Companies are investing in advanced purification technologies to achieve ultra-high purity lithium metal required for next-generation batteries and specialty applications. In addition, the adoption of innovative extraction methods, particularly direct lithium extraction (DLE), is gaining momentum as producers seek to improve recovery rates and reduce environmental impact. Partnerships with battery manufacturers and investments in recycling infrastructure are also emerging as important strategic approaches to strengthen supply security and support long-term market growth.

Key Developments:

- July, 2025: Ganfeng Lithium acquired the remaining 40% stake in the Goulamina lithium mine for US$ 342.7 million, gaining full ownership. The move strengthens its global supply base as 2024 LCE production rose 25% to 130,253 tons, supported by project ramp-ups.

- September, 2025: Chengxin Lithium Group plans to acquire a 21% stake in Sichuan Qicheng Mining for US$ 205 million, enhancing its control over the Murong lithium deposit, one of the highest-grade lithium mines in Sichuan. This deposit has proven Li2O resources of 989,600 tonnes with a production capacity of 3 million tonnes per annum, strengthening Chengxin’s position in the global lithium metal supply chain.

- December, 2025: Rio Tinto announced a strategic push to expand its lithium production, following its US$ 6.7 billion acquisition of Arcadium Lithium. The company plans to scale production from 75,000 mt/y to 200,000 mt/y of lithium carbonate equivalent by 2028 through four major projects in Canada and Argentina, including the 32,000 mt/y Becancour hydroxide facility and multiple direct lithium extraction plants. This expansion targets low-cost, large-scale lithium production to meet surging demand from electric vehicles and energy storage markets.

Companies Covered in Lithium Metal (99.9%) Market

- Albemarle Corporation

- Tianqi Lithium Corporation

- Ganfeng Lithium Co., Ltd.

- Rio Tinto (Arcadium Lithium)

- Chengxin Lithium Group Co., Ltd.

- China Energy Lithium Co., Ltd.

- China Lithium Products Technology Co., Ltd.

Frequently Asked Questions

The global Lithium Metal (99.9%) market is estimated to reach about US$ 797.7 billion in 2026.

Rapid electric vehicle adoption and the development of solid-state batteries are the primary demand drivers.

Asia Pacific leads the global market due to its strong lithium processing and battery manufacturing ecosystem.

The commercialization of solid-state batteries using lithium metal anodes represents the key growth opportunity.

Key players include Albemarle Corporation, Ganfeng Lithium Co., Ltd., Tianqi Lithium Corporation, Rio Tinto, SQM S.A., Pilbara Minerals Limited, and Umicore N.V.