- Bulk Chemicals

- Electroplating Market

Electroplating Market Size, Share, and Growth Forecast for 2025 - 2032

Electroplating Market by Metal Type (Gold, Silver, Platinum, Nickel, Zinc, Chromium, Copper, and Others), Application (Corrosion Resistance, Decorative Finishes, Electrical Conductivity, Wear Resistance, and Others), Industry (Automotive, Electronic & Electrical, Aerospace & Defense, and Others), Regional Analysis from 2025 to 2032

Electroplating Market Size and Share Analysis

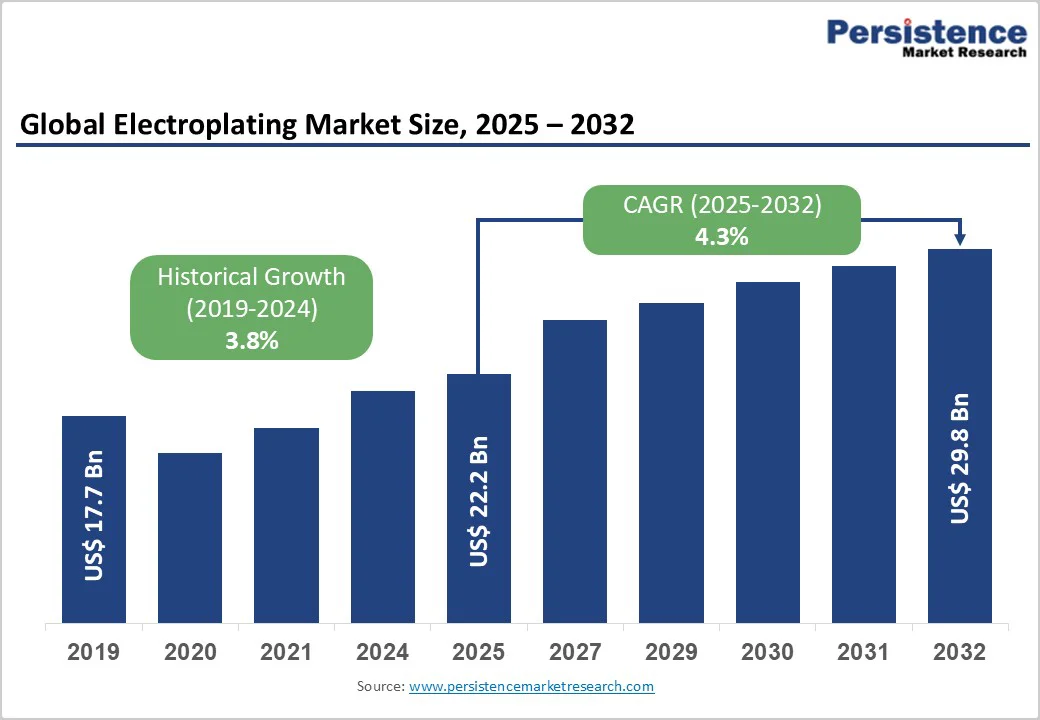

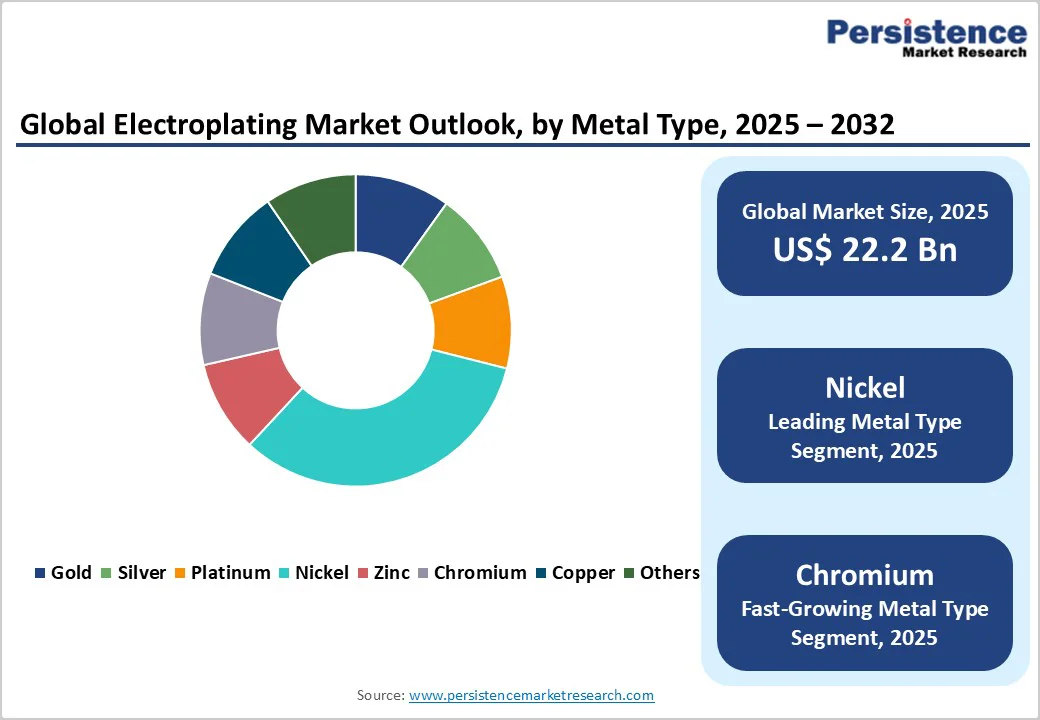

The global electroplating market size is likely to value at US$ 22.2 billion in 2025 and is projected to reach US$ 29.8 billion, growing at a CAGR of 4.3% between 2025 and 2032. The rise in demand from the automotive sector, particularly for electric vehicles (EVs), and the increasing demand from the aerospace and defense sectors for corrosion-resistant and wear-resistant component finishing, coupled with technological advancements in sustainable plating chemistries, are some of the prominent factors stimulating the global electroplating market growth.

Key Industry Highlights:

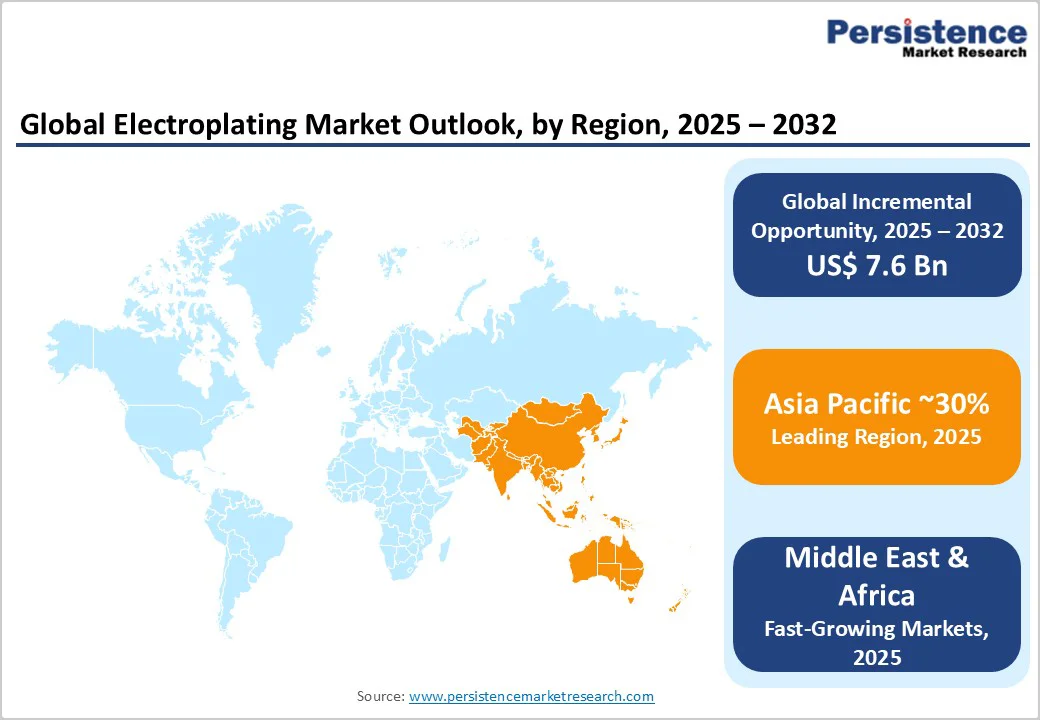

- Regional Leaders: Asia-Pacific to dominate the global market with a market share of nearly 30%, driven by China, Japan, India, and ASEAN manufacturing expansion, EV production growth at 60.2% CAGR, and emerging market industrialization supporting sustained electroplating demand.

- Leading Segments: Nickel plating dominates metal type segments at 32% market share, providing superior corrosion resistance and versatility across automotive, aerospace, electronics, and industrial applications requiring protective and functional coatings.

- Application: Electrical conductivity enhancement represents the fastest-growing application, growing at a 6.2% CAGR, driven by 5G infrastructure deployment, semiconductor interconnect requirements, and IoT device proliferation demanding precision metallization for performance reliability.

- Market Opportunity: Sustainable and eco-compliant electroplating chemistries including trivalent chromium and cyanide-free formulations, create premium market opportunities aligning with environmental regulations, corporate sustainability commitments.

| Key Insights | Details |

|---|---|

| Electroplating Market Size (2025E) | US$ 22.2 Bn |

| Projected Market Value (2032F) | US$ 29.8 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 4.3% |

| Historical Market Growth Rate (CAGR 2019 to 2024) | 3.8% |

Market Dynamics

Drivers - Electric Vehicle Production Expansion and Battery Component Electroplating

Electric vehicle adoption demonstrates unprecedented growth globally, with EV sales accounting for 21.2% of all new light-duty vehicle sales in the United States during the third quarter of 2024, reflecting sustained market acceleration. Battery systems integrated within electric vehicles necessitate specialized electroplating solutions for high-current bus bars, connectors, and thermal management components requiring superior conductivity and corrosion resistance.

The EV component plating segment projects growth at 8% CAGR through 2032, with zinc-nickel and tin-based plating systems gaining prominence for lithium-ion battery environment compatibility. Global electric vehicle market exhibits exceptional growth nearly 20% CAGR through 2032, creating substantial regional demand for advanced electroplating solutions supporting battery component fabrication and electrical system integration across expanding manufacturing infrastructure.

Technological Advancement in Sustainable and Eco-Compliant Electroplating Formulations

Environmental regulatory pressures including European Union REACH directives, EPA chromium emissions standards, and emerging Asia-Pacific environmental policies mandate adoption of sustainable plating chemistries reducing hexavalent chromium exposure and cyanide utilization. Trivalent chromium technology represents a critical innovation enabling chromium deposition with 95% reduced hexavalent chromium air emissions compared to traditional hexavalent chromium plating, ensuring regulatory compliance while maintaining corrosion resistance and decorative properties.

BASF, Atotech, and Clariant have invested substantially in developing cyanide-free gold plating and alkaline zinc formulations that achieve performance parity with conventional chemistries while eliminating hazardous compound utilization. The EU electroplating chemicals market projects growth from US$ 5.2 Billion in 2025 to US$ 7.6 Billion by 2035 at 3.9% CAGR, driven substantially by eco-compliant chemistry adoption across automotive, electronics, and aerospace manufacturing operations requiring sustainable finishing solutions aligned with corporate environmental objectives.

Restraint - Stringent Environmental Regulations and Hazardous Material Compliance Costs

Hexavalent chromium (HVC) compounds classified as known human carcinogens under Canadian Environmental Protection Act and EPA regulations require comprehensive emission control systems limiting point-source emissions to 0.03 mg/dscm, imposing substantial capital investment requirements for electroplating facilities. Hard chrome plating operations must implement advanced wastewater treatment systems, containment infrastructure, and air emission capture technologies, with compliance infrastructure costs potentially representing 15-25% of total facility operational expenses.

Smaller electroplating service providers face disproportionate compliance burden, as regulatory adherence requires sophisticated environmental management systems that established corporations can absorb through operational scale, effectively consolidating industry structure toward larger, better-capitalized entities capable of managing regulatory complexity and waste treatment infrastructure investments.

Opportunity - Aerospace and Defense Component Finishing Excellence Requirements

Aerospace and defense sectors demand electroplating excellence for critical component reliability under extreme operational conditions including -55°C to +150°C temperature ranges, corrosive salt-spray environments, and high-stress mechanical loading. Federal Aviation Administration (FAA) and Defense Logistics Agency specifications mandate electroplating processes producing microscopically uniform coatings without defects or thickness variations, creating premium service demand for technically sophisticated electroplating providers.

Nickel plating protects aerospace fasteners and landing gear components, while gold plating on electrical connectors ensures reliability across communication, navigation, and weapons systems. The aerospace and defense industry to provide opportunities for electroplating service providers offering aerospace-qualified processes, traceability documentation, and regulatory compliance expertise required for defense contractor qualification.

Industry 4.0 Integration and Automated Process Optimization Technologies

Smart manufacturing technologies including IoT-enabled monitoring systems, artificial intelligence process control, and real-time quality assurance platforms are transforming electroplating operational efficiency and product consistency. Advanced process monitoring reduces coating defects by up to 40% through predictive analytics identifying process drift before quality failures occur. Atotech, as part of MKS Instruments, developed vPlate® high-density interconnect plating systems paired with integrated software solutions enabling superior plating uniformity across complex circuit board geometries.

Digital twin technology and predictive maintenance platforms optimize equipment uptime and chemical utilization, reducing operational costs by 12-18% while improving sustainability metrics through material waste reduction. Companies implementing Industry 4.0 electroplating solutions gain competitive differentiation through enhanced quality consistency, reduced environmental impact, and accelerated product development cycles, positioning for premium market positioning and customer retention across electronics, automotive, and aerospace segments.

Category-wise Analysis

Metal Type Insights

Nickel plating dominates the global electroplating market, accounting for around 32% of total demand, owing to its unmatched versatility and durability. The metal’s excellent corrosion resistance, high hardness, and smooth surface finish make it indispensable across diverse industries such as automotive, aerospace, electronics, and industrial machinery.

In automotive applications, nickel plating enhances component lifespan by protecting parts like brake systems, engine valves, and decorative trims from rust and wear. In the aerospace sector, it is widely used on landing gear and turbine components for improved mechanical strength and reduced friction. Moreover, advancements in electroless nickel technology have enabled uniform coating on complex geometries, further broadening its industrial relevance and solidifying its dominance in the electroplating market.

Application Insights

Corrosion resistance applications account for about 38% of the global electroplating market, reflecting the strong industrial emphasis on extending component life and performance under harsh environmental conditions. Manufacturers in automotive, aerospace, marine, and heavy machinery sectors increasingly rely on electroplated coatings such as nickel, zinc, and chromium to protect metal parts from rust, oxidation, and chemical degradation. These coatings act as a barrier against moisture, salt, and corrosive agents, significantly reducing maintenance costs and downtime.

In the automotive sector, components like chassis parts, fasteners, and brake lines benefit from corrosion-resistant plating to ensure durability and safety. Aerospace applications involve plating aircraft landing gear, engine parts, and hydraulic systems to withstand extreme pressure and temperature variations. The growing demand for longer-lasting and more reliable equipment across industries continues to drive adoption, positioning corrosion protection as the primary functional advantage of electroplating technologies worldwide.

Industry Insights

The automotive sector represents the largest end-use industry in the global electroplating market, capturing around 35% of total demand. This dominance is primarily fueled by the rapid growth of electric vehicle (EV) production, where electroplated coatings play a crucial role in enhancing component reliability, conductivity, and appearance. Electroplating is widely used for both decorative and functional purposes, chrome and nickel finishes are applied to trims, grilles, and emblems for visual appeal, while zinc, copper, and nickel coatings protect engine parts, connectors, and fasteners from corrosion and wear.

The increasing integration of electronic systems in modern vehicles has further expanded the need for electroplated connectors and terminals to ensure efficient electrical performance. Lightweight and corrosion-resistant coatings contribute to longer vehicle lifespans and reduced maintenance costs. As automakers shift toward sustainability and improved performance, demand for advanced, environmentally friendly plating technologies continues to strengthen within the automotive industry.

Regional Insights

North America Electroplating Market Trends

North America holds a strong position in the global electroplating market, with the United States contributing approximately 82.4% of the regional demand. This dominance stems from the region’s mature and technologically advanced automotive, aerospace, and electronics manufacturing sectors, which require high-performance surface finishing solutions. In the U.S., electroplating is extensively utilized to enhance component durability, corrosion resistance, and aesthetic appeal in automobiles, aircraft, and precision electronic equipment.

The aerospace industry, in particular, relies heavily on nickel and chromium plating for landing gear, turbine blades, and hydraulic systems to ensure operational safety and longevity under extreme conditions. Meanwhile, the expanding electric vehicle and semiconductor manufacturing sectors are driving new opportunities for environmentally friendly and high-precision electroplating technologies. Additionally, stringent quality standards and ongoing investments in automation and sustainable plating processes continue to reinforce North America’s leadership and technological edge in the global electroplating market.

Europe Electroplating Market Trends

Europe exhibits steady growth in the electroplating market, propelled by the region’s rapid automotive electrification and stringent environmental regulations under the REACH framework, which emphasize the adoption of sustainable plating chemistries. The continent’s strong industrial base, led by Germany, plays a pivotal role in driving demand for high-quality electroplated components. Germany’s globally renowned automotive manufacturers, Volkswagen, BMW, Mercedes-Benz, and Audi, generate significant consumption of electroplated coatings for corrosion protection, conductivity, and aesthetic enhancement in vehicle components.

Beyond automotive, sectors such as aerospace, industrial machinery, and electronics also contribute to the regional demand for advanced surface finishing technologies. European electroplating companies are increasingly investing in trivalent chromium and cyanide-free processes to meet sustainability targets and comply with evolving environmental standards. Additionally, the growing shift toward electric and hybrid vehicles is fostering demand for plating applications in connectors, battery systems, and lightweight metal components, reinforcing Europe’s progressive and eco-conscious market growth trajectory.

Asia Pacific Electroplating Market Trends

Asia-Pacific to dominate the global market, capturing approximately 30.3% global electroplating market share in 2024, driven by expansive manufacturing bases across China, Japan, India, South Korea, and Southeast Asian economies. China dominates regional production and consumption, with electroplating applications spanning semiconductor fabrication, consumer electronics manufacturing, and automotive component finishing supporting the world's largest manufacturing output. India demonstrates exceptional growth at 7% CAGR through 2032, benefiting from expanding automotive manufacturing, EV adoption at 60.2% CAGR, and electronics sector development.

The region's manufacturing advantages including cost-effective solutions, rapidly advancing technology adoption, and expanding industrial capacity position Asia-Pacific as the critical growth engine, driven by continued industrialization, rising disposable incomes, and accelerating EV production expansion creating sustained electroplating demand across diverse industrial applications.

Competitive Landscape

The global electroplating market demonstrates moderately consolidated structure with approximately major multinational corporations controlling 50-60% of global market value, alongside numerous regional and specialized service providers serving niche applications and geographic markets. Top-tier competitors including Atotech (acquired by MKS Instruments), MacDermid Enthone Industrial Solutions, Clariant, and regional providers compete through integrated chemistry, equipment, and software solutions rather than commodity-based pricing.

Market consolidation reflects significant capital requirements for R&D infrastructure, regulatory compliance expertise, and specialized technical knowledge necessary for customer support across aerospace, automotive, and electronics sectors. Competitive strategies emphasize sustainable chemistry innovation, automation technology integration, and specialized industry expertise demonstrating technological differentiation and operational superiority versus price-based competition.

Recent Industry Developments

- In May 2025, Chemetall launched a new chromium-free electroplating additive system for copper and nickel plating applications, aimed at enhancing sustainability and compliance with REACH environmental standards.

- In June 2025, Coventya announced a strategic collaboration with Atotech Deutschland GmbH to co-develop next-generation electroplating additives focused on eco-friendly formulations and reduced hazardous waste.

- In March 2025, MacDermid Enthone Industrial Solutions expanded its electroplating chemical production facility in Singapore, strengthening supply capabilities for the growing automotive and electronics manufacturing markets across Southeast Asia.

Companies Covered in Electroplating Market

- Atotech Deutschland GMBH

- Interplex Holdings Pte. Ltd.

- Kuntz Inc.

- Pioneer Metal Finishing Inc.

- Roy Metal Finishing Inc.

- Bajaj Electroplaters

- J & N Metal Products LLC

- Peninsula Metal Finishing, Inc.

- Sharretts Plating Co. Inc.

- Allied Finishing

- MacDermid Enthone Industrial Solutions

- Clariant

- Cherng Yi Hsing Plastic Plating Factory Co., Ltd.

- Jing-Mei Industrial Limited

- Summit Corporation of America

- Klein Plating Works, Inc.

- Precision Plating Co.

Frequently Asked Questions

The global electroplating market was valued at US$ 22.2 billion in 2025 and is projected to reach US$ 29.8 billion by 2032, growing at 4.3% CAGR during the forecast period.

Key demand drivers include expanding electric vehicle production requiring specialized battery component plating, infrastructure deployment and semiconductor manufacturing supporting electrical conductivity applications, and regulatory mandates driving sustainable trivalent chromium and cyanide-free formulation adoption.

Nickel plating dominates the market with 32% share due to exceptional versatility across automotive fasteners, aerospace landing gear, electronic connectors, and industrial applications.

Asia-Pacific commands the largest regional share at 30.3% in 2024, driven by China, Japan, India, and ASEAN manufacturing dominance, expanding EV production at 60.2% CAGR, and industrial capacity investments supporting sustained electroplating demand.

Major opportunities include aerospace and defense component finishing excellence supporting 5.2% CAGR growth at US$ 3.2 billion annual market value through specialized high-reliability applications.

Key market players include Atotech Deutschland GMBH (Berlin, Germany), MacDermid Enthone Industrial Solutions (United Kingdom), Clariant (Switzerland), Interplex Holdings Pte. Ltd., Kuntz Inc., Pioneer Metal Finishing Inc., Bajaj Electroplaters, and Sharretts Plating Co. Inc.