- Plastics, Polymers & Resins

- Polylactic Acid Market

Polylactic Acid Market Size, Share, and Growth Forecast 2026 - 2033

Polylactic Acid Market by Raw Material (Corn starch, Sugarcane), End‑user (Packaging, Textile, Consumer goods, Bio‑medical, Agriculture, Electronics, Automotive & transport), and Regional Analysis, 2026 - 2033

Polylactic Acid Market Size and Trend Analysis

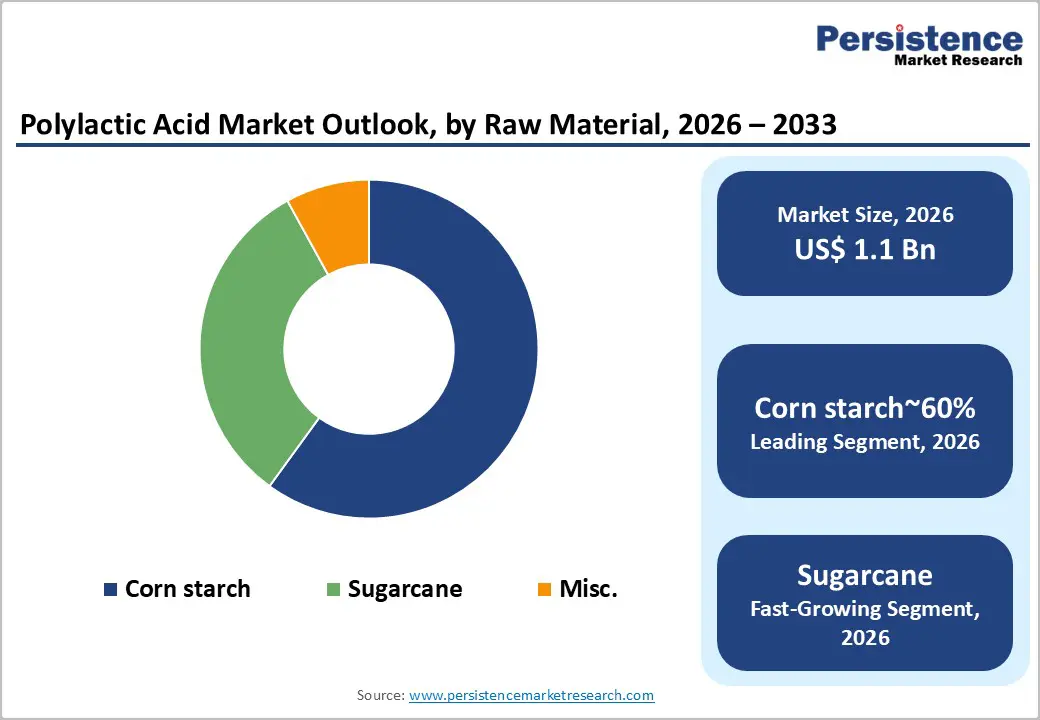

The global polylactic acid market size is likely to be valued at US$ 1.1 billion in 2026 and is expected to reach US$ 3.2 billion by 2033, growing at a CAGR of 16.7% during the forecast period from 2026 to 2033.

This robust expansion is driven by rising environmental awareness, tightening regulations on single-use plastics, and growing demand for bio-based, compostable polymers in packaging, textiles, and consumer goods applications.

Key Market Highlights

- Leading Region: Asia Pacific leads the polylactic acid market, accounting for 35% of the market share, driven by large populations, rising environmental regulations, and strong domestic PLA manufacturing in China, Japan, India, and ASEAN countries.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region with a CAGR of 18.9%, driven by plastic-ban policies, urbanization, and increasing demand for sustainable packaging and textiles.

- Dominant segment: Packaging is the dominant end-use segment, capturing 55% of PLA consumption due to its suitability for flexible films, rigid containers, and food-service applications.

- Fastest-growing segment: Textile is one of the fastest-growing segments, with a 17.8% CAGR, expanding faster than the overall market as PLA fibers gain traction in apparel, home textiles, and nonwovens.

- Key market opportunity: The expansion of PLA in bio-medical and 3D-printing applications, particularly in surgical sutures, drug-delivery systems, and personalized implants, represents a high-value growth opportunity.

| Key Insights | Details |

|---|---|

| Polylactic Acid Market Size (2026E) | US$ 1.1 Billion |

| Market Value Forecast (2033F) | US$ 3.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 16.7% |

| Historical Market Growth (2020 - 2025) | 14.2% |

Market Dynamics

Drivers - Government Plastic Bans and Circular Economy Policies are Rapidly Transforming Global Demand Toward Compostable PLA Alternatives

One of the most powerful growth drivers for the polylactic acid market is the rapid expansion of plastic-ban policies, single-use plastic restrictions, and circular-economy regulations across major global economies. Governments are actively pushing industries toward bio-based and compostable alternatives, such as PLA. The European Union has introduced the Single-Use Plastics Directive, which bans several disposable plastic items and promotes the use of sustainable materials.

At the same time, countries including India, China, and multiple ASEAN nations have rolled out phased bans on polyethylene bags and foam packaging. These regulatory actions are transforming packaging and consumer-goods supply chains by encouraging manufacturers to switch to PLA for films, containers, and disposable products. As enforcement becomes stricter and penalties increase, companies are rapidly adopting PLA-based materials to remain compliant, further boosting overall market demand.

Corporate Sustainability Commitments are Accelerating Widespread Adoption of Biodegradable PLA Across Global Packaging Industries

A strong global shift toward sustainable packaging and biodegradable materials, especially across food, beverage, and e-commerce industries, is a major driver. Packaging currently accounts for over 60% of global plastic use, and an increasing share of this demand is moving toward compostable solutions such as PLA. Many global consumer-packaged-goods brands and large retailers have committed to making all packaging recyclable, reusable, or compostable within the next decade.

These sustainability targets are accelerating the adoption of PLA across packaging formats such as films, trays, cups, and thermoformed containers. In addition, food-service businesses are increasingly using PLA in takeaway packaging, coffee capsules, and disposable cutlery to meet environmental goals. As consumers become more eco-conscious and governments push greener standards, sustainable packaging continues to play a central role in strengthening PLA demand worldwide.

Restraints - High Production Costs and Unstable Agricultural Feedstock Prices Continue to Limit Large-Scale PLA Market Penetration

One of the main challenges limiting the polylactic acid market is the higher production cost of PLA compared with traditional plastics such as polyethylene and polypropylene. PLA is produced using lactic acid derived from crops such as corn and sugarcane, making its cost highly sensitive to farming conditions and global commodity price movements. Weather disruptions, droughts, trade restrictions, and shifts in biofuel policies can all impact feedstock availability and pricing. When raw-material costs rise, PLA becomes less competitive against conventional plastics, especially in price-sensitive packaging and disposable product markets. This issue is particularly noticeable in developing economies where affordability is a major purchasing factor. As a result, many manufacturers hesitate to fully replace conventional plastics with PLA in low-margin applications. Until production efficiencies improve or feedstock supply becomes more stable, cost pressure will remain a significant barrier to faster market expansion.

Insufficient composting infrastructure weakens PLA’s real-world sustainability benefits and slows global adoption

Another key restraint affecting PLA adoption is the limited availability of industrial composting infrastructure across many regions. While PLA is biodegradable, most products require specific temperature and humidity conditions found only in industrial composting facilities to break down effectively. Unfortunately, such facilities remain underdeveloped in many parts of Latin America, Africa, and Asia.

In many cases, PLA waste ends up in landfills or mixed with traditional plastics, where it does not degrade efficiently and can disrupt recycling streams. This creates confusion among consumers and waste-management authorities about proper disposal. The gap between PLA’s environmental benefits and real-world waste systems reduces confidence among regulators and businesses. Without improved composting infrastructure and clearer waste-handling guidelines, the full sustainability potential of PLA cannot be achieved, which continues to slow adoption in several high-growth regions.

Opportunity - Sustainable Fashion Trends are Creating Strong Growth Opportunities for PLA Fibers in Textile and Apparel Markets

A major growth opportunity for the polylactic acid market includes the expanding use of PLA fibers in the textile and apparel industries. PLA offers several advantages, including renewable sourcing, a soft texture, and a lower carbon footprint compared with synthetic fibers such as polyester and nylon. These benefits strongly align with the rapidly growing sustainable fashion movement. PLA fibers are increasingly used in sportswear, apparel linings, nonwoven fabrics, and home textiles.

Many global fashion brands are actively testing PLA-based fabrics to meet circular-fashion goals and reduce environmental impact. Industry trends show the sustainable textile market growing at strong annual rates, driven by eco-conscious consumers in Europe and North America. As manufacturing technologies continue to improve durability, color retention, and comfort, PLA fibers are expected to gain wider acceptance. This segment is positioned to become one of the fastest-growing end-use markets for polylactic acid.

Biomedical Innovations and Expanding 3D Printing Applications Unlock Premium Demand for High-Performance PLA Materials

Another high-value growth area for the Polylactic Acid Market is its expanding role in biomedical and 3D-printing applications. PLA’s biocompatibility, controlled degradation, and ease of processing make it ideal for advanced medical uses. It is widely applied in surgical sutures, drug-delivery systems, tissue scaffolds, and orthopedic implants.

These products have gained regulatory acceptance from institutions such as the U.S. Food and Drug Administration and the European Medicines Agency, supporting wider clinical adoption. At the same time, PLA dominates the consumer and industrial 3D-printing market due to its low warping, minimal toxicity, and ease of use. As personalized healthcare, regenerative medicine, and desktop manufacturing continue to expand globally, demand for high-purity and specialty PLA grades is expected to rise, creating strong premium-margin growth opportunities.

Category-wise Analysis

Raw Material Insights

Corn starch remains the dominant raw material used in global polylactic acid production, accounting for approximately 60% of total PLA manufacturing capacity. This leadership is supported by a highly developed corn-to-lactic-acid supply chain, particularly in North America and China. Large-scale wet-milling infrastructure enables efficient fermentation, purification, and polymerization processes, keeping production relatively cost-effective compared to alternative feedstocks.

Corn-based PLA benefits from established logistics networks, technological maturity, and economies of scale, making it the preferred choice for many packaging and consumer-goods producers. However, growing concerns about food crop use, land-use impacts, and sustainability are encouraging manufacturers to explore alternative sources such as sugarcane and agricultural waste. Over time, diversification into non-food feedstocks may gradually reduce corn starch’s market share, although it is expected to remain the leading source in the near term.

End-user Insights

Packaging remains the largest and most influential end-use segment within the polylactic acid market, accounting for nearly 55% of total global consumption. PLA is widely used in flexible films, rigid containers, cups, trays, and clamshell packaging, particularly for food, beverages, retail products, and e-commerce shipments. Its high clarity, stiffness, and excellent printability make it a strong alternative to PET and polystyrene for short-shelf-life items. At the same time, its compostable nature supports zero-waste and sustainability initiatives adopted by major brands and retailers. Many consumer-goods companies now specify PLA for salad containers, bakery packaging, takeaway boxes, and disposable food-service products. As regulatory pressure on plastic waste continues to grow worldwide, packaging will remain the primary driver of PLA demand, driving large-scale volume expansion across developed and emerging markets.

Regional Insights

North America Polylactic Acid Market Trends

North America represents a mature and innovation-driven region for the polylactic acid market, with the United States leading in production capacity, technological development, and sustainability policies. Regulatory initiatives from the U.S. Environmental Protection Agency and various state-level plastic-reduction programs are encouraging companies to replace conventional plastics with compostable alternatives such as PLA.

Major consumer-goods brands based in the region have publicly committed to fully sustainable packaging over the next decade, driving large-scale adoption of PLA in food packaging, beverage containers, and online retail shipments. The region also benefits from strong research partnerships, innovation hubs, and advanced manufacturing infrastructure. Companies such as NatureWorks LLC operate large-scale PLA facilities and collaborate closely with converters and waste-management firms. Investments in composting systems are gradually improving end-of-life solutions, strengthening market confidence and long-term growth prospects.

Europe Polylactic Acid Market Trends

Europe is one of the most regulation-driven and sustainability-focused markets for polylactic acid, supported by strong environmental policies and high consumer awareness. Countries such as Germany, France, the United Kingdom, and Spain are leading adoption across packaging, food-service, and consumer-goods sectors. The European circular-economy framework strongly promotes bio-based materials, while extended producer responsibility programs encourage brands to use compostable packaging.

Several countries have also implemented plastic taxes and bans on specific single-use products, further accelerating PLA demand. Industry associations report rapid capacity expansion for bioplastics across the region, with PLA accounting for a significant share of new investments. European consumers increasingly prefer eco-friendly products, pushing retailers to adopt sustainable packaging solutions. With consistent regulatory support and growing environmental consciousness, Europe continues to offer stable and high-value growth opportunities for the polylactic acid market.

Asia Pacific Polylactic Acid Market Trends

Asia Pacific is the fastest-growing and largest regional market for polylactic acid, driven by strong government policies, rising sustainability awareness, and expanding manufacturing capacity. China leads demand through strict plastic pollution controls that promote compostable packaging across food service, retail, and agriculture. Japan supports PLA adoption through advanced biomaterials research and industrial applications. India and ASEAN countries are rapidly emerging as production and conversion hubs, benefiting from abundant agricultural feedstocks such as corn and sugarcane.

Government bans on single-use plastics are encouraging local companies to invest in PLA manufacturing technologies. Countries including Thailand, Vietnam, and Indonesia are also expanding export-focused PLA capacity to serve global brands seeking sustainable materials. The combination of regulatory pressure, low-cost feedstock supply, and growing domestic consumption positions the Asia Pacific as the most dynamic growth engine for the global polylactic acid market over the coming decade.

Competitive Landscape

The polylactic acid market features a moderately consolidated structure, with a small group of major global producers controlling most of the production capacity and technology. Leading companies such as NatureWorks LLC, TotalEnergies Corbion, COFCO, and Zhejiang Hisun Biomaterials Co., Ltd. dominate the industry through proprietary fermentation processes, polymer technologies, and large-scale facilities.

These players continue investing heavily in capacity expansions, new feedstock sources, and high-performance PLA grades. Many companies are forming long-term supply partnerships with brand owners and packaging converters to secure demand. Sustainability innovation, such as carbon-neutral PLA and closed-loop recycling initiatives, is becoming a key competitive advantage. Overall, success in this market increasingly depends on technological expertise, regulatory compliance, vertical integration, and strong sustainability positioning.

Key Developments:

- In February 2025: NatureWorks announced a 50% expansion of its Asian PLA manufacturing facility, adding advanced fermentation and polymerization lines to meet rising packaging and textile demand across China, India, and ASEAN, while strengthening regional supply security.

- In September 2024: TotalEnergies Corbion introduced a new PLA grade with improved heat resistance and barrier performance, designed for food and beverage containers, enabling brands to replace PET and polystyrene with compostable, high-durability packaging solutions.

- In March 2023, COFCO revealed plans to build a large-scale PLA facility using its corn-processing capabilities to supply domestic packaging markets, reduce imports, and align with China’s plastic-reduction policies while strengthening its bioplastics portfolio.

Companies Covered in Polylactic Acid Market

- Sulzer

- TotalEnergies Corbion bv

- NatureWorks LLC

- Futerro

- Omnexus

- COFCO

- Jiangxi Keyuan Biopharm Co., Ltd.

- Shanghai Tong‑jie‑liang Biomaterials Co., Ltd.

- Zhejiang Hisun Biomaterials Co., Ltd.

- UNITIKA LTD.

- BASF SE

- Danimer Scientific

- TORAY INDUSTRIES, INC.

- Evonik Industries

- Mitsubishi Chemical Group Corporation

- Corbion NV

- Purac Biochem (part of Corbion)

- Galactic SA

- Mitsubishi Chemical Corporation

- Bayer MaterialScience (Covestro AG)

Frequently Asked Questions

The global Polylactic Acid Market is valued at US$ 1.1 Billion in 2026 and is projected to reach US$ 3.2 Billion by 2033, growing at a CAGR of 16.7% from 2026 to 2033, with a historical CAGR of 14.2% between 2020 and 2025.

Key demand drivers include plastic‑ban policies, single‑use plastic restrictions, circular‑economy regulations, and rising demand for sustainable packaging and biodegradable materials in packaging, textile, and consumer‑goods applications.

The packaging segment is the leading end‑use category, capturing 55% of PLA consumption due to its suitability for flexible films, rigid containers, and food‑service packaging.

Asia Pacific is the largest regional market for polylactic acid, accounting for roughly 35% of global value, driven by plastic‑ban policies, urbanization, and strong domestic manufacturing in China, Japan, India, and ASEAN countries.

A key opportunity lies in the expansion of PLA in bio‑medical and 3D‑printing applications, including surgical sutures, drug‑delivery systems, and personalized implants, which offer high‑value, premium‑margin growth pockets.

Leading players include NatureWorks LLC, TotalEnergies Corbion bv, Futerro, COFCO, Zhejiang Hisun Biomaterials Co., Ltd., UNITIKA LTD., BASF SE, Danimer Scientific, TORAY INDUSTRIES, INC., Evonik Industries, and Mitsubishi Chemical Group Corporation, among others.