- Non-food Packaging

- Label Films Market

Label Films Market Size, Share, and Growth Forecast, 2026 - 2033

Label Films Market by Material Type (Polypropylene (PP), Others), Application (Food and Beverage, Pharmaceuticals, Others), End-user (Food and Beverage, Healthcare, Retail, Others), and Regional Analysis for 2026 - 2033

Label Films Market Size and Trends Analysis

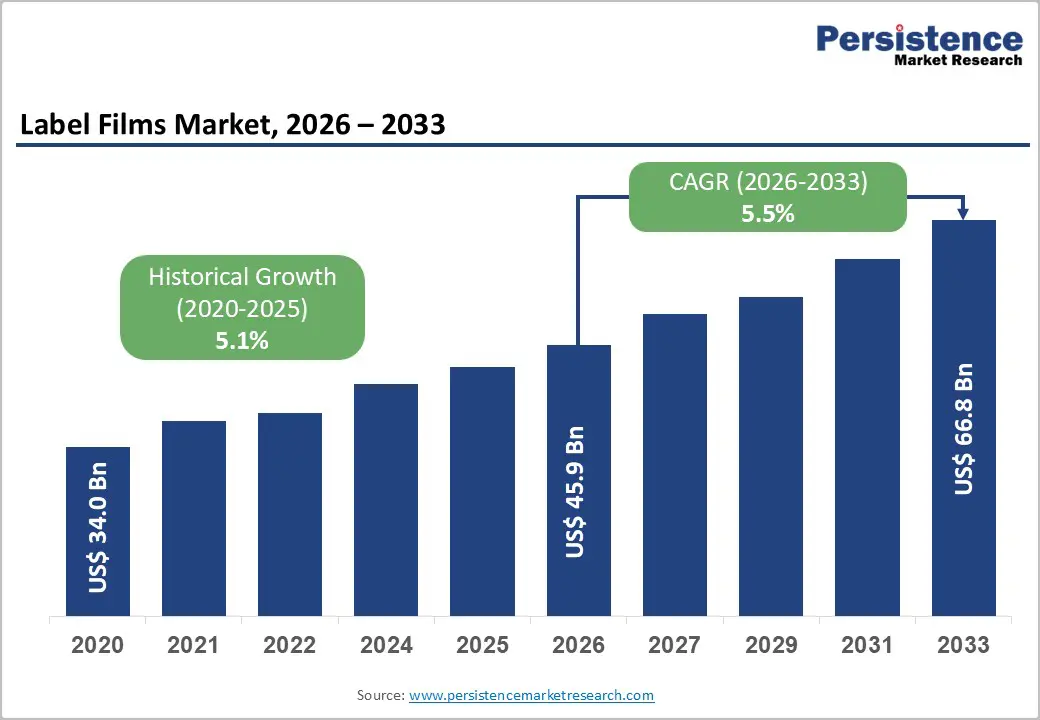

The global label films market size is likely to be valued at US$45.9 billion in 2026, projected to reach US$66.8 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of packaged goods, rising demand for high-quality branding, and advancements in flexible packaging technologies.

The need for durable and visually appealing labels, particularly in food and beverage, has significantly boosted the adoption of label films across various demographics. The market is further propelled by innovations in polypropylene and polyethylene films, catering to preferences for sustainable and printable options. The growing acceptance of label films as essential for product differentiation, particularly in retail, is a key growth factor.

Key Industry Highlights:

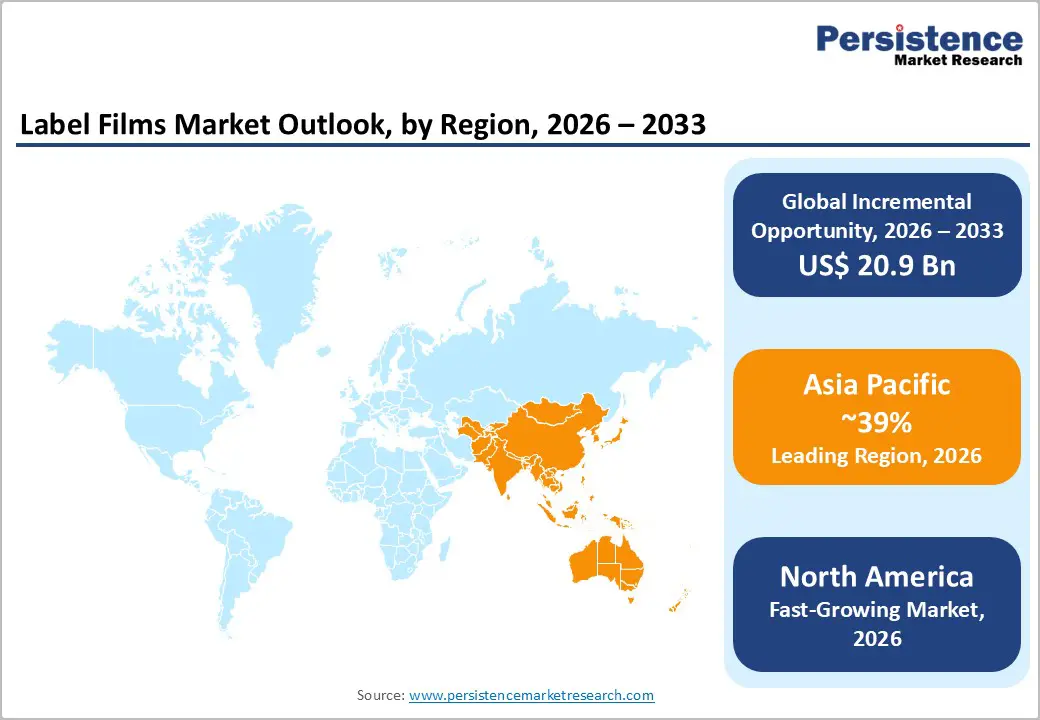

- Leading Region: Asia Pacific is expected to command a 39% market share in 2026, driven by massive packaging production, high prevalence of consumer goods, and strong R&D activities in China.

- Fastest-growing Region: North America is likely to be fueled by increasing e-commerce, rising awareness of branded packaging, and growing investments in sustainable films in the U.S.

- Dominant Material Type: Polypropylene (PP), to hold approximately 40% of the market share in 2026, due to its flexibility and printability.

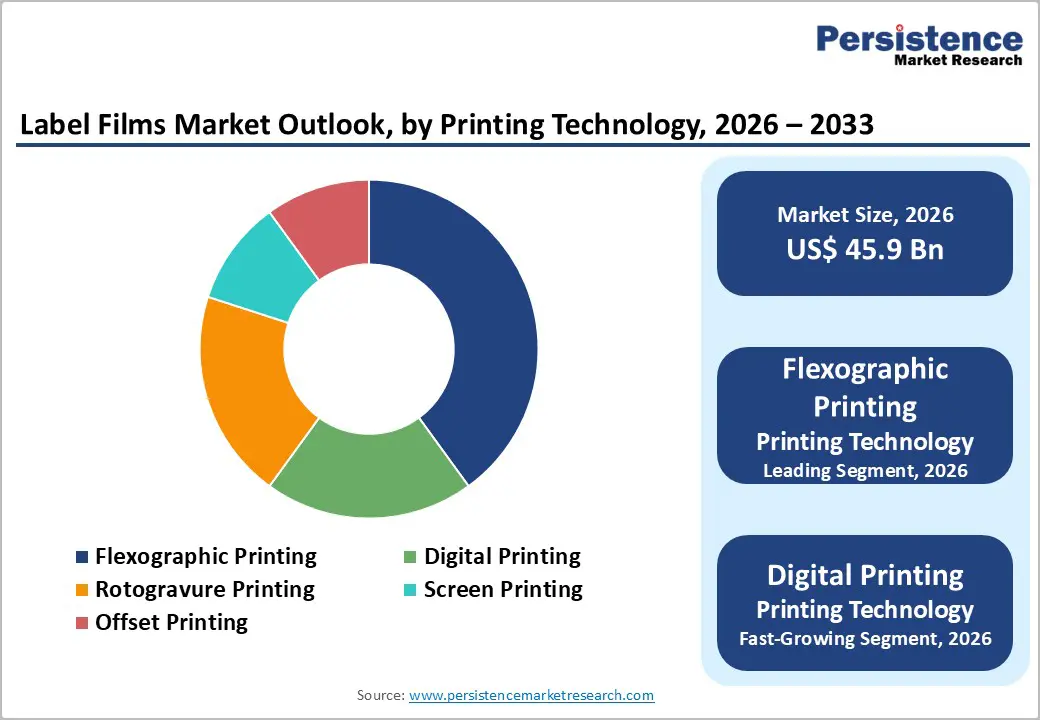

- Leading Printing Technology: Flexographic printing, to account for over 50% of market revenue, driven by high-speed production.

- Leading Application: The food and beverage segment is projected to account for almost 35% of the market revenue, driven by its strong reliance on labeling for safety, compliance, and transparent ingredient communication.

- Leading End-user: The retail sector is expected to capture 30% of the revenue share, driven by the need for eye-catching, durable labels that boost visibility and brand appeal, due to high product turnover and fierce shelf competition.

| Key Insights | Details |

|---|---|

| Label Films Market Size (2026E) | US$45.9 Bn |

| Market Value Forecast (2033F) | US$66.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Packaged Goods and Demand for High-Quality Branding

The increasing prevalence of packaged goods globally is a primary driver of the label films market. Over 80% of consumer products are labeled, with higher growth in emerging markets. This widespread packaging creates a substantial demand for versatile films. Label films offer superior adhesion and clarity, typically enhancing brand visibility by 25%, making them ideal for shelf competition. As consumption of packaged foods, beverages, personal care items, and household products continues to increase globally, brands are investing more in visually appealing and durable label films to differentiate their products on crowded retail shelves. Consumers associate premium packaging with product quality, safety, and trust, pushing companies to adopt high-clarity, high-gloss, and richly printed label films that enhance shelf impact.

The shift toward organized retail and e-commerce further accelerates this trend, as products must stand out both physically and digitally. High-performance label films offer superior printability, resistance to moisture and abrasion, and long-lasting aesthetic qualities essential for maintaining brand identity across supply chains and varied storage conditions.

High Development and Sustainability Compliance Costs

High development and sustainability compliance costs remain a significant restraint in the label films market, limiting the speed at which companies can adopt eco-friendly materials. Transitioning from traditional multilayer labels to recyclable or bio-based films requires heavy upfront investments in R&D, reformulation, and testing. Many sustainable substrates, such as advanced recyclable PET or bio-polymers are still priced higher than conventional alternatives, raising the overall production costs. The meeting of sustainability standards involves extensive certification, documentation, life-cycle assessments, and compliance with evolving global packaging regulations, all of which increase operational burden.

A pharmaceutical company that attempted to shift from multi-layer laminates to recyclable mono-material PET label films. The move required costly equipment upgrades because existing packaging lines were incompatible with the new materials. Material costs also surged, as some sustainable, high-barrier polymers were nearly four to five times more expensive than standard plastics. The company further faced intense regulatory scrutiny, needing to generate detailed technical documentation, COAs, recyclability proofs, and carbon-footprint data for every packaging component. These rising costs created delays and forced the company to adopt a phased transition instead of a full-scale switch.

Advancements in Sustainable and Smart Label Films

Advancements in sustainable and smart label films are reshaping the packaging industry as brands intensify their focus on eco-friendly materials, traceability, and consumer engagement. Sustainable label films such as recyclable mono-material BOPP, PET, and emerging bio-based options are gaining strong momentum as companies work to reduce environmental impact and comply with tightening global regulations. Smart label films integrating RFID, NFC, and printed sensors are enabling real-time monitoring, improved authentication, and enhanced supply-chain transparency, making them increasingly attractive across FMCG, pharma, and logistics sectors.

A leading global FMCG brand that shifted from traditional multilayer labels to recyclable mono-material BOPP films, reducing plastic usage by 22% and improving recyclability. The brand further adopted NFC-enabled smart labels in its premium product line, enabling consumers to verify authenticity and access detailed product information through simple smartphone scans. This move delivered an 18% reduction in logistics errors and a 12% rise in consumer engagement through interactive packaging features.

Category-wise Analysis

Material Type Insights

The polypropylene (PP) segment is expected to dominate the market, accounting for 40% of the share in 2026, driven by flexibility, moisture barrier, and printability, making it preferred for food. PP films, such as those from Treofan Group, provide a gloss finish, ensuring appeal. Its cost and versatility make it preferred for manufacturers. Treofan Group is a leading global manufacturer of biaxially oriented polypropylene (BOPP) films, supplying high-performance polypropylene films to food and packaging markets worldwide.

Polyethylene (PE) is likely to be the fastest-growing segment, driven by recyclability and increasing adoption in pharmaceuticals. PE offers transparency, appealing for tamper-evident. Focus on bio-PE innovation accelerates adoption in Asia Pacific and Europe. Braskem’s I’m green™ bio-PE is a polyethylene resin derived from sugarcane ethanol that retains identical mechanical and processing properties to conventional fossil-based PE, including transparency and recyclability, making it suitable for packaging applications across industries.

Printing Technology Insights

The flexographic printing segment leads the market, holding 50% of the share in 2026, driven by its high-speed production and suitability for large-volume printing. Its efficiency, low cost, and compatibility with various substrates make it the preferred choice for mass packaging and labeling. As demand for quick, reliable, and scalable printing grows, flexographic printing continues to maintain strong market dominance. UFlex integrates flexographic printing technology into its workflow because it delivers high-speed, cost-effective printing on films and flexible substrates used for mass packaging, enabling the company to fulfill large packaging orders efficiently for export customers while maintaining brand graphics and quality standards.

Digital printing is likely to be the fastest-growing segment, fueled by rising demand for short runs, customization, and personalized packaging. Its ability to handle variable data, fast turnaround, and high-quality graphics makes it ideal for promotional and niche products. Brands increasingly adopt digital printing to enhance flexibility, reduce waste, and support frequent design changes in competitive markets. HP Indigo Division (a business unit of HP Inc.) is a major provider of digital printing technology widely used in the packaging industry to meet rising demand for short runs, customized designs, and personalized packaging. HP Indigo digital presses allow converters and brand owners to print without plates, enabling fast, cost-effective production of variable designs, labels, and packaging with high-resolution graphics ideal for limited editions, promotional runs, and niche products.

Application Insights

The food and beverage segment is expected to lead the market, contributing 35% of the revenue share by 2026. This growth is driven by the widespread use of label films in packaged foods, beverages, and ready-to-eat products. The strict labeling regulations, safety standards, and demand for clear product information further solidify the segment's dominance. To address these requirements, the industry depends on reliable, regulation-compliant label films that preserve product freshness, enable traceability, and withstand high-volume packaging operations. Avery Dennison Corporation is a leading supplier in this space, providing label films and pressure-sensitive labels tailored for the food and beverage sector. Its food-grade materials are designed to meet safety standards, enhance freshness and traceability, and deliver dependable performance in high-speed manufacturing settings.

The personal care and cosmetics segment is expected to register the fastest growth, driven by evolving beauty trends, increasing premiumization, and a heightened emphasis on branding. Brands are increasingly choosing high-quality, visually appealing label films to elevate product appearance and shelf impact. Demand is growing for durable, smudge-resistant, and highly customizable labels as companies focus on luxury packaging and frequent new product introductions. In response, Avery Dennison introduced a premium portfolio of labels with textured and specialty substrates, enabling luxury brands to develop distinctive packaging that appeals to beauty-conscious consumers and supports premium brand positioning.

End-user Insights

The retail segment is projected to lead the market, accounting for 30% of the revenue share in 2026. This growth is driven by fierce competition on store shelves and the increasing need for high product visibility. Labeling plays a crucial role across various consumer goods, from food to personal care, fueling the demand for premium, attention-grabbing labels. As branding becomes more important and product launches continue to rise, the retail segment's dominance is further solidified. Avery’s Flex+ filmic label materials are designed to provide high clarity, vibrant graphics, and consistent performance on shelves. These labels help products stand out in crowded retail spaces while also meeting sustainability and production requirements.

The healthcare segment is likely to be the fastest-growing, driven by stringent pharmaceutical regulations and the rising use of medical devices. The demand for dependable labeling solutions has surged, particularly for high-barrier label films that ensure sterility, durability, and regulatory compliance. These labels are essential for medical packaging, offering resistance to chemicals, sterilization processes, and hospital conditions. 3M Company, a global leader in adhesive and labeling technology, offers its 3M™ Health Care Label Material 7000 Series, a medical-grade material specifically designed for healthcare and pharmaceutical applications. These labels are engineered to withstand autoclaving, ethylene oxide (EtO), and gamma sterilization processes while maintaining strong adhesion on a wide range of surfaces used in medical and pharmaceutical packaging, such as vials, bottles, bags, and devices.

Regional Insights

North America Label Films Market Trends

North America is projected to hold a 26.3% market share by 2026, driven by strong demand across the food and beverage, pharmaceutical, personal care, and logistics sectors. The region benefits from a well-established packaging ecosystem, known for its high-quality standards, advanced converting technologies, and a preference for premium labeling solutions. One of the key market trends is the growing shift toward sustainable and recyclable film materials, spurred by consumer expectations and state-level regulatory pressures on packaging. This trend is accelerating the adoption of mono-material BOPP and PET label films, which are designed to improve recyclability and minimize environmental impact.

Another significant trend is the rise of digital printing technology, allowing brands to create high-resolution graphics, streamline production timelines, and offer personalized packaging for marketing campaigns. The booming e-commerce sector is driving demand for durable, high-adhesion labels capable of withstanding complex supply chains, while supporting variable data printing for tracking and compliance. North American brands are also increasingly investing in smart labeling technologies, such as RFID and QR-enabled films, to improve product authentication, inventory management, and traceability.

Europe Label Films Market Trends

Growth in Europe is driven by stringent sustainability regulations, growing FMCG demand, and continued innovation in packaging technologies. The region remains highly mature, with strong adoption of premium labeling materials across food, beverage, pharmaceuticals, and personal care industries. European brands are increasingly prioritizing recyclable and eco-friendly packaging, which is accelerating the shift toward mono-material films such as BOPP and PET that support closed-loop recycling systems.

Regulations such as the EU Packaging and Packaging Waste Directive are pushing manufacturers to redesign label films with reduced environmental impact, including downgauged thickness, bio-based alternatives, and improved recyclability. Technological advancements in digital and hybrid printing are another major trend, enabling faster turnaround, high-resolution graphics, and customization for short production runs. This is particularly relevant as Europe sees rising demand for premiumization, personalization, and clean-label packaging.

Asia Pacific Label Films Market Trends

Asia Pacific is expected to dominate the market, holding a 39% share by 2026, fueled by the region’s growing consumer goods production, rapid urbanization, and rising demand for packaged products in emerging economies. Countries, including China, India, Indonesia, and Vietnam, are experiencing significant investments in sectors such as food and beverage, pharmaceuticals, and cosmetics, driving the need for high-quality labeling solutions. The rapid adoption of flexible packaging is also on the rise, prompting a shift toward lightweight, durable, and cost-effective film materials such as BOPP, PET, and polyethylene.

Sustainability is emerging as a key trend in the region, with manufacturers placing a greater emphasis on recyclable, mono-material label films to meet evolving environmental regulations and align with brand sustainability goals. Local companies are increasing their competitiveness by implementing energy-efficient manufacturing processes and offering customizable label solutions that cater to regional preferences.

Technological innovations in digital printing are also influencing the market, enabling faster production cycles and enhanced print quality for short-run and personalized labels. The expansion of e-commerce is driving demand for durable, high-adhesion labels that are optimized for shipping and logistics needs.

Competitive Landscape

The global label films market is highly competitive, driven by a strong mix of established packaging giants and specialized film manufacturers. In mature markets such as North America and Europe, companies such as Cosmo Films and Avery Dennison Corp maintain leadership positions through robust R&D capabilities, extensive distribution networks, and strong collaborations with major FMCG brands. Their focus on high-performance, durable, and regulatory-compliant films continues to reinforce their market dominance.

The Asia Pacific region is witnessing rapid expansion with players such as Jindal Poly Films gaining traction by offering cost-effective, localized solutions and capitalizing on the region’s booming consumer goods and e-commerce industries. The shift toward sustainability is a major competitive differentiator, with companies prioritizing recyclable, bio-based, and downgauged film innovations to meet tightening global environmental standards. Industry dynamics are further shaped by strategic partnerships, mergers, and acquisitions aimed at expanding product portfolios and geographic reach. Advancements in digital printing technologies and smart labeling solutions are enhancing customization and enabling brands to strengthen consumer engagement.

Key Industry Developments

- In September 2025, Cosmo Films launched CSP Dualcoat, a new dual-coated synthetic paper product that delivers superior performance across offset, flexographic, thermal transfer, HP Indigo, screen, and letterpress printing applications while providing enhanced durability and tear resistance for demanding branding and commercial display requirements.

- In January 2025, Avery Dennison launched a premium labels range comprising textured and specialty substrates that help luxury brands create distinctive packaging that resonates with beauty-focused consumers and supports brand premiumization.

Companies Covered in Label Films Market

- Cosmo Films

- Treofan Group

- Innovia Films

- Mondi Group

- Klöckner Pentaplast

- Irplast

- TAGHLEEF INDUSTRIES GROUP

- Bischof + Klein France

- DUNMORE Corp

- Manucor

- Renolit

- Invico

- SELENE

- POLIFILM Group

- Accrued Plastic

- Polinas Plastik Sanayi ve Ticaret

- Jindal Poly Films

- HERMA

- Avery Dennison Corp.

Frequently Asked Questions

The global label films market is projected to reach US$45.9 billion in 2026.

The rising prevalence of packaged goods and demand for high-quality branding are the key drivers.

The label films market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Advancements in sustainable and smart label films present a significant market opportunity.

Cosmo Films, Treofan Group, Innovia Films, Mondi Group, and Avery Dennison Corp are the key players.