- Metalworking & Fabrication

- Flexographic Printing Technology Market

Flexographic Printing Technology Market Size, Share, and Growth Forecast, 2025 - 2032

Flexographic Printing Technology Market by Technology (Inline Press, Stack Press, Central Impression Press), Ink (Water-Based, Solvent-Based Inks, UV-Cured Inks, Others), End-Use Industry (Food & Beverage, Healthcare & Pharmaceutical, Personal Care & Cosmetics, Consumer Goods, Industrial, Retail & E-Commerce, Others), and Regional Analysis for 2025 - 2032

Flexographic Printing Technology Market Share and Trends Analysis

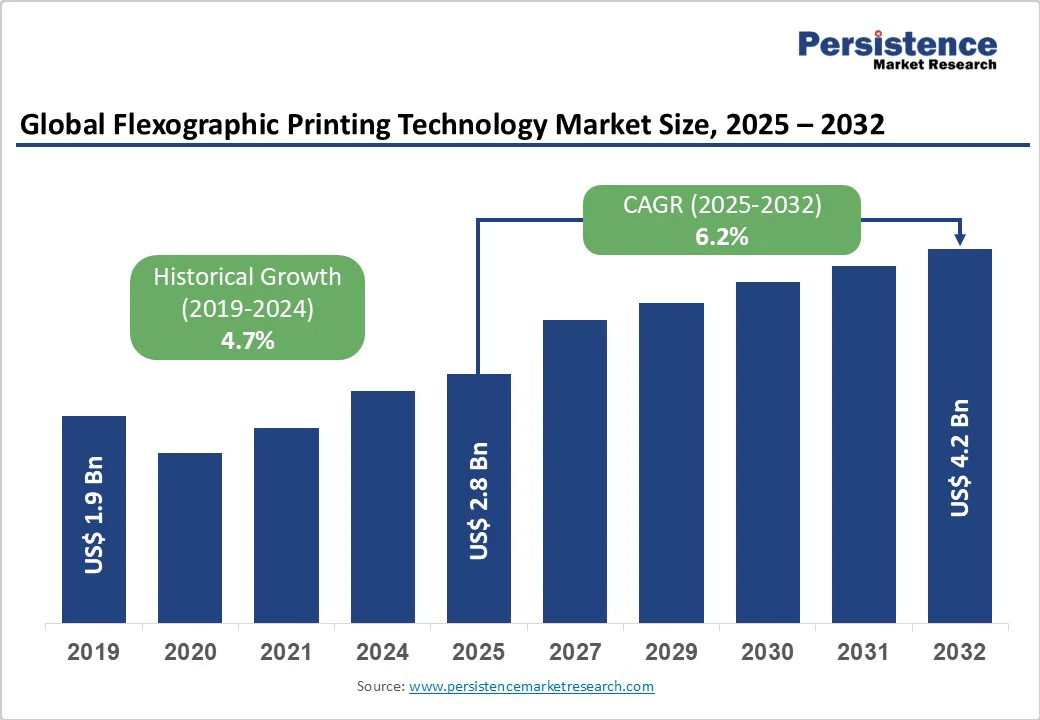

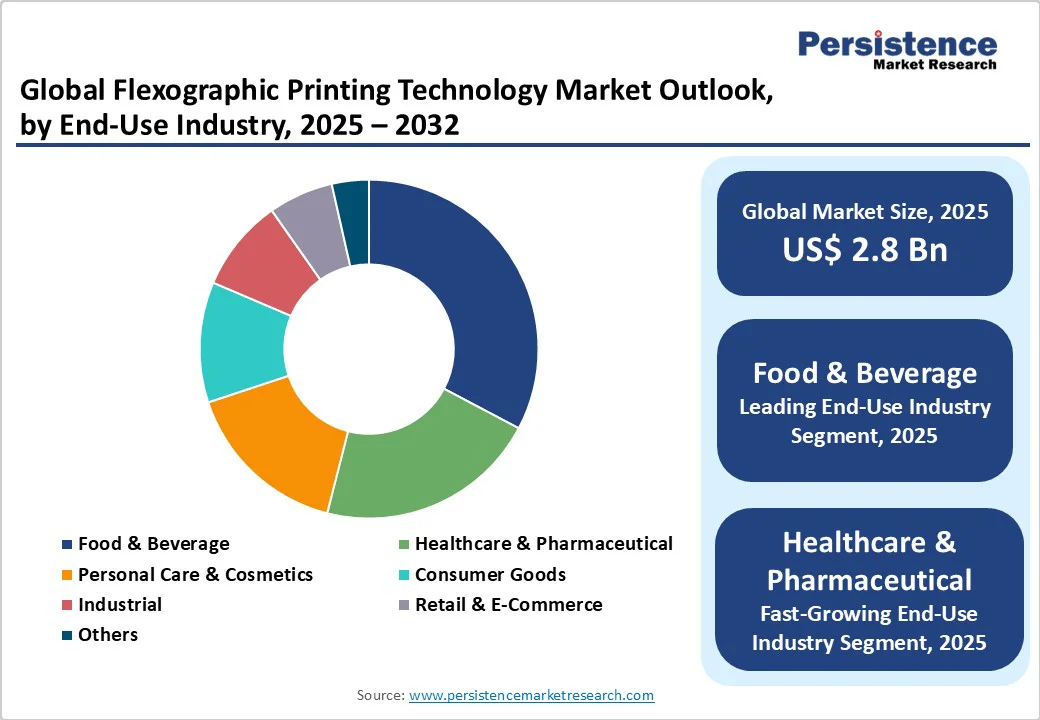

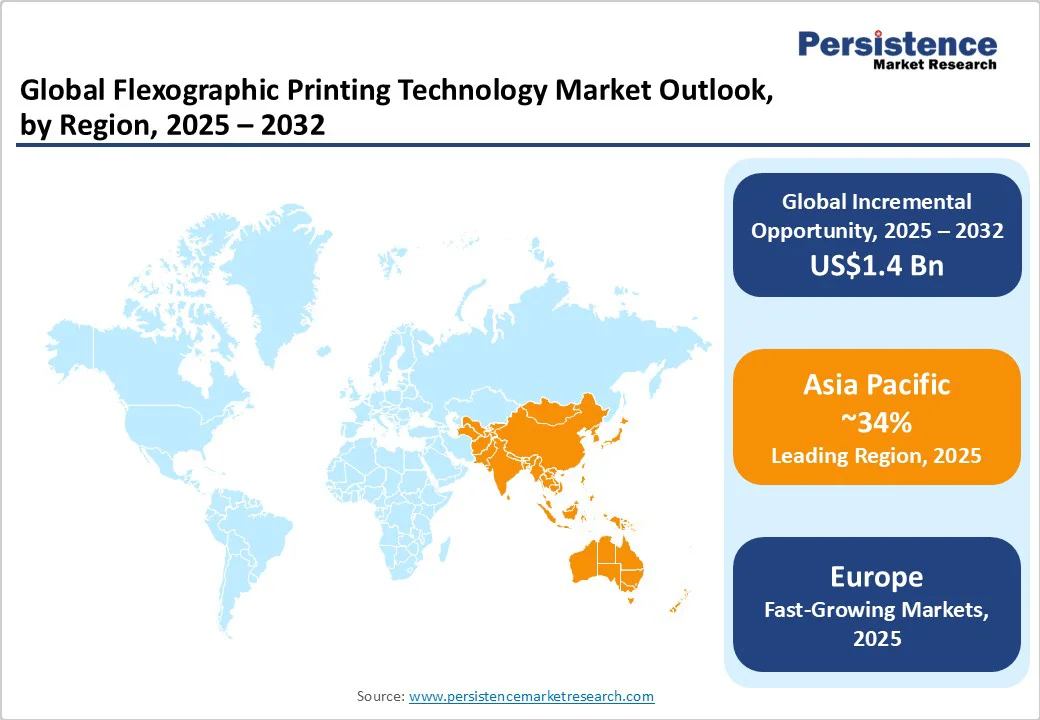

The global flexographic printing technology market size is likely to be valued at US$ 2.8 billion in 2025, and is projected to reach US$ 4.2 billion by 2032, growing at a CAGR of 6.2% during the forecast period 2025 - 2032.

The rising demand for high-quality, cost-effective, and efficient printing solutions across the packaging and labeling industries is driving growth. Increasing consumer preference for attractive, durable, and customized packaging, especially in the food & beverage, healthcare, and personal care sectors, is further fueling adoption.

Rapid industrialization, expanding e-commerce, and higher disposable incomes are also boosting the demand for visually appealing and protective packaging.

Key Industry Highlights

- Leading Technology: Inline presses are set to dominate with over 41% of the flexographic printing technology market revenue share in 2025 due to their ability to integrate multiple printing and converting processes.

- Leading Ink: Water-based inks are slated to account for over 38% share in 2025 owing to their eco-friendly properties, low volatile organic compound (VOC) emissions, and excellent print quality on paper and corrugated substrates.

- Leading End-Use Industry: Food & beverage is predicted to dominate with over 37% share in 2025, boosted by a massive demand for attractive, safe, and customizable packaging, along with compliance with food contact regulations.

- Dominant Region: Asia Pacific is projected to capture over 34% share in 2025, driven by rapid industrialization, rising urbanization, competitive labor costs, and government incentives.

- Other Regional Markets: The markets in North America and Europe are to grow steadily through 2032, supported by advanced technology adoption, stringent environmental regulations, and strong packaging sectors, with Europe focusing on sustainable and visually appealing solutions.

| Key Insights | Details |

|---|---|

| Flexographic Printing Technology Market Size (2025E) | US$ 2.8 Bn |

| Market Value Forecast (2032F) | US$ 4.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Shift toward Eco-Friendly Packaging Solutions

The global demand for environmentally responsible packaging serves as a primary catalyst for the flexographic printing technology market expansion. Regulatory frameworks, including the Single-Use Plastics Directive of the European Union (EU) and the U.S. Clean Air Act, are accelerating the adoption of water-based and UV-curable inks, which can reduce VOC emissions by up to 90% compared to solvent-based systems.

Transitioning to these eco-friendly inks also enables manufacturers to cut environmental compliance costs by up to 30%, while ensuring compatibility with biodegradable and recyclable substrates. Major packaging companies are investing billions annually in sustainable printing infrastructure, reinforcing flexography’s role in supporting corporate sustainability mandates.

Advancements in press technologies, including high-speed central impression (CI) presses and inline heliographic screening, have enhanced registration accuracy and color consistency. Automation features such as automated plate mounting, robotic changeovers, and real-time defect detection help reduce setup times often by up to 20-30% while improving overall equipment effectiveness (OEE).

These innovations support short-run, personalized packaging and enable agile manufacturing models. Integration of Industry 4.0 technologies, including IoT sensors and predictive maintenance platforms, minimizes downtime and optimizes energy consumption, further driving productivity and operational efficiency.

Raw Material Price Volatility

Flexographic printing operations are highly sensitive to fluctuations in raw material prices, including acrylic monomers for UV-curable inks, solvent-based resins, photopolymer plates, anilox rolls, and specialty pigments. Smaller converters with limited purchasing volumes face higher per-unit costs, constraining investment in premium ink systems.

Supply chain disruptions for specialized pigments and UV-curing components from limited suppliers further exacerbate cost pressures, contributing 8-12% of total production cost variability and complicating long-term pricing strategies and contract negotiations.

Flexographic printing operations require skilled and experienced operators for plate-making, ink management, and press handling, making workforce availability a critical challenge. Traditional flexo systems involve longer setup times for plate mounting and ink adjustments, reducing cost-effectiveness for short-run or frequently changing jobs.

Limited flexibility for rapid design changes and higher initial capital investments further constrain adoption, particularly for small and medium-sized enterprises. Environmental concerns related to solvent-based inks also pose regulatory and compliance challenges.

Digital-Hybrid Technology Integration to Create New Avenues

The emergence of digital-hybrid presses presents significant opportunities for manufacturers to serve both short and long production runs more efficiently. These presses integrate advanced automation features, such as automated plate mounting, real-time monitoring, and in-line color control, which enhance production efficiency while reducing operational costs and waste.

Hybrid systems allow converters to handle variable data jobs alongside conventional spot color applications, reducing production complexity and improving cost-effectiveness. Investments by manufacturers in hybrid printing technology have been targeted toward improving operational flexibility.

Moreover, growing consumer demand for personalized packaging and limited-edition product runs presents significant opportunities. Brands are increasingly leveraging variable data printing (VDP) to deliver unique packaging elements, promotional codes, and personalized messaging that enhance consumer engagement.

Modern workflow management systems streamline production, reducing setup times to 15-20 minutes compared to several hours with traditional methods, enabling efficient short-run production. The integration of QR codes, digital watermarks, and RFID-compatible substrates supports smart packaging applications, facilitating product tracking, authentication, and interactive consumer experiences.

Category-wise Analysis

Technology Insights

Inline press is expected to account for more than 41% share in 2025 due to enabling seamless integration of multiple printing and converting processes on a single press, reducing production time, and minimizing handling errors.

They are ideal for high-volume packaging applications, where speed, consistency, and efficiency are critical. The growing demand for complex, multi-color packaging and labels further drives the preference for inline systems, as they allow precise registration and quick changeovers to meet diverse consumer and regulatory requirements.

Central impression (CI) presses are predicted to grow at the highest rate due to their ability to deliver high-speed, high-quality printing. Brands increasingly demand precise registration, consistent color, and efficient use of inks, which CI presses provide.

The growing need for short-run, customized, and sustainable packaging solutions further drives its usage, as CI presses minimize setup waste and reduce production downtime. Their compatibility with advanced anilox rollers and inline finishing options meets the rising requirements for multi-color and complex designs.

Ink Insights

Water-based ink is anticipated to account for around 38% of the flexographic printing technology market share in 2025 due to its alignment with stringent environmental regulations and the growing demand for sustainable packaging. These inks are known to reduce VOC emissions, making them safer for workers and eco-friendly for end consumers.

Water-based inks offer excellent print quality on a wide range of substrates, including paper and corrugated packaging, meeting the packaging industry’s need for high-quality, safe, and recyclable solutions. Their cost-effectiveness and ease of use further drive widespread adoption.

UV-cured inks, on the other hand, are expected to exhibit the highest CAGR from 2025 to 2032, on the back of their fast-drying properties, which significantly reduce production time and increase efficiency.

They meet the growing demand for high-quality, vibrant, and durable prints on diverse substrates, including plastics, films, and labels. The technology eliminates solvent requirements, reduces volatile organic compounds, and provides enhanced durability for packaging applications requiring long-lasting performance.

Industry Insights

Food & beverage is expected to account for over 37% of the flexographic printing technology market revenues in 2025, on account of its high demand in the development of attractive, durable, and customized packaging that ensures product safety and shelf appeal. Growing consumer preference for convenience foods, ready-to-eat products, and eco-friendly packaging further drives adoption.

Food contact regulations necessitate specialized ink formulations and printing processes that flexographic systems efficiently provide. Food & beverage companies are increasingly using variable printing for promotional campaigns, QR codes, and branding, reinforcing flexography’s dominance in the sector.

The healthcare & pharmaceutical industry is expected to showcase a notable a CAGR during 2025 - 2032 due to the rising demand for secure, tamper-evident, and high-quality packaging for medicines, medical devices, and diagnostics.

Regulatory requirements for serialization, traceability, and anti-counterfeiting measures are driving the adoption of advanced flexo printing solutions. The need for clear labeling, variable data printing, and compliance with global standards creates strong opportunities for customized and efficient flexographic printing in this sector.

Regional Insights

North America Flexographic Printing Technology Market Trends

In North America, the flexographic printing technology market growth is anticipated to be driven by the widespread adoption of advanced technology, stringent regulatory frameworks, and a robust packaging industry. The U.S. alone is estimated to account for over 76% of the regional market value in 2025.

Strong food processing and consumer goods sectors, along with the EPA Clean Air Act and FDA food contact compliance, have accelerated the adoption of water-based and certified ink systems. The region’s well-established R&D infrastructure enables continuous innovation and rapid market introduction of new solutions, supported by major manufacturers such as Mark Andy, Bobst, and Koenig & Bauer investing millions annually in technology development.

Asia Pacific Flexographic Printing Technology Market Trends

Asia Pacific is projected to command over 34% of the flexographic printing market share by 2025, powered by rapid industrialization, rising urbanization, and expanding consumer markets in China, India, and Southeast Asia. Competitive labor costs up to 50-60% lower than developed markets, combined with government incentives and infrastructure support, attract significant investment in flexo printing facilities.

Rising e-commerce penetration and disposable incomes have been boosting the demand for packaging over the past decade, while the expertise of Japan in engineering advanced materials has enabled high-performance ink innovation. In the case of India, liberalized foreign direct investment (FDI) policies have further encouraged the establishment greenfield flexo press plants, collectively fueling regional market growth.

Europe Flexographic Printing Technology Market Trends

In Europe, the demand for flexographic printing solutions is primarily driven by its strong packaging and labeling industry, where high-quality, cost-effective, and fast printing solutions are essential. Increasing consumer preference for visually appealing and customized packaging in food, beverage, and personal care products fuels the adoption.

Compliance with the EU’s Single-Use Plastics Directive and REACH regulations has accelerated the adoption of sustainable printing technologies across member states. Harmonized environmental standards enable equipment manufacturers to develop standardized solutions that efficiently serve the entire regional market. VOC emission limits in Europe are 40% more stringent than in other regions, stoking the demand for premium ink systems.

Competitive Landscape

The global flexographic printing technology market structure is highly fragmented, with numerous global and regional players competing across offerings. Manufacturers focus on differentiation through advanced automation, high-speed presses, and integrated workflow solutions to reduce setup times and enhance print quality.

Strategic collaborations with ink suppliers and packaging brands help expand product portfolios and cater to niche segments like sustainable and personalized packaging.

Key Industry Developments

- In August 2025, Costa Rica-based Etiplast S.A. invested in a new Nilpeter FA-22 flexographic press to expand its production capacity and reinforce its leadership in the Central American market. The FA-22 is configured for flexible packaging applications, such as coffee bags and shrink sleeves, and will free up existing FA-14 presses to concentrate on label production. Etiplast says the move is part of its strategy to deliver greater flexibility, higher efficiency and improved consistency for its customers.

- In March 2025, DuPont’s Cyrel Flexographic Solutions business entered a new distribution partnership with All Printing Resources, Inc. (APR) to widen access to its full portfolio of Cyrel® platemaking solutions across North America. Under the agreement, APR will distribute the complete suite of Cyrel® plates and equipment, such as the Cyrel® FAST technology, and offer on-the-ground technical service and support to complement DuPont’s offering. The move is intended to make it easier for converters and trade shops to leverage Cyrel® innovations to boost print quality, productivity and sustainability in flexographic packaging.

- In February 2025, at PrintPack 2025, Insight Print Communications secured India’s first sale of the Fujifilm Revoria SC285S press, in partnership with Fujifilm. The advanced machine boasts LED-printhead technology, up to 2,400 dpi resolution, and a vertical toner-development system that enables high-quality output even on textured paper. The buyer, Print Point of Chennai, noted that the SC285S’s seven-color capability (including specialty inks) and consistent speed align with their aim to serve evolving client needs.

Companies Covered in Flexographic Printing Technology Market

- Bobst Group SA

- Windmöller & Hölscher (W&H)

- Mark Andy Inc.

- Comexi Group

- Koenig & Bauer Flexotecnica

- KOMORI Corporation

- Heidelberg Group

- Nilpeter

- Uteco Converting S.p.A.

- Shinko Machinery Co., Ltd.

- Monotech Systems Limited

- OMET

Frequently Asked Questions

The global flexographic printing technology market is projected to reach US$2.8 billion in 2025.

The rising demand for high-quality, durable, and customized packaging, along with the need for faster production and cost-efficient printing solutions, is a key market driver.

The market is poised to witness a CAGR of 6.2% from 2025 to 2032.

Increasing adoption of automation and digitalization in printing processes is creating strong growth opportunities.

Bobst Group SA, Windmöller & Hölscher (W&H), Mark Andy Inc., and Comexi Group are among the leading key players.