- Smart Packaging

- In-mold Labels Market

In-mold Labels Market Size, Share, and Growth Forecast, 2026 - 2033

In-mold Labels Market By Material (Polypropylene (PP), Polyethylene (PE), Others), Printing Technology (Flexographic Printing, Offset Printing, Others), Printing Inks, End-user Industry and Regional Analysis for 2026 - 2033

In-mold Labels Market Size and Trends Analysis

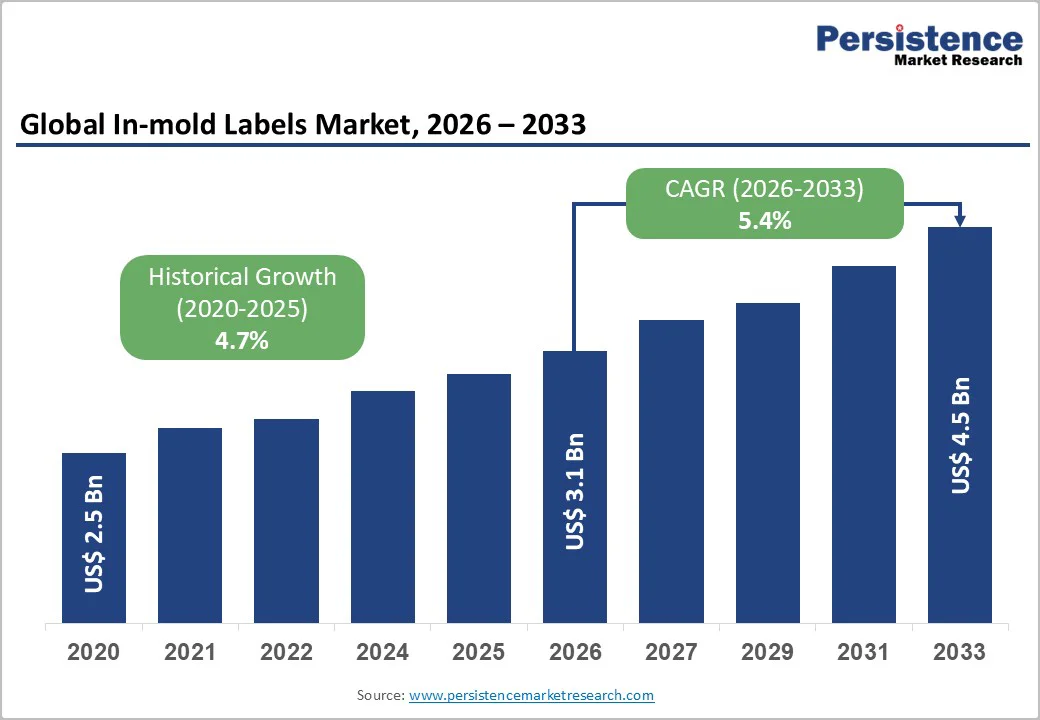

The global in-mold labels market size is likely to be valued at US$3.1 billion in 2026 and is expected to reach US$4.5 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033, driven by the rising need for integrated, durable, and tamper-resistant decoration in food and beverage and personal care packaging.

Growth in thin-wall injection molding and thermoforming across advanced and emerging manufacturing hubs supports adoption. Sustainability goals, including mono-material and recyclable polypropylene films, along with a shift toward hybrid and digital printing workflows, are shaping competitive dynamics.

Key Industry Highlights

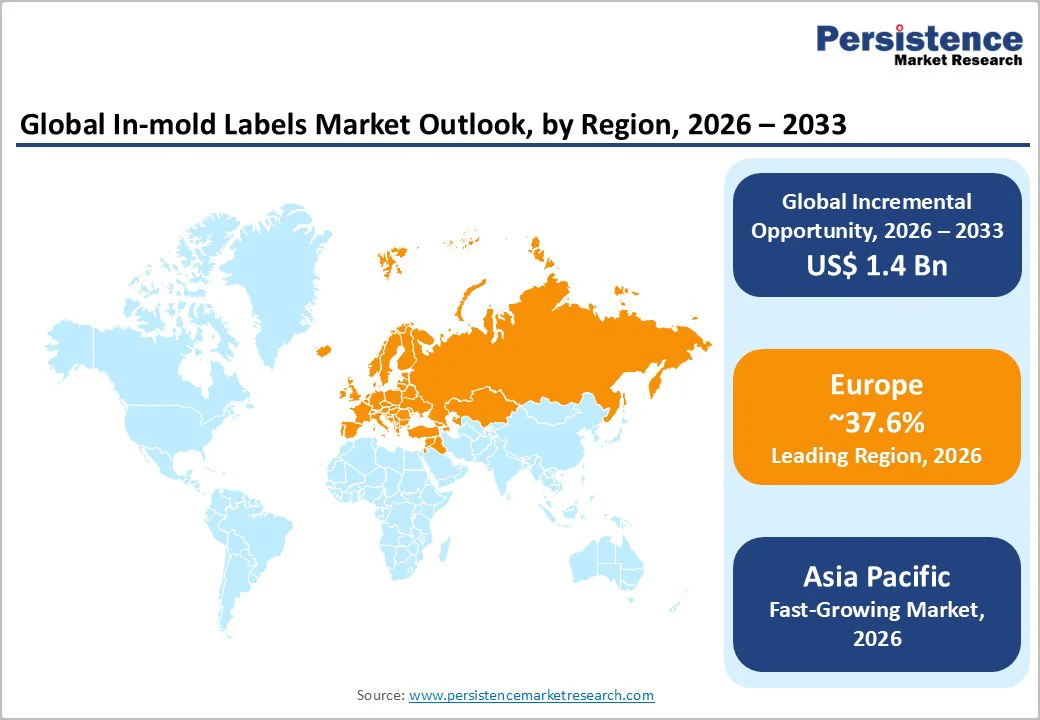

- Leading Region: Europe is expected to be the leading region, accounting for over 37.6% of total demand in 2026, driven by high penetration of injection-molded packaging in dairy, spreads, and ready-meal applications, alongside strict recyclability mandates that support mono-material PP and PE formats.

- Fastest-Growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rising FMCG consumption, expanding injection-molding capacity in China and India, and rapid adoption of digital printing technology for short-run IML applications.

- Investment Plans: Converters and resin manufacturers are increasing investments in mono-material PP and PE IML solutions, with several packaging groups announcing capacity expansions in high-speed flexographic and hybrid digital-flexo printing platforms. These investments aim to support recyclability targets and rising demand for customized product runs.

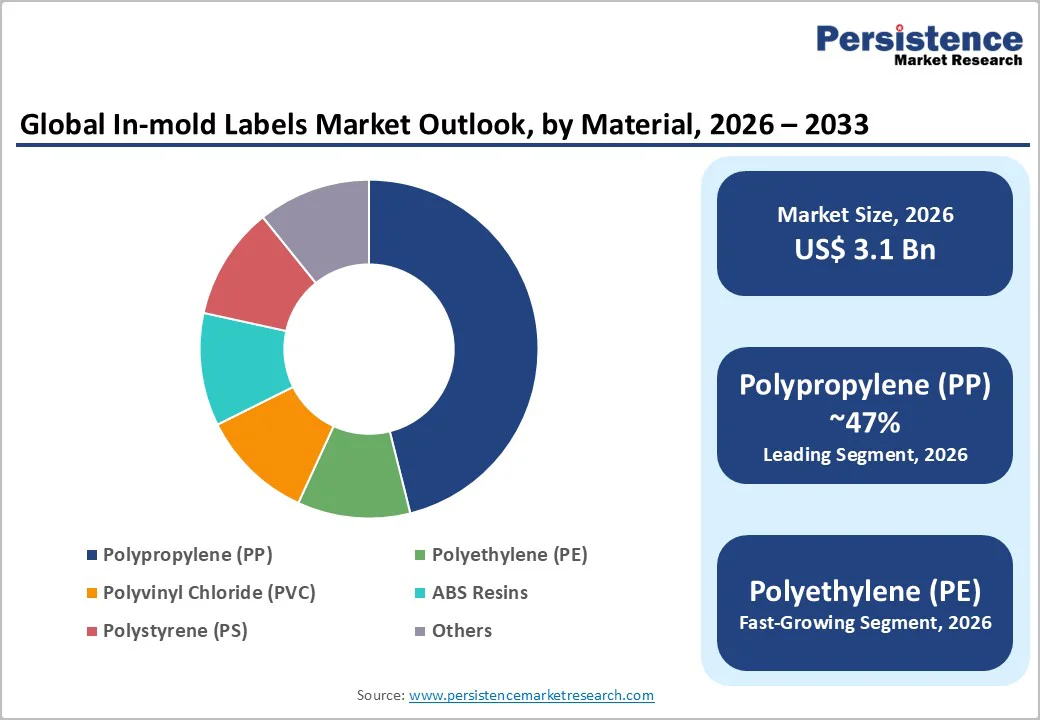

- Dominant Material: Polypropylene (PP) is anticipated to be the dominant material category with a 47% share in 2026, supported by its suitability for thin-wall molding, strong heat resistance, and compatibility with food-grade mono-material packaging structures.

- Leading Printing Technology: Flexographic printing is expected to be the leading technology, with a 51.3% share in 2026, driven by its operational speed, color consistency, and cost efficiency in high-volume production environments.

| Key Insights | Details |

|---|---|

|

In-mold Labels Market Size (2026E) |

US$3.1 Bn |

|

Market Value Forecast (2033F) |

US$4.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Durable, Integrated Decoration Demand

Brands rely on In-mold Labels (IML) to deliver abrasion resistance, moisture stability, and high-quality graphics that do not peel or distort during distribution and handling. Expansion of thin-wall metal injection molding for single-serve and resealable formats reinforces this preference. High-speed molding lines adopted by beverage and consumer goods producers are designed to accommodate IML with minimal downtime. The shift toward IML for large-volume SKUs increases per-unit label value through higher-grade films and pre-print processes, supporting market growth and contributing to consolidation among converters.

Sustainability and Recycling Policy Alignment

Global policy momentum surrounding packaging recyclability is accelerating the transition to mono-material polypropylene IML solutions. Brands and regulators are prioritizing packaging formats that move efficiently through mechanical recycling streams, which positions PP IML as a preferred option for thin-wall containers and FMCG items. Collaboration between resin manufacturers and IML converters is producing validated mono-PP systems suitable for commercial adoption.

As companies increase commitments to recycled-content targets and net-zero roadmaps, demand for certified PP grades, compatible ink systems, and recyclable adhesive formulations is rising. Although these materials carry higher near-term costs, they enable a premium circular-economy value proposition and create differentiation across the supply chain.

Printing & Digitalization for Versioning and Short Runs

While flexographic and gravure printing remain essential for long-run production, digital printing is gaining momentum as brands seek rapid SKU updates, seasonal variants, and localized editions. Digital inkjet systems offer quick turnaround times and allow converters to integrate anti-counterfeiting features and personalized elements without disrupting high-volume workflows. Hybrid print models combining flexo base layers with digital overlays offer both cost efficiency and flexibility in customization. Investments in heat-resistant digital ink technologies are making IML more suitable for molded parts that require durability. As converters adopt digital capabilities, the value proposition shifts from commodity film output toward integrated design, data, and personalization services.

Barrier Analysis - Upfront Tooling and Equipment Capital

High-speed IML operations require precision molds, robotics for label placement, and controlled stacking and feeding systems. These upgrades represent substantial capital requirements that hinder adoption for smaller converters or brand-owned molding facilities. Tooling and equipment retrofits often reach several hundred thousand dollars per cell, extending payback timelines and limiting flexibility for low-volume or experimental SKUs. As a result, market participation is weighted toward larger converters capable of absorbing capital costs and operating multiple high-utilization production lines.

Material and Process Compatibility Constraints

Technical limitations arise when integrating IML into legacy molding lines, especially when switching to mono-material recyclable formats. Variations in polymer melt temperatures, film thickness, and adhesive behavior require extensive testing and reformulation. Migration compliance and durability validation for regulated packaging, such as infant nutrition or pharmaceuticals, further extend qualification cycles. These testing phases frequently span two to six months, adding cost and time before commercial approval. Such complexities slow broad adoption and create obstacles for applications requiring tight regulatory oversight.

Opportunity Analysis - Mono-Material Circular IML Systems

Mono-PP and mono-PE IML systems present strong potential as global circular-economy commitments accelerate. If mono-material formats capture 30 to 40% of food and beverage IML volumes by 2030, the incremental value opportunity for certified films, specialty inks, and compatibility testing could reach mid-single-digit percentage growth beyond baseline forecasts, equivalent to tens or potentially hundreds of millions of dollars by 2033. Suppliers able to commercialize validated, recyclable film-ink-adhesive combinations will be positioned to capture premium market share associated with circular packaging requirements.

Smart IML (RFID/Traceability)

Interest is increasing in embedding RFID and NFC technologies within IML structures during molding. These labels can support reusable packaging models, supply-chain tracking, and anti-counterfeiting functions. Early commercial pilots have demonstrated strong potential for high-value applications where traceability and data integration justify higher costs. The opportunity is expected to scale rapidly from a small base, supported by collaborations between converters, RFID specialists, and brand owners. Integrating electronics within the label layer enhances the functional value of IML and opens long-term service-oriented revenue streams for suppliers.

Category-wise Analysis

Material Insights

Polypropylene (PP) is anticipated to hold a 46.5% market share in 2026, reflecting its position as the preferred substrate for thin-wall containers used in FMCG packaging. PP supports high-speed injection molding with stable label fusion, which helps converters maintain output consistency for applications such as yogurt tubs, margarine containers, and household cleaning product jars. Its strength-to-weight balance, moisture barrier, and heat stability are crucial for products exposed to hot filling, pasteurization, or repeated refrigeration cycles. PP is also well aligned with mono-material packaging strategies. For instance, several dairy brands in Europe now specify mono-PP containers paired with PP IML films to simplify recycling streams.

Polyethylene (PE) is expanding rapidly as brands explore softer, more flexible container formats suited to PE’s mechanical behavior. PE’s growth is supported by advances in surface-treatment and ink-adhesion technologies that enable high-quality labeling without distortion during molding. Converters are commercializing mono-PE IML solutions for squeezable food packs, children’s products, and lightweight household bottles. For example, several personal care brands have begun testing PE-based IML tubs to meet retailer-driven recyclability guidelines. Specialty PP blends with higher impact resistance or tailored melt-flow characteristics are also gaining momentum for applications requiring enhanced shelf durability or decorative precision. The increased availability of PCR-PE and PIR-PP resin grades is driving this shift, making PE and engineered PP variants the fastest-growing materials in the IML ecosystem.

Printing Technology Insights

Flexographic printing is projected to account for 51.3% of the market share in 2026, underscoring its dominance in long-run, high-volume packaging environments. Flexo’s rapid setup, consistent color reproduction, and compatibility with both PP and PE IML films make it the default choice for converters producing large batches of dairy tubs, condiment containers, and beverage lids. Major label converters in Europe, North America, and Southeast Asia rely on flexo as their primary workflow due to its predictable ink laydown and fast drying times, which reduce bottlenecks during high-speed molding. Some operations pair flexo with gravure for premium finishes on ice cream, ready meals, and nutraceutical packaging.

Digital printing is achieving the fastest CAGR as brands pursue shorter cycles, customized artwork, and seasonal refreshes. Its variable data, QR engagement, and authentication features, without plate changes, suit high-SKU segments such as confectionery, dairy desserts, and limited-edition beverage cups.

Converters are adopting hybrid presses that pair flexo base layers with digital finishing to optimize cost and creativity; several European players now run festival-themed yogurt tubs and personalized promotional packs this way. As these systems mature, digital printing is transforming competitiveness in IML converting for short to mid-size runs.

Regional Insights

North America In-Mold Labels Market Trends - Automation and Mono-PP Drive Sustainable Growth

Growth in North America is driven by its advanced manufacturing base, high consumption of packaged goods, and strong adoption of automation. The U.S. leads regional demand with extensive installation of thin-wall injection molding lines designed for fully integrated IML operations. Beverage, dairy, personal care, and household goods manufacturers contribute significantly to volume consumption, supported by a well-established converter ecosystem.

High-speed robotics, improved label-handling systems, and consistent investments in modernizing production lines drive market growth. Many U.S. brands are prioritizing sustainability commitments that emphasize recyclable packaging, which is accelerating interest in mono-PP IML solutions. These shifts influence supply-chain relationships and place greater emphasis on technical validation and compatibility testing.

Regulatory compliance plays a meaningful role in this region. U.S. food-contact requirements demand rigorous evaluation of inks, adhesives, and film substrates to ensure safety under intended use conditions. Although this adds complexity to material qualification, it creates barriers to low-cost substitution and reinforces market concentration among technically advanced suppliers. Investment patterns include upgrades to hybrid printing systems, expansion of digital capabilities, and deployment of robotic label feeders that improve repeatability and reduce scrap. With demand for personalization rising, converters are increasing capacity for digital finishing and rapid prototyping. Long-term opportunities center on circular-packaging partnerships and co-development of validated mono-PP systems tailored to North American recycling streams.

Europe In-Mold Labels Market Trends - Regulations Fuel Innovation in Circular Packaging

Europe is anticipated to be the leading region in 2026, accounting for over 37.6% of total demand, propelled by a strong regulatory framework, mature consumer-goods markets, and high penetration of thin-wall molded packaging. Germany’s industrial strength and advanced molding capabilities make it a hub for high-precision IML used in automotive, appliance, and premium consumer goods applications. The U.K. and France exhibit strong demand from personal care and food brands that emphasize sustainability and packaging aesthetics. Spain benefits from growing thermoforming activity and regional consumer-goods production.

Regulatory frameworks, particularly the EU Packaging and Packaging Waste Regulation, are the major growth drivers. Requirements for recyclability, recycled content, and environmental performance are prompting rapid development of mono-material PP and PE IML solutions. This regulatory emphasis accelerates innovation in ink systems, adhesives, and film treatments that ensure compatibility with European recycling infrastructures.

Investments focus on circular-economy solutions, regional testing laboratories, and partnerships between resin manufacturers and IML converters to develop certified recycling-ready systems. European firms are also at the forefront of lightweighting, eco-design, and high-quality digital printing for customized packaging campaigns. With retailers and brands setting aggressive sustainability targets, Europe is expected to remain a driver of innovation for the global IML industry.

Asia Pacific In-Mold Labels Market Trends - High-Volume Manufacturing Accelerates IML Market Expansion

Asia Pacific offers the highest volume growth potential, driven by rising disposable incomes, expanding packaged-goods consumption, and large-scale manufacturing activity. China leads regional adoption with extensive injection molding infrastructure and broad application of IML across household products, personal care items, and mass-market FMCG. The country’s significant manufacturing capability positions it as both a major consumer and exporter of IML-decorated goods.

Japan contributes through highly technical applications in premium personal care, automotive components, and durable goods that require precision decoration. Manufacturing investments across the Asia Pacific include the adoption of high-speed robotics, automated label placement cells, and digital printing assets that enhance local converter capabilities. Regional converters benefit from cost-competitive labor structures, enabling rapid scaling of high-volume production.

Regulatory developments vary across APAC, but many markets are advancing extended-producer-responsibility schemes and recyclability guidelines, strengthening demand for mono-PP IML systems. Although recycling infrastructure remains uneven, multinational brands increasingly require packaging aligned with global sustainability standards. Regional investments emphasize automation, certification of recyclable formats, and long-term supply agreements with major FMCG companies. As global supply chains shift toward regionalization, the Asia Pacific is expected to remain a key hub for high-volume IML production, technical development, and sustainability-driven innovation.

Competitive Landscape

The global in-mold labels market is moderately concentrated, with the top tier of large label and packaging companies accounting for an estimated 35 to 50% of global capacity. These companies maintain strong integration across film production, printing, and technical services, giving them scale advantages. Regional specialists and niche converters support localized demand and tailor offerings for specific molding applications or end-use markets. Market competition emphasizes validated recycling-compatible film structures, consistent print quality, and robust technical support during tooling and line integration.

Key strategies include circular-material innovation, hybrid printing adoption, and geographic expansion into high-growth APAC markets. Companies differentiate through validated recycling compatibility, rapid personalization services, and integrated film-adhesive-print systems that shorten brand qualification cycles and enhance long-term customer retention.

Key Industry Developments

- In April 2025, Tageos inaugurated an Innovation Center of Excellence (ICoE) near Munich, backed by a multi-million-Euro investment. The facility, over 700 m² of R&D and project space, is designed for rapid prototyping and integration of advanced technologies such as printed antennas, flexible sensors, and dual-frequency RFID/NFC inlays for IML applications, pointing to a push toward smart, connected packaging.

- In June 2025, Tageos unveiled its EOS-450 U9 inlay based on NXP’s UCODE 9 IC (approved for ARC Spec Z), optimized for food supply-chain and quick-service-restaurant workflows. The inlay reportedly offers high read performance even on challenging substrates and enables full traceability, supporting real-time tracking, expiry monitoring, and FIFO workflows for perishable goods packaged using IML.

Companies Covered in In-mold Labels Market

- CCL Industries

- Verstraete IML

- Korsini

- IntraPac Group

- Coveris

- Fuji Seal International

- Yupo Corporation

- Labeltech

- Smyth Companies

- Tekni-Plex

- Multi-Color Corporation (MCC)

- Holoplastics

- Pago International

- Schobertechnologies

- Brady Corporation

- Butler Automatic

- Henkel AG & Co. KGaA

- Huhtamaki Oyj

- Taghleef Industries

- Flexplast

Frequently Asked Questions

The in-mold labels market size is estimated to reach US$3.1 billion in 2026.

By 2033, the market value is projected to reach US$4.5 billion.

Key trends include rising adoption of mono-material packaging to support recyclability and increasing use of digital printing and high-definition graphics for brand differentiation.

Polypropylene (PP) is the leading material segment, accounting for 47% share of the IML material mix due to its molding compatibility, durability, and recyclability advantages.

The in-mold labels market is projected to grow at a CAGR of 5.4% between 2026 and 2033.

Major players include CCL Industries, Multi-Color Corporation (MCC), Huhtamaki, Constantia Flexibles, and Coveris.