- Non-food Packaging

- Clamshell Labelling Machines Market

Clamshell Labelling Machines Market Size, Share, and Growth Forecast, 2026 - 2033

Clamshell Labelling Machines Market by Labelling Type (Pressure Sensitive Labels, Shrink Sleeves, Others), Automation Level (Fully Automatic, Semi-Automatic, Manual), End-user Industry (Food and Beverages, Healthcare, Others), and Regional Analysis 2026 - 2033

Clamshell Labelling Machines Market Size and Trends Analysis

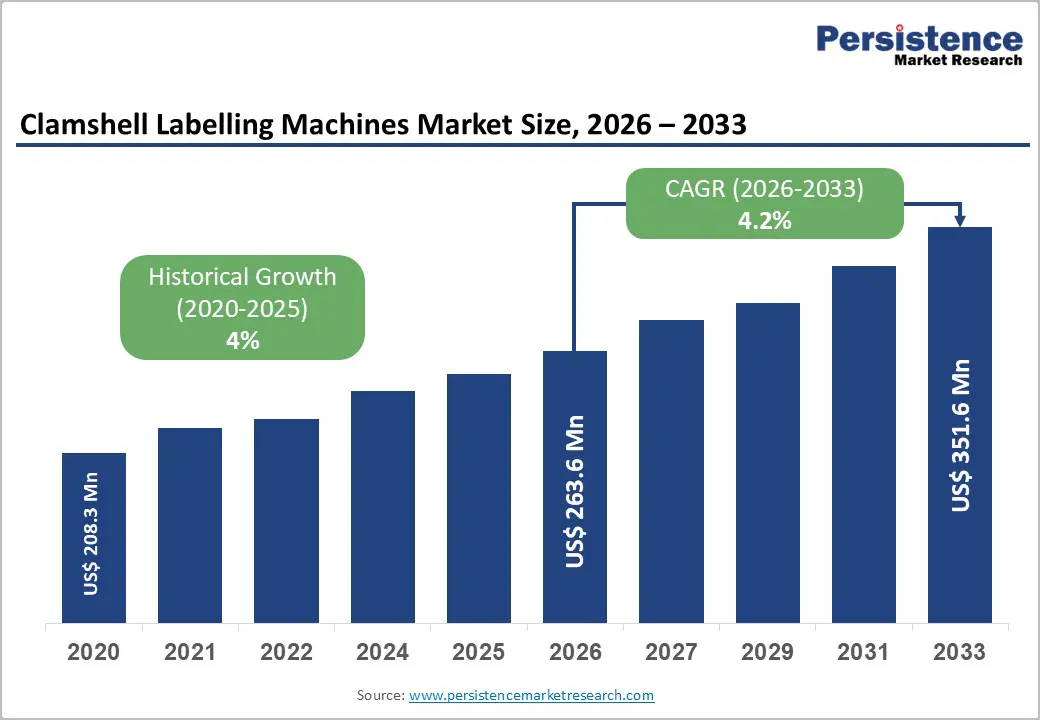

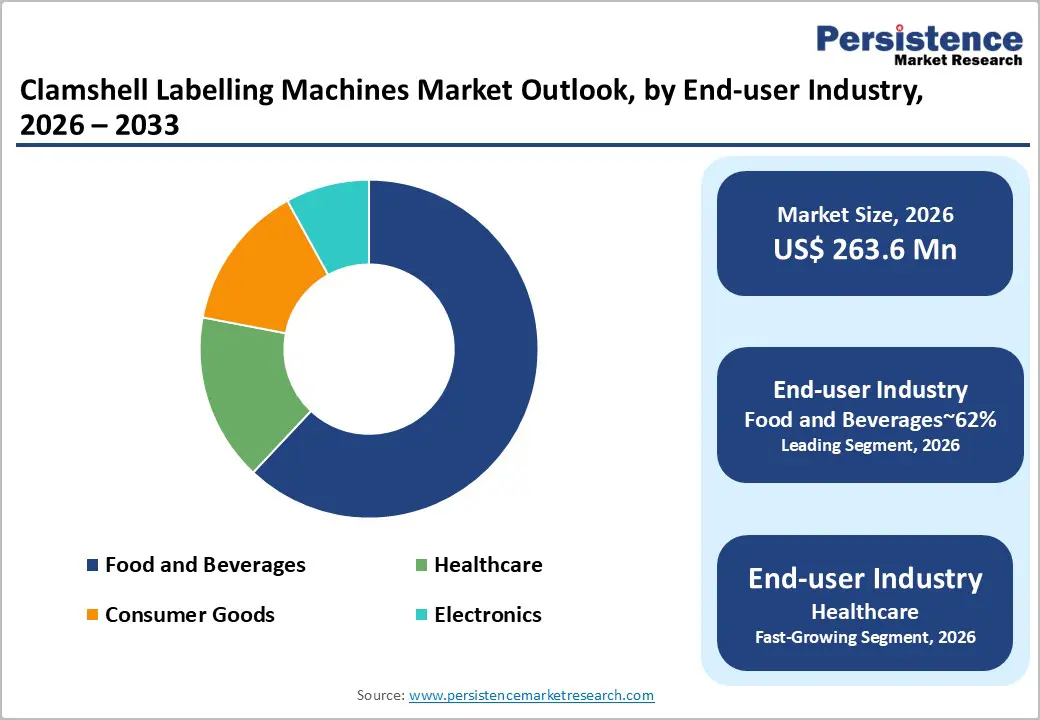

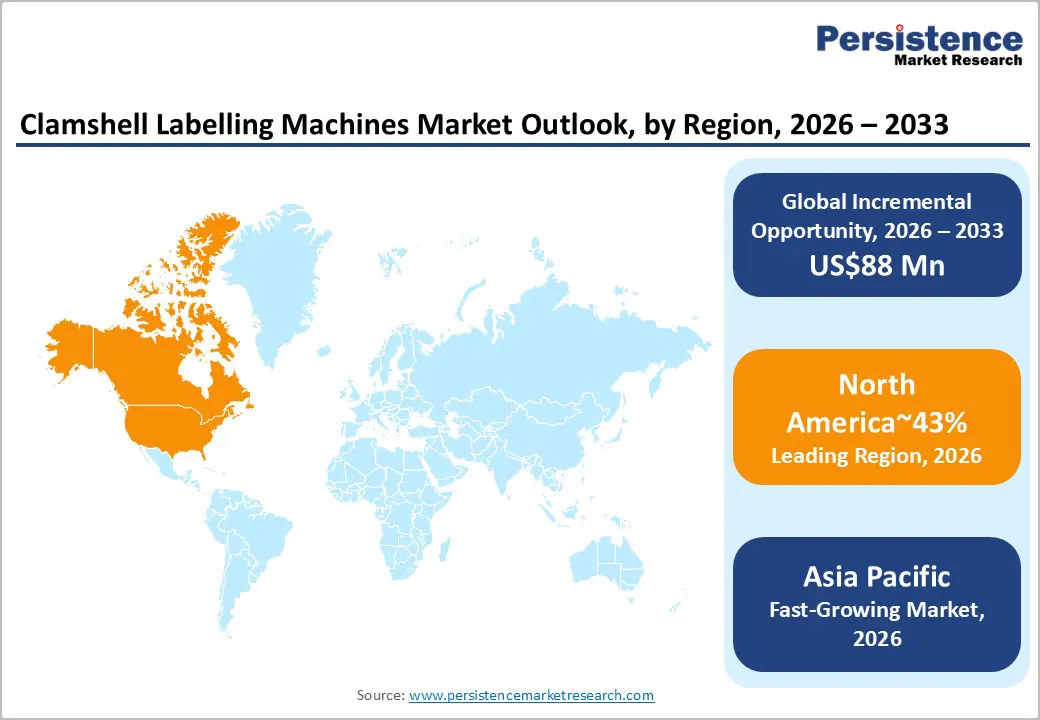

The global clamshell labelling machines market is likely to be valued at US$263.6 million in 2026 and is expected to reach US$351.6 million by 2033, growing at a CAGR of 4.2% from 2026 to 2033.

The market demonstrates highly resilient and steady expansion anchored by escalating packaging automation demands. Primary growth catalysts include the exponential rise of the global packaged food sector and rigorous regulatory standards instituted by health authorities enforcing precise, tamper-evident product coding. Consequently, manufacturers are systematically integrating AI-driven vision systems and high-throughput labelers to optimize operational efficiencies, reduce labor dependencies, and secure complex supply chain integrity across all major retail verticals.

Key Industry Highlights:

- Leading Region: North America is projected to lead due to deep automation penetration and regulatory stringency, accounting for approximately 43% share in 2026, supported by advanced AI-enabled inspection platforms and a mature packaging ecosystem.

- Fastest-Growing Region: Asia Pacific is expected to grow fastest due to rapid industrial expansion, investment in cold-chain infrastructure, evolving compliance standards, and accelerating automation adoption across the food and pharmaceutical sectors.

- Leading Labelling Type: Pressure-sensitive labels are expected to lead, accounting for approximately 64% share in 2026 through broad industrial adoption, high throughput compatibility, labelling precision, and suitability for high-value food and beverage applications.

- Leading End-user Industry: Food and beverages are projected to dominate due to versatility, cost efficiency, and suitability across fresh produce, ready-to-eat meals, and bakery applications, accounting for approximately 62% share in 2026.

| Key Insights | Details |

|---|---|

| Clamshell Labelling Machines Market Size (2026E) | US$263.6 Mn |

| Market Value Forecast (2033F) | US$351.6 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automation Demand in Packaging

The increasing adoption of automation in food and consumer goods packaging is structurally transforming operational efficiency across production lines. Automated clamshell labelling systems enable high-speed processing while maintaining tamper-evident standards, reducing reliance on manual labor and minimizing human error. Regulatory compliance pressures, including labelling accuracy requirements enforced by authorities such as the FDA, amplify investment incentives for automated solutions. These systems integrate seamlessly with upstream filling and sealing equipment, optimizing throughput and reducing downtime across high-volume production cycles. Adoption also enables standardization of labelling formats, enhancing cross-market compatibility and reducing SKU-specific reconfiguration time in multi-product facilities.

Automation demand drives broader market growth by reallocating resources toward high-value production activities and innovation initiatives. Process standardization reduces error rates, supports lean manufacturing practices, and improves overall equipment effectiveness metrics across food and beverage operations. Investment in semi-automatic and fully automatic systems allows manufacturers to maintain consistent quality while scaling output for expanding consumer demand. Automation platforms also facilitate real-time data collection, enabling predictive maintenance and process optimization. Market expansion is reinforced by increasing regulatory scrutiny, consumer expectations for accurate labelling, and demand for rapid fulfillment.

Rising Demand in the Global Packaged Food Sector

The expanding global packaged food industry is structurally driving the adoption of high-speed clamshell labelling systems across production lines. Shifts in consumer preferences toward ready-to-eat meals, fresh produce, and single-serve bakery products are intensifying requirements for automated packaging infrastructure. Regulatory frameworks mandating nutritional transparency and accurate labelling amplify investment incentives for precision machinery, embedding compliance considerations into capital expenditure decisions. Automated clamshell labelers support rapid production while reducing human error and integrating effectively with filling, sealing, and quality inspection equipment. Technological enhancements, such as vision systems and servo-driven applicators, reinforce operational consistency and reduce the risk of errors.

This surge in demand for packaged food structurally reallocates resources toward automation and advanced production capabilities. Equipment investment patterns reflect a strategic emphasis on efficiency, throughput, and regulatory adherence across high-volume processing lines. Lifecycle advantages include reduced labor dependency, minimized rework, and consistent output quality, reinforcing cost-effectiveness. Automation adoption further enhances lean manufacturing practices, aligning facility performance with stringent food safety and labelling standards. Collectively, these factors solidify automated clamshell labelling as an indispensable component within modern packaged food production ecosystems, driving structural growth and technology integration across the sector.

Barrier Analysis - Complex Label Alignment Challenges for Irregular Clamshell Shapes

Clamshell containers with irregular geometries, ridges, or integrated hinges introduce structural difficulties for consistent label placement across production lines. Misalignment risks increase when conventional labelling mechanisms are applied to these non-uniform surfaces, creating potential compliance and quality issues. Advanced sensor technologies and vision-enabled accuracy controls are required to detect contours and dynamically adjust label application in real time. This introduces significant technical complexity for equipment integrators, necessitating specialized calibration, software algorithms, and mechanical precision. The requirement for highly trained operators or engineers adds operational overhead and increases lifecycle costs. Precision alignment systems also demand rigorous maintenance and validation protocols to ensure sustained accuracy, particularly in high-volume or high-speed facilities. Regulatory scrutiny over labelling accuracy further magnifies the operational stakes of misalignment incidents.

These challenges structurally constrain market entry for niche or smaller labelling solution providers, as technology integration costs and development barriers are elevated. Engineering expertise in optical sensors, servo-driven applicators, and contour mapping is essential to maintain accuracy across irregular container formats. Integration with upstream and downstream packaging stages requires precise synchronization to prevent cumulative errors. The added complexity raises capital intensity and necessitates higher upfront investment, particularly in facilities handling diverse clamshell designs. Consequently, these technical and operational factors limit the broader diffusion of automated labelling solutions in irregular container segments.

Specialized Maintenance Requirements and Skilled Labor Constraints

High-speed, precision clamshell labelling machines necessitate frequent calibration and specialized maintenance to sustain operational accuracy. The technical complexity of these systems requires expertise in servo mechanisms, vision-guided sensors, and software-controlled applicators. Limited availability of technicians trained specifically for these advanced labelling platforms constrains both routine maintenance and rapid troubleshooting during unplanned downtime. Maintenance-intensive environments also amplify capital expenditure for spare parts, diagnostic tools, and preventive service schedules. Regulatory and quality standards further necessitate consistent calibration and validation to avoid labelling errors.

The scarcity of skilled labor limits the expansion of after-sales service networks for high-speed clamshell labelling equipment. Smaller or niche providers face difficulties in recruiting and retaining technicians capable of maintaining complex machinery across multiple production sites. Training programs are resource-intensive, requiring substantial investment in technical education and hands-on experience to achieve proficiency. Inconsistent maintenance practices increase operational risk, reduce line availability, and elevate lifecycle costs, particularly for facilities handling diverse container formats. Integration with production monitoring systems demands continual oversight to detect misalignment or sensor drift, further stressing limited personnel resources.

Opportunity Analysis - Integration of AI-Powered Vision Systems and Predictive Maintenance

The convergence of artificial intelligence with clamshell labelling machinery is structurally enhancing operational precision and reliability across production lines. AI-driven machine-vision systems enable real-time detection and correction of misalignments, barcode validation, and contour adjustments, reducing waste and ensuring compliance with labelling standards. Predictive maintenance modules leverage sensor data and machine learning algorithms to forecast component wear and potential failures, minimizing unplanned downtime and safeguarding throughput efficiency. The ability to capture continuous operational data also facilitates performance benchmarking and regulatory reporting, further embedding AI solutions into strategic production management. Adoption of such intelligent systems strengthens OEMs' competitiveness in the high-precision packaging ecosystem.

These capabilities structurally create new commercial avenues beyond traditional equipment sales by enabling subscription-based software and predictive service offerings. Manufacturers can generate recurring revenue streams through continuous monitoring, remote diagnostics, and proactive maintenance scheduling. Integration of AI platforms also supports modular scalability, allowing operators to expand labelling capabilities without extensive hardware retrofits. The convergence of machine intelligence and maintenance analytics fosters strategic differentiation for equipment providers, reshaping competitive dynamics within the global clamshell labelling market. This progression positions AI-powered solutions as a critical growth driver in the adoption of advanced packaging technology.

Transition toward Sustainable, Eco-Friendly Labelling Formats

Corporate sustainability mandates and regulatory pressures are structurally reshaping demand for eco-friendly clamshell labelling solutions across the packaging ecosystem. Machinery capable of processing liner-less labels, compostable paper-based formats, and bio-based adhesives addresses the growing need for environmentally responsible production while reducing reliance on single-use plastics. Adoption of such systems directly impacts upstream and downstream operations by minimizing material waste, enhancing recyclability, and ensuring compatibility with rapidly evolving regulatory frameworks. Manufacturers integrating agile, sustainability-oriented labelling technologies can strengthen partnerships with global FMCG brands focused on net-zero commitments. These developments elevate the market significance of green labelling systems within the high-speed packaging landscape, embedding eco-efficiency as a core operational requirement.

The structural shift toward sustainable labelling creates high-value opportunities for equipment providers able to innovate in material handling and applicator design. Specialized machinery ensures consistent label placement on diverse eco-friendly substrates, overcoming technical barriers inherent in thin or compostable materials. Integration of adaptable label applicators reduces line reconfiguration times, supporting multi-SKU flexibility while maintaining production throughput. Manufacturers that pioneer reliable, eco-compatible labelling platforms position themselves to capture premium partnerships and long-term adoption across global food, beverage, and consumer goods supply chains.

Category-wise Analysis

Labelling Type Insights

Pressure-sensitive labels are expected to lead, accounting for approximately 64% share in 2026, underpinned by their entrenched role in high-speed food and beverage production lines and widespread adoption across PET, foam, and paperboard clamshell substrates. Adoption remains anchored by superior adhesion, minimal setup requirements, and operational efficiency, with providers prioritizing throughput optimization, standardization, and continuous-motion integration in high-volume environments. Ongoing platform evolution, including AI-enabled inspection, vision-assisted alignment, and automation-ready applicators, continues to reinforce replacement cycles and utilization intensity. Leading brands such as Avery Dennison, CCL Industries, Multi-Color Corporation, Nita Labelling Systems, and Herma offer comprehensive PSL platforms that lock in enterprise workflows while supporting sustainable adhesives and all-temperature bonding.

Pressure-sensitive labels are expected to be the fastest-growing segment, driven by emerging needs for agile, short-run, and e-commerce-focused packaging formats. Growth is being catalyzed by innovations in eco-friendly adhesives, linerless technologies, and variable data printing capabilities, which materially improve speed, accuracy, and regulatory traceability. Leading brands, including Avery Dennison, CCL Industries, UPM Raflatac, 3M, and Multi-Color Corporation, are deploying new adhesive formulations and high-precision platforms to capture early-cycle demand and embed switching costs.

End-user Industry Insights

Food and beverages are anticipated to dominate the market, accounting for approximately 62% share in 2026, underpinned by its entrenched role in fresh produce, ready-to-eat meals, and bakery packaging, where clamshells are the non-negotiable standard for product protection. Adoption remains anchored by washdown-compatible labelling machinery, high-speed synchronization with conveyors, and C-Wrap tamper-evident application, with providers prioritizing throughput, precision, and dual-demand label placement in high-volume environments. Leading brands such as Mettler-Toledo, Bizerba, EPI Labelers, Nita Labelling Systems, and Esperanza offer integrated high-speed solutions and antimicrobial or breathable labelling technologies that lock in enterprise workflows. This combination of mature infrastructure, process reliability, and demand predictability sustains the segment’s dominance within structured F&B production lines.

Healthcare is expected to be the fastest-growing segment in the Clamshell Labelling market, driven by emerging needs for precise serialization, medical device traceability, and pharmaceutical compliance across diagnostic kits, surgical supplies, and therapeutic packaging. Growth is being catalyzed by the strict global rollout of serialization mandates, vision-enabled clamshell labelers, and automation-compatible systems, which materially improve accuracy, regulatory adherence, and operational reliability. Leading brands, including Avery Dennison, CCL Industries, UPM Raflatac, 3M, and Multi-Color Corporation, are deploying specialized high-precision platforms to capture early-cycle demand and embed workflow consistency. As industrial validation, workforce familiarity, and compliance assurance improve, the segment is expected to outpace overall market growth.

Regional Insights

North America Clamshell Labelling Machines Market Trends

North America is expected to remain the leading regional market, accounting for approximately 43% share in 2026, supported by deep automation penetration, regulatory stringency, and concentrated packaging innovation capabilities. The region is positioned to maintain structural dominance through high enterprise adoption of tamper-evident and traceable clamshell labelling systems across food, beverage, and pharmaceutical supply chains. Demand is anticipated to remain anchored in advanced C-wrap security formats, AI-enabled inspection platforms, and modular machinery architectures integrated within smart-factory environments. A consolidated competitive landscape led by ProMach, Pack Leader USA, Quadrel Labelling Systems, and Weber Packaging Solutions is likely to reinforce ecosystem depth and aftermarket service intensity. Sustainability mandates and minimalist labelling trends are expected to accelerate equipment retrofits capable of handling linerless and recycled substrates, while cloud-connected diagnostics and labelling-as-a-service models further embed lifecycle-driven monetization across mature production facilities.

The U.S is projected to anchor regional momentum, shaping procurement strategies through strict enforcement of federal labelling, traceability, and tamper-evidence frameworks. Large-scale food processing corridors and high-volume agricultural packaging clusters are anticipated to drive continued investment in fully autonomous, lights-out labelling installations and vision-guided robotic integration. Investment flows are expected to concentrate on cloud-enabled diagnostics and non-proprietary electronics architectures that reduce downtime risk and improve maintenance flexibility. As sustainability legislation and consumer safety expectations intensify, U.S.-based manufacturers are positioned to accelerate modernization cycles, reinforcing North America’s structural leadership in advanced clamshell labelling machinery and intelligent packaging ecosystems.

Asia Pacific Clamshell Labelling Machines Market Trends

Asia Pacific represents the fastest-growing regional market in 2026. China anchors regional demand through export-oriented manufacturing and the expansion of large-scale cold-chain infrastructure, while India, Japan, and ASEAN economies accelerate the modernization of food and pharmaceutical packaging lines. Structural drivers include rapid urbanization, rising disposable incomes, and a measurable shift from labor-intensive processes to automated precision systems. OEM competitiveness while attracting foreign direct investment into turnkey greenfield packaging facilities.

The “leapfrog effect” describes capital expenditure behavior, as processors bypass semi-automatic stages and deploy AI-integrated systems calibrated to exceed 250 units per minute to meet export-grade compliance. Expansion of integrated cold chains across China and India amplifies demand for moisture-resistant labelling configurations. Organized retail penetration remains structurally low in India relative to developed markets, implying strong forward demand elasticity. Emerging trends include QR-centric functional labelling, PLA-based clamshell adoption requiring low-heat application modules, and vertically integrated packaging hubs designed for high-throughput agricultural exports, reinforcing Asia Pacific’s long-term growth leadership.

Europe Clamshell Labelling Machines Market Trends

Europe represents a structurally mature and regulation-intensive market environment for clamshell labelling machines, characterized by engineering-led competitiveness and harmonized compliance architecture. Germany and the U.K. anchor regional revenues, supported by export-oriented agricultural clusters across France and Spain. Regulatory convergence within the European Union drives capital expenditure cycles, particularly through directives targeting the reduction of single-use plastics and enforcement of traceability under the Falsified Medicines Directive. Compliance-driven modernization, rather than volume expansion alone, remains the core catalyst for investment across pharmaceutical and high-value fresh produce supply chains.

The competitive structure is concentrated among advanced German and Italian OEMs operating in the premium automation tier, emphasizing hygienic stainless-steel washdown configurations and micron-level accuracy in label placement. Capital allocation trends favor robotics-integrated systems aligned with the EU’s carbon-neutral industrial strategy, prioritizing energy optimization and material efficiency. A clear operational shift is underway toward decentralized smart-packaging nodes across Southern Europe, where exporters integrate AI-enabled clamshell labelers that dynamically adjust to multi-geometry container formats.

Competitive Landscape

The global clamshell labelling machines market is moderately fragmented, with leadership concentrated among global packaging automation groups such as ProMach, Krones AG, Pack Leader USA, Quadrel Labeling Systems, and Nita Labeling Systems. Market structure reflects a tiered ecosystem in which multinational integrators coexist with regional OEM specialists and niche automation builders. Leading suppliers matter not solely due to installed base scale, but because they influence application standards, integration protocols, and procurement frameworks across food, pharmaceutical, and logistics packaging lines.

Competitive positioning is defined by vertical integration depth and horizontal portfolio breadth. Large conglomerates differentiate through end-to-end line integration, combining filling, inspection, coding, and labelling into unified control platforms, while mid-tier players focus on high-precision C-wrap systems or agricultural washdown configurations. Industry behavior indicates gradual ecosystem consolidation through bolt-on acquisitions, expansion of aftermarket service networks, and increasing adoption of cloud-connected diagnostics.

Key Industry Developments:

- In November 2025, ID Technology (a ProMach Brand) announced a multi-site facility expansion across North America, including major sites in York, PA, and Edmonton, Alberta. The significantly increased regional production capacity for labels and specialized applicator systems reduces lead times for the food and pharma sectors.

- In April 2025, Avery Dennison launched AD Cobra, a new RFID inlay specifically engineered for the unique operational challenges of the Indian market. This will provide a superior signal reliability for tracking clamshell-packaged goods through high-moisture and dense logistical environments.

Companies Covered in Clamshell Labelling Machines Market

- ProMach, Inc.

- Krones AG

- Avery Dennison Corporation

- Herma GmbH

- Sidel Group

- Videojet Technologies

- Markem-Imaje

- Domino Printing Sciences

- Quadrel Labeling Systems

- Label-Aire, Inc.

- Weber Packaging Solutions

- Nita Labeling Systems

- Pack Leader Machinery

- SATO Holdings Corporation

- Multivac

- ALTech UK

Frequently Asked Questions

The global clamshell labelling machines market is projected to be valued at US$263.6 million in 2026 and is expected to reach US$351.6 million by 2033, driven by rising automation in food packaging and increasing regulatory requirements for tamper-evident labelling.

The growing adoption of automated packaging lines in food, beverage, and healthcare industries is a primary driver, as high-speed clamshell labelling systems reduce labor dependency, improve accuracy, ensure regulatory compliance, and integrate seamlessly with filling, sealing, and inspection equipment.

The market is forecast to grow at a CAGR of 4.2% from 2026 to 2033, reflecting steady expansion supported by packaged food demand and increasing traceability standards across global supply chains.

North America leads the market, accounting for approximately 43% share, supported by advanced automation infrastructure, stringent labelling regulations, strong presence of packaging OEMs, and high adoption across food processing and pharmaceutical manufacturing sectors.

The market is moderately fragmented, with key players including ProMach, Inc., Krones AG, Avery Dennison Corporation, Herma GmbH, and Quadrel Labelling Systems. Competition is shaped by integrated automation capabilities, material science expertise, and expanding service-based packaging solutions.