- Smart Packaging

- Label Applicators Market

Label Applicators Market Size, Share, and Growth Forecast, 2026 - 2033

Label Applicators Market by Product Type (Automatic, Semi-Automatic, Others), Application (Flat Surface, Curved Surface, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Label Applicators Market Size and Trends Analysis

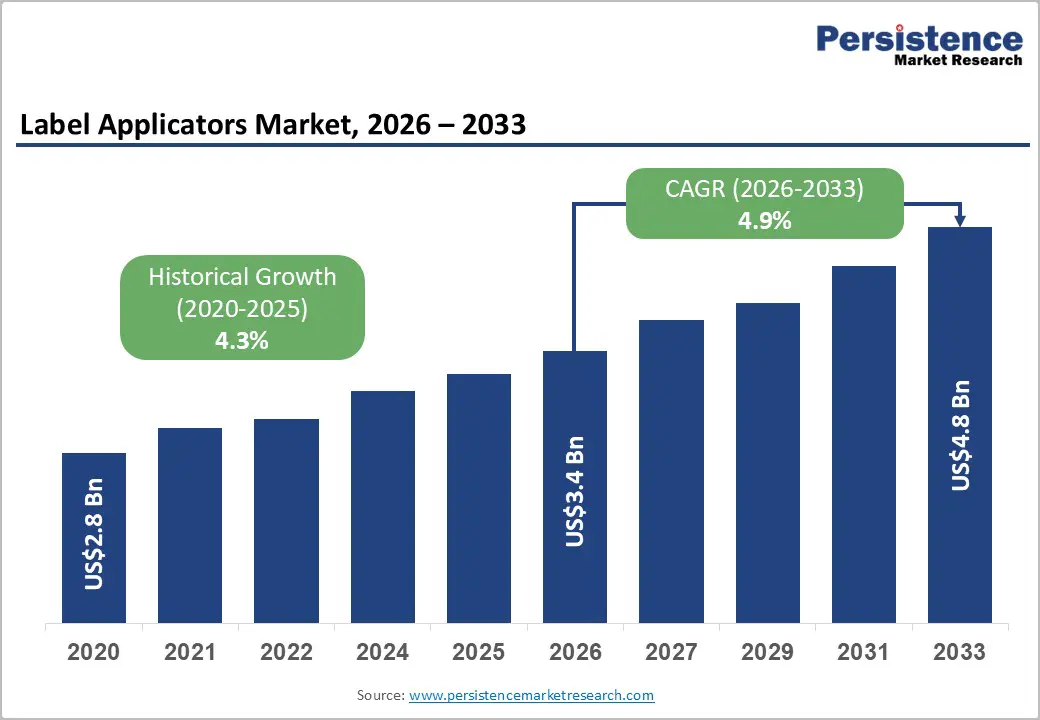

The global label applicators market size is likely to be valued at US$3.4 billion in 2026 and is expected to reach US$4.8 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033, driven by accelerating manufacturing automation, tightening regulatory traceability requirements, particularly in food & beverage and pharmaceutical sectors, and the broader integration of smart vision and Industry 4.0 technologies across packaging lines.

Capital expenditure is increasingly concentrated in mid- to high-speed automatic applicators and retrofit print-and-apply systems, whereas semi-automatic solutions continue to gain traction among mid-volume manufacturers that require operational flexibility and faster changeovers.

Key Industry Highlights:

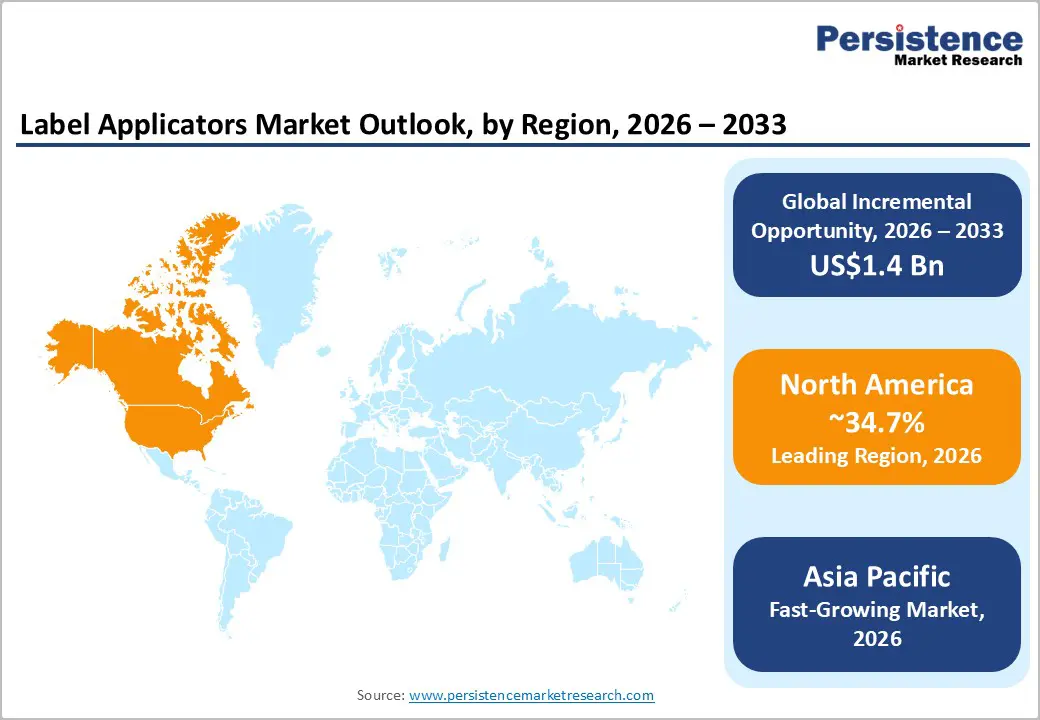

- Leading Region: North America is projected to lead the market with approximately 34.7% share, supported by high automation penetration, regulatory compliance upgrades, and a strong retrofit ecosystem across the food, beverage, and pharmaceutical industries.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by manufacturing expansion in China, India, and ASEAN, rising automation adoption, and increasing regulatory alignment with global traceability standards.

- Investment Plans: Capital expenditure is increasingly directed toward automatic and retrofit labeling systems, particularly vision-integrated and print-and-apply modules. Mid- to high-speed automation upgrades and modular retrofit programs are expected to account for a significant share of new investments through 2033.

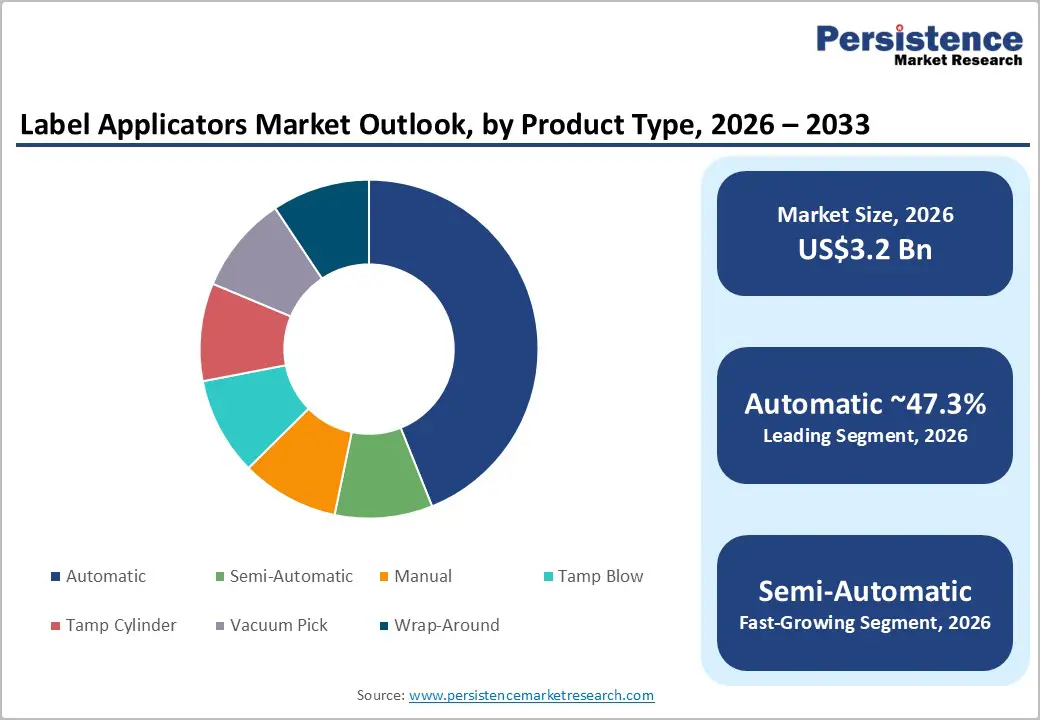

- Dominant Product Type: Automatic applicators are expected to dominate the product type category, accounting for approximately 47.3% of market share in 2026, due to large-scale adoption in high-speed FMCG, beverage, and pharmaceutical production lines.

- Leading End-use Industry: The food & beverage segment is the leading end-use industry, accounting for approximately 31.8% of the market, supported by regulatory labeling requirements, high production volumes, and diverse packaging formats.

| Key Insights | Details |

|---|---|

| Label Applicators Market Size (2026E) | US$3.4 Bn |

| Market Value Forecast (2033F) | US$4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automation and Industry 4.0 Adoption

Manufacturers across the food & beverage, pharmaceutical, and logistics sectors are prioritizing automation investments to reduce labor dependence, improve line efficiency, and enable end-to-end traceability. Digital factory initiatives increasingly incorporate automated wipe-on and print-and-apply labeling systems integrated with PLC and SCADA environments. Real-time device telemetry and cloud-based analytics improve throughput visibility, reduce labeling errors, and lower rework rates, strengthening the business case for automation capital expenditure.

The expansion of serialized labeling, particularly within regulated pharmaceutical supply chains, has further increased demand for applicators equipped with integrated printers, machine vision inspection, and data connectivity. Equipment suppliers that embed vision systems, connectivity, and remote diagnostics are achieving higher average selling prices and recurring service revenues, accelerating replacement cycles for legacy manual equipment.

Regulatory Traceability and Food/Pharma Compliance

Increasing regulatory scrutiny of labeling accuracy, ingredient disclosure, lot and expiry coding, and anti-counterfeiting has significantly increased the role of advanced labeling equipment. In the food and beverage industry, mandatory allergen declarations and nutritional transparency have intensified compliance requirements. In the pharmaceutical sector, serialization and track-and-trace mandates across multiple jurisdictions require precise label placement, variable data printing, and tamper-evident solutions.

As a result, manufacturers are shifting toward integrated applicator platforms that combine printing, inspection, and data capture capabilities. Demand is increasingly concentrated in bundled equipment and software solutions that support compliance documentation and audit readiness, driving higher system values and sustained after-sales service engagement.

Barrier Analysis -High Upfront Costs and Capital Investment Cycles

Automatic label applicators and integrated print-and-apply systems require substantially higher initial investment compared to manual or semi-automatic alternatives. For small and mid-sized enterprises, return-on-investment timelines often range from 18 to 48 months, depending on production volume and utilization rates. In cost-sensitive segments, these capital barriers reduce addressable demand, resulting in an estimated 20-35% slower automation penetration among small producers compared to large manufacturers. This dynamic sustains demand for semi-automatic and manual systems while moderating the pace of adoption of full automation.

Supply Chain and Component Constraints

Label applicator manufacturing relies on specialized components, including vision sensors, precision drives, and servo motors. Periodic supply-chain disruptions can extend equipment lead times and elevate production costs. Project delays of three to six months or longer introduce operational risk for end users planning capacity expansions. Prolonged shortages can increase bill-of-materials costs by mid-single- to low-double-digit percentages for advanced systems, thereby compressing suppliers' margins or raising end-user prices, which may defer purchasing decisions.

Opportunity Analysis - Retrofit and Modular Upgrade Market

A significant portion of installed packaging lines continues to operate with manual or semi-manual labeling systems. Modular retrofits, such as applicator heads, add-on print engines, and vision inspection modules, enable manufacturers to enhance automation without full line replacement. Market sizing estimate: If 20-30% of mid-tier production lines adopt retrofit solutions between 2026 and 2033, the resulting incremental opportunity could reach several hundred million dollars in equipment, software, and services. Suppliers offering standardized, low-disruption retrofit kits supported by financing options are positioned to capture a disproportionate share.

Smart and Sustainability-Focused Product Bundles

The convergence of sustainable packaging initiatives and smart labeling technologies is creating new value propositions. Demand is increasing for applicators compatible with recyclable label materials and adhesives, as well as connectivity features such as NFC and digital tracking. Sustainability-certified systems can command a mid-single-digit premium on average selling prices, particularly when bundled with compliance reporting and data integration capabilities. Actionable potential: Strategic collaboration between label material providers and applicator manufacturers can accelerate adoption and deepen customer lock-in.

Category-wise Analysis

Product Type Insights

Automatic label applicators are projected to account for approximately 47.3% of the market in 2026, reflecting their widespread adoption in high-speed food, beverage, and pharmaceutical production environments. These systems are engineered for continuous, high-throughput operations where precise label placement, repeatability, and minimal downtime are critical. Large-scale bottling plants, dairy processing facilities, and pharmaceutical solid-dose packaging lines increasingly rely on automatic wipe-on, tamp-blow, and wrap-around applicators integrated with conveyors, fillers, and inspection systems. Their compatibility with machine vision, serial printing, and real-time monitoring enables manufacturers to meet stringent regulatory and quality-assurance requirements.

The ability to standardize labeling operations across multiple global facilities further supports premium pricing and long-term supplier relationships. As multinational manufacturers continue to consolidate production and prioritize operational efficiency, automatic applicators remain the preferred solution for scalable, compliance-driven labeling operations.

Semi-automatic applicators are anticipated to be the fastest-growing product segment, driven by medium-volume producers seeking a balance between automation benefits and lower capital investment. These systems appeal to manufacturers that require flexibility to handle frequent SKU changes, short production runs, and diverse container formats, without the complexity of fully automated lines. Growth is particularly strong among craft beverage producers, nutraceutical companies, contract packers, and specialty personal care brands.

Recent advancements in ergonomic design, quick-change tooling, and integrated label dispensing mechanisms have significantly reduced setup time and operator training requirements. Semi-automatic applicators are increasingly used as transitional solutions for companies scaling from pilot or batch production toward higher commercial volumes. In emerging markets and cost-sensitive regions, they also serve as entry points into automation, enabling productivity gains while preserving operational adaptability.

End-use Industry Insights

The food and beverage industry is projected to account for approximately 31.8% of the market, making it the largest end-use segment. This dominance is supported by high production volumes, diverse packaging formats, and strict regulatory labeling requirements related to ingredients, allergens, nutritional information, and country-of-origin disclosures. Beverage bottling and canning operations, in particular, rely heavily on high-speed automatic applicators for wrap-around, front/back, and neck labeling.

Food processors deploy flat-surface and case labeling systems to support warehouse traceability, retail compliance, and logistics efficiency. The rapid expansion of private-label food brands and ready-to-eat products further increases labeling complexity and volume. Ongoing regulatory enforcement and frequent label revisions sustain continuous investments in adaptable, high-throughput labeling solutions across the segment.

The pharmaceutical and healthcare segment is expected to be the fastest-growing end-use segment, driven by serialization mandates, track-and-trace regulations, and heightened focus on patient safety. Label applicators in this segment must support precise placement, variable-data printing, tamper-evident labeling, and real-time verification to ensure compliance with global regulatory frameworks. Applications span blister packs, bottles, vials, syringes, and secondary cartons.

Demand increasingly centers on validated, high-precision systems integrating printing, vision inspection, and audit-ready data capture. Capital expenditure for labeling equipment is often embedded within broader facility expansion or validation budgets, favoring suppliers with proven regulatory expertise and service capabilities. As pharmaceutical manufacturing expands in both developed and emerging markets, compliance-driven automation continues to accelerate the adoption of labeling systems.

Regional Market Insights

North America Label Applicators Market Trends - Automation Retrofits, Serialization Compliance, and E-Commerce Fulfillment

North America is expected to lead the market, with an anticipated share of approximately 34.7% in 2026, driven by early automation adoption, stringent regulatory oversight, and a well-developed packaging ecosystem. The U.S. is the dominant national market, supported by a large installed base of legacy labeling equipment across food, beverage, pharmaceutical, and logistics facilities, which is increasingly undergoing retrofitting, modernization, and replacement. Canada contributes through strong pharmaceutical and food-processing activity, while Mexico’s role has expanded through near-shoring manufacturing and cross-border supply chain integration.

Primary growth drivers include the rapid expansion of e-commerce fulfillment, rising regulatory scrutiny on labeling accuracy, and sustained investment in Industry 4.0 initiatives. Major food and beverage producers and third-party logistics providers are deploying automated print-and-apply and pallet labeling systems to improve throughput and traceability in distribution centers. Pharmaceutical manufacturers operating in the U.S. continue to invest in high-precision, serialized labeling solutions to meet track-and-trace requirements.

Favorable leasing and equipment financing models, combined with a strong aftermarket service and spare-parts ecosystem, further accelerate adoption. Ongoing consolidation among packaging equipment suppliers reflects growing demand for integrated labeling platforms that combine hardware, software, and compliance services under a single vendor relationship.

Europe Label Applicators Market Trends - Sustainability-Led Hospitality Consumption and Cork Supply Strength

Europe represents a mature yet innovation-driven regional market, anchored by Germany, the U.K., France, and Spain, where advanced manufacturing practices and regulatory harmonization sustain consistent demand for label applicators. The region benefits from a dense concentration of food, beverage, pharmaceutical, and personal care manufacturers that operate across multiple countries and require standardized, compliant labeling systems. Buyers in Europe place strong emphasis on precision engineering, system reliability, and compatibility with recyclable packaging materials.

Sustainability regulations and extended producer responsibility frameworks have driven widespread packaging redesign initiatives, directly influencing upgrades to labeling equipment. Manufacturers are increasingly investing in applicators capable of handling thinner label substrates, wash-off adhesives, and mono-material packaging formats. Pharmaceutical companies across Germany and France continue to prioritize validated labeling systems that support serialization and multilingual compliance.

In the U.K. and Southern Europe, modular retrofits and semi-automatic upgrades are common among mid-sized producers adapting to regulatory changes without full line replacement. As a result, demand in Europe is characterized by steady replacement cycles, technology-driven upgrades, and a strong preference for suppliers offering long-term service support and regulatory expertise.

Asia Pacific Label Applicators Market Trends - Export-Scale Manufacturing with Rapid Hospitality Expansion

Asia-Pacific is expected to be the fastest-growing regional market for label applicators, driven by rapid industrialization, expanding consumer markets, and increasing regulatory alignment across China, Japan, India, and the ASEAN economies. China remains the largest market in the region, supported by extensive food processing, pharmaceutical manufacturing, and export-oriented consumer goods production. Japan contributes through high-precision manufacturing and early adoption of advanced automation, while India and Southeast Asia are experiencing accelerating demand as production volumes scale and labor costs rise.

Manufacturers in the Asia Pacific are progressively transitioning from manual labeling toward semi-automatic and cost-optimized automatic applicators. In India and ASEAN countries, contract packers, nutraceutical producers, and domestic food brands are investing in semi-automatic systems to manage SKU proliferation and growing compliance requirements. Multinational consumer goods and pharmaceutical companies operating in China and Singapore are increasingly deploying fully automated, vision-enabled applicators to meet export-quality standards.

Localization of manufacturing by global equipment suppliers, along with regional distributor partnerships and service hubs, has improved affordability and reduced lead times. As a result, the Asia Pacific is emerging as both a high-growth demand center and a strategic manufacturing base for label applicator systems.

Competitive Landscape

The global label applicators market exhibits moderate concentration, combining global platform manufacturers serving high-speed, regulated applications with a long tail of regional and niche suppliers focused on semi-automatic and manual systems. Large players dominate integrated, validated solutions, while smaller firms retain strong positions in retrofits and localized markets.

Leading strategies emphasize solution integration, technology differentiation through vision and connectivity, and channel expansion via financing and regional manufacturing. Modular retrofits and recurring service models are increasingly central to competitive positioning.

Key Industry Developments:

- In April 2025, LemuGroup launched the Ultra Compact 3 end-of-line automation device, designed for resource-limited packaging operations, helping smaller producers adopt higher automation without extensive reconfiguration costs.

Companies Covered in Label Applicators Market

- Krones AG

- HERMA GmbH

- Markem-Imaje

- Domino Printing Sciences

- ProMach (ID Technology)

- Avery Dennison Corporation

- Sidel Group

- Accraply (Barry-Wehmiller)

- Weber Packaging Solutions

- Quadrel Labeling Systems

- Label-Aire, Inc.

- Fuji Seal International, Inc.

- Panther Industries, Inc.

- Newman Labelling Systems Ltd

- CTM Labeling Systems

- Nita Labeling Equipment

- Marchesini Group

- Sacmi Imola S.C.

Frequently Asked Questions

The global label applicators market is projected to be valued at US$3.4 billion in 2026.

The label applicators market is expected to reach US$4.8 billion by 2033.

The label applicators market is anticipated to grow at a CAGR of 4.9% between 2026 and 2033.

Key trends include increasing adoption of automatic and print-and-apply systems integrated with vision inspection and expansion of retrofit and modular upgrade solutions for mid-life production lines.

Automatic applicators represent the leading product segment, accounting for approximately 47.3% of market share, due to strong adoption in high-speed food, beverage, and pharmaceutical production lines.

Major companies include Krones AG, Herma GmbH, Markem-Imaje, Domino Printing Sciences, and ProMach.