- Processed Food

- Food Service Market

Food Service Market Size, Share, and Growth Forecast, 2025 - 2032

Food Service Market Service Type (Full-Service Dining, Fine Dining, Others), Cuisine Type (Traditional Cuisine, Local Cuisine, Others), Distribution Channel, End-user, and Regional Analysis for 2025 - 2032

Food Service Market Size and Trends Analysis

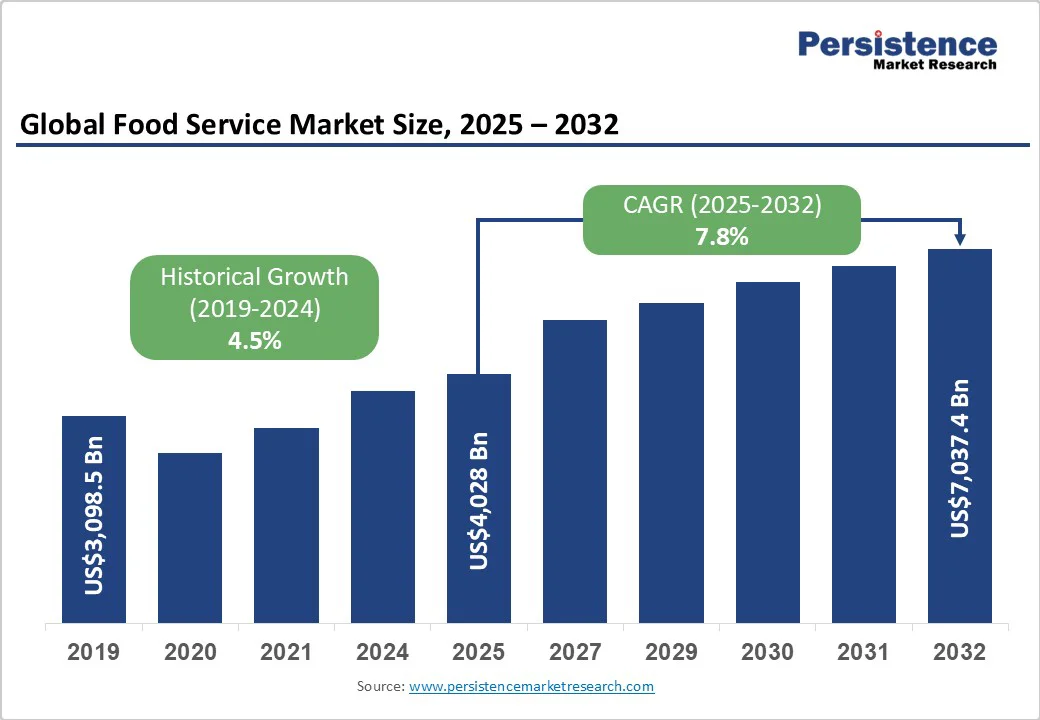

The global food service market size is likely to be valued at US$4,028 Bn in 2025 and is expected to reach US$7,037.4 Bn by 2032, growing at a CAGR of 7.8% during the forecast period from 2025 to 2032, driven by rising disposable incomes, rapid urbanization in emerging markets, accelerated adoption of online ordering and cloud kitchens, and the post-pandemic revival in dining-out behavior.

Technological transformation, expansion into emerging economies, and the shift toward healthier menu options present significant opportunity pathways. Overall, the market is poised for substantial expansion, supported by evolving consumer preferences and digital integration.

Key Industry Highlights

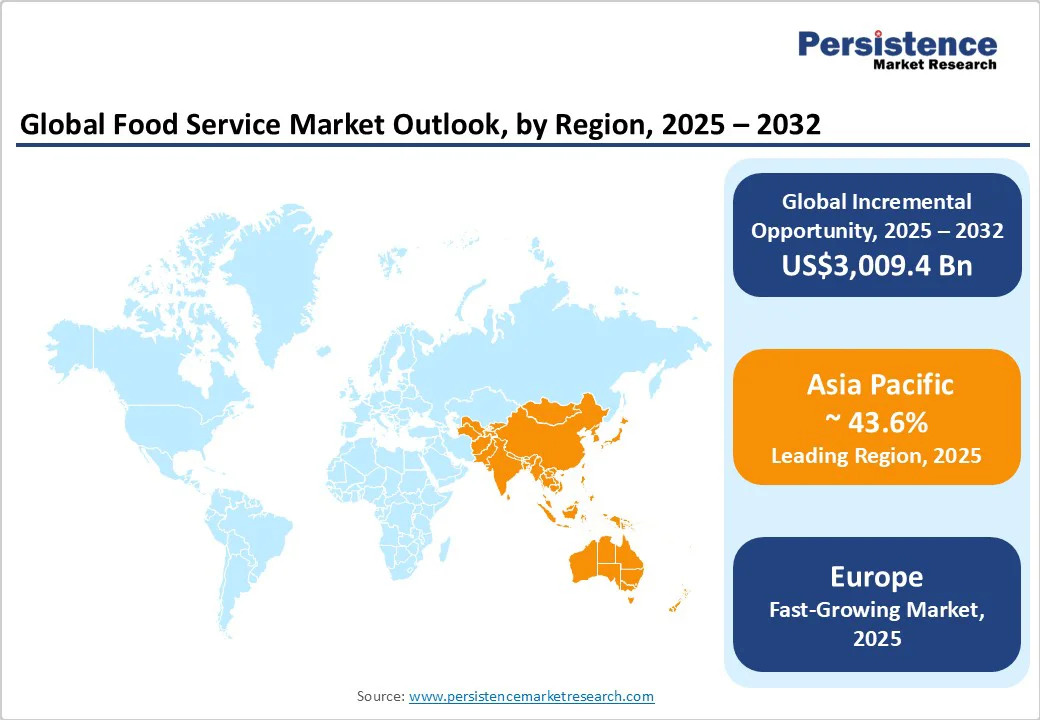

- Leading Region: Asia Pacific, accounting for 43.6% of the revenue share, driven by China, India, Japan, and ASEAN markets with high urbanization and digital adoption.

- The fastest-growing region is expected to be the Asia Pacific, driven

- by cloud kitchens, QSR expansion, and delivery platforms.

- Investment Plans: Expansion of cloud kitchens, AI-enabled kitchens, and delivery-first models, including Yum! Brands’ AI-powered KFC kitchens in Indonesia and the Philippines (2025) and Starbucks dark stores in China (2026).

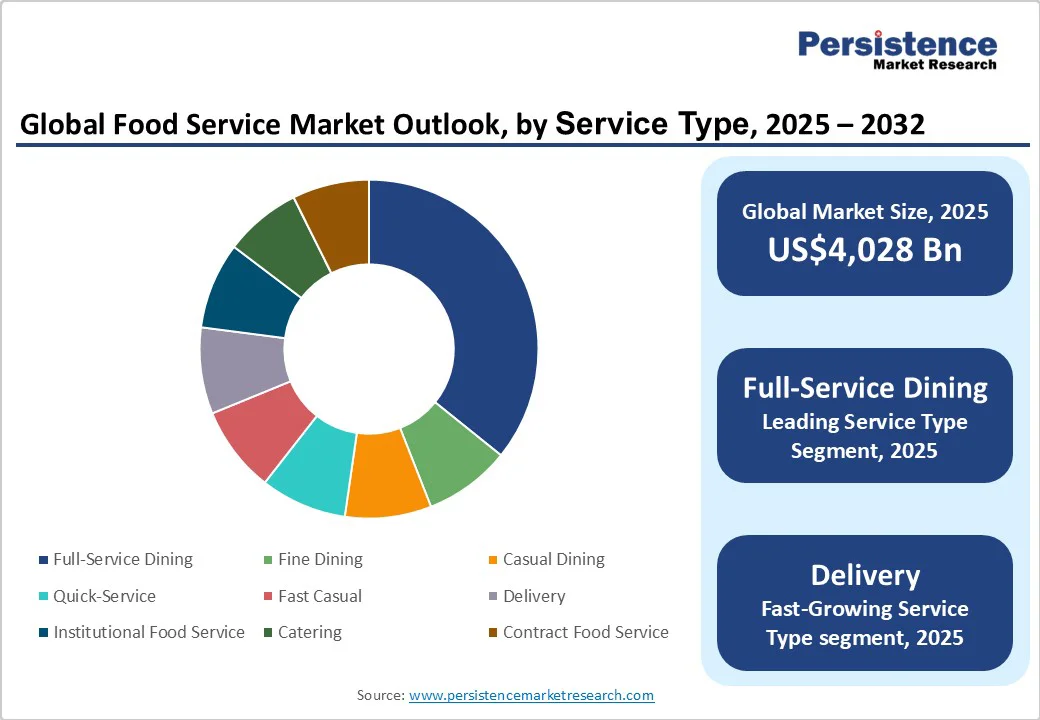

- Dominant Service Type: Full-Service Dining, accounting for approximately 38.4% of total market volume, benefiting from premium menus, experiential dining, and high repeat visits.

- Leading Cuisine Type: Traditional/Local Cuisine, representing 42.7% of total cuisine market share, driven by consumer preference for familiar flavors, regional specialties, and cultural dining experiences.

| Key Insights | Details |

|---|---|

|

Food Service Market Size (2025E) |

US$4,028 Bn |

|

Market Value Forecast (2032F) |

US$7,037.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising disposable incomes and urbanization in emerging markets

As middle-income households grow in Asia, Latin America, and Africa, out-of-home food consumption rises proportionally. Urbanization rates in China and India exceed 50% and continue to rise, driving increased demand for convenience dining and delivery services. Real per capita income growth in these markets has averaged 3–5% annually over the last decade. This demographic expansion directly drives demand for food services, particularly in tier-2 and tier-3 cities, increasing foot traffic in commercial districts, offices, and transit hubs.

Digital transformation, cloud kitchens, and online ordering proliferation

The rise of digital ordering platforms and cloud kitchens has improved operational efficiency and lowered market entry barriers. The adoption of AI, IoT, robotics, and automation in kitchen operations has enabled cost savings of 10–15% in some cases. This digital shift enables scalable growth in delivery and takeaway segments, enhances convenience, and fosters customer loyalty, positioning operators to capture a growing share of urban and digitally connected consumers.

Post-pandemic recovery and pent-up dining demand

The pandemic caused a sharp contraction in food service sales, with declines of nearly 30% in 2020. Expenditure rebounded post-pandemic, exceeding pre-pandemic levels by 2024. Consumer confidence in dining out, combined with increased capital expenditure for store refurbishments and expansion, is driving growth in experiential dining, themed restaurants, and international cuisines.

Barrier Analysis - Rising input costs and inflationary pressure

Food service margins are sensitive to fluctuations in raw materials, energy, and labor costs. Increases in commodity prices can erode operator margins by 2–3%. Smaller operators, lacking scale or hedging capabilities, are particularly exposed, which can constrain expansion and profitability.

Regulatory complexity and food safety compliance burdens

Operators face diverse food safety, health, labeling, and labor regulations across jurisdictions. Noncompliance risks fines, brand damage, or closure. Differences in international standards and import restrictions create operational challenges, which in turn raise barriers to entry and slow expansion in certain regions.

Opportunity Analysis - Expansion in underpenetrated emerging markets

Markets in Africa, Latin America, and Southeast Asia remain underpenetrated in modern food service offerings. Capturing even 1% of these emerging regions could represent a US$68 billion revenue opportunity by 2032. Localized menus, partnerships, and digital adoption are key to capitalizing on this potential.

Health, sustainability, and plant-based menu innovation

Consumers are increasingly opting for healthier, more sustainable, and plant-based options. Plant-based alternatives could account for 10–15% of food service menus by 2030, representing a multi-billion-dollar opportunity. Embedding sustainability initiatives also provides regulatory and branding advantages.

Vertical integration and supply chain platforms

Operators adopting central kitchens or platform-based supply chains can improve efficiency and margins while generating ancillary revenue. For example, servicing 10% of chain restaurants with a 1–2% take rate could yield US$1–2 billion in platform revenue, especially in fragmented supply chain markets.

Category-wise Analysis

Service Type Insights

The full-service dining segment is the largest within the service-type category, accounting for approximately 38.4% of total food service market volume in mature markets. This segment comprises fine dining and casual dining restaurants that provide table service, curated menus, and a comprehensive dining experience. Full-service establishments lead the market because they command higher per-visit spending, benefit from repeat patronage, and appeal to consumers seeking premium and immersive culinary experiences. Fine dining, for example, allows restaurants to differentiate through ambiance, chef-led menus, and exclusive offerings, while casual dining focuses on family-friendly or social dining experiences. A key example is The Cheesecake Factory in the U.S., which combines a broad menu with experiential dining to maintain a loyal customer base and strong revenue generation.

The fastest-growing segment is delivery, fueled by increasing smartphone penetration, urban lifestyles that prioritize convenience, and the expansion of digital platforms and cloud kitchens. Delivery-focused operators benefit from lower overhead costs compared to full-service locations, as they can operate from smaller, less expensive spaces while reaching a wide customer base through aggregator apps. Rebel Foods in India, which operates multiple cloud kitchen brands, exemplifies this trend by using technology-driven operations to scale delivery services across urban areas efficiently.

Cuisine Type Insights

Within the cuisine category, traditional/local cuisine remains the largest segment, representing approximately 40–45% of the total market share. This segment is dominant because consumers tend to favor familiar flavors and culturally significant dishes, especially in markets such as Asia and Europe where regional cuisine is deeply embedded in daily life. Restaurants offering local specialties often enjoy strong brand loyalty and repeat visits as they cater to both residents and tourists seeking authentic culinary experiences. For instance, Din Tai Fung in Taiwan has successfully scaled by focusing on traditional dumplings and local flavors while maintaining quality and consistency, which strengthens its market position.

The fastest-growing segment in cuisine type is health & wellness/plant-based options, projected to achieve a CAGR of 7–9% between 2025 and 2032. Growth is driven by rising health awareness, dietary restrictions, and sustainability concerns among consumers. Plant-based and wellness-focused menus appeal to a younger demographic that values ethical sourcing, low-calorie options, and foods that boost immunity. International brands such as Just Salad in the U.S. have leveraged this trend by offering fully customizable, health-focused meals, which attract repeat visits and foster brand differentiation. Governments and health agencies promoting nutrition awareness have reinforced the adoption of these menus, further accelerating market growth.

Regional Insights

Asia Pacific Food Service Market Trends - Rapid Expansion via Cloud Kitchens and Digital Innovation

Asia Pacific is the fastest-growing and largest regional contributor, accounting for 43.6% of global food service revenue. Asia Pacific represents the most dynamic and rapidly expanding region in the global food service industry. Growth is driven by large and increasingly urban populations in countries such as China, India, Japan, and members of the ASEAN bloc. Rising disposable incomes, evolving consumer preferences, and high digital penetration are fueling the adoption of QSR, fast casual, and cloud kitchen formats. Operators are leveraging technology to scale delivery services, implement loyalty programs, and optimize operations.

Recent developments include the rapid expansion of cloud kitchen platforms in cities like Shanghai, Mumbai, and Jakarta, enabling faster delivery and reduced real estate costs. Global chains such as Starbucks and Yum! Brands are increasing investments in tier-2 and tier-3 cities, while local players focus on app-based ordering and innovative menu customization. Partnerships between food delivery aggregators and restaurant operators have grown significantly, and investment in AI-powered predictive demand systems and automated kitchen technologies is accelerating, reflecting the region’s emphasis on innovation and operational scalability.

North America Food Service Market Trends - Tech-Driven Growth in a Mature, Brand-Dominant Market

The North America food service market is characterized by a mature and highly developed ecosystem. Growth is primarily driven by high disposable incomes, a strong culture of dining out, and widespread adoption of digital technologies that facilitate online ordering, loyalty programs, and delivery services. Major players such as McDonald’s, Starbucks, and Yum! Brands continue to dominate the landscape, leveraging brand recognition and operational scale. Regulatory frameworks emphasize food safety, labeling, and transparency, which enhances consumer trust but also requires ongoing compliance investments.

Recent developments include the expansion of cloud kitchen networks by QSR chains and the integration of AI-driven supply chain management systems to optimize inventory and reduce waste. Private equity investment has supported the rollout of automation technologies in kitchens and point-of-sale systems, while partnerships with delivery platforms have expanded last-mile reach. Innovations such as contactless ordering, smart kitchen appliances, and personalized digital marketing campaigns are increasingly shaping consumer experiences in both urban and suburban areas.

Europe Food Service Market Trends - Sustainability, Dark Kitchens, and Regulatory Harmonization

Europe’s food service landscape is diverse, with operations spread across the UK, Germany, France, Spain, and Italy. Harmonized EU regulations on food safety, allergen disclosure, and labeling support cross-border expansion and operational standardization. Growth is moderate, influenced by high labor costs and relatively saturated urban markets, but opportunities are emerging in niche segments such as plant-based and sustainable dining, premium casual restaurants, and subscription meal plans. Leading chains such as Elior Group, Compass Group, and Sodexo operate alongside strong domestic players, benefiting from consolidated distribution networks and scale efficiencies.

Recent developments include the launch of delivery-first dark kitchens in major cities like London and Berlin, as well as digital menus and mobile ordering platforms enhancing customer engagement. Sustainability initiatives, such as zero-waste programs and local sourcing commitments, are increasingly influencing consumer choices. Investment in technology for predictive demand forecasting and waste reduction has also become a priority for European operators seeking to improve profitability and maintain compliance with environmental standards.

Competitive Landscape

The global food service market is moderately consolidated at the top, with leading players controlling 20–30% of revenues in mature markets. Globally, many local operators contribute to a fragmented landscape. Competitive positioning is influenced by scale, supply chain control, brand equity, and technological adoption.

Leading operators prioritize technology-driven efficiency, cost leadership, and geographic expansion. Differentiation strategies include proprietary supply chains, menu innovation, omnichannel delivery, and emerging models like kitchen-as-a-service platforms.

Key Industry Developments

- In July 2025, DoorDash partnered with regional restaurant chains in the U.S. to launch virtual kitchens, enhancing delivery speed and operational scalability for small and mid-sized food service operators.

- In May 2025, Compass Group announced a sustainable sourcing initiative across the UK and Germany, integrating plant-based and locally sourced menu options to strengthen corporate and institutional catering services.

- In January 2025, Yum! Brands launched AI-enabled KFC cloud kitchens in Indonesia and the Philippines to improve delivery efficiency and reduce operational costs, targeting rapid expansion in tier-2 and tier-3 cities.

Companies Covered in Food Service Market

- Compass Group plc

- Sodexo SA

- Aramark Corporation

- Yum! Brands, Inc.

- McDonald’s Corporation

- Starbucks Corporation

- Restaurant Brands International

- Domino’s Pizza, Inc.

- Delaware North

- Elior Group

- Darden Restaurants, Inc.

- Chipotle Mexican Grill, Inc.

- Jollibee Foods Corporation

- Burger King

- Just Salad

- Rebel Foods

- DoorDash Kitchens

- Shake Shack, Inc.

- Pret A Manger

- Kitchen United

Frequently Asked Questions

The market size is estimated at US$4,028 Billion in 2025.

The food service market is projected to reach US$7,037.4 Billion by 2032.

Key trends include the growth of cloud kitchens and delivery-first models and the increasing adoption of AI and digital ordering platforms.

Full-Service Dining is the largest segment, accounting for approximately 38.4% of total market volume, driven by premium menus, repeat visits, and experiential dining.

The food service market is expected to grow at a CAGR of 7.8% from 2025 to 2032.

Major players include Compass Group plc, Sodexo SA, Yum! Brands, Inc., McDonald’s Corporation, and Starbucks Corporation.