- Processed Food

- Food and Beverage Disinfection Market

Food and Beverage Disinfection Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Food and Beverage Disinfection Market by Product (Chemical Disinfectants, UV Disinfection Equipment, Ozone Disinfection Systems, and Others), by Method (Chemical and Physical), by System Type (Manual Systems, Semi-Automatic Systems, and Automatic Systems) Application (Surface Disinfection, Packaging Disinfection, Food Processing Equipment Disinfection, and Others) End-user (Food Industry, Beverage Industry, and Others), and Regional Analysis from 2026 - 2033

Food and Beverage Disinfection Market Share and Trend Analysis

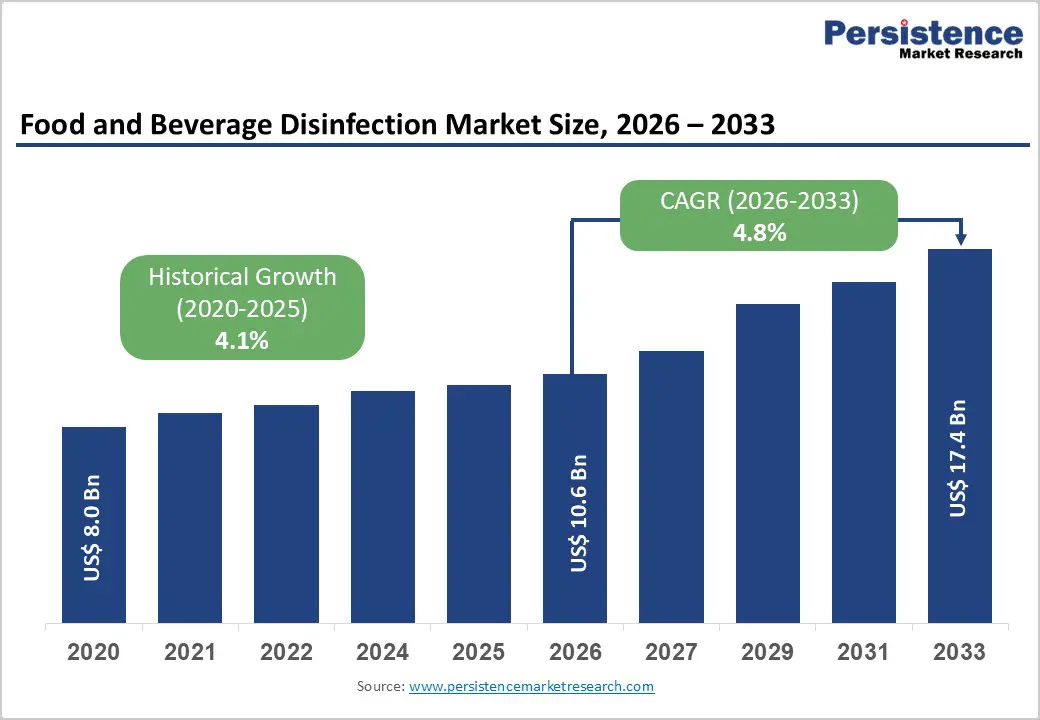

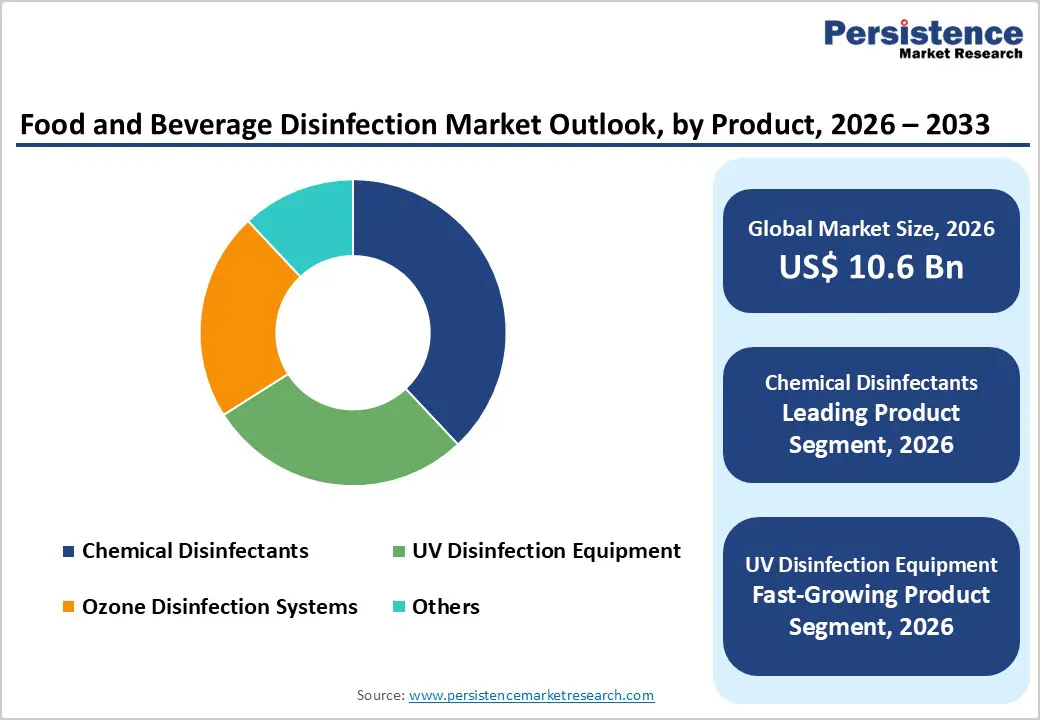

The global food and beverage disinfection market size is estimated to grow from US$ 10.6 billion in 2026 to US$ 17.4 billion by 2033. The market is projected to record a CAGR of 4.8% during the forecast period from 2026 to 2033. Global demand for food and beverage disinfection solutions is steadily rising, driven by tightening food safety regulations, increasing focus on contamination control, and heightened awareness of hygiene standards across processing environments. Manufacturers are actively investing in advanced disinfection technologies to minimize microbial risks, extend shelf life, and ensure regulatory compliance without compromising operational efficiency.

Expanding food processing capacity, growing packaged food consumption, and rising export requirements are supporting sustained market growth. Higher incidence of foodborne illness outbreaks, stricter sanitation audits, and increasing preference for automated and residue-free disinfection solutions are further accelerating adoption. In addition, increasing capital expenditure on smart manufacturing, greater integration of automated sanitation systems, and broader implementation of clean-in-place (CIP) and clean-out-of-place (COP) protocols are enabling wider uptake across developed and emerging markets. Continuous innovation in chemical formulations, UV system efficiency, ozone generation technologies, and automated dosing mechanisms is improving efficacy, safety, and cost optimization. The growing emphasis on preventive contamination control, sustainable processing, and digitally monitored hygiene systems is further propelling global demand for food and beverage disinfection solutions.

Key Industry Highlights:

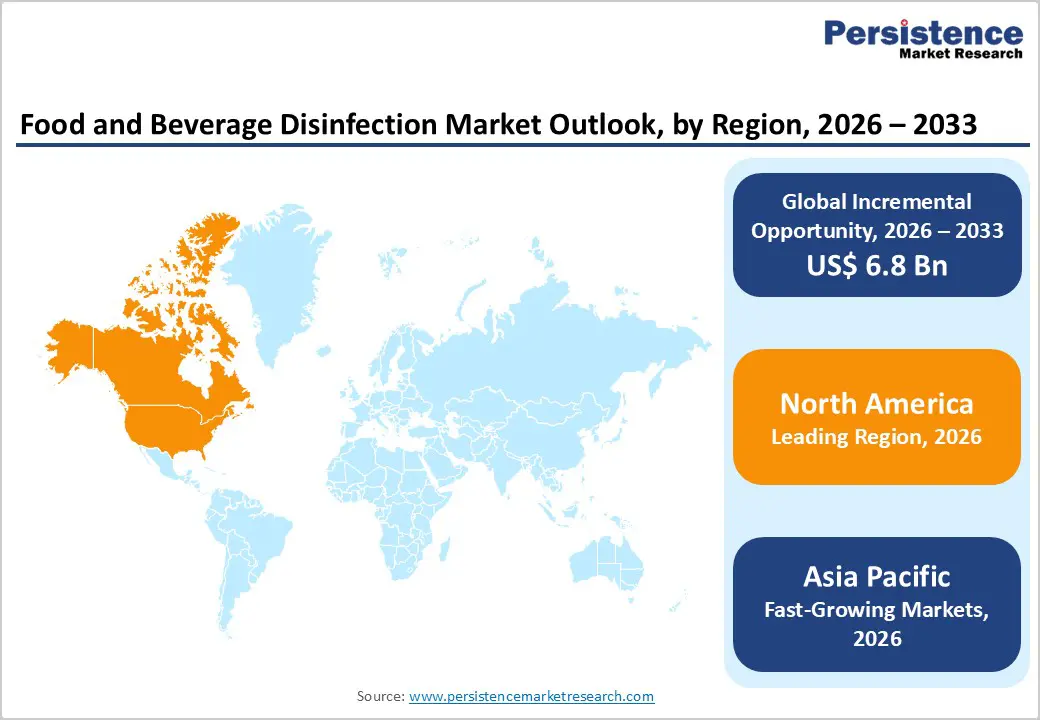

- Leading Region: North America holds the largest share at 46.7%, supported by stringent FDA and USDA food safety regulations, high automation penetration in processing facilities, strong adoption of advanced sanitation technologies, and the presence of leading disinfection solution providers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid food processing industrialization, rising packaged food consumption, tightening regulatory enforcement, increasing export-oriented manufacturing, and expanding investment in automated sanitation infrastructure.

- Leading Product Segment: Chemical disinfectants dominate the market due to broad-spectrum antimicrobial efficacy, cost-effectiveness, ease of application across diverse surfaces, and established regulatory approvals for food-contact environments.

- Fastest-Growing Product Segment: UV disinfection equipment is expanding rapidly as demand grows for non-chemical, residue-free, and environmentally sustainable disinfection technologies across processing and packaging lines.

- Leading System Type Segment: Manual systems remain the top segment, driven by lower capital investment requirements, flexibility in small- and mid-scale processing units, and widespread usage across emerging markets.

- Fastest-Growing System Type Segment: Automatic systems are scaling quickly as food manufacturers increasingly adopt automated, sensor-integrated, and CIP-compatible solutions to improve sanitation consistency, reduce labor dependency, and enhance compliance efficiency.

| Key Insights | Details |

|---|---|

|

Food and Beverage Disinfection Market Size (2026E) |

US$ 10.6 Bn |

|

Market Value Forecast (2033F) |

US$ 17.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.8 % |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1 % |

Market Dynamics

Driver - Tightening Food Safety Regulations and Rising Contamination Control Standards

Rise in regulatory oversight across global food processing industries is significantly accelerating demand for advanced disinfection solutions. Governments and food safety authorities are strengthening microbial control mandates, traceability requirements, and sanitation validation protocols to reduce foodborne illness outbreaks and cross-contamination risks. Regulatory frameworks such as HACCP, FSMA, and EU hygiene directives are compelling manufacturers to adopt validated, high-efficacy disinfection technologies across production lines, storage facilities, and packaging environments. As supply chains become more globalized, exporters must meet stringent international sanitation benchmarks, further reinforcing investment in reliable and standardized disinfection systems.

Simultaneously, growing consumer sensitivity toward food safety incidents has increased reputational risk for food and beverage brands. Even isolated contamination events can result in recalls, financial penalties, and long-term brand erosion. This has shifted sanitation from a compliance function to a strategic operational priority. Rising automation in food processing facilities also supports the adoption of integrated UV, ozone, and automated chemical dosing systems that ensure consistent microbial reduction while minimizing labor variability. Additionally, expansion in ready-to-eat, minimally processed, and high-moisture food categories demands more robust disinfection frameworks to maintain shelf stability and pathogen control. Collectively, regulatory tightening, export pressures, and consumer scrutiny are reinforcing sustained capital expenditure in modern food and beverage disinfection infrastructure worldwide.

Restraint - High Capital Investment, Chemical Residue Concerns, and Operational Complexity

Despite strong demand fundamentals, several structural challenges moderate market expansion. Advanced disinfection technologies such as automated UV tunnels, ozone generation systems, and sensor-integrated CIP platforms require substantial upfront capital expenditure. Small and mid-scale processors, particularly in developing economies, often face budgetary constraints that delay modernization initiatives. Beyond equipment costs, installation, validation, and employee training add to total ownership expenditure.

Operational complexity also presents hurdles. Maintaining optimal dosage levels, exposure times, and system calibration is critical to ensure microbial efficacy without compromising product integrity. Improper chemical concentration can lead to residue risks, corrosion of equipment, or non-compliance with permissible exposure thresholds. Increasing scrutiny regarding environmental discharge and worker safety standards further complicates chemical disinfectant usage. In addition, variability in raw material loads, organic matter presence, and surface types can reduce disinfection efficiency, requiring tailored protocols rather than standardized solutions.

There is also growing industry focus on sustainability, leading some processors to reconsider chlorine-based formulations due to by-product formation and wastewater management challenges. Navigating regional regulatory differences, validation documentation requirements, and evolving microbial testing standards adds administrative burden. These constraints collectively necessitate continuous technical upgrades, skilled workforce training, and process optimization, potentially slowing rapid adoption across cost-sensitive segments.

Opportunity - Automation Integration, Sustainable Technologies, and Smart Sanitation Systems

Technological evolution and sustainability imperatives are unlocking substantial long-term growth avenues. Increasing integration of Industry 4.0 frameworks within food processing plants is creating demand for digitally monitored disinfection systems capable of real-time performance tracking, automated dosing adjustments, and predictive maintenance alerts. Smart sanitation platforms linked to centralized monitoring dashboards enhance traceability, documentation accuracy, and audit readiness, strengthening regulatory compliance efficiency.

There is a significant opportunity in expanding non-chemical and low-residue technologies such as UV-C irradiation, advanced oxidation processes, electrolyzed water systems, and ozone-based surface treatment. These solutions align with environmental sustainability goals by reducing chemical discharge and minimizing water consumption. Energy-efficient designs and modular installations further improve scalability for both large enterprises and emerging market processors. Growth in high-value categories, including dairy alternatives, ready-to-eat meals, functional beverages, and export-oriented packaged foods, requires advanced packaging and surface disinfection technologies to preserve shelf life and ensure pathogen mitigation.

Emerging markets undergoing rapid food processing industrialization present untapped demand for automated sanitation infrastructure. Additionally, rising adoption of contract manufacturing and centralized mega-processing facilities increases the need for standardized, high-capacity disinfection systems. As sustainability, digitalization, and food safety converge, innovation-driven sanitation technologies are positioned to capture sustained investment momentum.

Category-wise Analysis

By Product Insights

The chemical disinfectants segment is projected to dominate the global food and beverage disinfection market in 2026, capturing a revenue share of 38.0%. Its leadership is primarily attributed to proven antimicrobial effectiveness across a wide range of pathogens, including bacteria, viruses, molds, and spores. Chlorine compounds, peracetic acid, hydrogen peroxide, and quaternary ammonium formulations are widely adopted due to regulatory approvals and compatibility with diverse food-contact surfaces. These solutions are extensively used in clean-in-place (CIP) systems, equipment sanitation, water treatment, and facility hygiene protocols. Chemical disinfectants offer scalability and operational flexibility, making them suitable for both large industrial processors and mid-sized facilities. Their relatively lower capital investment compared to advanced UV or ozone systems further strengthens adoption, particularly in cost-sensitive regions. Additionally, established supplier networks and standardized dosing protocols simplify integration into existing sanitation workflows. Continuous improvements in residue management, corrosion control, and environmentally optimized formulations are further reinforcing segment dominance globally.

By Application

The surface disinfection segment is expected to lead the global food and beverage disinfection market in 2026, accounting for a 38.0% revenue share. This dominance stems from the essential role of surface hygiene in preventing cross-contamination during food handling, processing, and packaging. High-touch areas such as conveyor belts, cutting tools, storage containers, preparation tables, and contact surfaces require frequent and validated sanitation to comply with HACCP and food safety standards.

Surface disinfection is prioritized because contamination at these control points can directly compromise product safety and trigger costly recalls. Manufacturers implement routine sanitation cycles, automated spraying systems, and foam-based chemical applications to ensure microbial reduction. The growth of ready-to-eat foods, fresh produce processing, and minimally processed beverages further elevates the importance of surface-level microbial control. Additionally, audit requirements and traceability documentation emphasize consistent sanitation performance. As production volumes expand globally, surface disinfection remains the most critical and consistently applied hygiene intervention across facilities.

By End-user

The food industry is projected to dominate the global food and beverage disinfection market in 2026, capturing a 60.0% revenue share. This leadership reflects the extensive sanitation requirements across meat, poultry, dairy, bakery, confectionery, and ready-to-eat food processing facilities. Food production environments involve multiple contamination risk points, including raw material handling, thermal processing, cooling, slicing, and packaging operations. Stringent microbial safety thresholds, frequent inspections, and export-driven compliance standards necessitate continuous disinfection practices. High processing volumes and diversified product portfolios further increase sanitation frequency compared to beverage-only facilities. The industry’s expansion into convenience foods, plant-based alternatives, and minimally processed categories also intensifies hygiene demands. In addition, large food manufacturers invest heavily in automated sanitation technologies to minimize downtime and ensure consistent microbial control. These structural and regulatory factors collectively sustain the food industry’s dominant contribution to overall market revenue.

Regional Insights

North America Food and Beverage Disinfection Market Trends

North America is expected to dominate the global food and beverage disinfection market in 2026, accounting for a 46.7% value share, led primarily by the United States. The region benefits from highly stringent food safety regulations enforced by agencies such as the FDA and USDA, which mandate validated sanitation protocols across processing environments. Strong awareness of contamination risks and low tolerance for foodborne illness outbreaks have pushed manufacturers to adopt advanced chemical and non-chemical disinfection systems.

The presence of large-scale food processors, integrated supply chains, and export-oriented production facilities further supports consistent demand. High automation penetration within North American plants encourages the adoption of UV tunnels, ozone treatment systems, and automated CIP solutions. Robust infrastructure, including cold-chain logistics and centralized processing hubs, strengthens operational efficiency and sanitation consistency. Additionally, substantial capital investment capacity enables rapid technology upgrades and compliance modernization. Continuous innovation, coupled with proactive regulatory enforcement and a strong food safety culture, reinforces North America’s sustained leadership position in the global market.

Europe Food and Beverage Disinfection Market Trends

Europe’s food and beverage disinfection market is expected to grow steadily in 2026, supported by strict hygiene regulations under the European Food Safety Authority (EFSA) framework and national enforcement bodies. Countries including Germany, France, the U.K., Italy, and the Netherlands maintain rigorous sanitation audits and compliance standards across food production facilities. The region emphasizes preventive contamination control, traceability, and environmental sustainability in sanitation practices.

European manufacturers are increasingly adopting low-residue disinfectants, ozone-based systems, and energy-efficient UV technologies to align with sustainability objectives and wastewater management regulations. Rising exports of dairy, processed meat, bakery, and ready meals necessitate adherence to global food safety benchmarks. Additionally, modernization of legacy processing plants is driving upgrades to automated sanitation systems and digital monitoring platforms. Strong focus on worker safety and chemical exposure standards further shapes product selection. These factors collectively ensure stable and compliance-driven expansion across the European market.

Asia Pacific Food and Beverage Disinfection Market Trends

The Asia Pacific food and beverage disinfection market is projected to register a higher CAGR of around 6.6% between 2026 and 2033, driven by the rapid industrialization of food processing sectors across China, India, Japan, and Southeast Asia. Expanding urban populations and rising packaged food consumption are increasing production volumes, thereby intensifying sanitation requirements. Governments are progressively strengthening food safety regulations following high-profile contamination incidents, encouraging processors to adopt standardized disinfection systems.

Growing foreign direct investment in food manufacturing and the establishment of export-oriented mega processing zones are accelerating infrastructure upgrades. Multinational companies operating in the region implement global hygiene standards, stimulating demand for automated and validated sanitation technologies. Increased awareness among local manufacturers regarding HACCP compliance and microbial risk mitigation further contributes to adoption. Additionally, improving access to advanced equipment suppliers and technical training programs enhances implementation efficiency. These combined dynamics position Asia Pacific as the fastest-growing regional market globally.

Competitive Landscape

The global food and beverage disinfection market remains highly competitive, with strong participation from Advanced UV Inc., Zenith Hygiene Group plc., Evonik Industries AG, Solvay, and FINK TEC GmbH. These companies capitalize on established distribution networks, long-standing partnerships with food processors, and deep technical expertise in both chemical and non-chemical sanitation technologies. Competitive strength is reinforced through ongoing innovation in UV-C systems, advanced oxidation technologies, specialty disinfectant chemistries, and automated dosing platforms aligned with evolving food safety regulations.

Heightened regulatory oversight and increasing foodborne contamination risks continue to drive technological upgrades across processing facilities. Manufacturers are prioritizing high-efficacy antimicrobial formulations, sustainable and low-residue solutions, and energy-efficient UV and ozone systems. Strategic R&D investments focus on enhancing microbial validation, automation integration, and digital monitoring capabilities, while expansion into emerging markets and collaboration with large-scale processors support scalable and compliant sanitation deployment globally.

Key Developments:

- In September 2025, Ecolab Inc. introduced its new Ecolab® CIP IQ™ solution at Drinktec 2025, a digital clean-in-place (CIP) system engineered to enhance operational efficiency while lowering water consumption in food and beverage manufacturing facilities. The AI-enabled platform, developed in collaboration with 4T2 Sensors, incorporates advanced fluid sensing capabilities into Ecolab’s existing 3D TRASAR™ sensor technology to deliver real-time monitoring and optimized sanitation performance.

- In July 2025, Truelink Capital announced the successful completion of its acquisition of Zep, Inc., a producer of maintenance, cleaning, and sanitation solutions serving food and beverage, industrial, commercial, and residential markets. The company was acquired from affiliates of New Mountain Capital.

- In July 2023, Nuvonic, a global provider of UV technology solutions, introduced the UVpro FMT (Flange Module Tank) UVC disinfection system designed for air and surface treatment within storage tanks. This advanced solution enhances hygiene control and operational safety in tank environments across multiple industries, including food and beverage processing.

- In November 2022, Goodway Technologies expanded its international presence by establishing a new office in Düsseldorf, Germany, strengthening its reach within Europe’s food and beverage sector. This expansion enhances the company’s ability to provide localized technical support, faster service response, and closer collaboration with regional food processors and manufacturing partners.

Companies Covered in Food and Beverage Disinfection Market

- Advanced UV Inc.

- Zenith Hygiene Group plc.

- Evonik Industries AG

- Solvay

- FINK TEC GmbH

- Halma plc

- Trojan Technologies Group ULC.

- SUEZ

- Xylem

- Solenis

- Alfaa UV.

- ULTRAAQUA

- PROQUIMIA S.A.

- ProMinent

- Endo Enterprises (UK) Ltd

- Reza Hygiene

- Others

Frequently Asked Questions

The global food and beverage disinfection market is projected to be valued at US$ 10.6 Bn in 2026.

Stringent food safety regulations, rising foodborne contamination risks, expanding processed food production, and increasing adoption of automated sanitation systems drive market growth.

The global food and beverage disinfection market is poised to witness a CAGR of 4.8%between 2026 and 2033.

Key opportunities lie in smart automated disinfection systems, sustainable and residue-free technologies, expansion in emerging processing hubs, and integration of digital monitoring solutions.

Advanced UV Inc., Zenith Hygiene Group plc., Evonik Industries AG, Solvay, and FINK TEC GmbH are some of the key players in the food and beverage disinfection market.