- Processed Food

- Allergen-Free Food Market

Allergen-Free Food Market Size, Share, and Growth Forecast 2026 - 2033

Allergen-Free Food Market by Product Type (Chocolate, Beverages, Processed Meat and Poultry, Others), Nature (Organic, Conventional), by Claim (Sugar-Free, GMO-Free, Others), by Sales Channel, Regional Analysis, from 2026 - 2033

Allergen-Free Food Market Share and Trends Analysis

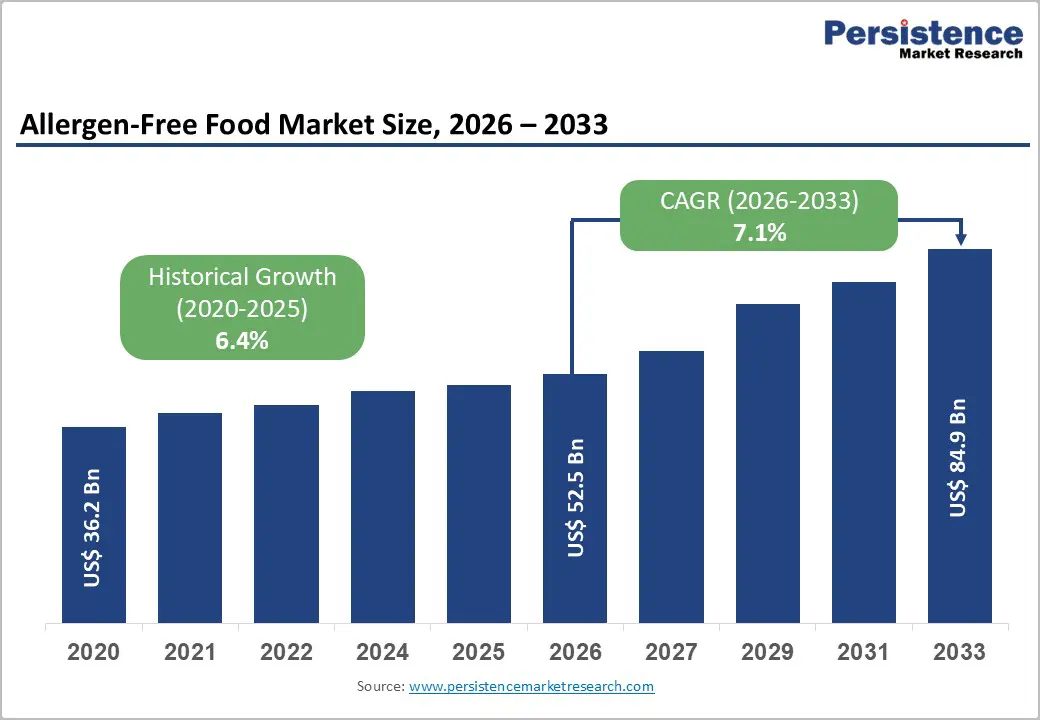

The global allergen-free food market size is expected to be valued at US$ 52.5 billion in 2026 and projected to reach US$ 84.9 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

The market is gaining strong momentum as food allergies and intolerances continue to rise globally, prompting consumers to actively seek products free from common allergens such as dairy, nuts, soy, eggs, and gluten. Regulatory agencies and health organizations have increased awareness around allergen risks and labeling transparency, encouraging manufacturers to reformulate products and launch certified allergen-free ranges. Advances in food processing, clean-label trends, and plant-based diets are further shaping product innovation. Retail expansion, e-commerce penetration, and premium positioning also influence purchasing behavior, making allergen-free foods a rapidly evolving and increasingly mainstream category.

Key Industry Highlights:

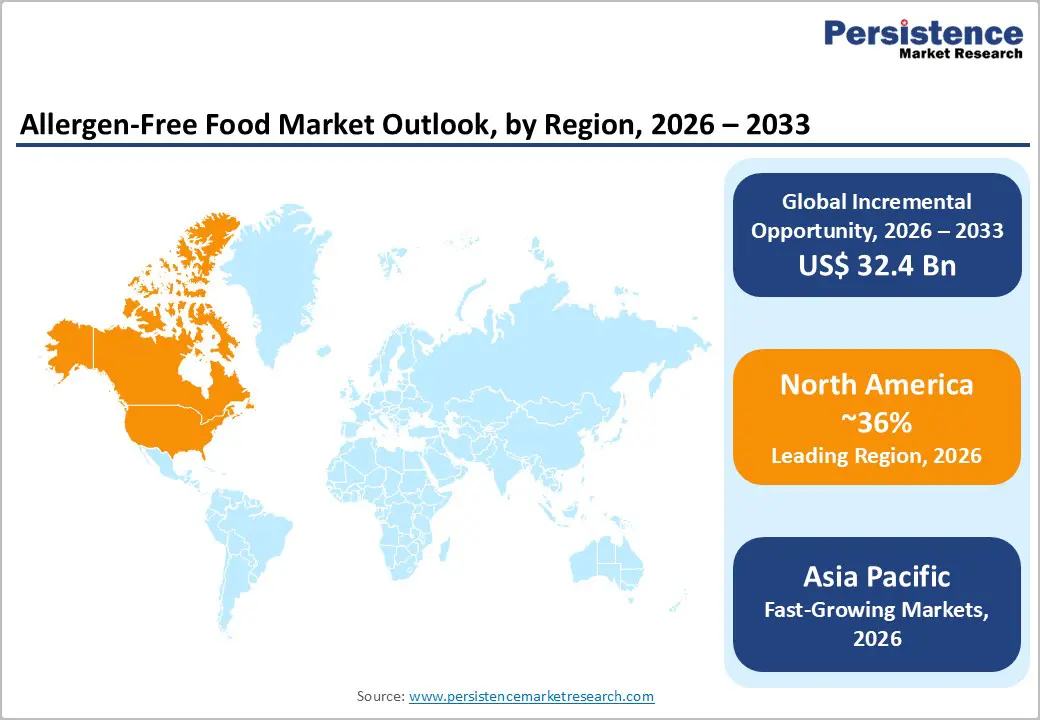

- Leading Region: North America leads the allergen-free food market, supported by high diagnosis rates of food allergies, strict labeling regulations, strong retail penetration, and widespread consumer awareness of dietary safety.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by urbanization, rising disposable incomes, expanding modern retail, growing health consciousness, and increasing adoption of clean-label packaged foods.

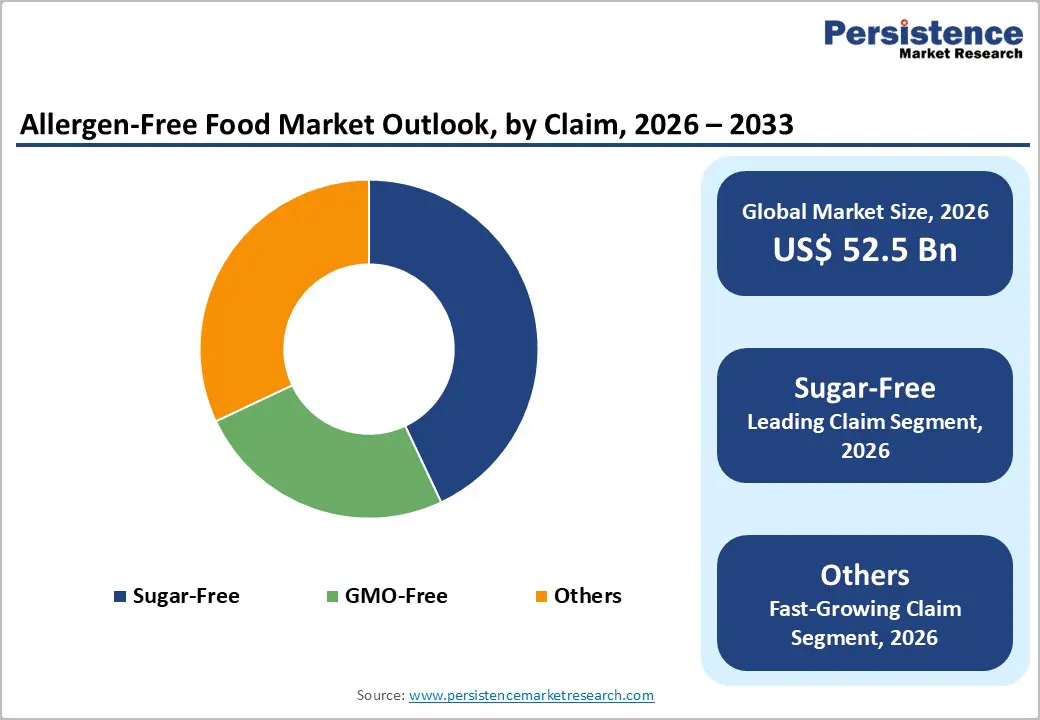

- Dominant Segment: Sugar-free products dominate the market due to rising diabetes prevalence, weight-management focus, clean-label preferences, and compatibility with allergen-free dietary needs across multiple food categories.

- Fastest Growing Segment: Organic are the fastest-growing segments, driven by clean-label demand, natural ingredient preferences, sustainability concerns, and rising health-conscious consumer adoption.

| Key Insights | Details |

|---|---|

|

Allergen-Free Food Market Size (2026E) |

US$ 52.5 billion |

|

Market Value Forecast (2033F) |

US$ 84.9 billion |

|

Projected Growth CAGR (2026-2033) |

7.1% |

|

Historical Market Growth (2020-2025) |

6.4% |

Market Dynamics

Driver - Rising Food Allergy Prevalence & Regulatory Push

Food allergies are increasingly recognized as a major public health concern, particularly in developed economies where clinical diagnosis rates and consumer awareness are high. Studies in Western countries suggest that roughly one in ten children is affected by food allergies, while U.S. public health authorities have reported steady growth in peanut and tree-nut sensitivities over the past decade. This expanding patient base is encouraging households to proactively avoid risk ingredients, driving routine purchases of certified allergen-free packaged foods rather than occasional specialty items. Parents, schools, airlines, and healthcare facilities are also strengthening procurement standards, further broadening institutional demand.

Regulatory intervention reinforces this growth momentum. Mandatory disclosure rules such as the U.S. Food Allergen Labeling and Consumer Protection Act and harmonized European labeling frameworks require manufacturers to clearly identify major allergens on packaging. These policies improve transparency, reduce accidental exposure risks, and build consumer confidence in certified products. Together, rising prevalence and strict compliance requirements are reshaping mainstream food portfolios, pushing multinational brands and private labels alike to expand allergen-free ranges across snacks, bakery, beverages, and ready-to-eat meals.

Restraints - Premium Pricing & Limited Awareness in Developing Regions

Despite rising demand, higher production costs continue to restrain wider market penetration. Allergen-free formulations rely on specialized raw materials, segregated manufacturing lines, extensive cleaning protocols, and third-party certification audits, often resulting in retail prices 20–50% above conventional equivalents. In price-sensitive markets, this premium limit trial purchases and repeat consumption, keeping allergen-free foods concentrated among affluent urban consumers. Taste and texture replication also remains technically challenging for certain categories, particularly bakery and dairy alternatives, causing some shoppers to perceive inferior sensory quality compared with traditional products.

In emerging economies, awareness gaps further constrain adoption. Diagnosis rates for food allergies remain comparatively low in parts of Asia, Africa, and Latin America, partly due to limited access to allergy specialists and underreporting in public health systems. Without strong educational campaigns or regulatory emphasis on allergen disclosure, many consumers underestimate dietary risks. This reduces urgency to pay higher prices for allergen-free foods, delaying category expansion until healthcare outreach, labeling enforcement, and nutrition literacy improve at the population level.

Opportunity - Plant-Based Innovation & Expansion in Emerging Markets

Rapid innovation in plant-based and fermentation-derived ingredients is creating major growth avenues for allergen-free food manufacturers. Many vegan formulations naturally avoid dairy, eggs, and other common allergens, aligning with both ethical consumption and medical dietary needs. Advances in precision fermentation and cell-free protein production are enabling manufacturers to replicate milk proteins or egg functionality without traditional animal sources, improving taste, texture, and baking performance. These technologies are attracting investment across Europe and North America, supporting premium product launches in cheeses, yogurts, desserts, and nutritional beverages while strengthening clean-label and organic positioning.

Geographic expansion represents another high-potential opportunity. Asia Pacific is emerging as the fastest-growing region, supported by urbanization, rising disposable incomes, and increasing health consciousness among middle-class consumers in China, India, and Southeast Asia. Government campaigns promoting clean-label foods and sugar-reduction initiatives are indirectly benefiting allergen-free categories. As modern retail chains and e-commerce platforms widen distribution, companies that localize pricing, flavors, and ingredient sourcing can secure early leadership in these high-CAGR markets.

Category-wise Analysis

By Product Type Insights

Chocolate occupies a leading position within the allergen-free food market because it successfully combines indulgence with safety-driven consumption. Frequent chocolate intake across age groups makes it one of the first categories where allergy-affected households seek certified alternatives, especially for children and gifting occasions. Manufacturers have aggressively reformulated portfolios to remove milk solids, nuts, gluten, and soy derivatives while retaining premium taste profiles, using cocoa butter blends, plant-based milks, and dedicated allergen-controlled production lines. Dark chocolate variants dominate launches, as they naturally contain fewer allergen inputs and appeal to health-conscious consumers seeking lower sugar and higher antioxidant content.

Innovation cycles remain rapid, with brands experimenting in filled bars, spreads, baking chips, and seasonal assortments that meet multi-allergen-free certifications. Limited-edition flavors and ethically sourced cocoa further enhance differentiation in premium retail channels. Online platforms and specialty health stores play an increasing role in distribution, helping niche brands reach targeted allergy-sensitive shoppers globally. Together, indulgence appeal, technical reformulation success, and expanding retail penetration sustain chocolate’s strong revenue contribution within the allergen-free product landscape.

By Claim Insights

Sugar-free positioning has emerged as the dominant claim category within the allergen-free food market, driven by overlapping consumer motivations around allergy management, diabetes prevention, and weight control. Shoppers increasingly view sugar reduction as complementary to “free-from” labels, reinforcing perceptions of overall healthfulness. Food manufacturers are responding by integrating natural sweeteners such as stevia, monk fruit, and erythritol into allergen-safe formulations across bakery items, chocolates, beverages, and snack bars. Regulatory encouragement for sugar disclosure and front-of-pack nutrition labelling further accelerates demand for low- and no-sugar options, strengthening retailer shelf prioritization for such products.

The versatility of sugar-free claims across multiple food categories allows brands to extend single formulations into wide product ranges, improving scale economics and marketing efficiency. Functional positioning linking sugar-free with clean-label, plant-based, and calorie-controlled benefits also resonates strongly with urban consumers. As lifestyle-related health concerns rise alongside allergy prevalence, sugar-free is expected to remain the most commercially attractive and innovation-rich claim segment within the allergen-free foods category.

Region-wise Insights

North America Allergen-Free Food Market Trends

North America remains a mature and innovation-driven market for allergen-free foods, supported by high diagnosis rates of food sensitivities and strong regulatory oversight. Clear labeling requirements and school safety policies encourage routine household purchases rather than occasional specialty use. U.S. and Canadian manufacturers are increasingly investing in dedicated production facilities to prevent cross-contamination, enabling expansion across bakery items, chocolates, frozen meals, and beverages. Retailers are allocating larger shelf space to “free-from” sections, while private-label brands introduce competitively priced alternatives that broaden consumer access.

Digital grocery platforms and subscription models are accelerating product discovery, especially for families managing multiple allergies. Premiumization also shapes regional demand, with organic, non-GMO, and functional nutrition claims layered onto allergen-free positioning. Product development focuses on improving taste and texture through plant-based proteins and fermentation-derived ingredients. Collaboration between healthcare groups, advocacy organizations, and food companies continues to raise awareness, ensuring that allergen-free foods remain a core component of North America’s evolving health-focused packaged food sector.

Europe Allergen-Free Food Market Trends

Europe’s allergen-free food market is shaped by harmonized labeling regulations and a long-standing consumer preference for clean, transparent ingredient lists. Shoppers in countries such as Germany, the UK, and France closely scrutinize packaging claims, pushing manufacturers to obtain third-party certifications and invest in traceable supply chains. Bakery and confectionery categories are particularly active, with reformulated breads, biscuits, and chocolates gaining shelf presence in mainstream supermarkets rather than only health-food stores. Plant-based dairy alternatives also play a central role, aligning allergen-free positioning with sustainability and animal-welfare priorities.

Local sourcing and artisanal branding are increasingly used to differentiate products, especially in premium segments. Discounters and private labels are expanding allergen-free assortments to capture value-seeking consumers, widening category reach beyond affluent urban households. E-commerce remains an important supplementary channel for specialty items, while cross-border trade within the European Union supports rapid distribution of new launches. Overall, Europe’s market is progressing steadily through regulatory consistency, strong retail integration, and consumer trust in certified food standards.

Asia Pacific Allergen-Free Food Market Trends

Asia Pacific represents the fastest-expanding regional market for allergen-free foods, driven by urbanization, rising disposable incomes, and growing interest in preventive healthcare. Middle-class consumers in China, India, Japan, and Southeast Asia are increasingly experimenting with packaged foods that highlight safety and nutritional transparency, encouraging multinational brands to localize formulations and labeling. Modern retail chains, specialty wellness stores, and online marketplaces are rapidly widening distribution, making allergen-free snacks, beverages, and bakery items more accessible than in previous years.

Domestic manufacturers are entering the space with region-specific flavors and affordable pack sizes to appeal to first-time buyers. Government-backed clean-label initiatives and sugar-reduction campaigns indirectly benefit allergen-free categories, while rising exposure to Western dietary trends supports adoption of dairy-free and gluten-free products. Product innovation emphasizes rice-based, coconut-derived, and legume-based ingredients that align with local culinary habits. As awareness spreads through healthcare providers and digital media, Asia Pacific is emerging as a long-term growth engine for allergen-free food companies.

Market Competitive Landscape

The allergen-free food market features intense competition between multinational food corporations and specialized health-focused brands seeking to capture rising safety-driven demand. Leading players leverage global manufacturing scale, regulatory expertise, and retail relationships to extend allergen-free variants across mainstream categories such as snacks, beverages, and ready meals. Their investments in reformulation science and contamination-controlled facilities strengthen brand credibility and volume growth.

Smaller and mid-tier companies compete through niche positioning, targeting pediatric nutrition, plant-based lifestyles, and functional wellness with transparent labeling and premium ingredients. Partnerships, licensing deals, and acquisitions are reshaping portfolios as companies pursue faster market entry and geographic expansion. Continuous product innovation, certification programs, and omnichannel distribution strategies remain central to sustaining differentiation and market share in this rapidly evolving sector.

Key Industry Developments:

- In June 2025, Gluten-free food supplier Juvela launched a new bakery brand called Oaf while investing £1.5m in a new allergen-free production site in South Wales.

- In May 2024, the Asian plant-based company developed its next-generation “chicken” recipe at SHICKEN’s certified allergen-free facility in Kent using exclusively British ingredients.

Companies Covered in Allergen-Free Food Market

- Nestlé S.A.

- Danone S.A.

- General Mills Inc.

- The Kraft Heinz Company

- Unilever PLC

- Mondelēz International, Inc.

- Conagra Brands, Inc.

- Kellogg Company

- The Hain Celestial Group, Inc.

- Tyson Foods, Inc.

- Blue Diamond Growers

- Chobani LLC

- Grupo Bimbo, S.A.B. de C.V.

- Others

Frequently Asked Questions

The allergen free-food market is estimated to be valued at US$ 52.5 Bn in 2026.

Rising food allergy prevalence, regulatory labeling requirements, clean-label trends, plant-based diets, and expanding retail availability drive market growth.

The global market is expected to witness a CAGR of 7.1% between 2026 and 2033.

The top players are Nestlé S.A., Danone S.A., General Mills Inc., The Kraft Heinz Company, and Unilever PLC.

North America is the leading region in the global allergen-free food market.