- Processed Food

- Plant-based Seafood Market

Plant-based Seafood Market Size, Share, and Growth Forecast 2026 - 2033

Plant-based Seafood Market by Product Type (Fish alternatives, Shrimp & Prawn alternatives, Crab alternatives, Others), by Source (Soy, Pea protein, Wheat, Algae & Seaweed, Others), Distribution Channel (Supermarkets/Hypermarkets, Online Stores, Specialty Stores, Others), and Regional Analysis, 2026 - 2033

Plant-based Seafood Market Share and Trends Analysis

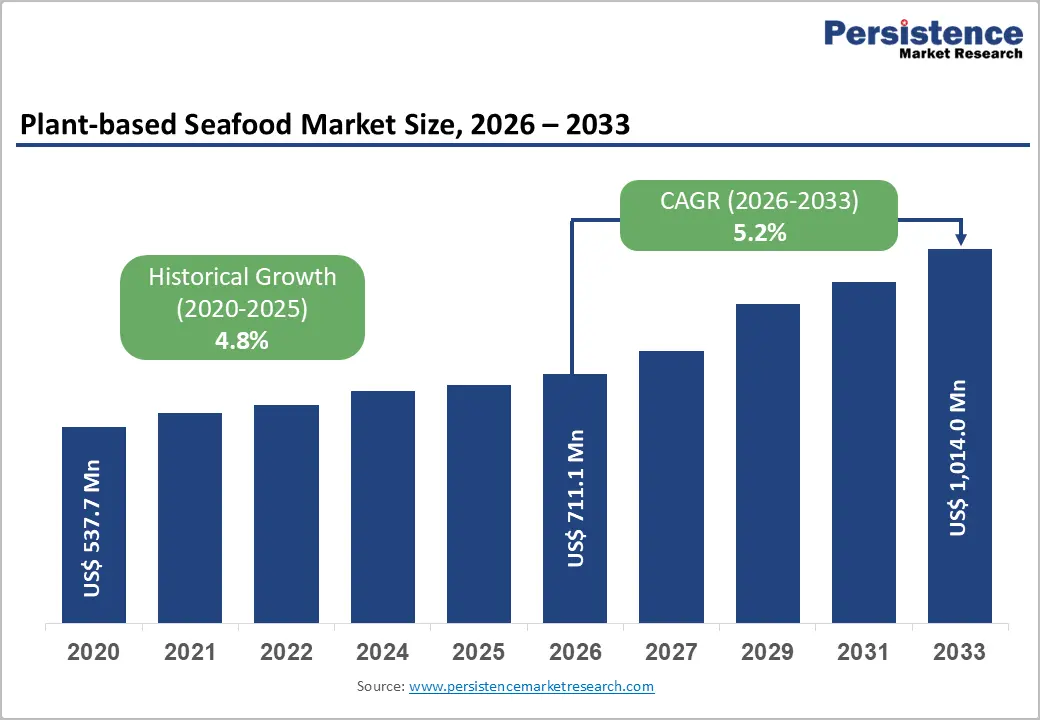

The global plant-based seafood market size is expected to be valued at US$ 711.1 million in 2026 and projected to reach US$ 1,014.0 million by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

This steady expansion is driven by intensifying concerns about overfishing, climate impacts of animal protein, and food safety risks associated with conventional seafood, alongside the rising popularity of flexitarian and vegan diets. Backed by advancements in food technology and ingredient functionality, plant-based seafood products are increasingly capable of mimicking the taste, texture, and nutritional profile of fish and shellfish, thereby gaining traction in both retail and foodservice.

Key Industry Highlights:

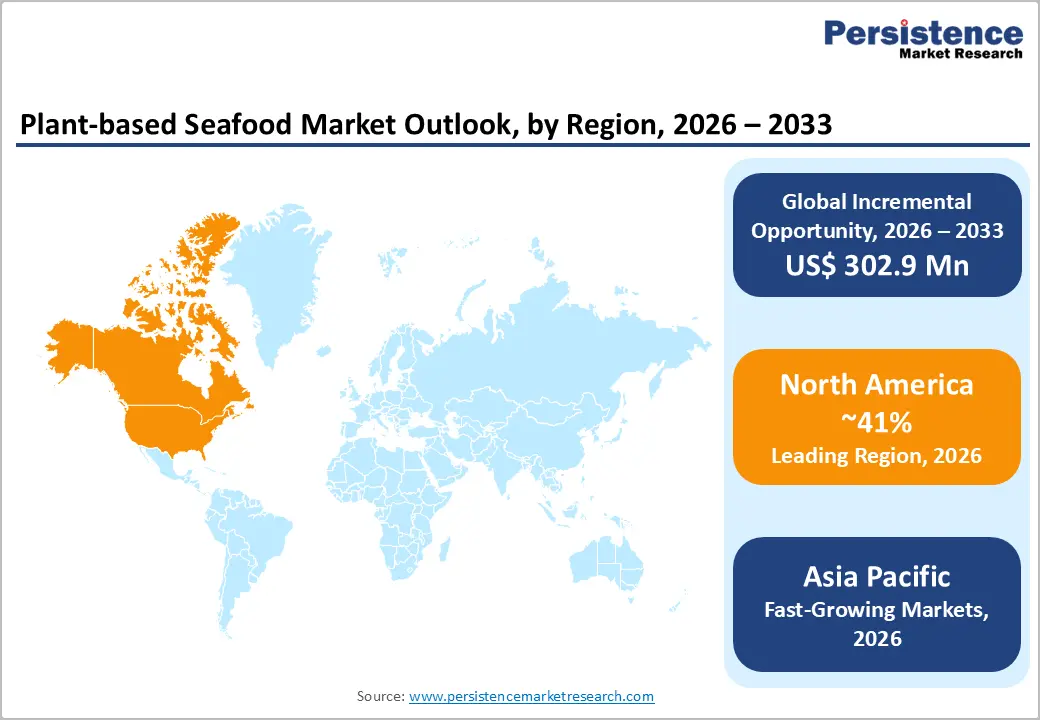

- North America is the leading regional market for plant-based seafood, holding around 41% share in 2025, driven by high awareness of overfishing and climate impacts, strong alternative protein innovation ecosystems, and broad retail and foodservice availability of fish, shrimp, and crab analogues.

- Asia Pacific is the fastest-growing region, supported by its role as the world’s largest seafood-consuming and aquaculture-producing area, rising middle-class incomes, growing food safety and sustainability concerns, and active alternative protein initiatives in markets such as China, Japan, Singapore, and Hong Kong.

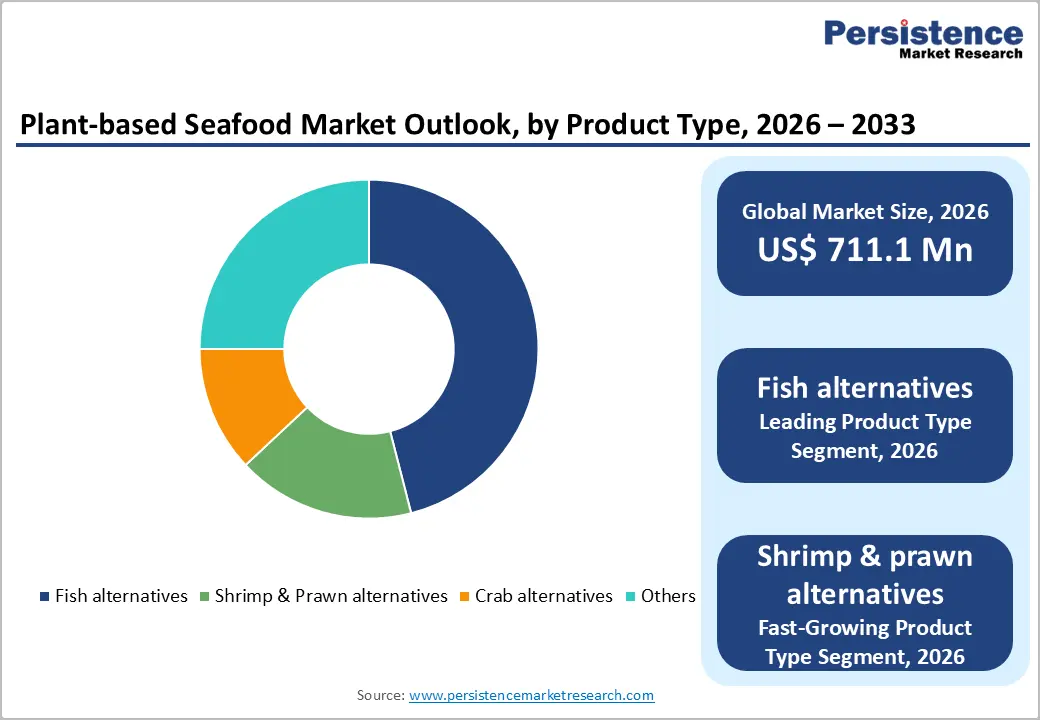

- By product type, fish alternatives dominate with approximately 46% market share in 2025, as plant-based tuna, salmon-style, and white-fish products integrate seamlessly into familiar dishes such as sandwiches, sushi, and fish-and-chips, lowering adoption barriers for mainstream seafood consumers.

- Shrimp and prawn alternatives represent the fastest-growing product segment, propelled by strong demand in Asian cuisines, mounting scrutiny of labor and environmental practices in conventional shrimp supply chains, and ongoing innovation in pea- and algae-based shrimp analogues suitable for stir-fries, tempura, and appetizer formats.

- The food technology is advancing, followed with the growth in e-commerce, and strategic foodservice partnerships to scale plant-based seafood globally, particularly in seafood-centric Asia Pacific markets, while communicating clear sustainability, health, and animal welfare benefits to increasingly conscious consumers.

| Key Insights | Details |

|---|---|

| Plant-based Seafood Market Size (2026E) | US$ 711.1 Mn |

| Market Value Forecast (2033F) | US$ 1,014.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Dynamics

Drivers - Rise in Sustainability and Overfishing Concerns

One of the strongest growth drivers for the plant-based seafood market is heightened awareness of ocean sustainability and overfishing. The Food and Agriculture Organization (FAO) reports that around 35% of global fish stocks are fished at biologically unsustainable levels, while per capita seafood consumption has more than doubled since the 1960s, placing enormous pressure on marine ecosystems. Scientific evidence linking trawling and intensive fishing to habitat destruction and biodiversity loss is encouraging consumers, retailers, and policymakers to seek alternatives. Plant-based seafood offers a way to decouple seafood consumption from wild catch and intensive aquaculture, reducing pressure on overexploited species and sensitive habitats. Retailers in North America and Europe increasingly use sustainability labels and sourcing policies that favor lower-impact proteins, giving plant-based seafood greater visibility and shelf space as part of their corporate environmental, social, and governance (ESG) strategies.

Health, Food Safety, and Allergen Considerations

Health and food safety concerns provide another powerful demand driver. Traditional seafood is associated with issues such as microplastic contamination, bioaccumulation of heavy metals like mercury, and periodic outbreaks of foodborne illness from pathogens or marine biotoxins. Studies cited by agencies including the World Health Organization (WHO) and national food safety authorities have raised awareness of these risks, especially for vulnerable groups such as pregnant women and children. Plant-based seafood eliminates concerns around parasites and many marine contaminants while enabling better control over fat, sodium, and cholesterol levels. At the same time, consumers with shellfish allergies estimated to affect up to 2% of adults in some markets can enjoy seafood-style dishes without exposure to crustacean proteins. Brands such as Good Catch Foods, New Wave Foods, and Sophie’s Kitchen use protein sources like pea, soy, and algae to recreate seafood experiences with consistent quality, supporting adoption among health-conscious and allergy-sensitive consumers.

Restraints - Taste, Texture, and Culinary Performance Gaps

Despite progress, one of the key restraints on plant-based seafood is the challenge of replicating the complex taste, texture, and cooking behavior of conventional fish and shellfish. Seafood has highly specific muscle structures, flaky textures, and fat distributions that are difficult to mimic using plant proteins. Consumer taste tests reported by category innovators and organizations such as the Good Food Institute (GFI) indicate that texture and aftertaste remain top barriers to repeat purchase for first-time buyers of plant-based seafood. Products can behave differently under high-heat cooking or deep frying, creating inconsistency for chefs and home cooks used to traditional seafood. Until food technology and extrusion techniques close this sensory gap for mainstream consumers, uptake may remain concentrated among early adopters and environmentally motivated shoppers rather than the broader seafood-eating population.

Price Premiums and Limited Scale in Some Regions

Price remains a notable barrier, particularly in price-sensitive markets. Due to relatively small production volumes, specialized ingredients, and the need for advanced processing technologies, plant-based seafood products often carry price premiums of 20-50% compared with mass-market frozen fish or shrimp. Retail scanner data in key markets tracked by organizations like GFI and industry trade bodies show that plant-based alternatives, including seafood, skew toward higher-income, urban consumers. In emerging economies across Asia Pacific, Latin America, and Middle East & Africa, limited cold-chain infrastructure, higher logistics costs, and lower consumer purchasing power can restrict distribution and adoption. Until manufacturers achieve greater economies of scale and localize supply chains, the category’s price positioning may limit its potential to become a true mass-market substitute in many regions.

Opportunity - Rapid Innovation in Ingredients, Technology, and Hybrid Products

Strong innovation momentum in plant proteins and food processing technologies presents major opportunities for plant-based seafood. Advances in high-moisture extrusion, shear cell technology, and flavor chemistry are enabling more convincing replication of muscle fibers, flaky textures, and umami-rich seafood flavors. Ingredient suppliers are refining functional soy, pea, wheat, and fava proteins, while algae and seaweed sources are being harnessed for natural marine flavors, iodine, and omega fatty acid fortification. Companies such as Impossible Foods, Quorn Foods, and Gardein (Conagra Brands) are exploring hybrid formats that combine plant proteins with fermentation-derived fats or heme analogues to deliver more authentic seafood experiences. These technologies, supported by academic research and collaborations funded by organizations like the Good Food Institute (GFI), create pathways to product differentiation across fish fillets, sticks, crab cakes, sushi fillings, and ready meals, broadening use cases in both retail and foodservice.

Expansion in Foodservice, QSR, and Asian Seafood-centric Markets

Significant headroom exists for plant-based seafood penetration in foodservice and quick-service restaurant (QSR) channels, especially in seafood-heavy cuisines across Asia Pacific and coastal regions worldwide. Global seafood demand is growing fastest in Asian markets, where rising incomes and urbanization support higher per capita consumption. Reports from FAO highlight that aquaculture now supplies over 50% of seafood consumed globally, yet concerns over antibiotics, disease outbreaks, and environmental impacts are rising. Plant-based seafood can serve as a complementary solution for restaurants, hotel chains, and QSR brands seeking to offer sustainable menu options without supply volatility linked to fishing seasons or disease in shrimp and fish farms. Companies like Nestlé (Vuna/Garden Gourmet), OmniFoods (OmniSeafood), and The Plant Based Seafood Co. are partnering with regional chains to pilot plant-based fish burgers, shrimp dishes, and dim sum items, opening substantial growth opportunities in markets where seafood is central to daily diets.

Category-wise Analysis

Product Type Insights

By product type, fish alternatives dominate the plant-based seafood market, accounting for approximately 46% share in 2025. This leadership is supported by the central role that fish plays in global seafood consumption patterns, with the FAO reporting that finfish represents the majority of seafood eaten worldwide. Fish alternatives such as plant-based tuna, salmon-style fillets, and breaded fish sticks fit seamlessly into established dishes like sandwiches, sushi rolls, tacos, and fish-and-chips, lowering the behavioral barrier for consumers. Brands including Good Catch Foods, Nestlé (Vuna/Garden Gourmet), and Loma Linda / TUNO (Atlantic Natural Foods) have introduced shelf-stable and chilled fish-style products across retail channels in North America and Europe, often fortified with omega fatty acids and vitamin B12 to emulate nutritional aspects of seafood. Shrimp and prawn alternatives represent the fastest-growing segment, driven by strong demand in Asian cuisines and growing concerns around labor practices and disease management in conventional shrimp farming.

Source Insights

Among protein sources, soy currently leads the plant-based seafood market, with an estimated share of around 39% in 2025. Soy is one of the most widely studied and commercially available plant proteins, recognized by authorities such as the U.S. Food and Drug Administration (FDA) for its cholesterol-lowering benefits when consumed as part of a diet low in saturated fat. Its functional properties good water-holding capacity, emulsification, and gel formation make it suitable for creating fibrous, meat-like textures in fish fillets and crab-style products. Many early entrants in plant-based seafood, including lines under Gardein (Conagra Brands) and Quorn Foods, rely heavily on soy or soy-wheat blends. However, pea protein is emerging as the fastest-growing source segment, supported by its non-allergenic positioning compared to soy and wheat, its neutral flavor profile, and strong investment into pea processing capacity in regions like North America and Europe. Companies such as New Wave Foods and The Plant Based Seafood Co. increasingly use pea protein to develop shrimp, scallop, and white-fish analogues.

Distribution Channel Analysis

Supermarkets and hypermarkets are the leading distribution channel for plant-based seafood, accounting for an estimated 45% share of global sales in 2025. Large grocery retailers have become critical gatekeepers for the broader plant-based category, with chains in North America and Europe dedicating freezer and refrigerated space to alternative proteins. Data compiled by organizations such as GFI show that plant-based meat and seafood are often merchandised adjacent to or within the conventional meat and seafood aisles to encourage trial by mainstream shoppers. Prominent placements, in-store sampling, and private-label launches are all helping normalize plant-based seafood in the weekly shop. Online stores, however, represent the fastest-growing channel, buoyed by subscription models, direct-to-consumer offerings, and the convenience of home delivery. Specialty vegan and natural food stores remain important discovery hubs but contribute a smaller share of total volume relative to large-format supermarkets and e-commerce platforms.

Regional Insights

North America Plant-based Seafood Market Trends and Insights

North America is the leading regional market, representing around 41% share of global plant-based seafood sales in 2025. The United States dominates regional consumption, supported by high per capita income, widespread concern about overfishing and climate impacts, and a robust ecosystem of alternative protein innovators and investors. Organizations such as the Good Food Institute (GFI) and Plant Based Foods Association (PBFA) have documented strong growth in plant-based retail categories over recent years, with seafood emerging as a key white-space opportunity within the broader alternative protein landscape. Regulatory clarity from agencies such as the FDA and U.S. Department of Agriculture (USDA) on labeling and safety for plant-based foods has further enabled market entry.

Asia Pacific Plant-based Seafood Market Trends and Insights

Asia Pacific is the fastest-growing regional market for plant-based seafood over the forecast period, reflecting its status as the world’s largest seafood-consuming region and its deep cultural ties to marine foods. The FAO notes that Asia accounts for more than 70% of global aquaculture production and a substantial share of wild catch, yet the region also faces acute challenges related to overfishing, coastal degradation, and aquaculture disease outbreaks. Rising middle-class incomes in China, India, and members of the Association of Southeast Asian Nations (ASEAN) are driving higher per capita seafood intake but also heightening awareness of food safety issues and supply volatility. Plant-based seafood provides a way to meet demand for familiar dishes such as dumplings, tempura, curries, and sushi while mitigating environmental and health concerns.

Competitive Landscape

The plant-based seafood market is characterized by a dynamic and innovation-driven competitive landscape. Companies compete primarily on product taste, texture, nutritional profile, and clean-label positioning. Continuous R&D investments focus on improving seafood-like flavor, fibrous structure, and omega-3 fortification using algae and plant proteins. Strategic partnerships with foodservice chains and retail expansion play a key role in strengthening market presence. Branding emphasizes sustainability, ocean conservation, and health benefits to attract flexitarian consumers. Pricing remains a competitive challenge, as manufacturers work to achieve cost parity with conventional seafood.

Key Market Developments

- In October 2025, The U.S.-based Plant Based Seafood Co., owner of the Mind Blown™ brand, announced that its award-winning Dusted Scallops became available in bulk packs through WebstaurantStore.com. The launch expanded the company’s foodservice portfolio by offering chefs, restaurants, and foodservice operators a new plant-based seafood option. The product joined Mind Blown’s existing foodservice lineup, which already included Crab Cakes and Crispy Crunchy Fried Shrimp.

Companies Covered in Plant-based Seafood Market

- Good Catch Foods

- New Wave Foods

- Ocean Hugger Foods

- Sophie’s Kitchen

- Gardein (Conagra Brands)

- The Plant Based Seafood Co.

- Impossible Foods

- Nestlé (Vuna/Garden Gourmet)

- Quorn Foods

- Loma Linda / TUNO (Atlantic Natural Foods)

- OmniFoods (OmniSeafood)

- BlueNalu

- Other

Frequently Asked Questions

The global plant-based seafood market is projected to reach approximately US$ 711.1 million in 2026, supported by rising concerns about overfishing, climate impacts of animal protein, and growing consumer interest in sustainable, low-contaminant alternatives to conventional fish and shellfish.

Key demand drivers include escalating awareness of overfishing and marine ecosystem degradation, health and food safety concerns regarding contaminants and pathogens in conventional seafood, rapid innovation in plant protein technologies, and the broader shift toward flexitarian and vegan diets that prioritize sustainability, animal welfare, and improved nutritional profiles.

North America currently leads the global plant-based seafood market, with an estimated 41% share in 2025, driven by high levels of environmental awareness, strong alternative protein innovation ecosystems, supportive retail and foodservice channels, and active engagement from both startups and major food manufacturers.

The most significant opportunity lies in scaling plant-based seafood across Asia Pacific and other seafood-centric regions through foodservice partnerships, retail expansion, and e-commerce, while leveraging advances in ingredients and processing technologies to close sensory and price gaps with conventional seafood and clearly communicate sustainability and health benefits.

Major players include Good Catch Foods, New Wave Foods, Ocean Hugger Foods, Sophie’s Kitchen, Gardein (Conagra Brands), The Plant Based Seafood Co., Impossible Foods, Nestlé (Vuna/Garden Gourmet), Quorn Foods, Loma Linda / TUNO (Atlantic Natural Foods), OmniFoods (OmniSeafood), BlueNalu, and several emerging brands and private-label lines from leading retailers in key regions.