- Industrial Machinery

- Fabric Cutting Machine Market

Fabric Cutting Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Fabric Cutting Machine Market By Machine Type (Automatic, Semi-automatic, Others), Cutting Method (Straight Knife, Laser, Others), Application, and Regional Analysis for 2026 - 2033

Fabric Cutting Machine Market Size and Trends Analysis

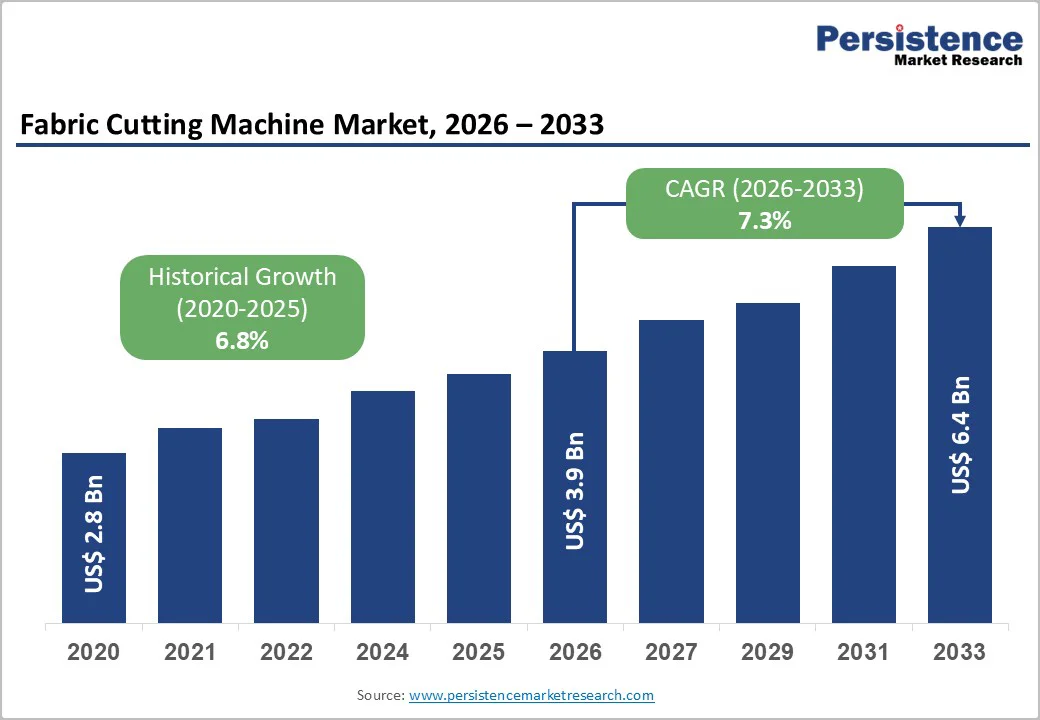

The global fabric cutting machine market size is likely to be valued at US$3.9 billion in 2026 and is expected to reach US$6.4 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033, driven by rising automation in apparel and technical textiles, faster adoption of precision cutting technologies such as laser and CNC-integrated systems, and productivity pressures that push manufacturers to reduce material waste and labor dependence.

Investments in automation and Industry 4.0 are increasing cutting system costs, with laser and digital cutters outpacing traditional knives, raising prices and shortening replacement cycles.

Key Industry Highlights

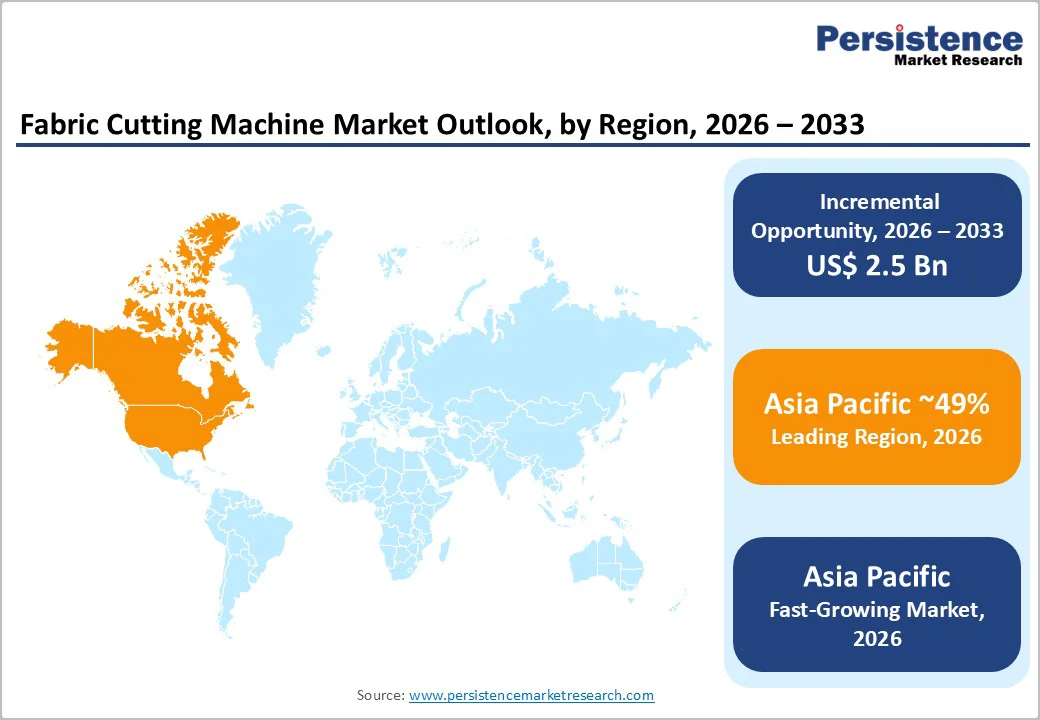

- Leading Region: Asia Pacific, anticipated to account for approximately 49% of the global market share, driven by large apparel clusters, rapid industrialization, and increasing automation across China, India, Bangladesh, and Vietnam.

- Fastest-growing Region: Asia Pacific, supported by rising labor costs, government-backed modernization programs, and accelerated adoption of automated and laser-based cutting systems.

- Investment Plans: Strong investments in automation, CAD/CAM software integration, and digital cutting-room upgrades, especially in China, India, and North America. OEMs are expanding regional service centers, training hubs, and pay-per-use models to support modernization.

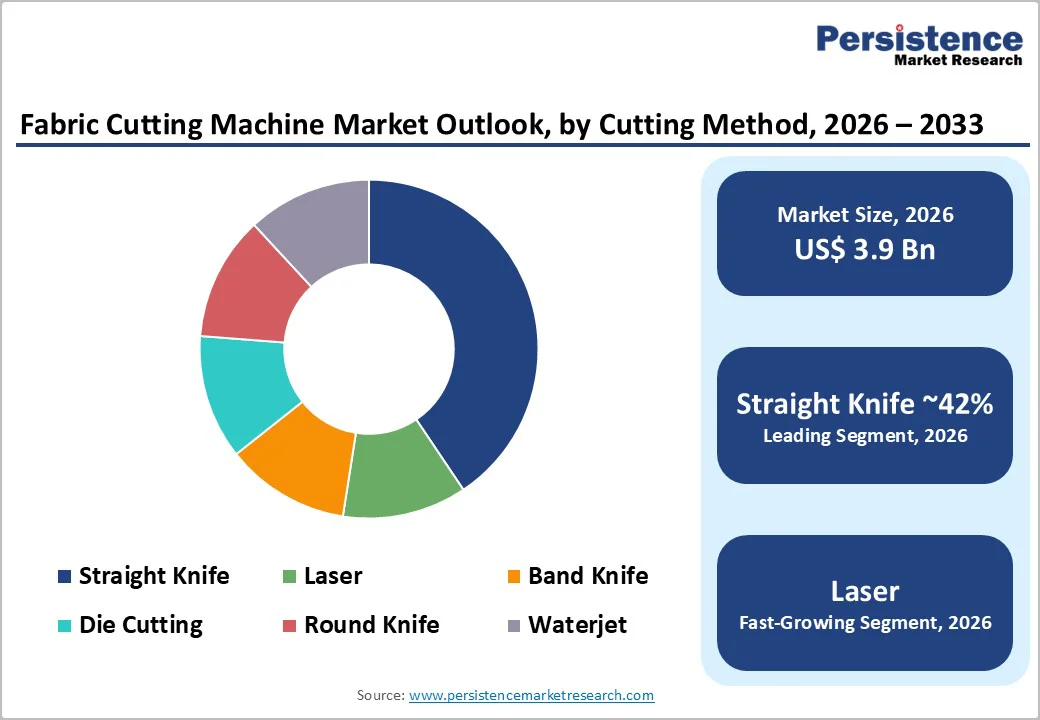

- Dominant Cutting Method: Straight-knife cutting, anticipated to hold 42% of market share, due to its high usage in bulk apparel production and cost-effective operation, maintaining a dominant share across traditional manufacturing hubs.

- Leading Application: Apparel and textiles, estimated to hold 43% and contribute the highest share due to mass garment manufacturing, fast-fashion cycles, and reliance on multi-layer and digital cutting systems.

| Key Insights | Details |

|---|---|

| Fabric Cutting Machine Market Size (2026E) | US$3.9 Bn |

| Market Value Forecast (2033F) | US$6.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automation and Industry 4.0 Adoption

Growing automation within apparel, upholstery, and technical textiles is increasing the adoption of digital, CNC, and multi-ply cutting systems. Automated cutting rooms improve throughput by two to five times compared with manual methods and reduce material waste through optimized nesting algorithms and vision-assisted cutting.

With rising labor costs and demand for consistent quality, manufacturers are transitioning to automated platforms capable of real-time monitoring, remote diagnostics, and data-driven workflow optimization. These technologies strengthen the value proposition for automatic systems, which already lead the market with a 45 percent share.

As automation becomes central to factory modernization, investment cycles for cutting equipment accelerate, supporting sustained growth across high-efficiency cutting solutions.

Technology Substitution: Laser, Digital, and CNC Systems

Rapid substitution of legacy knife-based systems with laser cutters, digital cutters, and CNC-integrated platforms is reshaping the competitive landscape. Laser cutting in particular delivers high precision, edge quality, and the ability to handle delicate or complex materials without mechanical distortion. Digital cutters support intricate patterns, variable-batch production, and seamless integration with CAD/CAM workflows.

These high-value technologies generally grow faster than the overall market due to advantages in accuracy, reduced tooling requirements, and compatibility with automation. Their higher purchase price and expanded aftermarket service needs lift the average selling price for cutting systems, enabling vendors to capture more value through software, service contracts, and systems integration.

Growth in Apparel, Nearshoring, and Technical Textiles

Demand from apparel manufacturing and rising consumption of technical textiles in automotive, filtration, infrastructure, and industrial use cases is increasing the need for high-precision cutting systems. Nearshoring in the U.S. and Europe is prompting factories to adopt advanced automation to offset labor differentials. Automotive and industrial textile production requires multi-layer cutting, clean edges, and strict quality control for engineered fabrics, driving the adoption of CNC and digital systems capable of meeting these requirements. As technical textiles expand in volume and complexity, manufacturers invest in cutting solutions that handle composites, reinforced fabrics, and multilayer assemblies. These trends broaden the addressable market and promote more stable, diversified demand.

Barrier Analysis - High Capital Costs and Long Procurement Cycles

Large automatic and CNC-integrated cutting machines involve significant upfront investment, which can limit adoption among small and mid-sized manufacturers. Procurement cycles are often lengthy due to the need for sample validation, workflow integration, and ROI assessment.

Typical payback periods of two to four years can delay approval, especially in price-sensitive markets. If labor savings or yield improvements appear uncertain, buyers often postpone purchases, extending replacement cycles. These factors restrain near-term market expansion and slow the penetration of advanced automation in emerging markets.

Supply Chain and Component Vulnerabilities

Advanced fabric cutting systems depend on precision components such as servo motors, linear drives, controllers, and laser modules. Disruptions in electronics or motion-control supply chains can raise input costs and extend delivery lead times by several weeks or months.

Increased logistics costs and shortages of specific components amplify production delays for OEMs and reduce short-term revenue recognition. Extended delivery schedules may also encourage customers to delay purchases or select lower-specification equipment, creating volatility in quarterly sales performance.

Opportunity Analysis - Aftermarket Services and Software-as-a-Service

Aftermarket services represent a growing revenue opportunity centered on predictive maintenance, extended warranties, training, system optimization, and software subscriptions. Advanced nesting software, production analytics, and cloud-based asset monitoring help manufacturers improve material utilization and minimize downtime.

If recurring service and subscription revenues capture even 10 to 15 percent of annual system value, the market could generate several hundred million dollars in incremental revenue by the end of the decade. As customers increasingly prioritize uptime and productivity, bundled hardware-software-service offerings strengthen OEM customer retention and create more predictable revenue streams.

Emerging Market Penetration and Cutting-Room Upgrades

Upgrading cutting rooms in South Asia, Southeast Asia, and parts of Africa and Latin America offers major growth potential. Many factories still rely on manual or semi-manual cutting, leaving substantial room for automation penetration. Expanding local service centers, financing schemes, and training programs can accelerate the adoption.

If automation penetration increases by only five to ten percent in key apparel hubs across Asia Pacific, the resulting revenue could reach several hundred million dollars through 2033. Local manufacturing partnerships, demonstration centers, and distributor networks will further ease buyer adoption and improve lifecycle support.

Category-wise Analysis

Cutting Method Insights

Straight-knife cutting is anticipated to be the leading segment, accounting for 42% of market share in 2026, due to its longstanding installed base, operational simplicity, and low overall ownership costs. Factories in cost-sensitive textile clusters such as Bangladesh, Vietnam, and parts of India depend extensively on straight-knife systems for bulk fabric cutting, particularly in everyday apparel categories such as shirts, denim, uniforms, and knitwear.

These machines offer high cutting speeds, adaptability across thick and multilayer fabrics, and longer operating life. The availability of local technicians and affordable spare parts further strengthens adoption for small and mid-sized manufacturers.

For instance, garment exporters in Tirupur and Ho Chi Minh City frequently use straight-knife systems for 50 to 80-layer fabric spreads, where complex automation is unnecessary. Even as laser, waterjet, and digital cutting technologies scale, straight-knife systems remain the default choice for large-layer cutting, thick materials, and simple repeat patterns.

Their durability, minimal downtime, and reliability under high-volume cycles ensure steady demand in regions with lower automation maturity. In many traditional apparel facilities, straight-knife cutting continues to function as the backbone of daily operations, especially where manual workflows and large order quantities prevail.

Laser cutting is the fastest-growing method, supported by precision capabilities, sealed-edge quality, and compatibility with delicate, composite, or digitally patterned fabrics.

Non-contact cutting prevents fabric distortion, allowing manufacturers to handle intricate designs in sportswear, lingerie, outdoor apparel, automotive trims, and aerospace composites. For example, premium activewear brands increasingly use CO2 laser systems to cut stretch fabrics, perforated ventilation zones, and bonded seams with high repeatability.

Eliminating physical tooling reduces wear-and-tear costs and shortens design-to-production cycles. Industries with stringent tolerance requirements, such as airbags or carbon-fiber interior parts, rely heavily on digital laser workflows.

Continuous improvements in laser efficiency, fume extraction systems, and CAD/CAM integration accelerate adoption. As suppliers target lower waste, higher precision, and cleaner cut aesthetics, laser cutting continues to outpace traditional knife-based systems across both high-value textiles and technical materials.

Application Insights

The apparel and textile industry remains the leading segment, estimated to hold 43% driven by high global garment production volumes and the need for efficient cutting operations across both mass-market and fast-fashion supply chains. Manufacturers depend heavily on reliable cutting platforms as cutting quality directly affects fit, fabric consumption, and sewing efficiency.

Large factories in China, Bangladesh, and Indonesia use multi-layer automated cutters to handle high-volume orders for T-shirts, denim, formalwear, and athleisure. Fast-fashion brands such as Zara, H&M, and Shein rely on digital cutting technologies to support rapid replenishment, micro-batch production, and frequent style variations.

Demand is further reinforced by the shift toward shorter fashion cycles and customization. For example, print-on-demand manufacturers increasingly use CNC or digital cutters to process unique patterns, limited-edition collections, and personalized apparel.

Precise cutting helps reduce material waste and supports sustainability initiatives within the fashion industry. As apparel companies continue to optimize speed, precision, and efficiency, cutting systems remain indispensable to their operational workflows.

The automotive segment is growing the fastest due to the rising use of engineered fabrics, multi-layer composites, airbags, thermal insulation, acoustic pads, and high-performance upholstery materials.

These components require extremely tight tolerances to meet durability, safety, and regulatory standards. Automotive OEMs and tier-1 suppliers rely increasingly on laser and CNC-integrated cutting systems for components such as seat covers, door panels, headliners, trunk liners, and EV battery insulation.

Growth in electric vehicles amplifies this demand, as EV interiors emphasize lightweight materials and advanced acoustic insulation. For instance, EV manufacturers in Europe and China frequently use automated laser cutters to process composite mats and non-woven materials that require clean edges without fraying.

The complexity of modern automotive fabrics positions cutting equipment as a critical quality-control asset, driving continued investment in high-precision digital platforms across global automotive production hubs.

Regional Insights

North America Fabric Cutting Machine Market Trends - Advanced Automation Adoption & Industry-Driven Digital Upgrades

North America’s cutting systems market is driven by strong automation adoption and demand across technical textiles, aerospace composites, automotive interiors, and advanced manufacturing sectors.

Higher average selling prices reflect buyers’ preference for digitally integrated systems featuring nesting software and automated material handling. Market growth is supported by selective apparel nearshoring, renewed domestic sportswear production, and expansions in industrial filtration and performance fabrics.

The U.S. accounts for most regional demand due to its large base of automotive suppliers, aerospace manufacturers, furniture producers, and premium apparel brands. Leading companies such as Boeing, Tesla, and Lear Corporation increasingly rely on digitally enabled cutting systems for composites, insulation, and interior components, boosting demand for precision equipment.

Small and mid-sized textile firms are also adopting semi-automatic cutters to offset rising labor costs and remain competitive. Buyers emphasize lifecycle support, software compatibility, and long-term reliability when selecting new systems.

Regulatory pressures on safety, energy efficiency, and waste reduction are further accelerating equipment modernization. Suppliers such as Gerber Technology and Lectra support this shift with expanded demo centers, integrated material-optimization tools, MES/ERP connectivity, and advanced training programs.

Vendors offering bundled hardware, software, and maintenance maintain a competitive advantage as industries move toward connected cutting rooms for engineered and customized materials.

Europe Fabric Cutting Machine Market Trends - Precision, Sustainability & High-Performance Cutting Technologies

Europe represents a high-value market for precision cutting technologies, driven by demand across fashion, upholstery, composites, and technical textiles. Key countries, Germany, Italy, France, Spain, and the U.K., lead adoption due to strict environmental standards, strong engineering capabilities, and a long-standing tradition of textile and material innovation. Manufacturers prioritize systems that deliver speed, accuracy, and sustainability.

Germany drives demand in industrial textiles and composites, with companies such as BASF, BMW, and ZF Group increasingly deploying CNC and digitally controlled platforms for carbon fiber, non-wovens, and specialty laminates. Strong engineering expertise supports early adoption of high-performance cutting systems for aerospace and automotive applications.

France, Italy, and Spain are the major contributors through the fashion, luxury apparel, and upholstery sectors. Italian furniture and upholstery manufacturers rely on precision digital cutters for leather, technical fabrics, and high-density foams.

French fashion houses, including LVMH and Kering, continue to invest in automated cutters and laser systems to enable high-mix, short-run production. EU-wide regulatory frameworks reinforce modernization by promoting energy efficiency, material traceability, and sustainability reporting, encouraging integration of advanced cutting systems with digital tracking tools.

Regional investments also include expansion of R&D and training centers by companies such as Lectra in France and Bullmer in Germany, alongside increased adoption of software-hardware integration, supporting the shift toward connected and efficient cutting operations.

Asia Pacific Fabric Cutting Machine Market Trends - Rapid Automation Growth across Apparel & Technical Textile Hubs

The Asia Pacific region is set to account for around 49% of the global cutting systems market and remains the fastest-growing due to extensive apparel clusters, a growing technical textiles base, and rising automation adoption. Key markets include China, India, Bangladesh, Vietnam, Indonesia, and other leading ASEAN countries, driving strong demand for both basic and advanced cutting solutions.

China leads with the largest installed base, supported by export-oriented manufacturers and increased automation investments. Companies such as Shenzhou International, Youngor, and Esquel Group have upgraded to automated and laser-based cutting platforms to enhance throughput and meet international quality standards.

Demand is also rising from sectors such as electric vehicles and aerospace, with companies such as BYD and COMAC leveraging composite materials. Japan focuses on precision applications in technical textiles, using high-end digital and CNC cutters for composites, filtration media, and performance fabrics. India and Southeast Asia are rapidly modernizing, supported by initiatives such as India’s Production Linked Incentive (PLI) scheme and Vietnam’s industrial cluster incentives.

Major garment groups such as Arvind, Shahi Exports, and Makalot are adopting automatic spreading and cutting systems to improve efficiency. Investment trends include regional service center expansion by global OEMs, leasing and pay-per-use models, and software integration partnerships. Suppliers such as Lectra, Gerber, and Tukatech have strengthened local presence for faster support and training.

Competitive Landscape

The global fabric cutting machine market is moderately concentrated, with leading players offering integrated hardware-software solutions, while regional manufacturers dominate low- and mid-tier segments with cost-effective, customized offerings. Advanced automation and laser cutting show higher concentration due to R&D and service ecosystem demands.

Market leaders differentiate through software capabilities, nesting optimization, predictive maintenance, and robust service networks. Key strategies include product innovation, software-hardware integration, geographic expansion, and flexible financing for SMEs. Emerging trends such as pay-per-use models, AI inspection, and vision-assisted cutting further shape competitive advantages.

Key Industry Developments

- In February 2025, Lectra unveiled its VectorCUT Pro high-speed knife cutting system, featuring improved cut quality and material efficiency, reinforcing its product portfolio for apparel and technical textile manufacturers seeking productivity gains.

- In January 2025, Gerber Technology introduced its latest Paragon™ HP high-ply cutter, designed to increase cutting speed and accuracy for automotive interior and heavy technical fabrics, reflecting growing demand for precision and throughput in industrial applications.

Companies Covered in Fabric Cutting Machine Market

- Lectra

- Gerber Technology

- Bullmer

- Tukatech

- FK Group

- Eastman Machine Company

- Yin Japan (YIN Group)

- Morgan Tecnica

- Zünd Systemtechnik

- Kuris Spezialmaschinen

- IMA Spa

- Hashima

- Pathfinder Cutting Technology

- Oshima Machinery

- Richpeace Group

- Juki Corporation

- Tajima Group

- Shima Seiki

- Autometrix

- Kuris Cutting Systems

Frequently Asked Questions

The global fabric cutting machine market size is estimated at US$3.9 billion in 2026.

By 2033, the fabric cutting machine market is projected to reach US$6.4 billion.

Key trends include growing adoption of laser and digital cutting technologies and rising demand for automation, CAD/CAM integration, and smart cutting rooms.

By cutting method, straight-knife cutting is the dominant method.

The market is expected to grow at a CAGR of 7.3% between 2026 and 2033.

Major companies include Lectra SA, Gerber Technology (a part of Lectra Group), Bullmer GmbH, Tukatech Inc., and FK Group.