- Metals & Minerals

- Stainless Steel Fabrication Market

Stainless Steel Fabrication Market Size, Share and Growth Forecast, 2026-2033

Stainless Steel Fabrication Market by End-Use Industry (Construction, Infrastructure, Automotive, Transportation, Others), Grade (100 Series, 200 Series, 300 Series, 400 Series, Duplex Series), and Regional Analysis for 2026 - 2033

Stainless Steel Fabrication Market Share and Trends Analysis

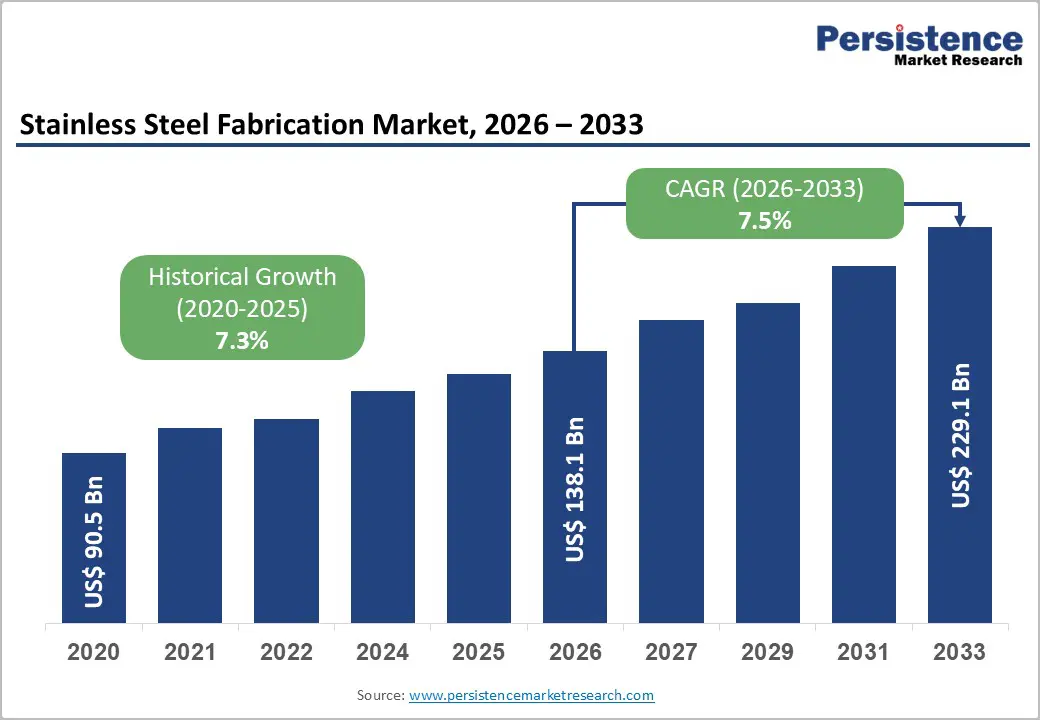

The global stainless steel fabrication market size is likely to be valued at US$138.1billion in 2026, and is projected to reach US$229.1billion by 2033, growing at a CAGR of 7.5% during the forecast period 2026–2033. This projection reflects strong demand across key end-use industries such as construction, automotive, transportation, and industrial manufacturing, where stainless steel is favored for its durability, corrosion resistance, and low maintenance requirements. Growth is primarily driven by accelerating global infrastructure development, particularly in Asia Pacific and North America, where urbanization, smart city initiatives, and large-scale transportation projects are increasing material requirements. Advancements in fabrication technologies, including automated welding, computer numerical control (CNC) processing, and precision cutting, are further enhancing production efficiency, scalability, and product quality. Rising urban populations, coupled with stricter quality, safety, and sustainability regulations, are further reinforcing stainless steel’s role as a preferred material in modern industrial and construction applications.

Key Industry Highlights

- Dominant End-Use Industry: Construction is set to command around 37% revenue share in 2026, while automotive is likely to grow the fastest at about 8.2% CAGR through 2033, driven by urbanization and transport electrification.

- Dominant Grade: 300 series stainless steel is anticipated to hold approximately 42% of total usage in 2026, while duplex series is expected to be the fastest-growing at roughly 9.1% CAGR through 2033, due to its superior strength and corrosion resistance.

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 38% share in 2026 and grow at an estimated 2026-2033 CAGR of 8.5%, fueled by large-scale infrastructure and manufacturing expansion.

- Competitive Environment: Market leaders are expanding production capacity, adopting automation, and forming partnerships to improve efficiency and meet rising high-performance demand.

- June 2025: Nippon Steel completed its US$ 14.9billion acquisition of U.S. Steel, creating one of the world’s largest steel producers with an annual crude steel capacity of 86million tons per annum (TPA).

| Key Insights | Details |

|---|---|

|

Stainless Steel Fabrication Market Size (2026E) |

US$ 138.1 Bn |

|

Market Value Forecast (2033F) |

US$ 229.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rapid Expansion of Construction, Infrastructure, and Automotive Sectors

The construction, infrastructure, and automotive sectors collectively drive significant demand for stainless steel fabrication. Urbanization and large scale investments in buildings, bridges, railways, airports, and industrial facilities require durable, corrosion resistant, and low maintenance materials, making stainless steel the preferred choice. Expansion of modern transport systems and electric vehicle production further increases demand for high strength materials used in structural frames, battery housings, and exhaust systems. This multi sector demand is supported by ongoing government infrastructure spending and broader industrial modernization agendas across key regions such as Asia Pacific, Europe, and North America.

Recent global developments further validate this trend. China exported over 5million tons of stainless steel in 2025, reflecting strong fabrication output and competitive positioning ahead of new export licensing controls effective January 2026, as reported by customs authorities. At the same time, Asia Pacific and North America are prioritizing transport electrification and highway/metro upgrades, enhancing long term material consumption. In Europe, renewed infrastructure funding and sustainability standards are increasing stainless steel adoption for long life structural systems. These macro trends collectively ensure that stainless steel fabrication will remain central to global industrial and infrastructure growth.

Technological Advancements and Industry 4.0 Integration

Emerging digital manufacturing technologies, such as robotics, AI assisted welding, and automated CNC systems, are transforming stainless steel fabrication by enhancing precision, throughput, and operational efficiency. Automation and process digitization reduce labor dependency, minimize variability, and shorten lead times, allowing fabrication facilities to deliver high quality, customized solutions at scale. Integration with Industry 4.0 practices, including connected machinery and real time data analytics, enables actionable performance insights and adaptive production workflows, strengthening competitiveness in an increasingly demanding market environment. These advancements also support sustainability goals by optimizing material usage and reducing energy intensity across production stages.

Industry movements underscore this technological push. In Europe, producers such as Aperam have invested in advanced facilities and digital controls to improve efficiency and respond to regulatory incentives tied to emissions and quality standards, enhancing fabrication capability and resilience. Meanwhile, Asia Pacific fabrication hubs are incorporating smart automation and precision tools to serve booming construction and automotive sectors. In North America, leading fabricators are deploying integrated automation and data systems to meet stringent safety and quality requirements, reflecting a global shift toward innovation led fabrication excellence.

Volatility in Raw Material Prices

A key structural challenge for the stainless steel fabrication market is the volatility in prices of essential raw materials, particularly nickel and chromium, which directly affect fabrication costs. Nickel and chromium markets are highly sensitive to supply demand imbalances, policy shifts, and export restrictions, leading to price unpredictability that complicates procurement strategies and cost forecasting. For example, constrained output or policy changes by major producers can cause sharp swings in prices, forcing fabricators to adjust pricing or compress margins to remain competitive.

This volatility was evident in early 2026 when Asian nickel prices rose sharply following Indonesia’s intention to restrict nickel ore mining, pushing spot prices significantly higher on raw material exchanges. Such movements ripple through fabrication supply chains, increasing alloy input costs at a time when downstream manufacturers are already managing tight margins. At the same time, fluctuating nickel availability due to production quota uncertainty and supply chain disruptions reinforces how fragile raw material pricing can impact stainless steel cost structures. These dynamics contribute to unstable contract terms and heighten risk for capital intensive end users reliant on long dated material commitments.

Environmental & Regulatory Compliance Costs

Stringent environmental and regulatory frameworks, such as the European Union (EU)’s Carbon Border Adjustment Mechanism (CBAM) that became operational in January 2026, are adding compliance costs and complexity for stainless steel producers and fabricators. CBAM imposes charges based on the embedded carbon emissions of imported goods, requiring additional reporting and cost calculations before importers can clear materials into EU markets. As a result, suppliers face increased regulatory burden and operational expenses, including emissions measurement systems and documentation processes that can extend lead times and erode margin flexibility.

Verified industry reporting highlights that, with CBAM entering its payment phase at the start of 2026, some steel and aluminum exporters are expected to cut export prices by up to 15–22% to compensate for the carbon cost passed on by EU importers and remain competitive in the region. This has pressured pricing strategies and influenced supplier selection criteria in global contracts, especially for high carbon footprint production routes. Moreover, difficulties in understanding new compliance coefficients and documentation published in late 2025 have led to unexpected cost surprises for steel importers, further illustrating how regulatory evolution can restrain agile expansion. These regulatory impacts create significant compliance and cost barriers, especially for small and medium sized fabricators without robust carbon reporting infrastructure.

Expansion in Emerging Markets and Industrial Growth

Emerging economies continue to represent significant growth opportunities for stainless steel fabrication, driven by sustained industrialization, large capital expenditure projects, and rising material demand across sectors. In regions such as Asia Pacific, Latin America, and select African markets, governments are prioritizing large-scale infrastructure programs, including urban development, transport networks, and manufacturing capacity expansions, that elevate the need for durable and corrosion-resistant materials. These macroeconomic trends underpin broad demand for fabricated stainless steel in construction frameworks, heavy machinery components, and transportation systems as firms scale operations.

China exported over 5.0million tons of stainless steel in 2025, reflecting strong production capacity and global trade flows ahead of new export license controls in 2026, according to the General Administration of Customs of China. Beyond China, India secured INR 11,887 crore (roughly US$ 1.43 billion) in investment commitments under the Speciality Steel PLI Scheme 1.2, supporting expansion of domestic stainless and specialty steel capacities by 8.7 million tonnes through FY 2031. Global stainless production grew at around 3% in the first nine months of 2025, indicating rising availability of material to support industrial, construction, and automotive fabrication demand. These developments highlights that emerging markets are not only growth engines but also strategic hubs for production and export, reinforcing long-term fabrication opportunities.

Adoption of Sustainable, Circular, and Specialized Fabrication Practices

Sustainability, circular economy initiatives, and specialized high-performance fabrication remain strategic opportunities for market participants. The 100% recyclability and long lifecycle of stainless steel align with increasing regulatory emphasis on low-carbon materials in construction, industrial manufacturing, and consumer goods. Manufacturers who embed recycled content, energy-efficient processes, and emissions-lowering technologies can meet both regulatory requirements and customer sustainability mandates, unlocking policy incentives and premium value segments.

Industry movements in the past years further validate this opportunity. Toyota Tsusho America completed the acquisition of Radius Recycling, Inc., a major North American metal recycling company, enhancing the supply of high-quality recycled steel resources and supporting broader circular economy goals. Meanwhile, European producers are investing heavily in low-emission, energy-efficient steel production, such as ArcelorMittal’s € 1.3billion electric furnace in Dunkirk, France, aligning fabrication processes with sustainability mandates and market expectations. The growing adoption of specialized stainless solutions in high-performance sectors, medical equipment, semiconductor manufacturing, and renewable energy infrastructure, also offers higher-margin, value-added opportunities. These developments position fabrication companies to leverage eco-conscious demand and precision-engineered applications, expanding reach and differentiating offerings in a competitive global market.

Market Restraints

Fluctuating Raw Material Costs

One of the primary growth restraints faced by the stainless steel fabrication market is the volatility in raw material costs. Stainless steel fabrication heavily relies on stainless steel as its primary raw material, and fluctuations in steel prices due to factors such as supply chain disruptions, trade tensions, and geopolitical instability can significantly impact fabrication costs.

Pricing fluctuations make it challenging for fabrication companies to accurately forecast production expenses and pricing strategies, leading to potential margin pressures and reduced profitability. Moreover, sudden spikes in raw material costs may deter potential clients from initiating new projects or prompt existing clients to seek alternative materials or suppliers, thereby hindering market growth.

Market Fragmentation

Another growth restraint for the stainless steel fabrication market is the presence of intense competition and market fragmentation. The market is characterized by numerous small to medium-sized fabrication companies competing for market share alongside larger established players. This saturation often leads to price wars, reduced profit margins, and compromises in product quality as companies strive to attract and retain customers.

The barriers to entry in the fabrication industry are relatively low, resulting in the emergence of new competitors and further intensifying competition. In such a competitive landscape, differentiation based on factors like technology, service quality, and innovation becomes crucial, posing challenges for smaller players with limited resources to invest in these areas and potentially impeding overall market growth.

Category-wise Analysis

End-Use Industry Insights

The construction segment is expected to lead the stainless steel fabrication market revenue share at an estimated 37%, driven by robust public and private investments in transportation hubs, bridges, commercial buildings, and industrial facilities where stainless steel’s strength, corrosion resistance, and long lifecycle enhance structural reliability and reduce maintenance costs. Sustained infrastructure capital expenditure and modernization programs across North America and Europe are reinforcing consistent procurement cycles and stable demand. For example, U.S. Steel restarted the blast furnace at its Granite City Works facility in late 2025 to meet rising customer demand, reflecting confidence in infrastructure related steel consumption ahead of 2026, while broader steel demand in major economies is projected to rebound modestly on the back of public infrastructure spending and improved financing conditions, underscoring continued market strength.

The automotive segment is anticipated to be the fastest growing end use category in stainless steel fabrication, projected to expand at approximately 8.2% CAGR through 2033, supported by electrification of vehicles, lightweight design mandates, and stricter emissions standards that increase demand for high strength, corrosion resistant stainless steel components in structural frames, exhaust systems, battery enclosures, and thermal management applications. Rising global vehicle production, notably in Asia Pacific, continues to broaden the volume of stainless steel used in passenger and commercial vehicles, reinforcing material adoption in new platform architectures. Specialized automotive stainless steel tube markets are growing rapidly as automakers increasingly prioritize lightweight and efficient components to meet performance, emissions, and safety requirements, further solidifying this segment’s above average growth trajectory.

Grade Insights

The 300 Series grade is most likely to lead with an estimated 42% of the stainless steel fabrication market share in 2026, valued for its corrosion resistance, weldability, and versatility across construction, industrial, automotive, and food processing applications. Its balanced mechanical and chemical properties suit architectural structures, process tanks, and structural frames, ensuring long lifecycle performance with minimal maintenance. In 2025, POSCO International expanded stainless steel exports, emphasizing high nickel 300 Series alloys for electrification and structural applications globally. High value 300 Series output continues to dominate key manufacturing hubs, with growing deployment in emerging energy and mobility sectors, including battery enclosures and fuel cell components, reinforcing its strategic importance.

The duplex series stainless steel grade is poised to be the fastest-growing, with a projected 9.1% CAGR, driven by its high strength-to-weight ratio and superior corrosion resistance for offshore, chemical, desalination, and high-stress industrial applications. Its performance advantages make it ideal for long-lifecycle, safety-critical structures. In 2025, Nippon Steel introduced a new duplex grade for offshore wind turbine components, highlighting innovation tailored to renewable energy and industrial infrastructure. Adoption is rising in marine, desalination, and advanced process equipment, signaling broader strategic deployment and solidifying duplex as the fastest-growing grade in stainless steel fabrication.

Regional Insights

North America Stainless Steel Fabrication Market Trends

North America is a significant contributor to the global market for stainless steel fabrication, with the United States leading regional demand due to federal infrastructure projects, industrial modernization, and expansion in aerospace and defense manufacturing. Stainless steel is favored for its durability, recyclability, and long lifecycle, aligning with stringent environmental and energy efficiency regulations. Automation, advanced fabrication technologies, and digital quality systems enhance production efficiency and support high-value, customized applications. Strong regional supply chains, proximity to raw material sources, and diversified procurement strategies help mitigate volatility risks and maintain consistent output.

Recent industrial movements further reinforce market stability. General Motors expanded its U.S. electric vehicle (EV) manufacturing operations, increasing stainless steel usage in structural and battery components for electric vehicles, reflecting sustained industrial demand. Meanwhile, major infrastructure upgrades in California and New York continue to drive procurement of corrosion-resistant stainless steel components for bridges, public transit, and commercial facilities. These initiatives demonstrate ongoing investment in durable, long-lasting materials, consolidating North America’s position as a stable yet technologically advanced market in the global fabrication landscape.

Europe Stainless Steel Fabrication Market Trends

Europe’s stainless steel fabrication market is supported by strong industrial infrastructure and a mature manufacturing base across Germany, France, Spain, and the U.K. Investments in rail networks, renewable energy plants, and commercial facilities continue to drive demand for stainless steel, valued for its recyclability, corrosion resistance, and long lifecycle. Regulatory frameworks, including carbon emissions limits and sustainability mandates, influence material selection and production processes, encouraging the adoption of eco-friendly fabrication practices. Automation, precision manufacturing, and digital quality controls further enhance competitiveness among regional fabricators, particularly for high-value industrial applications.

ArcelorMittal announced a € 1.3 billion low-emission furnace project at its Dunkirk facility, reflecting investment in sustainable steel production that supports fabrication downstream. Meanwhile, Germany’s expansion of wind farm and rail infrastructure projects requires large volumes of corrosion-resistant stainless steel for structural components. France and Spain are also increasingly using stainless steel in modernized commercial and transport facilities with sustainability and energy efficiency considerations. These initiatives demonstrate the region’s steady, innovation-driven growth while balancing regulatory compliance with market demand.

Asia Pacific Stainless Steel Fabrication Market Trends

Asia Pacific is projected to be the largest and fastest-growing regional market for stainless steel fabrication, holding an estimated 38% share with a projected CAGR of 8.5%, fueled by massive infrastructure development, industrial expansion, and rising automotive production. China dominates, with urbanization, transportation networks, and export-oriented manufacturing driving broad stainless steel application. India and ASEAN economies are increasingly adopting high-value fabrication and specialized products, supported by renewable energy investments and urban growth.

Recent industry activities reinforce this growth. In 2025, China’s Baosteel commissioned a new high-capacity fabrication line for structural and automotive stainless steel components, meeting domestic and export demand. Similarly, India’s state-backed metro and smart city projects increased procurement of stainless steel frameworks and industrial components. Competitive dynamics include dense regional fabricator networks, partnerships with global original equipment manufacturers (OEMs), and adoption of automation to enhance throughput. Combined with cost-efficient manufacturing and favorable policy support, Asia Pacific remains the key driver of global stainless steel fabrication market expansion.

Competitive Landscape

The global stainless steel fabrication market exhibits a moderately consolidated structure, with leading players such as Acerinox, Outokumpu, POSCO, Nippon Steel, and Jindal Stainless controlling a significant portion of market revenues. These established companies leverage extensive global distribution networks, strong client relationships across construction, automotive, and industrial sectors, and in-house expertise in advanced fabrication technologies. They also invest in automation, robotics, and digital manufacturing systems to enhance precision, reduce lead times, and maintain competitive advantage.

Regional and niche players, including Allegheny Technologies, Aperam, and Dongkuk Steel, focus on specialized applications, high-alloy grades, and localized markets. Barriers such as capital-intensive equipment, stringent quality standards, and raw material volatility restrict new entrants, but technological advancements, such as Industry 4.0 integration, AI-assisted welding, and additive manufacturing, enable smaller firms to participate in high-value segments. Market consolidation is expected to continue gradually, as leading manufacturers expand through strategic partnerships, acquisitions, and international capacity expansion, while innovation-driven firms target niche or high-performance applications.

Key Industry Developments

- In October 2025, Jindal Stainless inaugurated its first stainless steel fabrication unit in Mumbai with an investment of approximately INR 125 crore, aimed at strengthening downstream value-added capabilities and improving proximity to key customers in infrastructure and industrial sectors.

- In August 2025, JSW Steel and POSCO signed a non-binding Heads of Agreement to explore a 6 MTPA integrated steel plant in Odisha, India. The collaboration aims to combine operational expertise and advanced technology, with potential expansion into renewable energy and EV battery materials.

- In August 2025, Guangxi Hongyi New Materials inaugurated its first phase of a 1 million TPA high-end stainless steel processing facility in Wuzhou, China. The automated plant focuses on cold-rolled, 2B-grade surface finishes, aiming to boost the region’s industrial value chain and generate an annual output value exceeding CNY 10 billion.

Companies Covered in Stainless Steel Fabrication Market

- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- Jindal Stainless

- Acerinox S.A.

- Outokumpu Oyj

- Sandvik AB

- Thyssenkrupp Stainless GmbH

- Allegheny Technologies

- Tata Steel Long Products

- JFE Steel Corporation

- Aperam SA

- Yieh United Steel Corp.

- Baosteel Group

- JSW Steel

Frequently Asked Questions

The global stainless steel fabrication market is projected to reach US$ 138.1 billion in 2026.

Large-scale infrastructure development, automotive electrification, and industrial modernization are driving the market.

The market is poised to witness a CAGR of 7.5% from 2026 to 2033.

Massive steel production in China and India and widening adoption of sustainable, high-performance fabrication practices are opening high-value opportunities for market players.

Key players in the market include ArcelorMittal, Acerinox, Outokumpu, POSCO, Nippon Steel, and Jindal Stainless.