- Advanced Materials

- Fire Resistant Fabrics Market

Fire Resistant Fabrics Market Size, Share, and Growth Forecast 2026 - 2033

Fire Resistant Fabrics Market by Fabric Type (Inherent, Treated, Hybrid), Material (Cotton, Nylon, Aramid, Polyester, Wool, Fiberglass, Other), Processing Method (Woven, Non-woven, Knitted), Industry (Industrial Safety, Defense, Firefighting, Transportation, Other), and Regional Analysis for 2026 - 2033

Fire Resistant Fabrics Market Size and Trend Analysis

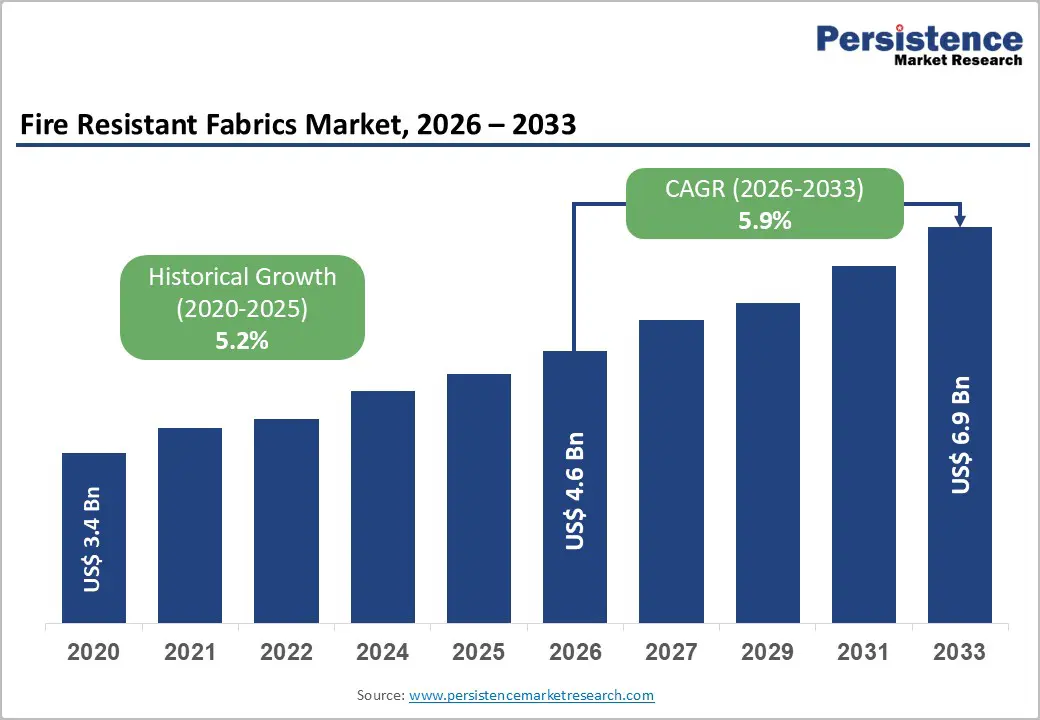

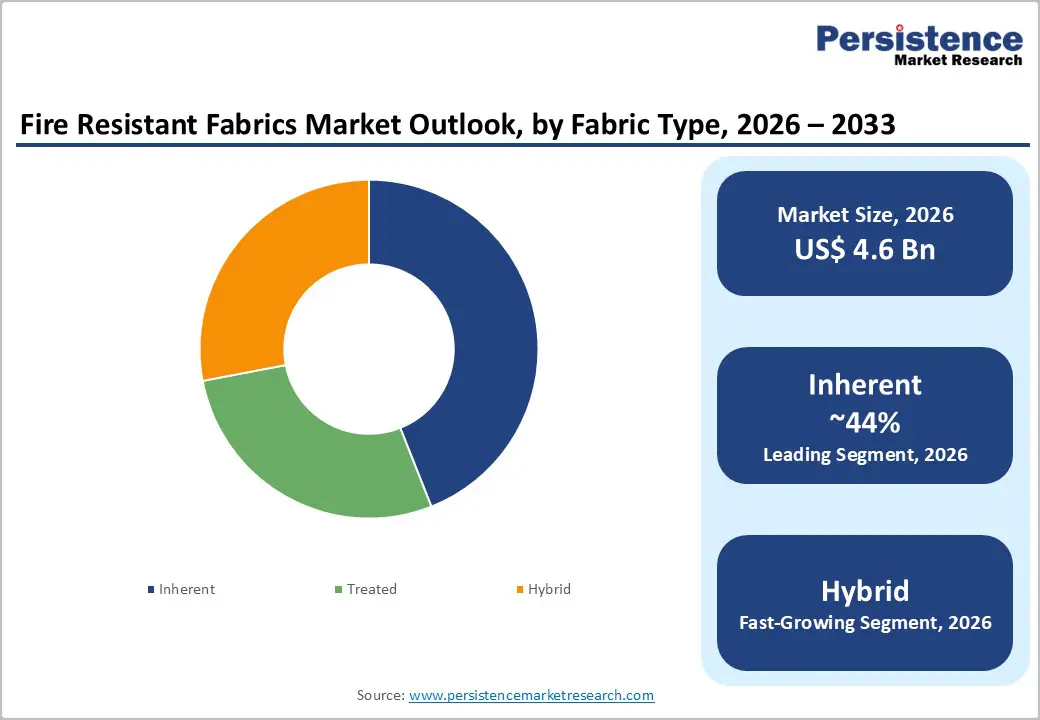

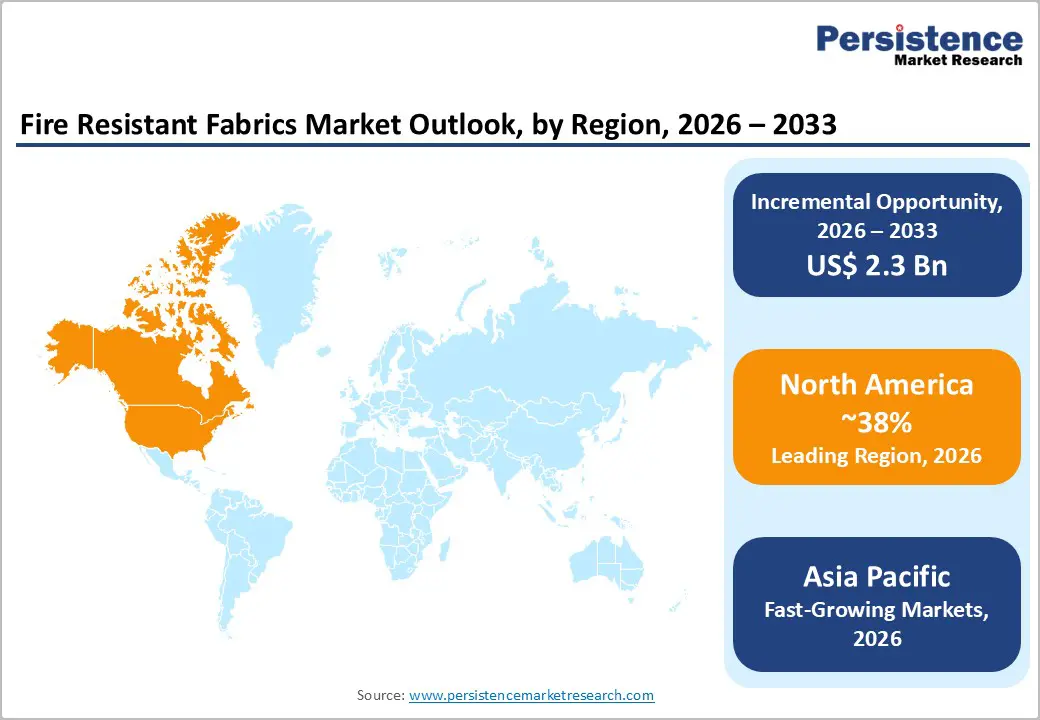

The global fire resistant fabrics market size is expected to be valued at approximately US$ 4.6 billion in 2026 and is projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033. This sustained growth is anchored in tightening global occupational safety regulations that mandate flame-protective personal protective equipment (PPE) across oil and gas, electrical utilities, and chemical processing industries, combined with escalating defense procurement and expanding firefighting infrastructure investment across emerging economies.

Workplace accidents and occupational diseases cost about US$3.9 trillion annually, strengthening regulatory and risk-management commitment to flame-protective workwear and sustaining steady demand for certified fire-resistant fabrics.

Key Industry Highlights:

- Leading Region: North America leads the global FR fabrics market with approximately 38% global revenue share in 2025, anchored by comprehensive OSHA, NFPA 2112, and NFPA 70E regulatory mandates driving non-discretionary FR workwear procurement across oil and gas, electrical utility, and chemical processing sectors.

- Fastest Growing Region: Asia Pacific is projected to register a leading CAGR, driven by expanding industrial safety regulation enforcement in China and India, escalating defense spending across the region, and rapid growth in the chemical and oil and gas sector workforces requiring certified FR workwear compliance.

- Dominant Fabric Type: Inherent fire resistant fabrics lead with approximately 44% market share in 2025, entrenched by their performance permanence throughout garment service life, retaining certified flame resistance regardless of laundering cycles, making them mandatory specifications in military, firefighting, and highest-risk industrial applications.

- Fastest Growing Fabric Type: Hybrid fire resistant fabrics are the fastest-growing fabric type, combining inherent FR fiber blends with treated finishes to achieve dual NFPA 2112 and ASTM F1506 arc flash certification at intermediate cost, capturing the growing multi-hazard protection requirement in electrical utility workwear programs.

- Key Opportunity: Emerging economy firefighting and defense procurement expansion, with CTIF reporting growing professional fire service workforces across Asia and the Gulf, creates high-value procurement demand for EN 469 and NFPA 1971 certified inherent FR fabric systems from suppliers with international standard compliance capabilities.

DRO Analysis

Drivers - Evolving Occupational Safety Standards Fueling Demand for Flame-Resistant Workwear

Workplace accidents and occupational illnesses impose an estimated US$3.9 trillion annual cost, pushing employers and regulators to strengthen safety programs. As enforcement tightens across high-risk industries, such as oil and gas, electrical utilities, and chemical processing, companies increasingly specify certified flame-protective PPE to limit liability and protect workers. This reinforces a risk-management mindset in procurement, where compliance is treated as non-negotiable rather than discretionary.

Because protective garments must be purchased, documented, and replaced on defined wear cycles, demand becomes recurring instead of one-time. The result is steady, compliance-driven consumption of certified fire-resistant fabrics, supporting market growth even during periods of broader industrial spending uncertainty.

Defense Sector Expansion Strengthening Demand for Fire-Resistant Technical Textiles

Global defense spending is rising, driven by NATO’s 2% of GDP target and SIPRI’s estimate of USD 2.44 trillion in 2023, boosting demand for advanced fire-resistant fabrics in military uniforms, vehicle crews, and aircraft interiors. Military specifications typically exceed civilian workwear requirements, combining flame resistance with ballistic-fragment protection, camouflage durability after laundering, reduced infrared signature, and resistance to chemical and biological threats.

Aramid systems such as DuPont Nomex and Teijin Twaron are widely incorporated into procurement standards across the U.S., EU, and NATO partners, supporting recurring demand linked to modernization programs and fleet replacement cycles.

Restraints - Economic Constraints Slowing Uptake of High-Performance Fire-Resistant Fabrics

The premium pricing of inherent fire-resistant fabrics, particularly aramid-based solutions such as Nomex and Twaron, presents significant adoption challenges in price-sensitive industrial markets and developing economies. These fabrics typically range from USD 15–40 per meter, compared to USD 3–8 per meter for treated cotton alternatives, making upfront garment costs a critical factor for employers managing large workforces. Consequently, market penetration remains constrained across regions such as South and Southeast Asia, Sub-Saharan Africa, and Latin America, where regulatory enforcement is less stringent and procurement decisions prioritize initial cost over lifecycle value.

Treated FR Fabric Limitations: Increasing Replacement Cycles and Operational Risk

Chemically treated fire-resistant fabrics, in which flame-retardant compounds are applied to base materials such as cotton or polyester rather than embedded within the fiber structure, exhibit inherent performance limitations. The protective treatment degrades over time due to repeated laundering, mechanical wear, and chemical exposure, potentially reducing effectiveness below required safety thresholds defined by standards such as NFPA 2112 and EN ISO 11612. The Protective Clothing Council indicates that improperly maintained garments may lose compliance within 25–50 wash cycles, creating quality assurance risks and lowering buyer confidence.

Opportunities - Hybrid FR Textiles Combining Inherent Fibers and Treatments Fuel Market Expansion

Hybrid fire?resistant fabrics blend inherent FR fibers (e.g., modacrylic, FR viscose) with treated natural fibers to deliver higher performance at mid-range cost. They’re the fastest-growing category, positioned between premium aramids and lower-performing treated cotton. Demand is rising in North American electrical utilities as NFPA 70E compliance pushes employers toward single-fabric solutions that protect against both flash fire and arc flash.

Hybrid constructions certified NFPA 2112 and ASTM F1506 help simplify PPE programs while improving wearer comfort versus heavier aramid garments. Major suppliers such as Milliken and TenCate are investing in hybrid platforms, reporting Arc Thermal Performance Value (ATPV) levels around 8–12 cal/cm² alongside better comfort and workability.

Emerging Economies Driving Demand for Specialized Fire-Resistant Fabric Solutions

The firefighting end?use segment is becoming a high?growth outlet for premium fire?resistant fabrics as Asia Pacific, the Middle East, and Africa expand municipal and industrial fire-service capacity. CTIF notes rising firefighter workforce levels across Southeast Asia and the Gulf, creating recurring procurement needs for full structural ensembles, proximity suits, station wear, and vehicle-crew protection, built on inherent FR fabric systems compliant with EN 469 or NFPA 1971.

In parallel, NATO modernization programs are specifying next?generation combat uniforms using inherent FR textiles that also reduce infrared signature and improve moisture management, lifting fabric value versus standard industrial workwear.

Category-wise Analysis

Fabric Type Insights

Inherent fire?resistant fabrics lead the market, with about 44% share in 2025, because their protection is built into the fiber chemistry, not applied as a finish. As a result, flame resistance remains consistent throughout the garment’s service life, even after repeated laundering, abrasion, or exposure to chemicals, key advantages over treated alternatives that can lose effectiveness over time.

This permanence makes inherent fabrics the default choice in the highest?risk environments, including proximity and structural firefighting, military combat uniforms, and oil & gas hot?work operations where protection failure can be life?threatening. DuPont Nomex meta?aramid, a foundational inherent FR fiber, is widely specified across major protective standards such as NFPA 2112, EN ISO 11612, and MIL?C?83141, reinforcing steady, institutional demand.

Material Insights

Aramid dominates the material segment, with 38% share in 2025, because its high LOI (>28%), strength, and thermal stability make it essential for top-spec military, firefighting, and industrial PPE. Para-aramids such as DuPont Kevlar and Teijin Twaron add cut and ballistic-fragment resistance alongside flame protection, supporting military uniform demand.

Meta-aramids such as DuPont Nomex and Teijin Conex deliver the thermal protective performance required in proximity and structural firefighting. Industry sources such as AFMA note aramid use in protective apparel growing faster than the broader textile market, helped by stricter regulations and defense procurement. However, high fiber prices (roughly USD 25–30/kg for para-aramid) limit adoption in cost-sensitive, high-volume applications.

Processing Method Insights

Woven processing leads the processing method segment with approximately 68% market share in 2025, reflecting woven fabric's dominant position as the standard construction method for fire resistant garments across all end-use applications, from workwear shirts and trousers to military combat uniforms and structural firefighting turnout gear outer shells. Woven FR fabrics offer superior dimensional stability and controlled air permeability compared with non-woven and knitted alternatives.

Knitted FR fabrics are the fastest-growing processing method, gaining traction in base layer thermal underwear and arc flash balaclava applications where comfort stretch properties are performance requirements.

Industry Insights

Industrial safety leads the industry segment with approximately 42% share in 2025, encompassing a broad range of oil and gas, chemical processing, and metals and mining industry workwear applications. The concentration of petroleum and petrochemical industry workers in the Gulf of Mexico, North Sea, Middle East, and Asia Pacific industrial corridors, each operating under stringent hot work permit and flash fire risk PPE regulations, creates large, predictable procurement volumes for certified FR workwear fabrics.

The International Association of Oil and Gas Producers (IOGP) and American Petroleum Institute (API) both publish detailed guidance on FR clothing requirements for oil and gas operations, creating industry-standard specifications that align fabric procurement toward certified performance levels, sustaining the industrial safety segment's dominant revenue position through non-discretionary compliance spending.

Regional Insights

North America Fire Resistant Fabrics Market Trends & Analysis

North America is the world's most mature and regulation-intensive fire resistant fabrics market, shaped by the OSHA 29 CFR 1910.269 electrical utility FR clothing mandate, NFPA 2112 flash fire protection standard, and NFPA 70E arc flash standard, collectively creating a comprehensive regulatory framework that drives non-discretionary FR fabric procurement across oil and gas, electrical utilities, chemical processing, and manufacturing sectors.

U.S. Fire Resistant Fabrics Market Size

The United States commands approximately 82% of the North American fire resistant fabrics market, anchored by its extensive oil and gas production and refining infrastructure, the world's largest electrical utility sector, and the OSHA and NFPA regulatory frameworks that mandate FR workwear across both sectors.

Europe Fire Resistant Fabrics Market Trends, Drivers, & Insights

Europe is a highly regulated FR fabrics market defined by the EU PPE Regulation 2016/425 and harmonized performance standards, including EN ISO 11612, EN ISO 11611, and EN 469, that collectively mandate certified flame protective garments across industrial, welding, and firefighting applications throughout EU member states. The European Chemicals Agency (ECHA) regulations under REACH are progressively restricting legacy flame retardant compounds used in treated fabrics, accelerating the transition toward inherent and hybrid FR fabric alternatives across European garment manufacturers.

Germany Fire Resistant Fabrics Market Size

Germany holds approximately 22% of the European fire resistant fabrics market, driven by its world-class chemical industry, including BASF, Covestro, and Evonik operations requiring large FR workwear inventories, and its strong automotive manufacturing sector, where welding and hot work operations mandate EN ISO 11611 certified flame protective clothing.

U.K. Fire Resistant Fabrics Market Size

The United Kingdom accounts for approximately 16% of the Europe fire resistant fabrics market, anchored by its North Sea oil and gas production infrastructure requiring offshore worker FR workwear. The UK's Health and Safety Executive (HSE) enforcement of Personal Protective Equipment at Work Regulations 1992 sustains FR garment compliance demand.

France Fire Resistant Fabrics Market Size

France represents approximately 13% of the European fire resistant fabrics market, with demand driven by its nuclear energy sector and by France's active defense procurement under the French Armed Forces Programming Law (LPM 2024–2030). France's large petrochemical and aerospace manufacturing sectors further sustain industrial safety FR workwear demand at scale.

Asia Pacific Fire Resistant Fabrics Market Analysis

Asia Pacific is the fastest-growing regional market for fire resistant fabrics, propelled by expanding industrial safety regulatory enforcement and rapid growth in the oil and gas, chemical, and manufacturing sectors. The regional market is also rising due to escalating defense spending across China, India, and Southeast Asia.

China Fire Resistant Fabrics Market Size

China holds approximately 35% of the Asia Pacific fire resistant fabrics market and is simultaneously the world's largest FR fabric manufacturer, particularly of treated cotton FR workwear, and a rapidly expanding end-user market as GB/T occupational safety standards increasingly mandate FR clothing in chemical and petroleum industries.

India Fire Resistant Fabrics Market Size

India accounts for approximately 16% of the Asia Pacific FR fabrics market and is one of the region's fastest-growing country markets at approximately 7.0% CAGR through 2033. India's rapidly expanding oil refining capacity, with Reliance Industries and HPCL-Mittal Energy expansions, combined with the Factories Act and petroleum safety regulations mandating FR workwear for oil and chemical sector workers, is driving growing compliance procurement.

Japan Fire Resistant Fabrics Market Size

Japan represents approximately 14% of the Asia Pacific FR fabrics market, with demand anchored by its world-class chemical and petrochemical industries, nuclear power operations, and precision manufacturing sector. Japan's segment grows at approximately 4.8% CAGR through 2033, with Teijin's domestic aramid fiber operations sustaining a strong inherent FR fabric supply chain.

Competitive Landscape

The global fire-resistant fabrics market exhibits moderate consolidation within the premium inherent fiber and specialized fabric segment. Leading companies, including DuPont de Nemours, Teijin Ltd., Lenzing AG, Kaneka Corporation, and TenCate Protective Fabrics, collectively account for approximately 45–50% of premium segment revenues, supported by proprietary fiber technologies, compliance with international safety standards, and strong distribution networks. Key strategic priorities include the development of sustainable fiber solutions, hybrid fabric innovations for multi-hazard protection, and digital certification platforms.

Key Developments:

- November 2025: DuPont announced the launch of Tyvek® APX™, a next-generation disposable chemical protective fabric, marking a significant innovation in the fire-resistant and protective fabrics market. The product was unveiled at the A+A 2025 trade fair in Düsseldorf, Germany.

- April 2026: Lenzing Group unveiled its “Lenzing Solutions for Protective Wear”, a three-tier cellulosic fiber portfolio designed for next-generation fire-resistant (FR) and protective fabrics. The integrated system combines LENZING™ FR fibers (inherent protection), TENCEL™ Lyocell blends (hybrid protection), and FR-finished Lyocell solutions (cost-effective protection), marking the first unified cellulosic approach across multiple protection levels.

- January 2026: Indorama Ventures announced the launch of Trevira® CS Eco fabrics made using permanently flame-retardant fibers and yarns containing 50% recycled textile material, marking a significant advancement in sustainable fire-resistant fabric solutions.

Top Companies in Fire Resistant Fabrics Market

- DuPont de Nemours, Inc. (Wilmington, Delaware, USA), is the global leader in inherent FR fiber technology through its Nomex meta-aramid and Kevlar para-aramid brands, foundational materials for military, firefighting, and industrial FR fabric systems worldwide. DuPont's Nomex fiber is specified in most global military combat uniform FR standards and NFPA-compliant industrial protective garment programs, giving the company unmatched institutional procurement depth and brand authority in the premium inherent FR market segment.

- Teijin Ltd. (Osaka, Japan) is the world's second-largest aramid fiber producer, offering Twaron para-aramid and Conex meta-aramid inherent FR fiber systems for defense, firefighting, and industrial protective applications. Teijin's vertically integrated operations, spanning fiber production through technical fabric weaving and finished garment supply, enable comprehensive FR fabric solution delivery.

- Milliken & Company (Spartanburg, South Carolina, USA) is a leading specialty chemical and textile company whose Westex brand FR fabrics, including the UltraSoft and INDURA product families, are among the most widely specified treated and hybrid FR fabric systems in the North American oil and gas and electrical utility workwear markets. Milliken's BioSmart and bio-based FR treatment chemistry investments are advancing sustainable workwear solutions that meet both NFPA performance standards and corporate sustainability procurement criteria simultaneously.

Global Fire Resistant Fabrics Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 3.4 Billion |

|

Current Market Value (2026) |

US$ 4.6 Billion |

|

Projected Market Value (2033) |

US$ 6.9 Billion |

|

CAGR (2026–2033) |

5.9% |

|

Leading Region |

North America, ~38% market share (2025) |

|

Dominant Segment |

Inherent Fabric Type, ~44% market share (2025) |

|

Top-ranking Segment |

Aramid Material, ~38% market share (2025) |

|

Incremental Opportunity |

US$ 2.3 Billion |

Companies Covered in Fire Resistant Fabrics Market

- DuPont de Nemours Inc.

- Teijin Ltd.

- Lenzing AG

- Solvay S.A.

- Kaneka Corporation

- Indorama Ventures Fibers Germany

- TenCate Protective Fabrics

- Milliken & Company

- W. L. Gore & Associates Inc.

- Syensqo SV

- Gun Ei Chemical Industry Co. Ltd.

- Huntsman Corporation (Textile Effects)

- Bulwark FR (VF Corporation)

Frequently Asked Questions

The fire resistant fabrics market is projected to reach US$ 6.9 billion by 2033 at a CAGR of 5.9%, representing an incremental opportunity of US$ 2.3 billion, driven by expanding occupational safety regulatory mandates, global defense procurement growth, and firefighting infrastructure expansion across emerging markets.

The primary demand drivers are tightening occupational health and safety regulations, including OSHA 29 CFR 1910.269, NFPA 2112, and NFPA 70E in the U.S. and EU PPE Regulation 2016/425 across Europe, that mandate employer-provided certified FR workwear across oil and gas, electrical utility, and chemical sectors, combined with global military expenditure reaching a record USD 2.44 trillion in 2023 per SIPRI, driving advanced inherent FR fabric procurement for military combat uniform modernization programs globally.

Inherent fire resistant fabrics lead with approximately 44% share in 2025. Their leadership is sustained by the performance permanence that makes inherent FR fabrics mandatory in the highest-risk applications. DuPont's Nomex meta-aramid, specified in NFPA 2112, EN ISO 11612, and MIL-C-83141 military standards, anchors the inherent segment's dominant institutional procurement position.

North America leads the global fire resistant fabrics market with approximately 38% revenue share in 2025. The region's dominance is anchored by the world's most comprehensive FR workwear regulatory framework, encompassing OSHA, NFPA 2112, and NFPA 70E, that creates large-scale, non-discretionary, recurring procurement across millions of oil and gas, electrical utility, and chemical processing workers requiring employer-provided certified flame-protective personal protective equipment.

The most significant opportunity is the Asia Pacific firefighting and defense market expansion, with CTIF documenting rapid professional fire service workforce growth across Southeast Asia and the Gulf, and Asian defense spending reaching record levels per SIPRI, creating high-volume first-time procurement demand for EN 469 and NFPA 1971 certified inherent FR firefighting ensemble fabrics and advanced military FR textile systems in markets with minimal incumbent supplier presence.