- Advanced Materials

- Carbon Fiber Market

Carbon Fiber Market Size, Share, and Growth Forecast, 2025 - 2032

Carbon Fiber Market By Product Type (Continuous Carbon Fibers, Long Carbon Fibers, Short Carbon Fibers), Application (Aerospace & Defense, Automotive, Renewable Energy, Sports & Leisure, Others), Raw Material (PAN-based, Pitch-based, Rayon-based), and Regional Analysis for 2025 - 2032

Carbon Fiber Market Share and Trends Analysis

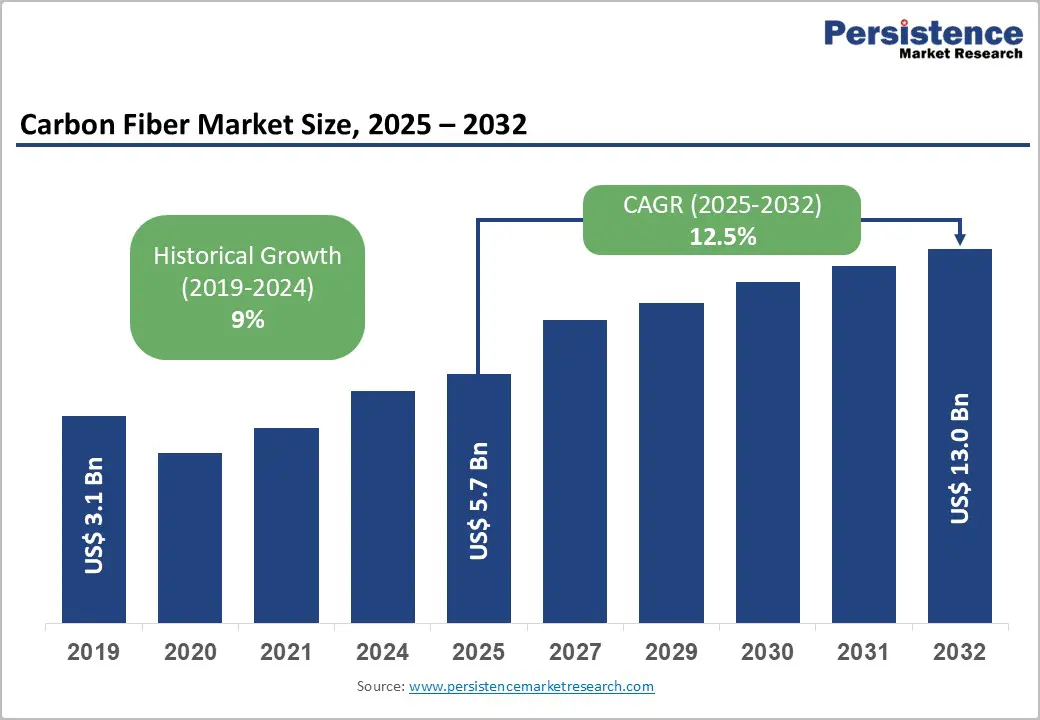

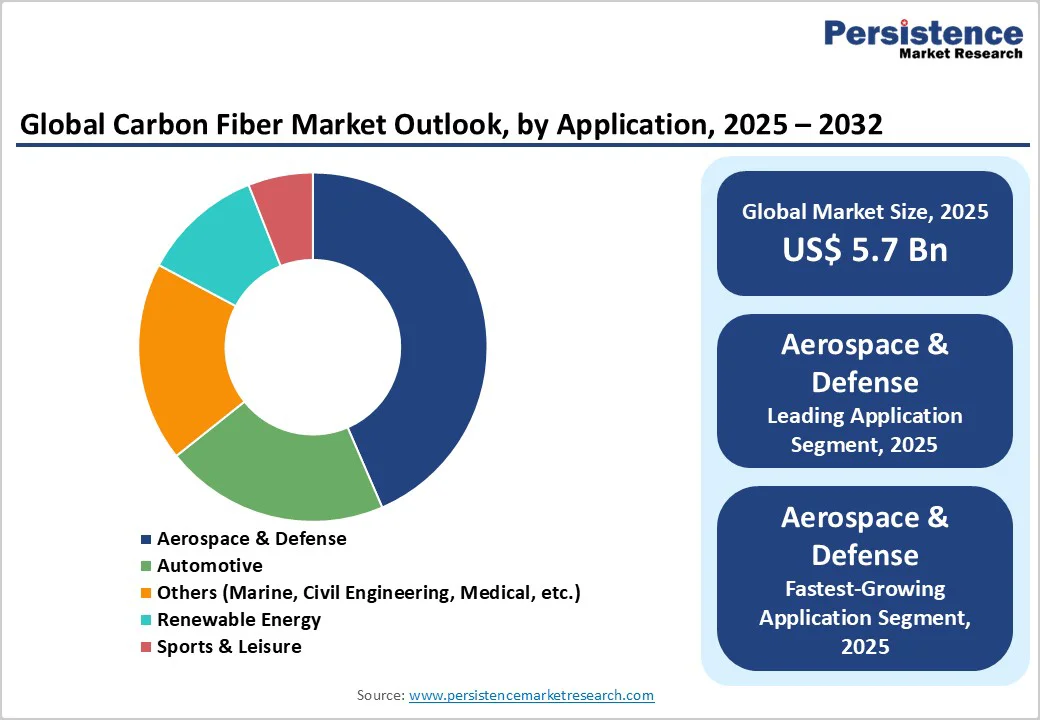

The global carbon fiber market is expected to reach US$5.7 billion in 2025. It is estimated to reach US$13.0 billion by 2032, growing at a CAGR of 12.5% during the forecast period 2025 - 2032, driven by the increasing demand for composite materials from critical industries such as aerospace & defense, automotive, and renewable energy.

Growth is driven by strict environmental regulations promoting lightweight materials, next-gen aircraft demand for high-strength composites, and advances enhancing carbon fiber quality and cost efficiency. Rapid industrialization across the Asia Pacific further boosts adoption and expands production capacity.

Key Industry Highlights

- Leading & Fastest-growing Raw Materials: PAN-based carbon fibers are set to dominate with a 72% market share in 2025; pitch-based fibers are likely to grow the fastest through 2032, owing to their suitability for aerospace applications.

- Leading & Fastest-growing Application: Aerospace & defense is set to remain the largest and the fastest-growing application segment, capturing around 43.5% market share in 2025 and registering a CAGR from 2025 to 2032.

- Dominant Region & Fastest-growing Regional Market: Asia Pacific commands the largest regional share of 40% in 2025, exhibiting the fastest growth, driven by China’s aggressive capacity expansion.

- Second-largest Regional Market: Europe is anticipated to hold a substantial 32.7% share in 2025, powered by Germany’s aerospace, automotive, and renewable energy sectors.

- Competitive Dynamics: Strategic acquisitions and partnerships are shaping the market's competitive landscape and addressing cost and sustainability challenges.

- Key Driver: Increasing regulatory pressure for lightweight materials and expansion in electric vehicles and renewable energy infrastructure are the prime growth accelerants for the market.

- October 2025: Kineco Exel Composites India (KECI) achieved full-scale production at its Banda facility, dedicated to manufacturing IEC 61400-5-certified carbon fiber components for the wind energy sector.

| Key Insights | Details |

|---|---|

| Carbon Fiber Market Size (2025E) | US$5.7 Bn |

| Market Value Forecast (2032F) | US$13.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 12.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Adoption in Aerospace & Defense

The aerospace & defense sector is one of the most lucrative drivers of carbon fiber market growth due to the material’s superior strength-to-weight ratio, corrosion resistance, and fuel-efficiency benefits. Carbon fiber composites constitute approximately 40-50% of the weight of modern commercial aircraft, as exemplified by the Boeing 787 Dreamliner, which extensively incorporates carbon fiber sandwich and laminate structures. This has led to a notable reduction in maintenance costs and improved aircraft performance.

Regulatory mandates to reduce carbon emissions and improve fuel economy are driving aerospace manufacturers to replace conventional metals with carbon fiber composites, thereby boosting market growth. With the global commercial aviation fleet expected to grow steadily over the next decade, the demand for lightweight composite materials is likely to intensify.

Government and military investment in advanced defense technologies also accelerates the adoption of carbon fiber for lightweight armor and weaponry, making aerospace & defense an indispensable sector for market expansion.

High Production Costs and Recycling Challenges

The high production cost of carbon fiber remains a significant barrier impeding broader market penetration. The cost of PAN-based carbon fibers, for instance, ranges around US$21.5 per kilogram, heavily influenced by precursor material costs and complex manufacturing processes with low yield efficiencies. This restricts affordability for smaller manufacturers and certain cost-sensitive end industries. The recycling and sustainability of carbon fibers present additional structural challenges.

Due to its composite nature, efficient recycling of these composites is difficult, often resulting in downcycling to lower-grade products and raising environmental concerns. Regulatory tightening in multiple geographies around hazardous emissions during manufacturing compounds these obstacles.

Development of Low-Cost Coal-Derived Carbon Fiber

Emerging research into converting coal tar, a by-product of coke production, into carbon fiber precursors opens new opportunities for cost reduction and enhanced market penetration. Projects led by collaborations among government bodies, large research organizations, and academic institutions are pioneering technologies to convert coal into high-performance carbon fiber composites, potentially multiplying the value of coal tar by a factor of many. This innovation addresses both raw material costs and sustainability by utilizing abundant, otherwise low-value feedstock sources.

If successfully commercialized, coal-derived carbon fibers could unlock new market segments, especially in automotive and construction, where cost sensitivity is highest. Market estimates suggest this opportunity could deliver significant incremental growth, repositioning carbon fiber as a more advanced yet accessible material.

Category-wise Analysis

Product Type Insights

Continuous carbon fibers are poised to dominate the global market, holding an estimated share of approximately 55% in 2025. This dominance is attributed to their superior mechanical properties, including high tensile strength and excellent fatigue resistance, making them the material of choice for demanding applications such as aerospace structures, high-performance automotive components, and sporting goods.

Continuous carbon fibers are predominantly used in advanced manufacturing processes such as filament winding, automated fiber placement, and pultrusion, as they enable precise control and consistent quality.

On the other hand, short carbon fibers are projected to be the fastest-growing product type from 2025 to 2032. Short fibers, typically ranging from a few millimeters to centimeters in length, offer advantages in cost efficiency and manufacturing flexibility, especially in injection molding and composite compounding processes.

Their increasing adoption is largely driven by expanding usage in automotive mass production, where short carbon fibers are integrated into thermoplastics to achieve lightweighting at comparatively lower costs. They also offer benefits, including enhanced stiffness and higher impact resistance, for consumer goods, electronic casings, and industrial parts, contributing to their rapid growth trajectory.

Application Insights

The aerospace & defense sector is set to remain the largest as well as the fastest-growing application, with an estimated market share of 43.5% 2025 from 2025 to 2032.

This dominance is chiefly driven by the relentless pursuit of the aircraft industry of weight reduction to improve fuel efficiency. Carbon fiber composites constitute around 40-50% of new aircraft structures, with aviation giants such as Boeing and Airbus emphasizing their extensive use.

In 2025, the automotive sector is likely to account for approximately 20.8% of the market share, driven by automotive original equipment manufacturers (OEMs)' push towards lightweight, fuel-efficient vehicles, especially in electric and hybrid models.

The incorporation of carbon fiber into body panels, chassis, and battery enclosures is accelerating due to regulations on vehicle emissions, supported by automakers' commitments to achieve sustainability targets. Wind energy applications are also expanding, leveraging carbon fiber for large blades that enable higher energy output and operational longevity.

Raw Material Insights

The dominant raw material for the carbon fiber market remains polyacrylonitrile (PAN)-based precursors, which are estimated to hold approximately 72% of the market share in 2025.

This segment’s dominance stems from its superior mechanical properties, including tensile strength exceeding 5 GPa and a modulus exceeding 250 GPa, making it highly suitable for aerospace, automotive, and high-performance sporting goods applications. The PAN-based fiber is also favored due to its mature technology, consistent quality, and cost advantages over alternative precursors such as pitch or rayon.

However, pitch-based carbon fibers are gaining momentum and are projected to grow at the highest CAGR during 2025 - 2032.

These fibers are characterized by their high thermal and electrical conductivity, which opens up niche applications such as electromagnetic shielding, high-temperature electronics, and specialized aerospace components. Innovations aim to reduce production costs, improve performance characteristics, and expand their application footprint, particularly in industries that demand high thermal stability and electrical conductivity.

Regional Insights

North America Carbon Fiber Market Trends

North America is expected to command an estimated 17.7% of the global market share in 2025, with the U.S. leading as the primary contributor, owing to its advanced aerospace, automotive, and defense industries.

The U.S. aerospace industry is highly innovative, with major OEMs such as Lockheed Martin investing heavily in lightweight composites. Regulatory frameworks such as the U.S. Clean Air Act and federal incentives for electric vehicle adoption are fueling demand for lightweight, efficient materials.

The region is also characterized by a robust innovation ecosystem, with significant R&D investments from industry leaders and government agencies such as DARPA, supporting breakthroughs in low-cost manufacturing and recycling technologies.

Infrastructure modernization and substantial venture funding are also driving regional expansion. Key investment trends include capacity expansion, strategic partnerships, and the adoption of recycled carbon fiber solutions, aiming to achieve sustainability goals.

Europe Carbon Fiber Market Trends

Europe is poised to hold an estimated 32.7% of the market share in 2025, supported by its aerospace giants, Airbus and Eurofighter, and a thriving automotive sector led by BMW, Mercedes-Benz, and Volkswagen. Germany, France, and Spain are actively developing wind energy and high-performance automotive markets, deploying carbon fiber composites to enhance efficiency and sustainability.

Regulatory harmonization across the European Union (EU), stringent implementation of environmental policies, and attractive incentives for green manufacturing are fostering a conducive environment for growth.

The focus on stakeholders in the European market on lightweight, high-performance components in aerospace, automotive, and renewable energy applications is propelling sectoral expansion. Investment in research clusters and collaborative supply chains further accelerates technological innovation and cost reductions.

Asia Pacific Carbon Fiber Market Trends

Asia Pacific is not only anticipated to be the largest but also the fastest-growing regional market. Set to account for approximately 40% of the carbon fiber market share in 2025 and post a high CAGR through 2032, rapid industrialization, urbanization, and government incentives favoring high-tech manufacturing are the prime growth determinants for the market here.

China, Japan, India, and ASEAN nations are central to this growth, with China spearheading capacity expansion with new manufacturing plants for both raw material production and composite integration.

The regional market also benefits from a competitive manufacturing landscape, low raw-material costs, and government policies that promote electric vehicles and renewable energy infrastructure. Japanese firms are leading in high-performance and high-temperature carbon fibers, meeting the demands of aerospace and electronics.

India is rapidly expanding its aerospace and automotive sectors, with local government incentives aimed at reducing import dependence. Regional investments are predominantly focused on innovation, scale of production, and sustainability.

Competitive Landscape

The global carbon fiber market structure is highly consolidated. The top companies, Toray Industries, Zoltek Corporation, SGL Carbon, Mitsubishi Chemical, and Teijin Limited, control about three-fourths of the market share in 2025. These leading firms possess extensive R&D capabilities, global manufacturing footprints, and diversified product portfolios, enabling them to innovate rapidly and meet customized customer needs.

The competitive landscape is characterized by high barriers to entry due to capital-intensive manufacturing processes, stringent quality standards, and complex supply chains. Market players are increasingly engaging in strategic acquisitions, joint ventures, and technology partnerships to expand production capacity, develop low-cost solutions, and address sustainability challenges.

Key Industry Developments

- In November 2025, Toray unveiled a recycling technology that maintains the strength and surface quality of carbon fibers, enabling reuse without performance loss. The innovation advances sustainability by supporting high-value applications of recycled composites, reducing waste, and improving resource efficiency across aerospace, automotive, and other carbon fiber-intensive industries.

- In October 2025, Cleantech startup Uplift360 and aerospace company Leonardo converted an end-of-life helicopter rotor blade into a prototype drone arm using Uplift360’s low-temperature ChemR recycling process. The project recovered high-quality carbon fiber, promoting sustainable aerospace manufacturing, supply chain resilience, and circular economy objectives under the U.K.’s Strategic Defence Review.

- In October 2025, Epsilon Composite acquired Italian partner Cometec Srl, a carbon fiber roller specialist, to expand its Italian presence and market reach. Building on 35 years of collaboration, the deal enhances supply chains, local service, and technological synergies while preserving Cometec’s identity and operational independence.

Companies Covered in Carbon Fiber Market

- Toray Industries Inc.

- Zoltek Corporation

- SGL Carbon

- Mitsubishi Chemical Carbon Fiber and Composites Inc.

- Teijin Limited

- Hexcel Corporation

- DowAksa USA LLC

- Formosa Plastics Corporation

- Holding Company Composite

- Hyosung Advanced Materials

- Solvay

- Anshan Sinocarb Carbon Fibers Co. Ltd

- Zhongfu Shenying Carbon Fiber Co. Ltd

- Jiangsu Hengshen Co. Ltd

- Nippon Graphite Fiber Co. Ltd

Frequently Asked Questions

The global carbon fiber market is projected to reach US$5.7 Billion in 2025.

Increasing demand for composite materials from critical industries such as aerospace & defense, automotive, and renewable energy, and stringent environmental regulations fostering lightweight alternatives in vehicle manufacturing are driving the market.

The carbon fiber market is poised to witness a CAGR of 12.5% from 2025 to 2032.

The expansion of next-generation aircraft requiring high-strength composites and technological advancements improving carbon fiber quality and cost efficiency are key market opportunities.

Toray Industries Inc., Zoltek Corporation, and SGL Carbon are a few of the key players in the carbon fiber market.