- Healthcare Services

- Revenue Cycle Management Market

Revenue Cycle Management Market Size, Share, and Growth Forecast, 2026 – 2033

Revenue Cycle Management Market by Component (Services, Cloud-based Software), Delivery Mode (Web-based, Others), Function (Claims & Denial Management, Medical Coding & Billing, Others), End-user (Hospitals, Physician Offices, Others), and Regional Analysis 2026 – 2033

Revenue Cycle Management Market Size and Trends Analysis

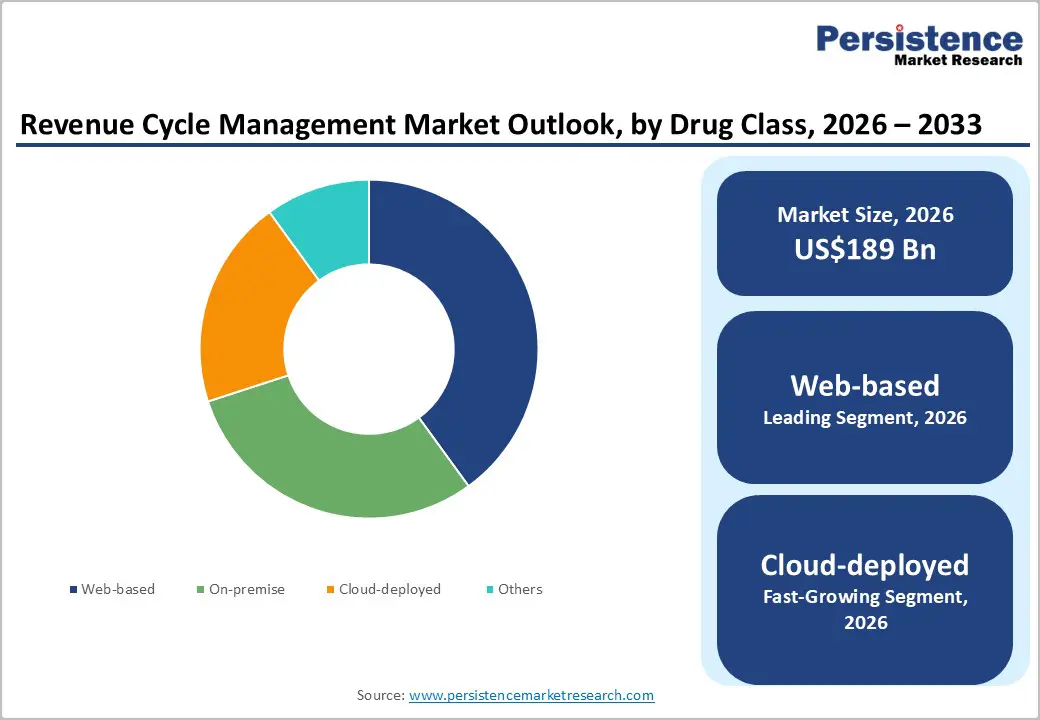

The global revenue cycle management market size is likely to be valued at US$189 billion in 2026 and is expected to reach US$400 billion by 2033, growing at a CAGR of 11.3% during the forecast period from 2026 to 2033, driven by increasing healthcare spending and regulatory pressures, which are pushing the adoption of RCM solutions to improve reimbursement processes and reduce denials.

Market growth is driven by the need to prevent revenue leakage, the adoption of AI automation to address staffing gaps, and the consolidation of providers seeking integrated financial platforms. As healthcare shifts to value-based care, RCM solutions are now a strategic priority for both operations and executive leadership to ensure financial sustainability amid tighter margins.

Key Industry Highlights:

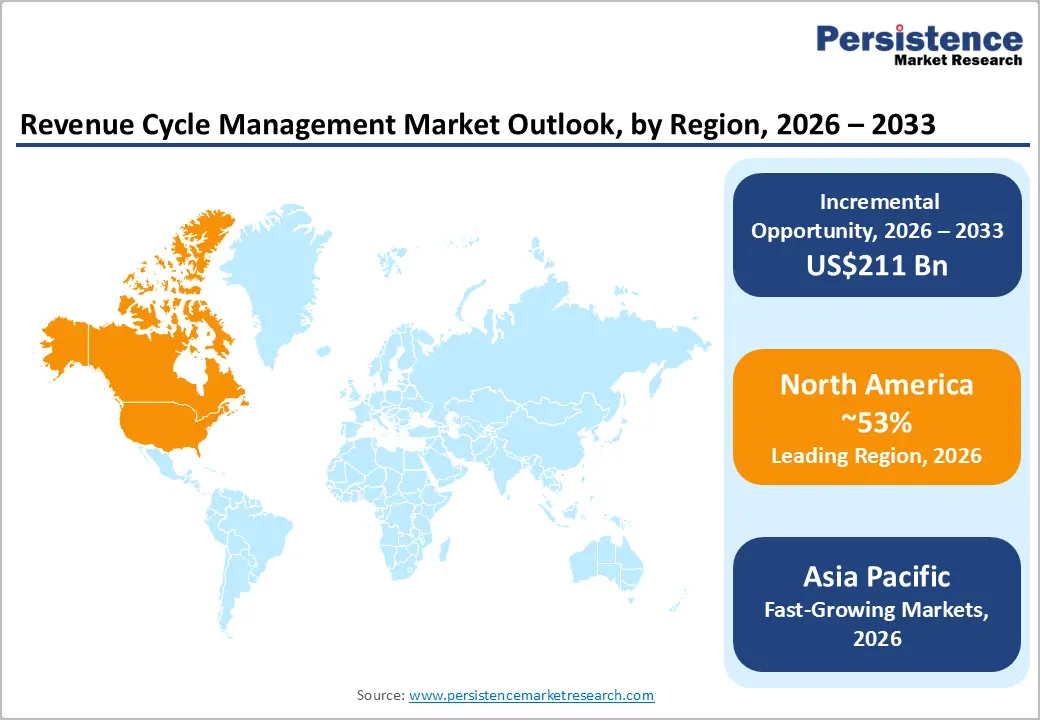

- Leading Region: North America is expected to lead the global revenue cycle management market, accounting for approximately 53% of the market, supported by complex reimbursement structures, high healthcare IT spending, early digital adoption, and stringent regulatory compliance requirements.

- Leading Delivery Mode: Web-based RCM solutions are expected to remain the leading delivery mode, accounting for approximately 53% of the market, as browser-accessible architectures enable faster deployment, lower upfront IT burden, and easier system access across distributed care networks.

- Leading End-user: Hospitals are expected to remain the leading end-user segment, accounting for approximately 61.90% of the market, driven by high patient throughput, complex case mixes, and the need for enterprise-grade revenue cycle platforms across inpatient and outpatient departments.

| Key Insights | Details |

|---|---|

| Revenue Cycle Management Market Size (2026E) | US$189 Bn |

| Market Value Forecast (2033F) | US$400 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.9% |

Market Factors – Drivers, Barriers, and Opportunity Analysis

Driver Analysis - Rising Healthcare Costs and Regulatory Compliance

The revenue cycle management (RCM) market is being driven by rising operational costs and increasingly complex regulatory requirements that reshape reimbursement dynamics. Hospitals and clinic networks face persistent margin pressure as labor, IT, and payer complexity grow faster than reimbursement, elevating RCM from a back-office function to a strategic margin-protection tool. Providers are prioritizing workflow automation, end-to-end platform integration, and embedded analytics to reduce administrative waste, stabilize cash flow, and prevent revenue leakage across eligibility, coding, billing, and collections. AI-enabled orchestration is accelerating adoption, allowing organizations to scale operations efficiently and decouple revenue performance from staffing volatility.

Regulatory shifts further amplify demand for modern RCM solutions. Value-based care models require tracking quality metrics, outcomes attribution, and contract-specific reimbursements, while price transparency mandates complicate pre-service estimation and compliance. Evolving coding standards and payer rules increase denial risk, making automated coding validation, rules engines, and audit trails essential. Together, cost containment and compliance pressures are driving consolidation toward cloud-native, interoperable RCM platforms that embed automation, governance, and security into everyday revenue operations.

Administrative Cost Containment and Workforce Capacity Constraints

Healthcare providers face sustained financial pressure as rising operating costs coincide with constrained availability of trained revenue cycle staff. Revenue cycle functions are labor-intensive, process-heavy, and highly error-sensitive, making manual workflows increasingly unsustainable. Staffing shortages across coding, billing, and claims management create backlogs, delayed reimbursements, and higher denial risk. As payer rules evolve and documentation requirements grow more complex, administrative burdens on limited teams intensify, compelling providers to adopt operating models that reduce manual dependence while maintaining compliance and cash flow stability.

Automation and AI-enabled RCM platforms directly address these challenges by handling repetitive, rules-based tasks across eligibility checks, prior authorizations, coding, claim submission, and denial management. Standardized digital workflows improve throughput consistency, reduce human error, and provide end-to-end visibility, allowing scarce staff to focus on higher-value tasks such as exception handling and payer negotiations. Technology-led labor substitution is shifting from an efficiency initiative to a strategic necessity. In June 2025, FinThrive introduced Agentic AI at HFMA, enabling autonomous workflows, real-time adjustments, and faster revenue recovery, operationalizing the transition from manual dependency to structural workforce replacement, a core driver of advanced RCM adoption.

Barrier Analysis: Workforce Displacement Risk and Skills Gap in AI-Driven RCM

The fear of technological unemployment is a significant restraint on AI-driven Revenue Cycle Management (RCM) adoption. Automation impacts core billing and coding workflows, raising concerns about role redundancy and long-term employability among administrative staff. Many healthcare organizations face a widening skills gap, as existing teams struggle to adapt to AI platforms, model-driven workflows, and exception-based processes. Limited training capacity and uneven access to structured reskilling programs slow readiness for large-scale automation. Consequently, leadership often delays or scales back AI deployments to avoid workforce disruption, labor relations challenges, and productivity shocks.

Operational resistance also slows implementation. Frontline staff may view AI as a replacement rather than an augmentation, reducing adoption and utilization. Partial automation in underprepared environments can temporarily increase denials and rework, creating near-term performance volatility and reinforcing executive caution. Until continuous upskilling frameworks mature, AI adoption will face structural drag. In June 2025, Ensemble Health Partners partnered with Firelands Health to deliver end-to-end AI-enabled RCM. By externalizing much of the automation to a specialized operator, the partnership reduces the immediate need for Firelands’ teams to master complex AI workflows, model supervision, and exception handling, enabling faster adoption while mitigating workforce disruption.

Opportunity Analysis: Outsourcing-Led Expansion and Global Delivery Models in RCM

The globalization of Revenue Cycle Management (RCM) delivery is creating a structurally attractive growth pathway, as providers seek scalable cost containment without compromising service continuity. Hybrid models combining domestic client-facing teams with offshore processing centers are gaining traction, enabling 24/7 eligibility checks, coding backlog clearance, and claims follow-ups. This approach improves throughput, shortens revenue cycles, and stabilizes administrative costs under persistent margin pressure. Vendors offering “RCM-as-a-Service” convert episodic outsourcing into long-term managed service contracts, enhancing revenue visibility, client retention, and resilience against demand volatility.

Emerging markets are also becoming growth centers as hospital networks professionalize billing, compliance, and payer engagement. Expanding insurance coverage, digitization of health records, and private hospital growth in Asia Pacific and Latin America are increasing demand for standardized RCM processes. Global vendors can leverage delivery footprints to localize offerings, support multilingual payer workflows, and deploy modular platforms suited to fragmented ecosystems. In September 2025, Ensemble Health Partners partnered with Benefis Health System to provide comprehensive RCM management. The collaboration integrates AI automation and expertise, streamlining operations, enhancing ROI visibility, and reinforcing the shift toward strategic, multi-year outsourcing to stabilize administrative costs and absorb demand fluctuations.

Cloud – EHR Convergence and Platformization of RCM

Cloud-native RCM platforms integrated with EHR systems are transforming provider economics by shifting revenue cycle operations from capital-intensive IT stacks to scalable, service-based models. Seamless interoperability enables automated charge capture, real-time eligibility checks, cleaner claims, and continuous denial prevention, reducing revenue leakage and shortening cash cycles. Multi-site hospitals and ambulatory networks benefit from standardized workflows, centralized governance, and remote access, while AI modules improve coding accuracy, documentation integrity, and payer rule orchestration without adding headcount.

Adoption is accelerating in Asia Pacific and Europe, driven by digital health reforms, payer modernization, and cloud-first mandates. Vendors offering secure, compliant, EHR-embedded suites, modular pricing, and configurable workflows for fragmented payer environments are positioned to capture disproportionate market share as cloud–EHR convergence becomes the default model for revenue cycle management.

Category–wise Analysis

Delivery Mode Insights

The web-based delivery mode is expected to remain the leading deployment model in the RCM market, accounting for approximately 53% share. Browser-based platforms provide the fastest path for AI integration, payer connectivity, and mobile-first patient engagement. Vendors such as Epic Systems, Oracle Cerner, Optum, Waystar, and R1 RCM are driving adoption among mid-sized hospitals and physician groups through rapid onboarding, zero on-prem hardware, and continuous feature updates for denial management and prior-authorization automation.

Embedded Agentic AI workflows help preempt coding and eligibility errors, while Text-to-Pay modules, IVR billing bots, and digital wallets integrated into Epic MyChart, Waystar Pay, and athenaOne enhance self-pay collections. FHIR API-based interoperability layers strengthen synchronization across Epic, MEDITECH Expanse, and ambulatory EHRs, reducing clinical–financial leakage. Security measures such as tokenization, device-agnostic access, and blockchain-backed audit trails reinforce trust in web-first stacks.

Cloud-deployed RCM is projected to be the fastest-growing deployment model as enterprise providers scale GenAI workloads that require hyperscale compute from AWS, Azure, and Google Cloud. Cloud-native platforms from Oracle Cerner, Waystar, athenahealth, and R1 RCM support agentic claim negotiation, propensity-to-pay scoring, and real-time denial triage. Vertical healthcare clouds and zero-trust architectures further enable secure, elastic, 24/7 revenue operations, positioning the cloud as the preferred AI-ready RCM backbone.

End-user Insights

Hospitals are expected to remain the leading end user in the RCM market, holding roughly 61.9% share, as enterprise-scale billing complexity across emergency care, inpatient episodes, surgical services, imaging, and in-house pharmacy drives demand for fully integrated financial platforms. Large systems are consolidating onto unified revenue platforms, with Epic Resolute, Oracle Cerner Revenue Management, Optum Change Healthcare, R1 RCM, and Ensemble Health Partners increasingly deployed as single-vendor suites to replace fragmented solutions.

Agentic AI adoption across Tier-1 networks is anticipated to automate denial recovery, medical necessity documentation, and undercoding detection directly within Epic, MEDITECH Expanse, and Oracle Health workflows. Provider-sponsored health plans and direct-to-employer contracting further heighten the need for adjudication-grade RCM capabilities, while pre-service automation via eligibility, estimates, and financial clearance tools from Waystar, Experian Health, and Zelis shifts revenue protection upstream. Enterprise security, tokenized payments, and high-availability cloud backbones remain standard requirements.

Physician offices are projected to be the fastest-growing end user as independent practices and specialty groups adopt enterprise-grade RCM to address staffing gaps and denial pressure. Cloud-native stacks from athenahealth, NextGen Healthcare, Tebra, and eClinicalWorks, combined with AI-assisted coding, charge capture, and documentation, enhance first-pass yield and cash cycles.

Specialty-focused revenue engines and offshore/nearshore operations expand operating leverage, while digital front-end payments increase patient-pay collections, enabling predictive charge capture and denial-preemption capabilities across ambulatory RCM.

Regional Insights

North America Revenue Cycle Management Market Trends

North America is expected to lead the RCM market, accounting for roughly 53% of global share, driven by large provider networks, early enterprise adoption of AI-enabled automation, and deep payer–provider integration across claims, eligibility, and prior-authorization workflows. Market momentum is shifting from rule-based automation to agentic AI capable of autonomously resolving denials, optimizing coding pathways, and coordinating with payer decision engines.

Nearshore delivery models are gaining traction as providers balance service quality, data security, and turnaround time for high-touch financial processes. Vendor consolidation is likely to intensify as large enterprises acquire AI-native specialists to deliver integrated clinical, administrative, and financial operating systems. Demand is further reinforced by workforce shortages in billing and coding, elevated denial rates affecting cash flow, and rising bad-debt exposure, which heightens the strategic value of predictive eligibility, propensity-to-pay scoring, and real-time denial prevention.

The U.S. is expected to anchor regional performance due to the complexity of its multi-payer system, regulatory pressure on price transparency, and accelerated adoption of cloud-native, EHR-integrated RCM platforms. Canada is projected to expand automation within hospital finance and provincial health systems, emphasizing interoperable claims workflows and digital patient-access tools. Key competitive players include Epic Systems with embedded RCM modules, Oracle Health (Cerner) with cloud-based revenue integrity, Optum with AI-driven analytics and managed services, and athenahealth with cloud-native workflows optimized for ambulatory and physician practices.

Europe Revenue Cycle Management Market Trends

Europe is expected to serve as the global anchor of stability in the healthcare RCM market, supported by government-led digital transformation agendas, strong public-sector dominance, and regulatory frameworks emphasizing data sovereignty and interoperability. Market growth is likely to be shaped more by national health system modernization, unified patient identity frameworks, and cross-border billing enablement under the European Health Data Space, rather than by payer-driven volatility.

Providers are expected to accelerate migration toward EU-native cloud infrastructure and sovereign data environments to meet privacy, residency, and security requirements, influencing vendor architecture decisions across billing, coding, and reimbursement workflows. AI adoption in RCM will likely focus on detecting fraud, waste, and abuse in public funds, while value-based procurement models prioritize reducing administrative burden, audit risk, and processing latency.

Germany is projected to anchor regional performance due to its large hospital network, dual-billing complexity across statutory and private insurance, and investments in interoperable digital health infrastructure. The U.K. will remain a key demand driver as NHS-led paperless mandates and front-end digitalization programs expand automated patient access, eligibility verification, and claims orchestration. Vendors, including Dedalus Group, CompuGroup Medical, Agfa HealthCare, and Oracle Health, are expected to emphasize support for sovereign cloud environments, open APIs, multilingual NLP for coding, federated AI, and human-in-the-loop governance to comply with the EU AI Act and evolving public procurement requirements.

Asia Pacific Revenue Cycle Management Market Trends

Asia-Pacific is likely to be the fastest-growing region, driven by the rapid digitization of care delivery, large-scale expansion of public coverage, and accelerated adoption of cloud-native, AI-enabled platforms. Health systems are bypassing legacy on-premise billing models and moving directly to automated workflows for eligibility verification, coding, claims routing, and patient collections.

Government-backed digital health infrastructures are enabling real-time claims orchestration across fragmented provider networks, while rising medical tourism and cross-border insurance utilization are driving demand for multi-currency, multi-payer billing solutions. Market momentum is further reinforced by universal health coverage programs, the adoption of DRG-based reimbursement in large hospitals, and the consumerization of healthcare payments through super-app ecosystems and conversational billing interfaces integrated into daily digital channels.

India plays a dual role as both a domestic growth center and a global IT services hub, amplifying regional influence on RCM worldwide. Large Indian health systems are scaling AI-driven billing platforms to manage high-volume government scheme claims alongside private insurance complexity, accelerating adoption of RPA, automated coding, and denial prevention.

Concurrently, India’s RCM IT and BPO services support providers in North America, Europe, and the Middle East, creating a feedback loop of capability transfer, platform maturity, and cost-efficient innovation. Key regional vendors, including Tencent Health, Alibaba Health, Apollo HealthRIS, Dedalus, and Oracle Health, are prioritizing super-app integration, localized data residency, Zero-Trust security, and edge-enabled billing workflows to support high-volume, low-latency operations across diverse care settings.

Competitive Landscape

The global RCM market is highly competitive and tiered, led by platform-focused giants such as Epic, Oracle Health, and Meditech, alongside specialists such as R1 RCM, Waystar, and Ensemble. Control over EHR integration, workflow depth, and compliance drives high switching costs and entrenched relationships. AI-first disruptors such as Akasa, FinThrive, and Tebra add automation-led pressure, keeping the market crowded. Competition centers on platform expansion, M&A, and embedding AI into core workflows.

Differentiation now depends on agentic AI, data access, and platformization, with leaders leveraging ecosystem control and challengers competing on speed, niche solutions, and flexible integration. The trend favors single-dashboard models, predictive denial management, and tighter payer-provider data alignment, putting sustained pressure on mid-tier vendors.

Key Industry Highlights:

- In September 2025, Waystar launched AI-powered denial prevention and reimbursement recovery solutions, reducing denials, boosting reimbursements, and improving provider financial outcomes. The innovations set a new standard for “Agentic AI” in the RCM lifecycle.

- In September 2025, CareCloud acquired HFMA’s MAP App, embedding AI-driven hospital benchmarking into revenue cycle workflows. The move enhanced operational insights, enabled real-time performance shifts, and strengthened health system efficiency.

- In May 2025, Infinx acquired i3 Verticals’ healthcare RCM business for $96 million, expanding customer segments, integrating proprietary technology, and accelerating tech-enabled service innovation in RCM.

Companies Covered in Revenue Cycle Management Market

- Oracle (Including Cerner Corporation)

- Optum, Inc.

- R1 RCM Inc.

- Athenahealth, Inc.

- Mckesson Corporation

- Experian Information Solutions

- Veradigm LLC

- Conifer Health Solutions, LLC

- Gebbs Healthcare Solutions

- Cognizant (Including Trizetto)

- Medical Information Technology, Inc.

- Waystar Health

- Change Healthcare

- The SSI Group, LLC

- Huron Consulting Group Inc.

Frequently Asked Questions

The global revenue cycle management market is projected to be valued at US$ 189 billion in 2026 and is expected to reach US$400 billion by 2033, driven by rising healthcare costs, regulatory complexity, and the need to optimize reimbursements.

AI-driven automation is essential to combat staffing shortages, minimize revenue leakage, and manage the increasing complexity of payer environments. It automates repetitive tasks such as claims processing and denial management, improving efficiency and cash flow stability for healthcare providers.

The revenue cycle management market is forecast to grow at a CAGR of 11.3% from 2026 to 2033, reflecting the accelerated adoption of advanced, AI-integrated financial platforms.

North America is the leading regional market, accounting for approximately 53% share, supported by complex reimbursement structures, high healthcare IT spending, early digital adoption, and stringent regulatory compliance requirements.

The revenue cycle management market is highly competitive and tiered, with key players including Oracle (Cerner), Optum, Inc., R1 RCM Inc., athenahealth, Inc., and Epic Systems. Competition centers on platform integration, AI capabilities, and the ability to offer end-to-end, automated revenue operations.