- Smart Packaging

- Edible Water Pods Market

Edible Water Pods Market Size, Share, and Growth Forecast, 2026 - 2033

Edible Water Pods Market by Ingredients (Alginate-based, Plant-based, Others), Flavors & Infusions (Plain Water, Flavored Water, Others), Distribution Channels, and Regional Analysis for 2026 - 2033

Edible Water Pods Market Size and Trends Analysis

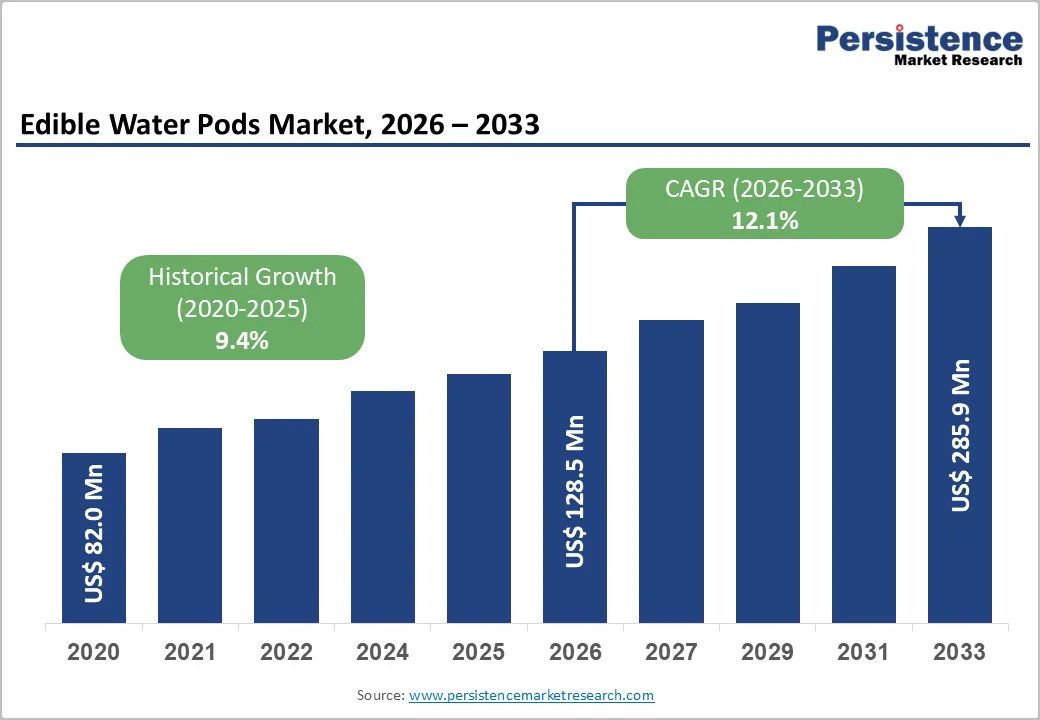

The global edible water pods market size is likely to be valued at US$128.5 million in 2026 and is expected to reach US$285.9 million by 2033, growing at a CAGR of approximately 12.1% between 2026 and 2033, driven by broader consumer acceptance and scaling adoption across events, sports venues, and foodservice environments.

Early demand remains concentrated in controlled-use channels where sustainability objectives outweigh price sensitivity. Over the forecast period, gradual expansion into retail and e-commerce, particularly through flavored and functional hydration formats, is expected to support faster revenue growth and improved margin structures.

Key Industry Highlights

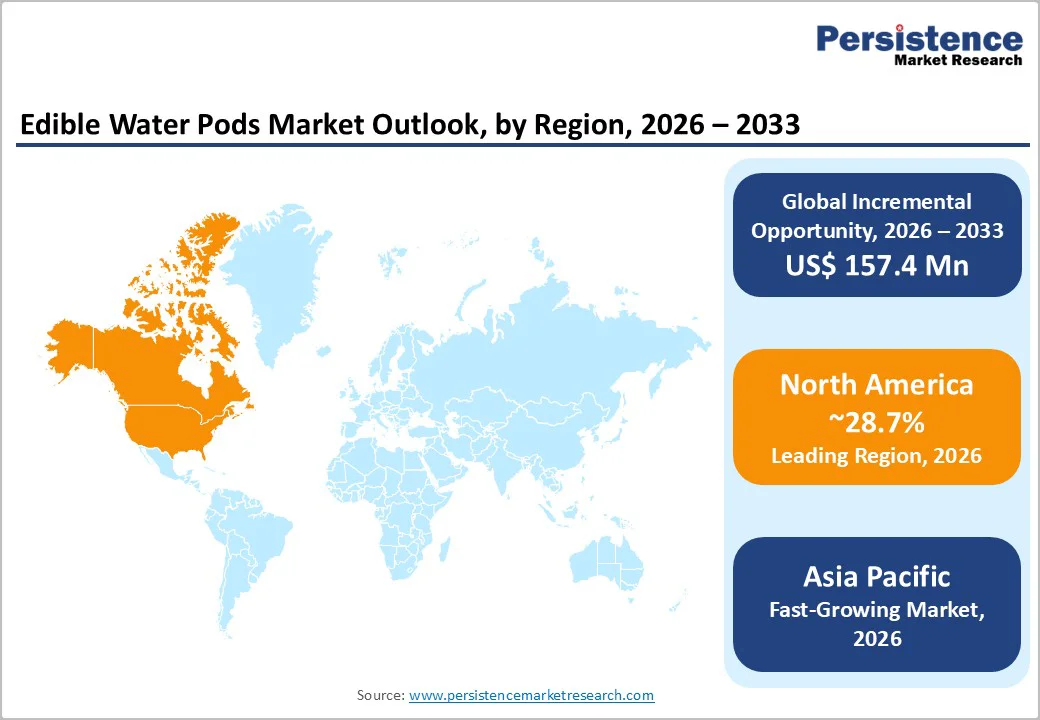

- Leading Region: North America is projected to account for 28.7% of the market share, supported by early adoption, large-scale event deployments, and strong institutional demand driven by sustainability mandates.

- Fastest-growing Region: Asia Pacific, estimated to register the highest growth rate through 2033, driven by abundant seaweed resources, expanding manufacturing capacity, and government-led plastic reduction initiatives across Southeast and East Asia.

- Investment Plans: Ongoing investments are concentrated in manufacturing scale-up, seaweed-based material innovation, and automated encapsulation technologies, with a growing share of capital directed toward Asia Pacific production hubs and North American commercialization partnerships.

- Dominant Ingredients: Alginate-based ingredients are anticipated to hold approximately 56.4% revenue share, due to proven performance, regulatory acceptance, and suitability for high-volume event and foodservice applications.

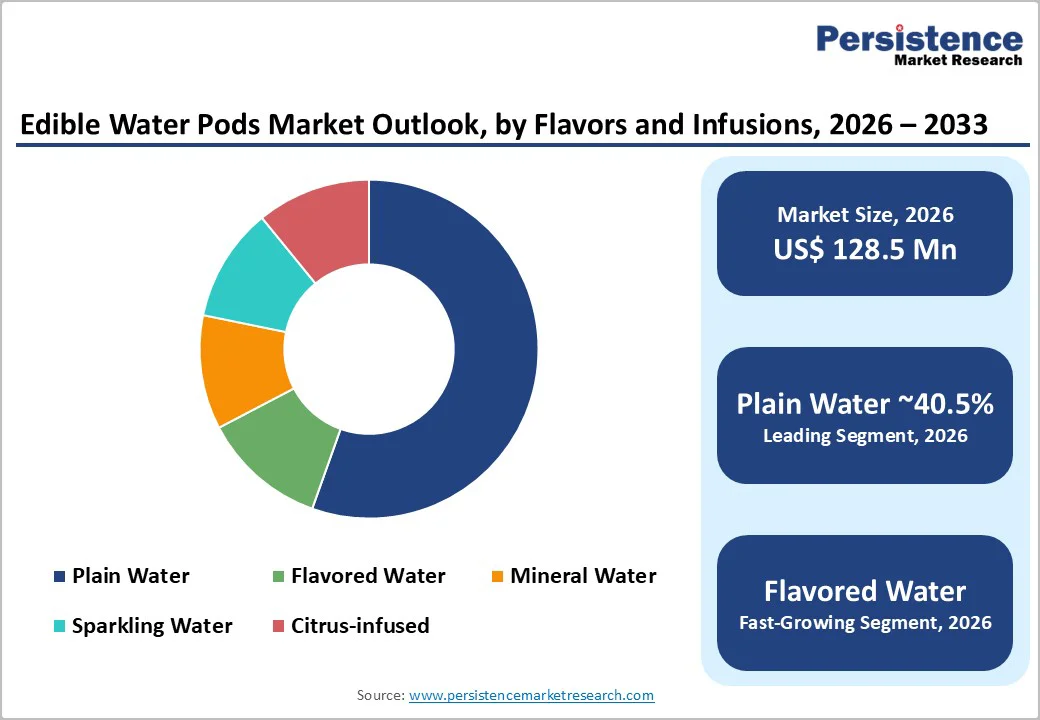

- Leading Flavors and Infusions: Plain water pods are estimated to account for around 38.7% of the total demand, driven by their role in early-stage pilots, simplified regulatory compliance, and widespread use in institutional and public sustainability programs.

| Key Insights | Details |

|---|---|

| Edible Water Pods Market Size (2026E) | US$128.5 Mn |

| Market Value Forecast (2033F) | US$285.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 12.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability Policy and Corporate ESG Procurement

Heightened regulatory focus on reducing single-use plastic waste, combined with corporate environmental, social, and governance commitments, is a central growth driver for edible water pods. Governments and public authorities increasingly restrict disposable plastic usage at events, public venues, and foodservice locations. At the same time, multinational corporations and event organizers are embedding zero-waste and net-zero targets into procurement frameworks.

Edible and biodegradable hydration formats align directly with these mandates, resulting in pilot programs and long-term supply agreements. These initiatives accelerate production volumes while sustaining pricing discipline, as institutional buyers are willing to accept modest cost premiums in exchange for reduced environmental impact and improved compliance outcomes.

Ingredient Availability and Manufacturing Scale Economies

The maturation of alginate and seaweed-derived ingredient supply chains has significantly improved the commercial feasibility of edible water pods. Food-grade hydrocolloids are now available at consistent quality and scale, enabling standardized manufacturing processes. In parallel, investments in continuous forming and filling equipment have increased production efficiency and reduced per-unit costs.

As production throughput improves, fixed costs are distributed over higher volumes, lowering the cost barrier for broader market participation. These efficiencies also enable product diversification, including flavored, mineral, and fortified variants, which support higher margins and expand use cases beyond limited-event applications.

Experiential Consumption and Health-Conscious Consumer Behavior

Changing consumer behavior, particularly among younger demographics, is reinforcing demand for edible water pods. Experience-driven consumption favors novel, tactile, and visually distinctive formats that encourage trial and social sharing. Edible pods provide a unique hydration experience that performs well in high-visibility environments such as festivals and sports events.

The growing preference for clean-label, plant-based, and additive-free products also supports the adoption of seaweed- and alginate-based membranes. As flavored and functional options gain traction, usage shifts from one-time novelty toward repeat consumption, increasing lifetime customer value and improving overall market sustainability.

Barrier Analysis - Unit Economics and Retail Price Sensitivity

Despite ongoing cost reductions, edible water pods remain more expensive per serving than conventional bottled water. This price differential limits penetration in mass retail and highly price-sensitive markets. While institutional buyers and premium venues can absorb higher costs, mainstream grocery channels require either further cost compression or clear functional differentiation to justify pricing.

If average selling prices remain close to US$1.0 per pod while bottled water equivalents remain significantly lower, adoption will remain constrained in value-driven segments without subsidies, sponsorship models, or added nutritional benefits.

Food Safety, Shelf Life, and Regulatory Complexity

Edible water pods are classified as food products, subjecting them to stringent food safety, hygiene, and labeling requirements. Shelf-life management, microbial stability, and allergen disclosure add complexity to manufacturing and distribution. In some jurisdictions, edible membranes may fall under novel food regulations, requiring additional approvals.

These regulatory processes increase compliance costs and lengthen commercialization timelines. As a result, many producers initially restrict deployments to controlled environments such as events and closed foodservice systems, delaying broader retail expansion.

Opportunity Analysis - Functional and Fortified Hydration Applications

Functional edible pods enriched with electrolytes, vitamins, or performance nutrients represent a high-margin growth opportunity. Sports events, fitness centers, and endurance activities increasingly demand convenient, sustainable hydration solutions. By 2033, functional formats could account for a meaningful share of total unit volumes, significantly improving average selling prices.

Strategic collaborations with sports nutrition brands and wellness companies can accelerate adoption while positioning edible pods as a recurring consumption product rather than a novelty item.

Foodservice, QSR, and Takeaway Integration

Beyond water, edible membranes can encapsulate sauces, condiments, and liquid ingredients for quick-service restaurants and delivery platforms. Replacing traditional sachets with edible alternatives multiplies addressable volume and improves factory utilization.

Even partial substitution within foodservice packaging volumes would materially increase demand while reducing unit costs through scale. These applications also align with foodservice operators’ sustainability commitments, strengthening the commercial case for long-term adoption.

Emerging Markets and Local Seaweed Value Chains

Emerging economies in Asia and parts of Latin America offer long-term growth potential due to high plastic waste generation and abundant seaweed resources. Local sourcing of seaweed reduces raw material costs and logistics dependencies while supporting regenerative aquaculture models.

Redirecting a small fraction of bottled water consumption toward edible pods in large population markets represents a substantial volume opportunity. Public funding for sustainable materials and coastal economic development further enhances market attractiveness.

Category-wise Analysis

Ingredients Insights

Alginate-based membranes are anticipated to account for the largest share of 56.4%, supported by their functional reliability, regulatory acceptance, and scalability in commercial production. Extracted primarily from brown seaweed, alginate forms a semi-permeable, elastic membrane when combined with calcium ions, enabling effective liquid encapsulation without compromising food safety. This chemistry has been widely adopted in food processing and pharmaceutical applications, which has accelerated regulatory familiarity and reduced approval complexity for edible pod use.

From a commercialization perspective, alginate-based systems offer predictable mechanical strength and controlled dissolution, making them suitable for high-volume applications such as marathons, music festivals, and corporate sustainability events. Several large-scale deployments at sporting events have demonstrated alginate pods’ ability to withstand handling while delivering consistent sensory performance. Established global seaweed supply chains and standardized processing parameters further support cost efficiency and supply continuity, reinforcing alginate’s leadership position in near-term market deployments.

Plant-based and seaweed-derived membranes are likely to be the fastest-growing ingredient segment, driven by increasing demand for fully vegan, biodegradable, and low-impact materials. These formulations often use minimally processed seaweed extracts or blended plant polymers to enhance compostability and reduce reliance on refined hydrocolloids. Their alignment with regenerative marine sourcing and circular economy principles has made them particularly attractive to sustainability-focused brands and municipalities.

Ongoing material innovation is addressing earlier limitations related to texture variability, moisture sensitivity, and shelf stability. Recent pilot programs have demonstrated improved durability and sensory neutrality, enabling usage beyond controlled event environments. For example, seaweed-based edible packaging has been trialed for single-serve hydration and condiment applications in select foodservice and hospitality settings. As processing techniques mature and costs decline, these formulations are expected to gain share at the expense of conventional membranes, particularly in regions with strong plant-based consumption trends.

Flavors and Infusions Insights

Plain water is expected to be the leading flavor segment, estimated to hold 38.7% of the market share, reflecting its role as the default format for early commercialization and institutional pilots. Its neutral composition simplifies formulation, eliminates allergen concerns, and supports longer shelf stability compared to flavored variants. These characteristics have made plain water pods the preferred choice for first-time deployments in sports events, conferences, and educational demonstrations focused on plastic reduction.

Plain water pods reduce complexity across manufacturing, storage, and distribution, lowering execution risk for new market entrants. Many large-scale public trials, including endurance races and city-sponsored sustainability initiatives, have relied on unflavored pods to validate logistics, consumer acceptance, and waste-reduction impact. As a result, plain water continues to anchor baseline demand while serving as a platform for gradual product line expansion.

Flavored edible water pods are emerging as the fastest-growing sub-segment, supported by improving formulation stability and rising consumer expectations for taste and functional benefits. Citrus, berry, and lightly infused botanical flavors have gained traction, particularly in controlled environments such as fitness events, experiential marketing activations, and premium hospitality venues.

Flavoring enhances palatability and encourages repeat consumption, shifting edible pods from novelty items toward habitual hydration solutions. Manufacturers are also exploring functional flavor variants, incorporating electrolytes or natural extracts to support sports hydration and wellness positioning. These developments enable premium pricing and open collaboration opportunities with beverage and nutrition brands. As encapsulation techniques improve and shelf-life constraints are addressed, flavored pods are expected to expand into direct-to-consumer and e-commerce channels, contributing disproportionately to revenue growth despite lower unit volumes than plain water.

Regional Insights

North America Edible Water Pods Market Trends - Event-Led Commercialization and Brand-Driven Scale-Up

North America is projected to represent the largest regional market for edible water pods, accounting for approximately 28.7% of global demand, supported by early commercialization, strong sustainability mandates, and an active innovation ecosystem. The U.S. leads the region due to the concentration of large-scale public events, sports leagues, and festivals that actively pilot plastic-free hydration alternatives. These controlled environments have allowed edible water pods to demonstrate operational feasibility at scale while meeting visibility-driven sustainability goals.

Several U.S.-based innovators have contributed to market development through product trials and brand partnerships. Companies such as Loliware have expanded edible packaging applications beyond water to include beverage and foodservice use cases, reinforcing confidence among institutional buyers. Edible water pods have been deployed at endurance races and corporate sustainability events, where waste reduction metrics are closely tracked and reported. These deployments have helped normalize edible hydration formats among both organizers and consumers.

North America also benefits from clearly defined food safety frameworks, which, while stringent, provide predictability once compliance is achieved. This clarity has encouraged venture capital and strategic investors to fund manufacturing scale-up, ingredient refinement, and automation. Recent investment activity has focused on increasing production throughput and improving shelf stability, positioning the region as a commercialization and branding hub rather than a low-cost manufacturing center.

Europe Edible Water Pods Market Trends - Policy-Driven Adoption and Public-Sector Innovation

Europe is a strategically significant market, driven by aggressive plastic reduction policies, coordinated regulatory mechanisms, and strong public-sector involvement in sustainable materials innovation. The region’s momentum is closely tied to legislative measures restricting single-use plastics at events, foodservice outlets, and public venues, creating a favorable environment for edible alternatives.

The U.K. has emerged as a focal point for innovation and market visibility. Companies such as Notpla have gained international recognition through high-profile deployments of edible water pods and seaweed-based packaging at major sporting events and public gatherings. These initiatives have demonstrated scalability while reinforcing the commercial viability of seaweed-derived materials. The U.K.’s supportive innovation funding environment has further accelerated product development and pilot expansion.

Germany and France contribute manufacturing expertise, food processing infrastructure, and strong hospitality-driven demand, while Spain plays a growing role in seaweed sourcing and coastal biomass utilization. Public funding programs across the region support research into biodegradable materials and circular economy solutions. The pace of retail-scale deployment varies, as novel food approval requirements in certain countries extend commercialization timelines. As a result, Europe’s growth remains the strongest in institutional and event-based channels rather than mass retail.

Asia Pacific Edible Water Pods Market Trends - Seaweed-Based Production Scale and Rapid Cost Optimization

Asia Pacific is the fastest-growing regional market for edible water pods, underpinned by abundant seaweed resources, large population centers, and increasing regulatory pressure to address plastic waste. Countries across East and Southeast Asia combine raw material availability with manufacturing scale, enabling lower production costs and faster capacity expansion compared to Western markets.

Indonesia has gained prominence through companies such as Evoware, which leverage locally sourced seaweed to produce edible and biodegradable packaging solutions. These initiatives not only address domestic plastic pollution challenges but also position the region as a global supply base for seaweed-derived materials. Similar activity is emerging in coastal economies across Southeast Asia, where sustainable aquaculture is increasingly supported by government and development programs.

In Japan and South Korea, innovation focuses on material performance, food safety, and premium applications, often aligned with convenience retail and vending formats. China, meanwhile, offers manufacturing depth and logistics infrastructure, supporting scale-driven cost optimization. Government-led plastic reduction campaigns and bans on certain disposable products further reinforce demand. While regulatory frameworks differ widely across the region, partnerships with local manufacturers and distributors significantly reduce entry barriers, making Asia Pacific both a high-growth consumption market and a critical production hub.

Competitive Landscape

The global edible water pods market is emerging and moderately fragmented. A small number of technology-driven innovators control core intellectual property and early commercial relationships, while numerous smaller players and ingredient suppliers support niche applications. Market concentration remains low, but consolidation is beginning as companies seek scale, distribution access, and manufacturing efficiency.

Market leaders prioritize product innovation, manufacturing efficiency, and strategic partnerships. Differentiation is achieved through sustainable sourcing, proprietary membrane technologies, and B2B-focused commercialization models that emphasize volume stability and margin protection.

Key Industry Developments

- In July 2025, Loliware partnered with Entec Polymers to expand global distribution of its SEA Technology® seaweed-based bioresins, enabling broader adoption of edible and compostable materials across North America and Europe.

- In June 2025, Nestlé initiated trials of edible water pods at selected Europe-based sports and event venues, collaborating with an edible packaging specialist to explore sustainable alternatives for beverage packaging.

Companies Covered in Edible Water Pods Market

- Notpla

- Loliware

- DisSolves

- Evoware

- MarinaTex

- Skipping Rocks Lab

- TOMRA (edible packaging R&D initiatives)

- WikiFoods

- Jelly Drops

- Stora Enso (biomaterials initiatives)

- Ingredion

- CP Kelco

- Cargill

- DuPont Nutrition & Biosciences

- FMC BioPolymer

- AquaBrew (edible packaging concepts)

- Sway Innovation

- TIPA (edible and compostable packaging solutions)

Frequently Asked Questions

The global edible water pods market is estimated to be valued at US$128.5 million in 2026.

By 2033, the edible water pods market is projected to reach US$285.9 million.

Key trends include the shift toward plastic-free hydration solutions, increased use of seaweed- and alginate-based membranes, growing interest in flavored and functional pods, and expanding deployment in sports events, festivals, and foodservice operations.

The alginate-based ingredient segment is the leading category, accounting for approximately 56.4% of total revenue, due to its scalability, food safety profile, and proven performance in commercial applications.

The edible water pods market is expected to grow at a CAGR of 12.1% between 2026 and 2033.

Major companies include Notpla, Loliware, DisSolves, Evoware, and MarinaTex.