- Food Packaging

- Foodservice Packaging Market

Foodservice Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Foodservice Packaging Market by Material Type (Plastic, Paper & Paperboard, Aluminum, Biodegradable/Compostable Materials), Product Type (Containers & Clamshells, Cups & Beverage Packaging, Trays & Boxes, Plates & Bowls, Flexible Packaging, Miscellaneous), End-user (Quick Service Restaurants [QSRs], Full-Service Restaurants [FSRs], Cafés & Coffee Chains, Institutional Foodservice, Online Food Delivery/Cloud Kitchens), and Regional Analysis, 2026 - 2033

Foodservice Packaging Market Size and Trend Analysis

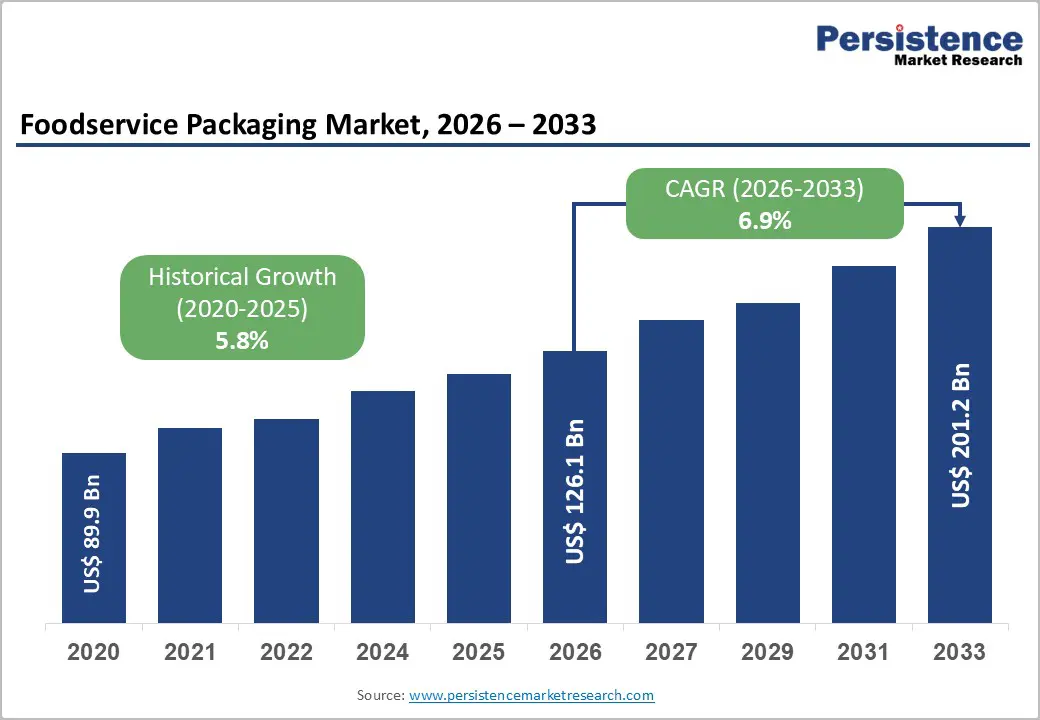

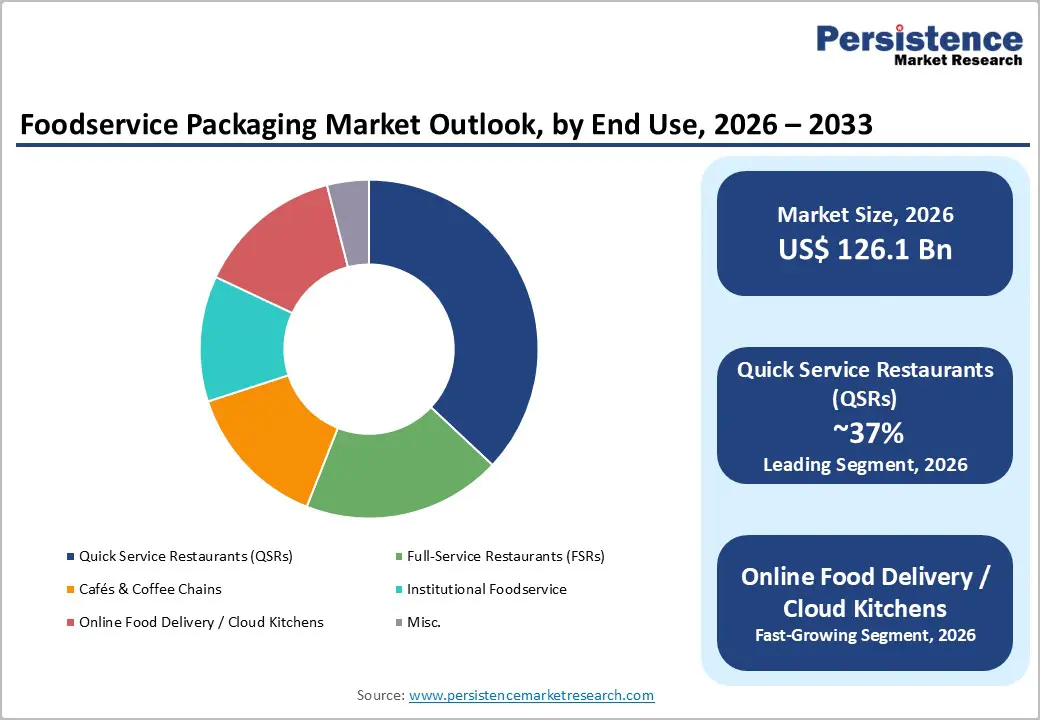

The global foodservice packaging market size is expected to be valued at US$ 126.1 billion in 2026 and projected to reach US$ 201.2 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033. The rapid proliferation of online food delivery platforms and mandated regulatory transitions to single-use plastics underpin foodservice packaging demand dynamics.

The post-pandemic normalisation of food delivery infrastructure with platforms such as Uber Eats, DoorDash, and Zomato, institutionalising delivery-first consumption in urban markets across North America, Europe, and the Asia Pacific, has made tamper-evident, thermally efficient, and sustainable packaging a non-negotiable operational requirement. Simultaneously, tightening EU Single-Use Plastics Directive enforcement and equivalent mandates across the Asia Pacific are compelling the fastest technology transition in the sector's history, channelling investment into fibre-based, biodegradable, and compostable material innovations.

Key Industry Highlights:

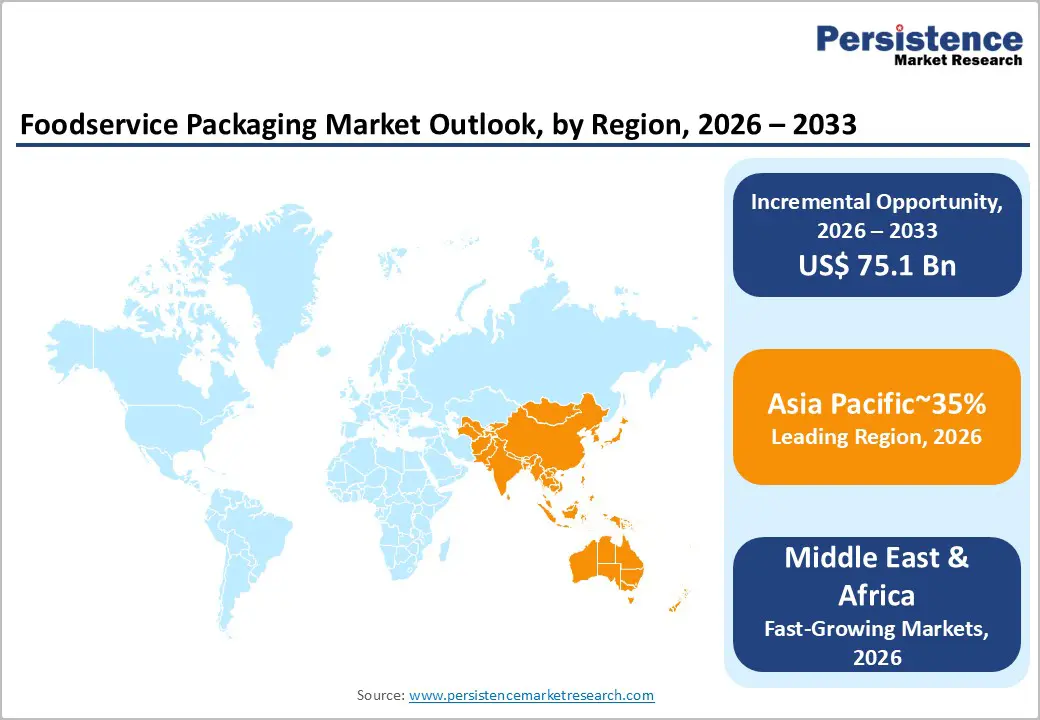

- Asia Pacific leads the global foodservice packaging market as the fast-growing market with approximately 35% revenue share in 2025 and a projected CAGR exceeding 8% through 2033, propelled by China's plastic restriction mandate, India's expanding QSR networks, and delivery platform proliferation.

- North America holds approximately 27% of global revenue in 2025, anchored by the U.S. market valued at US$ 28 billion, driven by the world's highest QSR density, surging food delivery adoption, and an accelerating state-level regulatory transition away from polystyrene and single-use plastic packaging formats.

- Plastic dominates the Material Type segment with approximately 49% market share in 2025, reflecting its unmatched cost, barrier, and design performance across QSR and delivery packaging formats, though regulatory pressure and material innovation are systematically shifting procurement toward fibre-based and compostable alternatives.

- Biodegradable/compostable materials represents the fast-growing material segment at a projected CAGR of 7% through 2033, driven by EU SUPD enforcement, China's Phase II plastic restrictions, India's single-use plastic ban, and brand-level ESG commitments compelling procurement substitution across all major foodservice end-use categories.

DRO Analysis

Drivers - Online Food Delivery and Cloud Kitchen Proliferation Driving Packaging Demand

The transformation of global food consumption toward delivery-first models has created a durable and high-volume demand channel for foodservice packaging. According to the research, the food delivery market generated revenues exceeding US$ 1.2 trillion in 2024, with penetration still deepening across Southeast Asia, India, and Latin America. Cloud kitchens, which operate without front-of-house infrastructure, are entirely dependent on packaging quality and integrity for brand differentiation and customer satisfaction. This model directly amplifies per-order packaging consumption while placing premiums on heat retention, tamper evidence, and moisture barriers.

India's food processing sector, valued at US$ 354.5 billion in 2024 and projected at US$ 535 billion by FY26, exemplifies the macro backdrop driving foodservice packaging adoption, with rapid urbanisation and organised QSR network expansion compelling packaging procurement at scale across both branded chains and independent operators.

Mandatory Regulatory Transitions Away from Conventional Single-Use Plastics

Binding regulatory frameworks enacted across major economies are compelling a permanent structural shift in foodservice packaging material procurement toward fibre-based, compostable, and recyclable alternatives. The EU Single-Use Plastics Directive (SUPD) banned a defined list of single-use plastic food and beverage packaging items from July 2021, with extended producer responsibility (EPR) obligations for remaining plastic formats.

EU plastic packaging waste reached 16.16 million tonnes in 2022 (per Eurostat), with only 40.7% recycled, a statistic that continues to drive legislative tightening and brand-level voluntary commitments. In the United States, over 12 state-level bans on polystyrene and single-use plastic food containers are operational, while China's Phase II plastic restriction policy mandated the elimination of non-degradable disposable tableware from the restaurant sector by 2025. These interlocking mandates are generating simultaneous replacement demand across every major foodservice packaging format.

Restraints - Cost Premium of Sustainable Packaging Alternatives Over Conventional Plastics

Despite regulatory momentum, the cost differential between conventional plastic packaging and certified compostable or fibre-based alternatives remains a significant adoption barrier for price-sensitive foodservice operators. Moulded fibre containers can cost 2–4 times more than equivalent polystyrene formats, while certified home-compostable films command premiums exceeding 50% over standard polyethylene equivalents.

For QSRs and independent food operators in developing markets operating on thin EBITDA margins, typically 5%–10%, this cost gap directly impacts procurement decisions. The EU's accommodation and food services sector, which employed 10.9 million people in 2022, with among the lowest average personnel costs across EU sectors, illustrates the structural cost sensitivity of the end-user base, constraining the pace of sustainable packaging transition beyond regulatory mandates.

Infrastructure Gaps in Compostable and Recycled Packaging End-of-Life Processing

The functional value of compostable and recycled-content foodservice packaging is substantially undermined by inadequate waste collection, sorting, and processing infrastructure in most markets. Even where regulations mandate the use of compostable packaging, industrial composting facilities capable of processing PLA and other certified compostable materials are absent or inaccessible in the majority of municipalities globally.

In the EU, significant volumes of plastic packaging waste are still exported due to insufficient domestic recycling capacity, and wide disparities exist between member states, with Slovakia and Belgium recycling far more than Malta and France (per Eurostat). This infrastructure gap means that a substantial proportion of technically compostable or recyclable foodservice packaging is either landfilled or incinerated, eroding the environmental credentials that justify premium pricing and complicating brand sustainability claims.

Opportunities - High-Barrier Fibre and Moulded Pulp Packaging Solutions for Sustainable Transition

The confluence of regulatory mandates and brand sustainability commitments is generating significant commercial opportunity for manufacturers offering high-performance, fibre-based packaging solutions that match or exceed the functional properties of plastic formats. Mondi's launch of FunctionalBarrier Paper Ultimate in August 2025, a recyclable high-barrier paper packaging solution for coffee, tea, and snacks offering oxygen, moisture, and grease resistance, exemplifies the technical frontier being commercialised.

Amcor's partnership with Metsä Group, announced in May 2025 to develop moulded fibre-based packaging incorporating high-barrier film liner and Muoto™ molded fiber technology, demonstrates how established players are investing in next-generation material platforms. As the EU's packaging and packaging waste regulation mandates minimum recycled content thresholds and recyclability requirements for all packaging formats by 2030, vendors capable of delivering certified recyclable or compostable formats at competitive price points will capture structural replacement demand across every major foodservice segment.

Rapid QSR and Café Chain Network Expansion Across Asia Pacific Emerging Markets

The accelerating penetration of organised quick service restaurant chains and branded café networks across Tier-2 and Tier-3 cities in China, India, Vietnam, Indonesia, and the Philippines represents a structurally high-growth procurement channel for standardised foodservice packaging. McDonald's, KFC (Yum! Brands), Starbucks, and domestic chains are collectively executing thousands of new unit openings annually in the Asia Pacific, each requiring consistent, branded, and compliant packaging supply chains.

India's government-backed food sector investment, including 41 Mega Food Parks, US$ 13.4 billion in cumulative FDI between 2000 and June 2025, and PLI allocations exceeding Rs. 1,400 crore, is creating food processing infrastructure that directly supports organised foodservice ecosystem development and packaging demand. Packaging vendors offering integrated supply chain solutions, local manufacturing presence, and format customisation capabilities are positioned to benefit from this wave of QSR network formalization across the region's high-growth markets.

Category-wise Insights

Material Type Analysis

The Plastic segment dominates the global Foodservice Packaging market by material type, holding approximately 49% of the total market share in 2025. This leadership reflects plastic's unmatched combination of barrier performance, light weight, design flexibility, and low unit cost that has made it the default material across every major foodservice format from QSR beverage cups and clamshell containers to flexible delivery packaging. Polyethylene (PE), polypropylene (PP), and expanded polystyrene (EPS) collectively underpin the segment's volume dominance, with food safety certification requirements and supply chain infrastructure deeply embedded around these materials.

In the U.S., where food and beverage manufacturing accounted for 16.8% of total manufacturing sales in 2021, plastic remains the dominant procurement choice for scale QSR operators due to its thermal properties and cost-efficiency. However, the Biodegradable/Compostable Materials segment is the fastest growing at a CAGR of 7% through 2033, driven by SUPD compliance, brand ESG commitments, and material technology advancement.

Product Type Analysis

The Containers & Clamshells segment leads the market by product type, accounting for approximately 32% of global revenue share in 2025. This dominance is directly attributable to the explosive growth of online food delivery and takeaway culture, where rigid containers and clamshell formats serve as the primary packaging vessel for hot meals, salads, grain bowls, and prepared foods across QSR, FSR, and cloud kitchen segments. The segment's market leadership is reinforced by the operational requirements of delivery platforms, which demand packaging that maintains food temperature integrity over delivery windows of 20–45 minutes while preventing leakage and preserving presentation.

The Cups & Beverage Packaging sub-segment ranks second, driven by the global proliferation of café chains and speciality coffee outlets, with Starbucks alone operating over 38,000 locations globally requiring a consistent cup supply. Flexible Packaging is the fastest-growing product type, driven by the snack and side-item delivery segment.

End-user Analysis

The Quick Service Restaurant (QSR) segment is the dominant end-use category in the global Foodservice Packaging market, commanding approximately 38% of total market share in 2025. QSRs represent the highest-volume, most standardised, and most procurement-intensive segment within foodservice, with global chains requiring massive, consistent packaging supply across thousands of outlets. McDonald's serves approximately 70 million customers daily across more than 40,000 restaurants globally, generating packaging requirements across cups, bags, containers, wrappers, and trays at an industrial scale that few packaging suppliers can match.

The Online Food Delivery / Cloud Kitchens segment is the fastest-growing end-use, as the structural shift toward delivery-first food consumption catalyzed by the pandemic and sustained by platform ecosystem investment, requires purpose-built packaging optimised for the rigours of transit. According to the EU's accommodation and food services data, over 2.0 million enterprises in the food and beverage services segment demonstrate the sector's scale and packaging consumption depth.

Regional Insights

North America Foodservice Packaging Market Trends and Insights

North America holds approximately 27% of the global Foodservice Packaging market revenue in 2025, underpinned by one of the world's most developed QSR ecosystems, high per-capita foodservice spending, and a regulatory environment transitioning rapidly away from single-use plastics at both state and federal levels. The region's market is characterised by large-format chain operators driving standardized, high-volume packaging procurement, while simultaneously facing mandatory compliance with an expanding patchwork of state-level single-use plastics bans and EPR legislation that is reshaping material sourcing toward fibre-based and compostable alternatives.

U.S. Foodservice Packaging Market Size

The U.S. Foodservice Packaging market is valued at approximately US$ 28 billion in 2025, reflecting the structural scale of a market served by over 1 million foodservice establishments and anchored by the world's highest QSR outlet density. U.S. food and beverage manufacturing, which employed approximately 1.7 million workers and accounted for 16.8% of total manufacturing sales in 2021, provides an institutional foundation for domestic packaging supply chains. The USDA's sustained investment in food processing infrastructure, combined with state-level bans on polystyrene food containers across California, New York, Maryland, and 12 additional states, is simultaneously maintaining volume demand while accelerating the transition to recyclable and compostable packaging formats that command higher average selling prices.

Europe Foodservice Packaging Market Trends and Insights

Europe accounts for approximately 23.0% of the global Foodservice Packaging market revenue in 2025, shaped by the most comprehensive single-use plastics regulatory framework globally under the EU Single-Use Plastics Directive and the forthcoming Packaging and Packaging Waste Regulation (PPWR). The region's accommodation and food services sector, comprising nearly 2.0 million enterprises and employing 10.9 million people as of 2022, provides the primary demand base, with Germany, the U.K., and France anchoring procurement volumes. The shift toward compostable and paper-based alternatives is structurally more advanced in Europe than in any other region, driven by both regulatory compulsion and consumer environmental awareness.

Germany Foodservice Packaging Market Size

Germany's Foodservice Packaging market is valued at approximately US$ 5.7 billion in 2025, driven by the country's stringent packaging waste legislation, including the Verpackungsgesetz (Packaging Act) mandating participation in dual collection systems and its highly organised foodservice industry spanning premium QSR chains, hospital and institutional catering, and a dense café culture. Germany is among the EU's highest plastic packaging recyclers (per Eurostat), yet ongoing legislative tightening under the PPWR is compelling foodservice operators to transition to reusable and recyclable formats, stimulating demand for high-performance fibre, molded pulp, and certified compostable packaging.

U.K. Foodservice Packaging Market Size

The U.K. Foodservice Packaging market is valued at approximately US$ 4.9 billion in 2025, sustained by London's position as Europe's most active food delivery market and the country's dense branded café and QSR network. The UK Plastics Pact, a commitment by leading brands and retailers to make 100% of plastic packaging reusable, recyclable, or compostable by 2025, has driven substantial packaging reformulation investment across major food operators, including McDonald's UK, Greggs, and Pret a Manger, creating premium demand for compliant fibre-based and compostable packaging solutions certified to EN 13432 standards.

Asia Pacific Foodservice Packaging Market Drivers and Analysis

Asia Pacific holds approximately 35% of the global Foodservice Packaging market revenue in 2025 and is the fastest-growing region, projected to expand at a CAGR exceeding 8% through 2033. China dominates the region's absolute revenue base, while India represents the most dynamic high-growth frontier, supported by rapidly expanding QSR networks, surging food delivery adoption, and government-backed food processing investment.

The region is simultaneously the largest consumer of disposable foodservice packaging globally and the epicentre of regulatory transition, with China's Phase II plastic restriction policies, India's ban on select single-use plastic items from July 2022, and similar mandates across Vietnam, Thailand, and Indonesia collectively compelling material substitution at a regional scale.

China Foodservice Packaging Market Size

China's Foodservice Packaging market is valued at approximately US$ 15.7 billion in 2025, reflecting the country's position as the world's largest foodservice market by outlet count and delivery volume. China's Phase II plastic restriction mandate, which required the elimination of non-degradable disposable tableware from the restaurant sector by the end of 2025, has triggered a structural replacement cycle across the entire foodservice packaging supply chain, shifting procurement toward PLA-based, starch-based, and paper-laminated alternatives at an industrial scale.

China's massive food delivery ecosystem, with platforms Meituan and Ele.me processing over 80 million daily orders at peak periods, generates the world's highest per-market consumption of delivery-specific packaging formats, including insulated bags, tamper-evident containers, and beverage carriers.

India Foodservice Packaging Market Size

India's Foodservice Packaging market is valued at approximately US$ 7.4 billion in 2025, underpinned by one of the world's fastest-expanding organised foodservice ecosystems and a food processing sector growing toward US$ 535 billion by FY26. The government's investment in 41 Mega Food Parks, cumulative food sector FDI of US$ 13.4 billion (2000–June 2025), and PLI scheme allocations exceeding Rs. 1,400 crore are catalysing the organised food supply chain that directly drives foodservice packaging demand.

India's ban on select single-use plastics from July 2022, covering plates, cups, cutlery, and straws, is compelling the country's 7 million+ food processing and foodservice establishments to transition procurement toward paper, bagasse, and compostable format alternatives at an unprecedented scale.

Competitive Landscape

The global Foodservice Packaging market exhibits a moderately consolidated structure at the tier-1 level, with global packaging conglomerates including Amcor plc, Sealed Air Corporation, Huhtamaki Oyj, Novatek International, Pactiv Evergreen, and Mondi Group commanding significant combined revenue share through broad product portfolios, global manufacturing footprints, and deep QSR chain supply relationships.

The market becomes substantially more fragmented in the sustainable and speciality packaging tiers, where regional and emerging material innovators are capturing disproportionate growth. Leading players are differentiating through certified compostable material platforms, high-barrier fibre technology, and integrated supply chain management services. A notable strategic trend is the shift toward material innovation partnerships, exemplified by Amcor's collaboration with Metsä Group rather than purely organic R&D, accelerating the commercialisation of next-generation sustainable formats. Private label and regional manufacturers maintain strong positions in price-sensitive developing markets.

Key Market Developments

- In May 2025, Amcor partnered with Metsä Group to develop moulded fibre-based packaging solutions for food applications, combining high-barrier film liner and lidding technology with wood-based Muoto™ molded fiber, enabling recyclable, sustainable packaging for perishable food products and extended shelf life.

- In December, 2025, Amcor Collaborated with industry partners under the CRISP initiative led by the Danish Technological Institute to advance circular recycling of polyethene (PE) and polypropylene (PP) food packaging. The project focuses on developing food-grade recycled packaging from post-consumer waste, supporting EU recyclability targets and strengthening the transition toward a circular economy in the foodservice packaging market through improved traceability and reuse of plastic materials.

Companies Covered in Foodservice Packaging Market

- Amcor

- Sealed Air

- Berry Global

- Smurfit Kappa

- Graphic Packaging Holding Company

- WestRock Company

- Huhtamaki

- Dart Container Corporation

- Anchor Packaging Inc.

- Pactiv LLC

- D&W Fine Pack

- New WinCup Holdings, Inc.

- Linpac Packaging Ltd

- Georgia-Pacific LLC

Frequently Asked Questions

The global Foodservice Packaging market is valued at US$ 126.1 billion in 2026, up from US$ 89.9 billion in 2020, reflecting a historical CAGR of 5.8%. The market is projected to reach US$ 201.2 billion by 2033 at a CAGR of 6.9%, driven by food delivery proliferation, QSR expansion, and regulatory transitions to sustainable packaging materials across all major geographies.

The two primary demand drivers are the structural proliferation of online food delivery platforms and cloud kitchens, which have institutionalised tamper-evident, thermally efficient packaging as a baseline operational requirement and binding regulatory mandates across the EU, China, India, and the U.S., compelling the replacement of conventional single-use plastic formats with certified fibre-based, biodegradable, and compostable packaging alternatives.

Asia Pacific leads the global Foodservice Packaging market with approximately 35% revenue share in 2025 and the highest projected regional CAGR through 2033. The region's leadership reflects China's massive food delivery ecosystem, India's expanding QSR networks and food processing investment of US$ 535 billion by FY26, and simultaneous regulatory transitions away from single-use plastics across multiple high-growth markets.

The most significant opportunity lies in high-barrier fibre, moulded pulp, and certified compostable packaging formats that meet both regulatory compliance and functional performance requirements. With the EU's PPWR mandating recyclability targets by 2030, China's Phase II plastics restrictions driving industrial-scale material replacement, and India's organised foodservice sector expanding toward US$ 535 billion, vendors offering certified sustainable formats at competitive price points are positioned for structurally durable demand capture.

The global Foodservice Packaging market is led by Amcor plc, Huhtamaki Oyj, Sealed Air Corporation, Mondi Group, and Pactiv Evergreen Inc.