- Retail

- U.S. Bottled Water Market

U.S. Bottled Water Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Bottled Water Market by Product Type (Spring Water, Purified Water, Mineral Water, Sparkling Water, Other), Packaging Type (PET Bottles, Cans, Other), Distribution Channel (Supermarket, Grocery Stores, Convenience Stores, Other), and Regional Analysis for 2026-2033

U.S. Bottled Water Market Size and Trend Analysis

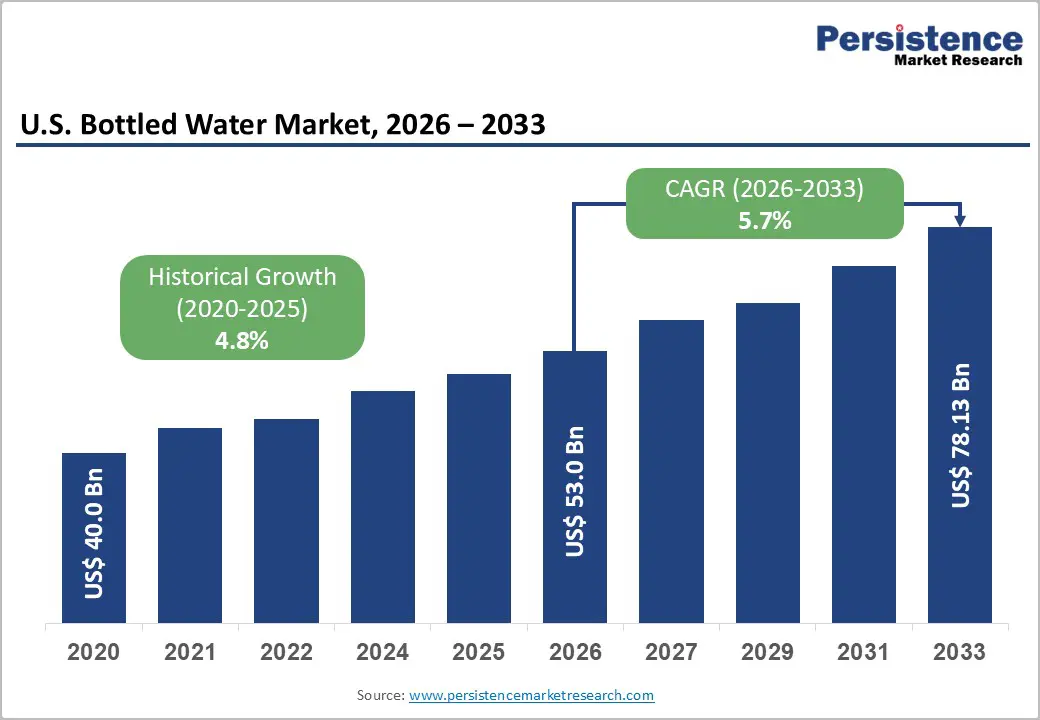

The U.S. Bottled Water Market is supposed to be valued at US$ 53.0 Bn in 2026 and is projected to reach US$ 78.1 Bn by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The market is being driven by a fundamental shift in consumer preferences toward health-conscious hydration alternatives, convenience-driven lifestyles, and heightened awareness of water quality concerns. According to the International Bottled Water Association (IBWA), Americans consumed 47.3 gallons of bottled water per capita in 2024, with bottled water maintaining its position as the number one beverage by volume for the ninth consecutive year. This growth is bolstered by consumers actively switching from sugary beverages, regulatory frameworks addressing water contamination in certain regions, and continuous innovation in product offerings such as functional and mineral-enhanced waters that deliver perceived health benefits beyond basic hydration.

Key Market Highlights

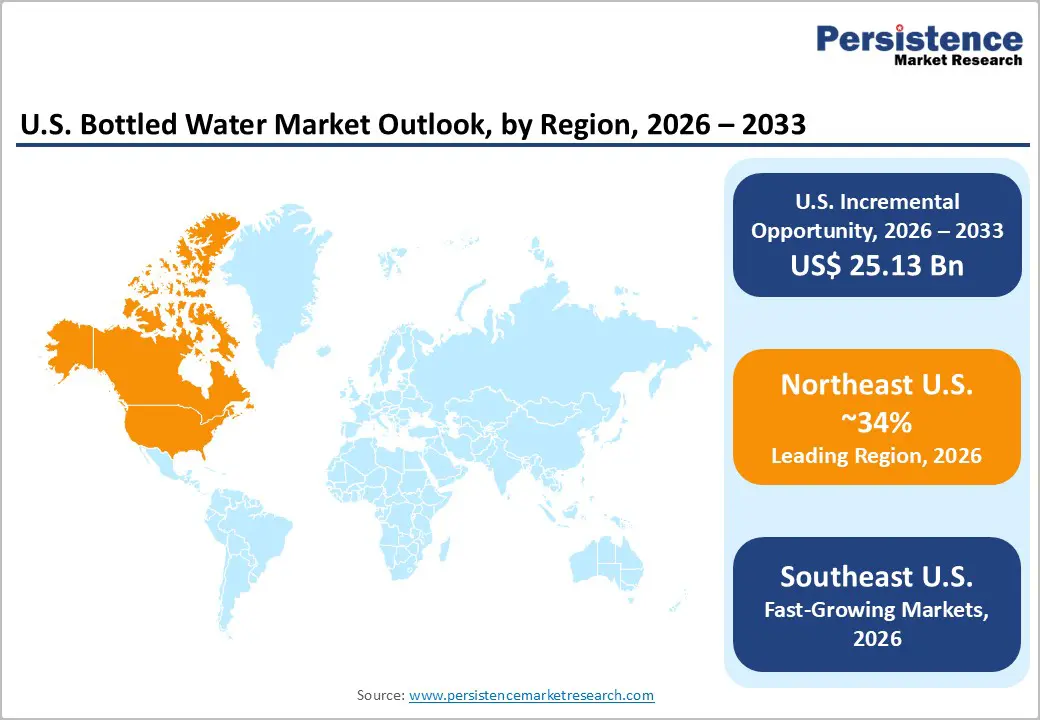

- Leading Region: The Northeast U.S. maintains a market leadership position, with 34% market share, driven by established consumption patterns, elevated health consciousness among affluent urban populations, and mature retail infrastructure supporting comprehensive brand availability and competitive pricing dynamics, ensuring sustained market dominance.

- Fastest Growing Region: The Southeast U.S. is experiencing accelerated growth rates driven by rapid urbanization and population expansion into Sunbelt metropolitan areas, creating substantial demand increments among relocating populations establishing new consumption patterns in communities with emerging infrastructure development.

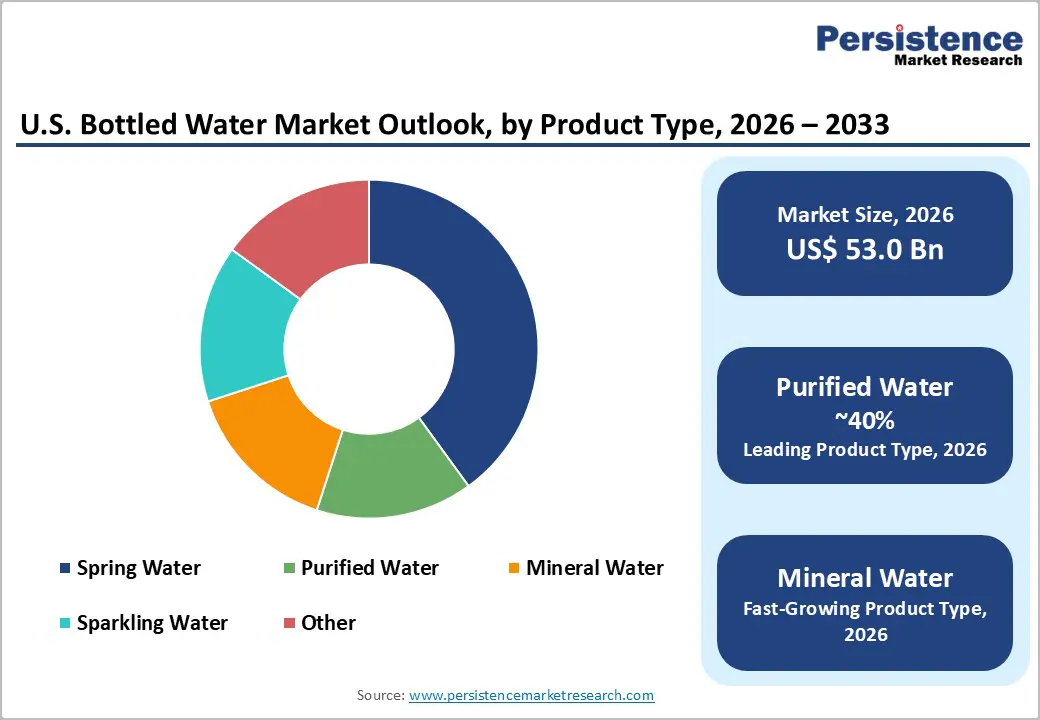

- Dominant Segment: Purified Water maintains category leadership with 40% market share, reflecting consumer preference for perceived superior purity, advanced filtration eliminating contaminants, and established brand recognition among mainstream demographics prioritizing water cleanliness.

- Fastest Growing Segment: Mineral Water products enriched with vitamins, minerals, and bioactive compounds are expanding at 8.12% CAGR, significantly outpacing traditional still water growth and capturing premium-conscious consumers seeking personalized health benefits and differentiated product experiences.

- Key Market Opportunity: Sustainable Packaging Innovation, particularly aluminum cans expanding at 7.0% CAGR, represents a substantial opportunity for companies positioning environmental responsibility as a primary brand differentiator, enabling premium pricing and access to affluent eco-conscious consumer demographics.

| Key Insights | Details |

|---|---|

| U.S. Bottled Water Market Size (2026E) | US$ 53.0 Bn |

| Market Value Forecast (2033F) | US$ 78.1 Bn |

| Projected Growth CAGR (2026-2033) | 5.7% |

| Historical Market Growth (2020-2025) | 4.8% |

Market Dynamics

Market Growth Drivers

Health and Wellness Consciousness Among Consumers

The rapid rise of health and wellness priorities has become a key driver of sustained growth in the bottled water market. Consumers increasingly view bottled water as a calorie-free and sugar-free substitute for carbonated soft drinks and other sweetened beverages. Data from the Beverage Marketing Corporation indicates that 34% of bottled water sales growth over the past eleven years resulted from consumers shifting away from soft drinks and fruit beverages, highlighting the influence of health-driven purchasing behavior. This trend is especially prominent among younger consumers who associate bottled water with their wellness goals and seek functional hydration options.

The perceived purity and absence of artificial additives position bottled water as a trusted choice, with health-conscious consumers viewing filtered and mineral-enriched variants as cleaner alternatives to municipal tap water. As lifestyle diseases including obesity and diabetes continue escalating across the U.S., public health advocates promote bottled water consumption as a preventative measure, further accelerating adoption rates across diverse consumer segments.

Convenience and On-The-Go Consumption Dynamics

Modern consumer lifestyles characterized by rapid urbanization, busy schedules, and increased mobility have established bottled water as the quintessential on-the-go beverage, driving unprecedented demand for portable, single-serve hydration solutions. The convenience factor is particularly attractive to professionals, fitness enthusiasts, and families managing time-constrained routines, where pre-packaged bottled water eliminates the need for home water filtering systems or carrying refillable containers.

Single-serve PET bottles, which account for 71.2% of the bottled water market, provide unmatched portability and accessibility, enabling consumers to maintain hydration during travel, work, and recreational activities. Modern retail infrastructure, including ubiquitous availability at supermarkets, convenience stores, and mass merchandisers like Walmart, Target, and Costco, has normalized bottled water as an impulse purchase item, supported by promotional strategies including multipack offers and bulk purchase discounts that enhance consumer accessibility regardless of geographic location or socioeconomic status.

Market Restraints

Environmental Concerns and Plastic Waste Accumulation

Despite robust market growth, rising environmental concerns over plastic waste have become a significant constraint on expansion. Increasing consumer awareness of the ecological impact of single-use plastics is driving reluctance toward plastic-intensive packaging models. Regulatory pressures are mounting, with the European Union mandating a 25% reduction in single-use plastics by 2025, setting a precedent for similar measures in the U.S..

Microplastic accumulation, transportation-related emissions, and inadequate recycling infrastructure exacerbate environmental degradation, prompting eco-conscious consumers to reconsider bottled water purchases. This challenge is most pronounced in urban areas with reliable tap water systems, where affluent demographics increasingly adopt home filtration and reusable alternatives.

Competition from Home Filtration Systems and Tap Water Advocacy

Home water filtration systems and ongoing advocacy for municipal tap water quality have intensified competition against bottled water, particularly in developed markets with reliable infrastructure. The U.S. Environmental Protection Agency (EPA) actively promotes tap water as a sustainable alternative, emphasizing educational campaigns that contrast bottled water’s environmental impact with federally regulated municipal systems.

According to NHANES data, tap water accounts for 62% of total drinking water consumption in the U.S., with affluent consumers showing a strong preference for tap water during economic downturns due to cost sensitivity. Advanced filtration technologies, such as reverse osmosis, activated carbon, and ultraviolet treatment, have narrowed the perceived quality gap, eroding bottled water’s historical advantage. This trend limits market expansion in regions with proven water quality and compels manufacturers to pursue premium strategies focused on functional additives and mineral enrichment.

Market Opportunities

Rapid Expansion of Functional and Enhanced Water Segments

Functional and enhanced water products enriched with vitamins, minerals, electrolytes, and bioactive compounds represent the fastest-growing segment in the bottled water market, projected to expand at a CAGR of 8.12% through 2031, significantly outpacing traditional still water. This category leverages premiumization trends and rising health-conscious consumer demand for beverages offering tangible wellness benefits beyond basic hydration, commanding price premiums of 200% to 400% over mass-market alternatives. Recent innovations include mineral-infused waters, electrolyte-enhanced solutions for fitness enthusiasts, and immunity-boosting formulations with added vitamins and probiotics.

Brands such as RAIN Pure Mountain Spring Water and Water Almighty have introduced aluminum-bottled spring water and mineral-enriched variants targeting eco-conscious and health-focused consumers. This opportunity aligns with growing preferences for personalized hydration, addressing objectives like athletic recovery, cognitive performance, and immune support, enabling manufacturers to capture high-margin revenue streams while differentiating in competitive markets.

Sustainable Packaging Innovation and Premiumization Potential

The shift toward sustainable packaging materials, such as aluminum cans, recycled PET (rPET), glass, and plant-based alternatives, offers significant growth opportunities for brands prioritizing environmental responsibility. Aluminum cans, with 100% recyclability and infinite reuse potential, are witnessing rapid adoption at a 7.0% CAGR through 2030, driven by consumers willing to pay premiums for eco-friendly formats. The premium bottled water segment increasingly leverages sustainable packaging as a key differentiator, emphasizing recycled content, biodegradable materials, and plastic-free solutions.

Strategic collaborations, including Nestlé’s launch of plant-based bottles with Acreto and PepsiCo’s partnership with LanzaTech to produce water from captured carbon emissions, underscore industry commitment to sustainability. These initiatives enable brands to command higher pricing, strengthen eco-conscious brand equity, and tap into emerging segments such as eco-luxury and premium wellness products.

Category-wise Insights

Product Type Analysis

Purified water continues to dominate the U.S. bottled water market with a share exceeding 40%, driven by consumer preference for water perceived as free from impurities, chemicals, heavy metals, and microbial contaminants. Its strong position is supported by advanced filtration technologies that ensure superior cleanliness compared to alternative sources. Health-conscious consumers favor purified water over spring or mineral variants, particularly in regions with heightened concerns about municipal water safety.

The convenience of portable, reliable hydration for travel, work, and recreation further sustains demand. Leading brands such as Aquafina and Dasani, both sourced from municipal systems, maintain market leadership through extensive distribution networks and strategic marketing. Economies of scale, efficient retail penetration, and strong brand familiarity enable consistent volume growth despite rising competition from mineral and functional water segments.

Packaging Type Analysis

PET (Polyethylene Terephthalate) bottles dominate the U.S. bottled water packaging segment with over 80% market share, driven by advantages such as convenience, lightweight portability, cost efficiency, and an established recycling infrastructure. Standardized PET recycling programs, including deposit return schemes and municipal collection systems, have reinforced consumer perception of PET as an environmentally acceptable option despite growing sustainability concerns. Single-serve PET bottles remain integral to on-the-go consumption across sports, workplace hydration, and travel scenarios, supported by attributes like reduced transportation emissions, shatter resistance, and product visibility through transparent packaging.

However, aluminum cans are gaining traction at a 7.0% CAGR, appealing to eco-conscious consumers with superior recyclability, infinite reuse potential, and premium positioning. The packaging landscape is evolving, with PET dominating mass-market segments while aluminum and glass formats increasingly cater to premium and sustainability-focused demographics willing to pay higher prices for environmentally responsible solutions.

Distribution Channel Analysis

Supermarkets remain the dominant distribution channel for bottled water, accounting for approximately 80% of market share. Their leadership is driven by extensive product assortments, competitive pricing through volume discounts, and convenient retail locations. These off-trade channels enable consumers to compare brands and select products based on water type, price, and packaging format. Supermarkets and grocery stores cater to bundled shopping preferences while leveraging strong negotiating power with manufacturers to secure favorable pricing and promotional support.

Leading retailers such as Walmart, Target, Kroger, and Costco exert significant influence over category management, shaping brand visibility and purchasing behavior. Convenience stores serve as secondary channels for impulse purchases and immediate hydration needs, whereas mass merchandisers and warehouse clubs focus on bulk sales for price-sensitive households. This concentration of distribution power favors established national brands with robust networks, creating barriers for smaller regional competitors.

Regional Insights

Northeast U.S. Bottled Water Trends

The Northeast U.S., including major metropolitan areas such as New York, Boston, Philadelphia, and Washington D.C., represents the leading regional market for bottled water, with a market share of 34%. This dominance is driven by established consumption patterns, high health consciousness, and a mature retail infrastructure. Affluent urban populations exhibit strong per-capita consumption and a preference for premium and specialty products, including mineral water, functional beverages with added nutrients, and eco-friendly packaging formats like aluminum and glass.

Premiumization trends continue to enhance revenue per unit despite moderate volume growth. Aging water infrastructure and historical contamination incidents have reinforced consumer concerns about tap water quality, sustaining bottled water demand as a perceived safer alternative. Additionally, regulatory frameworks in states such as Massachusetts, New York, and Connecticut emphasize sustainability and plastic reduction, incentivizing manufacturers to adopt eco-friendly packaging and positioning environmental responsibility as a key brand differentiator.

Southeast U.S. Bottled Water Trends

The Southeast U.S., including Florida, Texas, Georgia, and the Carolinas, is the fastest-growing regional market for bottled water, driven by rapid urbanization, population migration to Sunbelt states, and increasing water infrastructure challenges in high-growth metropolitan areas. Demographic expansion and relocation patterns are creating strong demand among consumers adapting to varying municipal water quality standards. Hurricane-prone states such as Florida, Louisiana, and Texas sustain emergency demand for bulk-packaged water during storm seasons when boil advisories and infrastructure disruptions occur.

The region shows high preference for large-volume multi-packs and bulk formats, appealing to price-sensitive households and businesses requiring substantial hydration solutions. Retail expansion in emerging metropolitan areas is accelerating distribution through supermarkets, convenience stores, and mass merchandisers. Additionally, agricultural and industrial activities, coupled with concerns over contamination from runoff and operations, reinforce consumer reliance on packaged water as a safer alternative, driving growth above the national average.

Competitive Landscape

Market Structure Analysis

The U.S. bottled water market is moderately to highly fragmented, with five major multinational corporations, Nestlé Waters, PepsiCo, The Coca-Cola Company, Groupe Danone, and Suntory Beverage & Food Ltd, holding significant market share through diversified brand portfolios targeting varied consumer segments. These leaders leverage extensive distribution networks across supermarkets, convenience stores, and direct-to-consumer channels, creating competitive barriers for smaller regional players. Strategic differentiation focuses on segmentation for mass-market, health-conscious, and sustainability-driven consumers. Industry consolidation continues through acquisitions, while innovation strategies emphasize functional water, eco-friendly packaging, and digital engagement to strengthen brand loyalty. R&D investments target personalized hydration and health-focused formulations to align with evolving consumer preferences.

Key Market Developments

- November 2024: Primo Water Corporation and BlueTriton Brands completed their merger to form Primo Brands Corporation, creating a leading North American pure-play healthy hydration company with a diversified portfolio including Poland Spring, Pure Life, Deer Park, and Ozarka.

- October 2024: The Coca-Cola Company launched bottles made entirely from 100% recycled plastic across Canada, advancing the company's World Without Waste initiative targeting 50% recycled material by 2030, with the innovation projected to conserve 7.6 million pounds of plastic and reduce 7,000 metric tons of CO2 emissions annually.

- October 2024: Water Almighty unveiled two new spring water products in aluminum bottles, Mighty Pure and Mighty Minerals, emphasizing sustainability and functionality in design and formulation, demonstrating product innovation toward functional and eco-conscious segments.

Top Companies in the U.S. Bottled Water Market

Nestlé Waters (Vevey, Switzerland) operates a diverse brand portfolio including Perrier, Poland Spring, and S.Pellegrino, commanding significant global and domestic market share through established distribution networks, premium product positioning, and continuous innovation in functional water development. The company leverages extensive manufacturing infrastructure, research capabilities, and brand equity accumulated across multiple decades to maintain a competitive advantage in premium water segments.

PepsiCo, Inc. (New York, U.S.) dominates mass-market segments through its flagship brand Aquafina, one of the world's bestselling bottled water brands with extensive retail availability across supermarkets, convenience stores, and foodservice establishments. The company's integrated beverage portfolio and global distribution infrastructure enable aggressive pricing strategies and promotional support, maintaining market leadership in high-volume commodity segments.

The Coca-Cola Company (Atlanta, U.S.) competes through the brand Dasani and operates substantial bottled water operations across North America and internationally, leveraging unmatched retail distribution, brand recognition, and marketing resources to maintain significant market share in mass-market and premium segments. The company's vertical integration, spanning manufacturing, distribution, and retail, enables operational efficiency, supporting competitive pricing and market penetration.

Companies Covered in U.S. Bottled Water Market

- Nestlé Waters

- PepsiCo, Inc.

- The Coca-Cola Company

- Groupe Danone

- Suntory Beverage & Food Ltd

- Mountain Valley Spring Company LLC

- CG Roxane LLC

- Momax Technology Ltd.

- Fromm Works Inc.

- KobraTech

- Primo Water Corporation

- FIJI Water Company LLC

- National Beverage Corp.

Frequently Asked Questions

The U.S. Bottled Water Market was valued at US$ 53.0 billion in 2026 and is projected to reach US$ 78.1 billion by 2033, growing at a CAGR of 5.7% throughout the forecast period, driven primarily by health consciousness and sustainability initiatives.

The market growth is primarily driven by rising health and wellness consciousness as consumers switch from sugary beverages, increased convenience demand for on-the-go consumption, elevated water contamination concerns in certain regions, and continuous product innovation in functional water categories with added vitamins and minerals.

Purified Water maintains market leadership with approximately 40% market share, dominating due to consumer perception of superior purity from advanced filtration technologies, health consciousness prioritizing water cleanliness, brand familiarity among mainstream demographics, and widespread retail availability supporting consistent demand.

The Northeast U.S., encompassing major metropolitan areas including New York, Boston, and Philadelphia, represents the leading regional market driven by established consumption patterns, elevated health consciousness among affluent urban populations, and mature retail infrastructure with comprehensive brand availability.

Sustainable Packaging Innovation, particularly aluminum cans expanding at 7.0% CAGR, presents substantial opportunities enabling companies to command premium pricing, enhance brand equity among eco-conscious consumers, access high-margin product segments, and capture growing affluent demographics prioritizing environmental responsibility.

Major market leaders include Nestlé Waters, PepsiCo (Aquafina brand), The Coca-Cola Company (Dasani brand), Groupe Danone, Primo Water Corporation, FIJI Water Company LLC, and Mountain Valley Spring Company, collectively commanding substantial market share through diversified brand portfolios and extensive distribution networks.