- Processed Food

- Edible Offal Market

Edible Offal Market Size, Share, and Growth Forecast, 2025 - 2032

Edible Offal Market By Product Type (Liver & Kidneys, Tripe & Tongue, Others), Animal Source (Bovine, Poultry, Others), Distribution Channel, and Regional Analysis for 2025 - 2032

Edible Offal Market Size and Trends Analysis

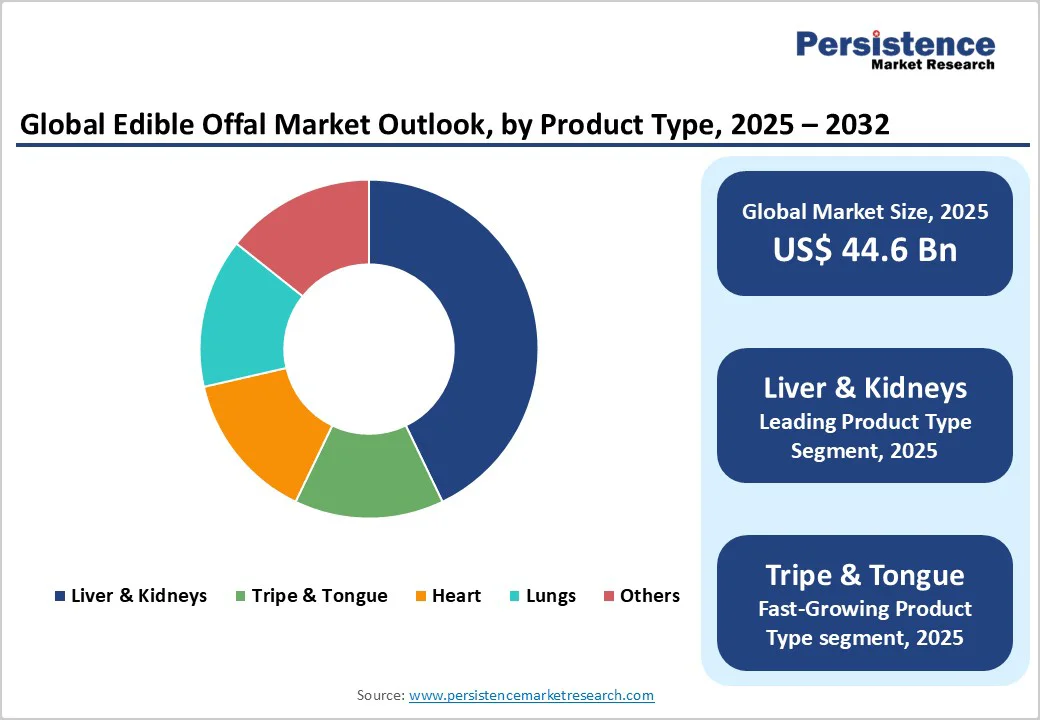

The global edible offal market size is likely to be valued at approximately US$44.6 Billion in 2025, and is expected to reach about US$59.4 Billion by 2032, growing at a CAGR of around 4.3% during the forecast period from 2025 to 2032, driven by the rising global protein consumption, increasing utilization of animal by-products in food industries, and expanding export opportunities from Asia and South America. Edible offal such as liver, kidneys, tripe, and heart remains vital in traditional cuisines, with rising demand for nutrient-rich foods and sustainable meat processing driving market growth.

Key Industry Highlights

- Leading Region: Asia Pacific accounted for 42.8% of the global market share in 2025, driven by traditional consumption patterns, strong export demand from China and India, and expanding cold chain infrastructure.

- Fastest-Growing Region: Asia Pacific, supported by livestock expansion, rising middle-class income, and regional trade integration under RCEP.

- Investment Plans: Major producers in the U.S., Brazil, and Australia are investing over US$500 Million (2024–2026) in processing automation, traceable supply chains, and cold storage infrastructure to enhance export competitiveness.

- Dominant Product Type: The liver and kidneys segment holds 41.8% market share in 2025, supported by their nutritional value and broad culinary adoption across Asia, Africa, and Europe.

- Leading Animal Source: The bovine offal segment represents 47.4% of the total market revenue in 2025, driven by abundant cattle supply and consistent export performance from Brazil, India, and the U.S.

| Key Insights | Details |

|---|---|

|

Edible Offal Market Size (2025E) |

US$44.6 Bn |

|

Market Value Forecast (2032F) |

US$59.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Global Demand for Protein-Rich Foods

Global per-capita meat consumption has increased by nearly 14% between 2015 and 2023, driven by economic growth in Asia, Latin America, and Africa (FAO, 2024). Edible offal, recognized for its high protein content (15–22%) and micronutrients such as iron and vitamin A, serves as an affordable protein source in lower- and middle-income economies. As the global population surpasses 8 billion, and protein demand is expected to rise by approximately 75% by 2050, the offal market provides a sustainable avenue for meeting nutritional needs while minimizing carcass wastage.

Circular Economy and Waste Minimization in Meat Processing

According to the OECD and FAO (2024), nearly 30% of livestock biomass remains underutilized in traditional meat processing systems. Governments and industry players increasingly focus on circular utilization of animal parts, where edible offal plays a critical role. Regulatory incentives promoting waste-to-value transitions, especially in the European Union’s Sustainable Meat Processing Framework, encourage full-carcass utilization. This shift has increased offal exports from the EU by over 12% since 2020, signaling how sustainability mandates are strengthening the edible offal value chain.

Expansion of International Trade and Cold Chain Logistics

Global trade in edible offal products has expanded significantly, particularly from Australia, New Zealand, Brazil, and India to markets in China, Vietnam, and the Middle East. The improvement of cold chain infrastructure and the standardization of sanitary certifications have made international shipments more viable. For instance, China imported nearly 1.8 million tonnes of offal products in 2023, accounting for over 25% of global offal trade. Enhanced logistics and traceability systems are reducing spoilage losses and improving export profitability for meat processors.

Barrier Analysis - Cultural Perception and Declining Offal Consumption in Developed Economies

While edible offal is a traditional food staple in developing nations, it faces cultural aversion and declining demand in Western markets. In regions including North America and Northern Europe, younger demographics often associate offal with low-quality or outdated cuisine. As a result, offal consumption per capita in the U.S. fell by more than 20% between 2015 and 2023 (USDA, 2024). This shift restricts premiumization potential and limits product innovation within those geographies.

Food Safety Concerns and Stringent Export Regulations

The edible offal supply chain is more sensitive to microbiological risks and contamination, particularly during handling and storage. Exporters face rigorous inspection protocols under international sanitary standards such as OIE and HACCP. Compliance costs have risen by 15–18% over the last five years for offal exporters due to stricter hygiene and traceability mandates. These constraints increase operational expenditures for small- and mid-scale processors and may slow global trade expansion in the short term.

Opportunity Analysis - Product Diversification through Ready-to-Cook and Processed Offal Items

Consumer demand for ready-to-eat (RTE) and ready-to-cook (RTC) food products is reshaping the meat industry. The edible offal sector can capitalize on this through value-added processing, such as liver pâté, tripe sausages, and kidney-based snack items. The processed offal category is projected to register a CAGR of 6.1% through 2032, outpacing the raw frozen segment. Expansion of modern retail and e-commerce channels across Asia and the Middle East further supports this shift toward convenience-based food consumption.

Rising Export Potential from Developing Countries

Emerging producers such as India, Brazil, and Thailand are poised to expand their edible offal exports, supported by lower production costs and abundant livestock resources. India’s bovine offal exports alone exceeded US$1.6 Billion in 2024 (APEDA data). With improved cold storage and trade logistics, developing economies are expected to contribute nearly 40% of the incremental global supply by 2032. This opens lucrative avenues for local meat processors and investors targeting high-growth Asian and Middle Eastern demand centers.

Nutraceutical and Pet Food Industry Integration

Offal by-products are increasingly utilized in nutraceuticals, pharmaceuticals, and premium pet foods. Liver extracts and tripe powders are valuable ingredients for vitamin formulations and animal feed supplements. The global pet food market, worth over US$120 Billion in 2024, is incorporating higher protein organ meats to meet pet nutritional standards. This vertical integration enhances utilization rates and offers processors alternative revenue streams with better margins.

Category-wise Analysis

Product Type Insights

Liver and kidney segments collectively account for over 41.8% of the market share in 2025, driven by their widespread culinary use and high nutrient density. Liver is rich in vitamins A and B12, making it a sought-after ingredient in traditional dishes across Asia, Africa, and Eastern Europe. Demand is bolstered by the rising recognition of organ meats in functional nutrition. With increased cold storage capacities and rising exports from South America to China and Egypt, the liver and kidney segments continue to anchor market stability.

The tripe and tongue category is the fastest-growing segment, supported by a resurgence in ethnic and gourmet cuisines. Dishes such as Mexican menudo and Korean gopchang have gained international appeal. Global restaurant chains and specialty meat brands are reintroducing offal dishes under “nose-to-tail” sustainability campaigns. Improved packaging methods, including modified-atmosphere storage, enhance product shelf life, accelerating retail adoption.

Animal Source Insights

Bovine offal dominates the market with an estimated market share of 47.4% in 2025, primarily due to large-scale cattle production in Brazil, India, and the United States. The segment benefits from diverse utilization ranging from human consumption to pharmaceutical and pet food manufacturing. Bovine liver and heart are high in protein and essential minerals, making them core export items. With growing halal certification coverage in global trade, bovine offal maintains broad acceptance across Islamic markets.

The poultry offal segment is the fastest-growing segment. Rising global poultry production and the lower environmental footprint of chicken meat compared to red meat support demand growth. Poultry liver and gizzard are integral to Asian cuisines, while the Western market is gradually adopting chicken offal in pet food formulations. Continuous innovations in poultry slaughtering and automated processing also improve yield recovery and safety compliance.

Distribution Channel Insights

The foodservice sector accounted for over 50.5% of global edible offal sales in 2025, owing to strong demand from restaurants, catering services, and institutional kitchens. Urbanization and rising middle-class dining expenditure are encouraging offal-based dishes in quick-service restaurants (QSRs) and ethnic eateries. Chefs increasingly incorporate organ meats into gourmet menus, emphasizing sustainability. Wholesale and institutional procurement ensure price stability and consistent quality standards.

Retail and e-commerce channels represent the fastest-growing segment, reflecting a transition toward packaged and branded offal products. Online grocery platforms in China, India, and Southeast Asia now list liver, tripe, and kidney items with traceable sourcing details. Increased cold chain coverage and digital payment adoption improve last-mile distribution. The rise of health-conscious consumers exploring nutrient-dense foods further amplifies online visibility and acceptance of organ meats.

Regional Insights

North America Edible Offal Market Trends - Export-Driven Offal Market with Advanced Processing & Traceability

North America leads the market, with the U.S. representing the largest domestic market. Despite declining per-capita consumption, the region benefits from high export volumes of frozen and processed offal to Asia and Latin America. U.S. meat processors, supported by the USDA’s Meat Export Federation, leverage advanced cold storage and compliance infrastructure. Canada and Mexico contribute to steady supply chain integration through NAFTA trade routes.

Key drivers include a strong focus on sustainable meat processing, pet food diversification, and export-oriented production. Regulatory frameworks such as the USDA Food Safety and Inspection Service (FSIS) ensure traceability, enhancing export credibility. The North American market witnesses innovation in offal-based nutraceuticals and functional pet food. Companies are investing in precision rendering and value-added packaging to improve quality retention. The region attracts moderate investment activity, particularly in processing automation and logistics digitization. In 2024, major U.S. processors launched blockchain-enabled traceability systems to meet export compliance. Despite cultural limitations in domestic demand, robust export capacity sustains North America’s relevance in the global edible offal supply chain.

Europe Edible Offal Market Trends - Compliance-Focused Offal Market with Halal & Zero-Waste Initiatives

Europe edible offal market outlook remains stable, driven by high compliance standards and growing halal certification adoption to reach Middle Eastern markets, with leading countries including Germany, France, Spain, and the U.K. Consumption patterns are polarized; Southern European markets show steady domestic intake through traditional recipes, while Northern regions rely heavily on exports. Germany remains the largest offal exporter within the EU, benefiting from integrated slaughterhouses and standardized certification systems under EU Regulation 853/2004.

Growth is supported by eco-efficiency mandates and animal by-product utilization policies within the EU’s Green Deal framework. The market benefits from government-backed research on nutrient recovery and zero-waste processing. France’s “zero-loss meat value chain” initiative (2023) has improved by-product conversion efficiency by 10%. The U.K. market sees expanding ethnic food demand due to migration trends, sustaining retail offal sales in urban areas. Investment flows into plant modernization, hygienic rendering, and cross-border cold chain connectivity are rising, with over €480 million invested in 2024–2025.

Asia Pacific Edible Offal Market Trends - High-Consumption, Fast-Growing Offal Market with Regional Trade Expansion

Asia Pacific dominates the market, accounting for over 42.8% of global revenue in 2025 and projected to remain the fastest-growing region through 2032. China, India, Japan, and ASEAN nations constitute the largest consumer bases. The region’s growth is fueled by traditional dietary habits, large livestock bases, and expanding meat export industries.

China remains the single largest importer, sourcing offal primarily from Australia, Brazil, and the U.S. India leads in buffalo offal exports, serving over 60 international destinations under its APEDA-regulated export system. Japan and South Korea maintain stable consumption through restaurant chains specializing in yakiniku and gopchang cuisine. Regulatory structures such as China’s General Administration of Customs (GACC) have tightened quality oversight, improving trust in imported products. The expansion of regional trade blocs (RCEP and ASEAN agreements) is reducing tariffs and enhancing supply continuity. Investments in modern abattoirs and refrigeration logistics, particularly in India and Vietnam, are rapidly increasing. The region’s market is characterized by competitive fragmentation, with domestic processors scaling production for both human consumption and industrial by-product applications.

Competitive Landscape

The global edible offal market is moderately fragmented, with the top 10 companies accounting for around 32% of total market revenue in 2025. The market features a mix of multinational meat conglomerates and regional processors. Consolidation is growing as firms pursue vertical integration, linking slaughtering, processing, and export logistics. Competitive positioning depends on cost efficiency, hygiene standards, and global certification compliance.

Key players emphasize innovation, cost leadership, and market expansion. Investment in digital traceability, product diversification (offal-based snacks and pet foods), and strategic partnerships with logistics providers remains central. Leading firms are also implementing sustainable rendering technologies to improve yield recovery and carbon efficiency.

Key Industry Highlights

- In April 2024, Tyson Foods Inc. expanded its Arkansas processing facility with a US$75 Million investment to enhance organ meat recovery and packaging automation. The initiative aligns with Tyson’s sustainability goals and strengthens its export competitiveness.

- In August 2024, JBS S.A. acquired a 40% stake in Brazil-based Nova Alimentos, focusing on frozen offal exports to Asian markets. The partnership aims to increase JBS’s processed offal output by 25% by 2026.

- In February 2025, Australian Agricultural Company (AACo) launched a traceable offal export program using blockchain to track product provenance across Japan and South Korea. This enhances consumer transparency and food safety assurance.

Companies Covered in Edible Offal Market

- Tyson Foods Inc.

- JBS S.A.

- Danish Crown Group

- Vion Food Group

- NH Foods Ltd.

- Australian Agricultural Company (AACo)

- BRF S.A.

- Cargill Inc.

- Marfrig Global Foods

- Minerva Foods

- Foyle Food Group

- Kerry Group Plc.

- Allanasons Pvt. Ltd.

- Friboi

- Tönnies Group

- Smithfield Foods Inc.

- Hormel Foods Corporation

- Olymel L.P.

- Nippon Meat Packers Inc.

- ABP Food Group

Frequently Asked Questions

The edible offal market size is estimated at US$44.6 Billion in 2025.

By 2032, the market is projected to reach US$59.4 Billion.

Key trends include the surging demand for nutrient-rich and affordable protein, expansion of ready-to-cook offal products, increased exports from emerging markets (India, Brazil, Thailand), and integration of organ meats into pet food and nutraceutical applications.

The liver and kidneys segment leads the market with a 41.8% share in 2025, attributed to their nutritional value, versatility in cuisine, and high export demand from Asia and the Middle East.

The edible offal market is expected to grow at a CAGR of 4.3% between 2025 and 2032.

Major players include Tyson Foods Inc., JBS S.A., NH Foods Ltd., Australian Agricultural Company, and Danish Crown Group.