- Medical Devices

- Global Co2 Incubators Market

Global Co2 Incubators Market Size, Share, and Growth Forecast 2026 - 2033

CO2 Incubators Market by Product Type (Water-jacketed CO2 Incubators, Direct heat CO2 Incubators, Air jacketed CO2 Incubators), by Application (Tissue engineering, In vitro fertilization, Neuroscience research, Cancer research, Others), by End-user, by Regional Analysis, 2026-2033.

Co2 Incubators Market Size and Trend Analysis

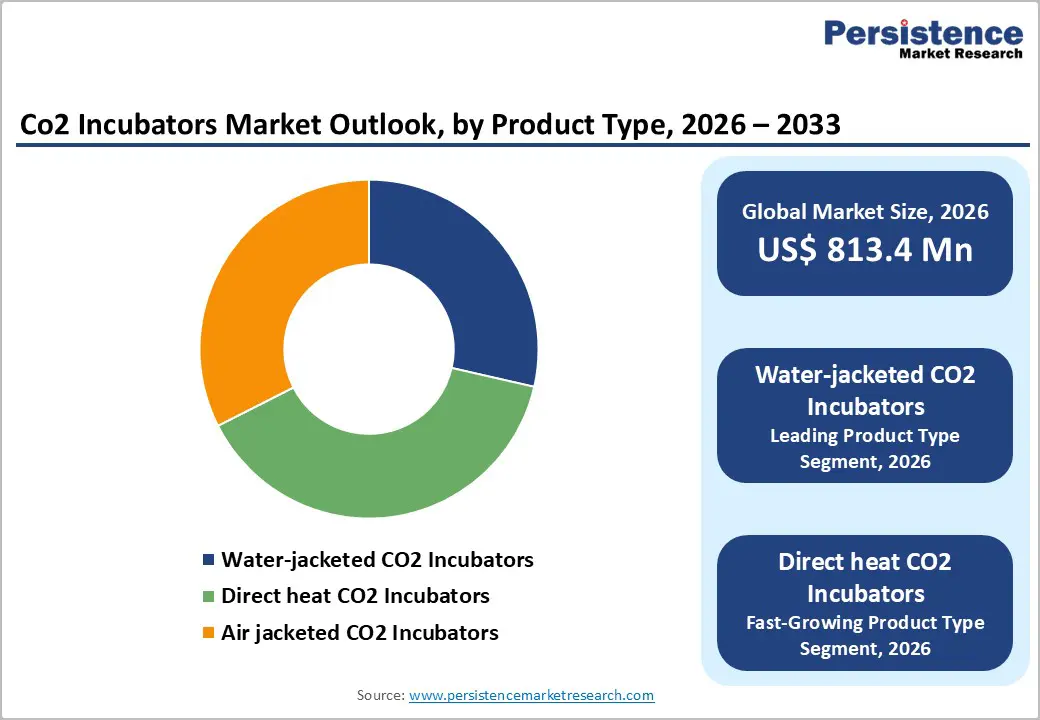

The global CO2 incubators market size is expected to be valued at US$ 813.4 million in 2026 and projected to reach US$ 1,167.7 million by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

CO2 incubators are used for a wide range of application which includes cell culture development, research in field of cancer and neuroscience, tissue engineering, embryonic cell research, etc. Thus, the increasing number of applications of CO2 incubators is expected to drive the growth of the CO2 incubators market during the forecast period.

One of the rising concerns among researchers has been avoiding the contamination of cells while conducting research. The recent advances in CO2 incubators that involves development of CO2 incubators with heat sterilization and air filters such as HEPA are steps taken by the manufacturers to avoid cell contamination and help the researchers to get better results.

Apart from this, the manufacturers are also addressing the need of special features required for special cells. For instance, Biospherix’s X3 incubator can be configured into individual chambers that can in effect become multiple smaller chambers, with independent controls that enables to optimize different conditions in each chamber. These advances by the manufacturers will help the CO2 market to grow at a considerable rate during the forecast period.

The outbreak of Covid-19 has a mixed impact on the CO2 incubators market. The growing investment in research by government as well as private sector to combat the virus is expected to have a positive impact and lead to have a slight positive growth in revenue of the CO2 incubators market. However, the initial lockdown and the disruption in the supply chain may have led to a slight drop in the CO2 market in the initial few months of 2020.

Key Industry Highlights

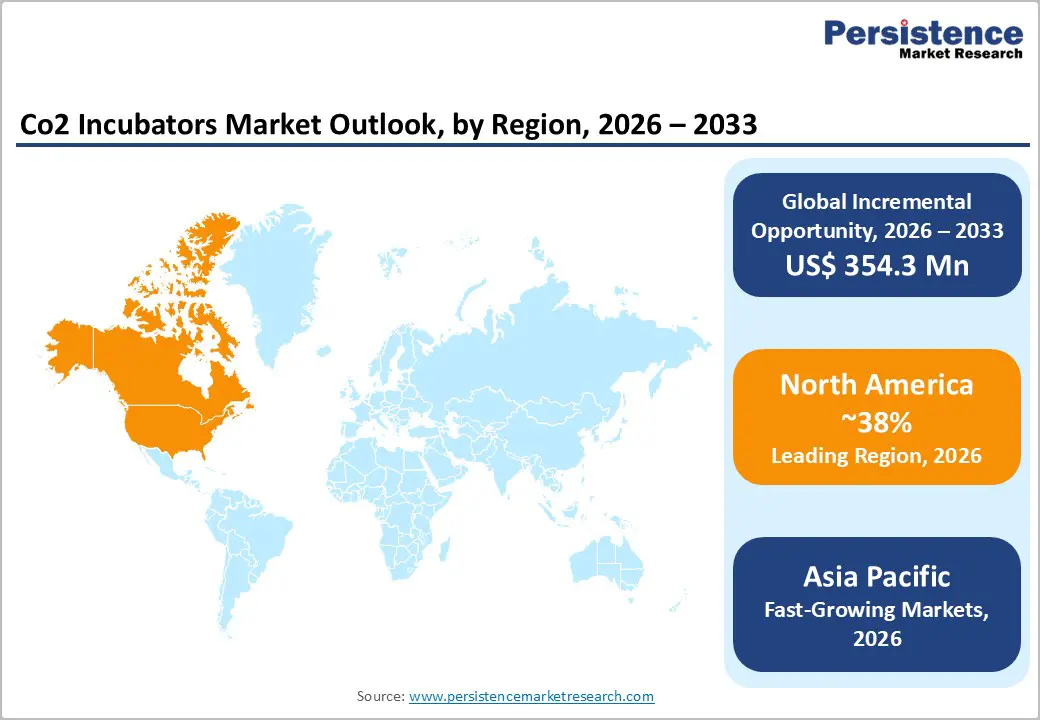

- Leading Region: North America leads the global CO2 incubators market, supported by advanced life sciences research, strong biopharmaceutical infrastructure, and high adoption of IVF and cell culture technologies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising stem cell and regenerative medicine research, expanding biopharma manufacturing, government funding, and increasing laboratory infrastructure.

- Dominant Segment: Water-jacketed CO2 incubators are the dominant product segment, owing to superior thermal stability, uniform heating, reliability for long-term cell culture, and proven GMP compliance.

- Fastest Growing Segment: Direct-heat CO2 incubators are the fastest-growing segment, supported by rapid temperature recovery, reduced contamination risk, compact stackable designs, and adoption in high-throughput biopharma and research labs.

| Global Market Attributes | Key Insights |

|---|---|

| Co2 Incubators Market Size (2026E) | US$ 813.4 Mn |

| Market Value Forecast (2033F) | US$ 1,167.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.6% |

Market Dynamics

Driver – Surge in biopharmaceutical and cell therapy production

A primary driver of the global CO2 incubators market is the rapid expansion of biopharmaceutical manufacturing and cell-based therapies, which require precise environmental conditions to support cell growth, proliferation, and differentiation. Biopharmaceutical companies account for nearly 41–48% of cell culture end-user demand, fueled by the production of monoclonal antibodies, vaccines, and gene therapies that rely on scalable mammalian cell cultures. Stem cell research and regenerative medicine further accelerate this demand, with Asia Pacific’s stem cell markets experiencing double-digit growth due to government investments, such as China’s $18 billion biotech plan. These trends increase the need for advanced CO2 incubators capable of maintaining 37°C, 5% CO2, and high humidity over long culture periods to ensure reproducibility and cell viability.

Another key growth factor is the rising demand from in vitro fertilization (IVF), tissue engineering, and neuroscience and oncology research. IVF clinics and stem cell labs require incubators with superior temperature uniformity, contamination control, and rapid recovery features to replicate physiological conditions accurately. High-throughput research labs also prefer multi-gas and hypoxic incubators to support organoid cultures and 3D tissue models, further boosting CO2 incubator adoption across academic, clinical, and commercial settings globally.

Restraints – High capital and maintenance costs

A significant restraint in the CO2 incubators market is the high capital and operational costs associated with advanced incubator models. Water-jacketed and direct-heat incubators require substantial upfront investment, alongside recurring expenses for installation, validation, and maintenance. Water-jacketed units need regular distilled water refills, cleaning to prevent contamination, and long stabilization times, increasing operational overhead. Advanced features like HEPA filtration, UV sterilization, and multi-gas controls further add to costs, limiting adoption in budget-constrained laboratories and emerging markets.

Additionally, stringent regulatory standards imposed by agencies such as the FDA and EMA for GMP-grade cell culture equipment necessitate rigorous validation, IQ/OQ/PQ documentation, and compliance with ISO Class 5 cleanroom conditions. Labs must demonstrate rapid CO2 recovery and stable environmental conditions, extending procurement timelines and favoring established brands over cost-sensitive or custom solutions. Inconsistent ambient conditions in smaller facilities or research centers may also challenge incubator performance, further hindering adoption of high-end models in some regions.

Opportunity – Direct heat incubators for rapid recovery and contamination control

A major opportunity in the CO2 incubators market lies in direct-heat models, which offer rapid temperature recovery and enhanced contamination control. These incubators can reach 37°C within approximately eight hours and utilize high-heat sterilization to minimize microbial risk. Features such as independent humidity pans, door heaters, and H2O2 decontamination capabilities make them ideal for high-throughput biopharmaceutical laboratories, research institutes, and IVF clinics that require frequent access to culture samples. As the Asia Pacific biopharmaceutical sector expands at 7.9–12.8% CAGR, demand for compact, stackable direct-heat incubators with multi-gas functionality is expected to rise significantly.

Another growth opportunity exists in supporting stem cell, oncology, and organoid research. Hypoxic and 3D culture-capable incubators are critical for translational medicine, personalized therapies, and regenerative medicine studies. Smart incubators equipped with IoT monitoring, predictive maintenance, and compatibility with organ-on-chip systems can differentiate manufacturers and target academic and clinical laboratories in high-growth regions. Government support for regenerative medicine in countries such as India, Japan, and China will further amplify demand for versatile incubators in tissue engineering, neuroscience, and cancer research, providing long-term growth potential.

Category-wise Analysis

By Product Type Analysis

Water-jacketed CO2 incubators lead the product type segment due to their superior thermal stability, uniform heat distribution, and resilience during power outages. These incubators use a water-filled jacket to maintain 37°C for extended periods, offering 4–5 times longer temperature retention than direct-heat models, which is critical for vibration-sensitive and long-term cultures such as stem cells and primary mammalian cell lines. Their water jackets and integrated cooling coils buffer against ambient fluctuations, ensuring consistent conditions for sensitive experiments in biopharmaceutical manufacturing, IVF procedures, and academic research. Despite requiring more routine maintenance, including water refills and cleaning to prevent microbial contamination, water-jacketed incubators are preferred in GMP-compliant environments due to their reliability, uniformity, and low thermal drift. Laboratories focused on process development, long-term culture stability, and high-value cell production continue to favor these models, reinforcing their dominant position in the CO2 incubator market.

By End-user Analysis

Biopharmaceutical companies are the leading end-users of CO2 incubators, reflecting the large-scale cell culture requirements for biologics and advanced therapies. These companies account for a significant portion of global cell culture demand, particularly for monoclonal antibodies, recombinant proteins, and cell therapy production, where incubators provide controlled temperature, CO2 concentration, and humidity to ensure consistent growth and batch-to-batch reproducibility. Incubators are extensively used in process development, scale-up, and GMP manufacturing of mammalian cell lines such as CHO and HEK293. Rigorous contamination control, uniform environmental conditions, and regulatory compliance make high-performance CO2 incubators essential for biopharmaceutical operations. While academic and research laboratories contribute to overall demand, the volume and scale of biopharmaceutical production combined with investments in regenerative medicine, gene therapies, and vaccine development drive the segment’s leadership. The integration of CO2 incubators into large production pipelines ensures reliability, efficiency, and reproducible outcomes, maintaining biopharma companies as the dominant end-user category in the global market.

Region-wise Insights

North America CO2 Incubators Market Trends

North America represents a mature and leading market for CO2 incubators, driven by strong biomedical research activity, advanced healthcare infrastructure, and widespread adoption of assisted reproductive technologies. The United States accounts for most of the regional demand, supported by a high number of fertility clinics and academic research institutions conducting cell culture–based studies. CO2 incubators are extensively used in in vitro fertilization laboratories, stem cell research, cancer biology, and vaccine development, ensuring stable baseline demand. Continuous funding from government agencies and private organizations supports life science research, encouraging laboratories to upgrade to advanced incubators with improved contamination control, gas uniformity, and digital monitoring. In addition, the presence of major biotechnology and pharmaceutical companies accelerates replacement demand for high-performance incubators compliant with stringent laboratory standards. Growth is further supported by increasing focus on personalized medicine, cell-based therapies, and regenerative research, which rely heavily on controlled cell culture environments.

Asia and Pacific CO2 Incubators Market Trends

Asia Pacific is expected to witness strong growth in the CO2 incubators market, supported by expanding pharmaceutical and biotechnology research, rising investments in life sciences, and increasing clinical research activity. Countries such as China, Japan, South Korea, and India are strengthening their research infrastructure through government funding and private sector investment. CO2 incubators are increasingly adopted in academic laboratories, contract research organizations, and hospital research centers for cell culture, virology studies, and drug discovery. The growing focus on vaccine development, infectious disease research, and biologics manufacturing further boosts demand. In addition, the rapid expansion of fertility clinics across urban centers is increasing usage of CO2 incubators in assisted reproductive technology laboratories. Local manufacturing capabilities and the availability of cost-effective equipment improve accessibility for small and mid-scale laboratories. These factors collectively position Asia Pacific as a high-growth region in the global CO2 incubators market.

Market Competitive Landscape

The CO2 incubators market is moderately consolidated, with leading players like Thermo Fisher Inc., Esco Micro Pte Ltd., PHC Holdings Corporation, Eppendorf, and Sheldon Manufacturing Inc. commanding significant shares through comprehensive portfolios spanning water-jacketed, direct-heat, and air-jacketed models. Strategies focus on R&D for contamination-resistant designs, IoT integration for remote monitoring, and service contracts for validation support, while differentiators include rapid recovery times, multi-gas capabilities, and GMP certifications. Emerging trends involve subscription-based maintenance and modular systems tailored for biopharma scale-up.

Key Industry Developments:

- In June 2025: Thermo Fisher Scientific introduced the fully integrated IntelliStack Incubator along with CO2 Incubator Shakers, offering precise control for cell culture samples.

- September 2024: Heal Force Bio-meditech Holdings Limited unveiled the Heal Force HF180 CO2 Incubator to enhance cell culture reliability and laboratory efficiency.

Companies Covered in Global Co2 Incubators Market

- Thermo Fisher Inc.

- NuAir Inc.

- Esco Micro Pte ltd.

- Bionics Scientifics

- Sheldon Manufacturing Inc.

- Cardinal Health

- PHC Holdings Corporation

- Toshvin

- Amphenol advanced sensors

- Heal Force

- Eppendorf

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 813.4 Mn in 2026.

Rising demand for in vitro fertilization, increasing cell culture research, vaccine development, and biotechnology advancements globally.

The global market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Expansion in Asia Pacific, adoption in regenerative medicine, advanced incubator technologies, and growing pharmaceutical and academic research sectors.

Key companies include Thermo Fisher Inc., NuAir Inc., Esco Micro Pte Ltd., Bionics Scientifics, and Sheldon Manufacturing Inc.