- Non-food Packaging

- Cap Liner Market

Cap Liner Market Size, Share, and Growth Forecast, 2026 - 2033

Cap Liner Market by Product Types (Heat Induction Cap Liner, Foam Liners, Others), Materials (Plastic, Rubber, Others), Applications, End-user Industry, and Regional Analysis for 2026 - 2033

Cap Liner Market Size and Trends Analysis

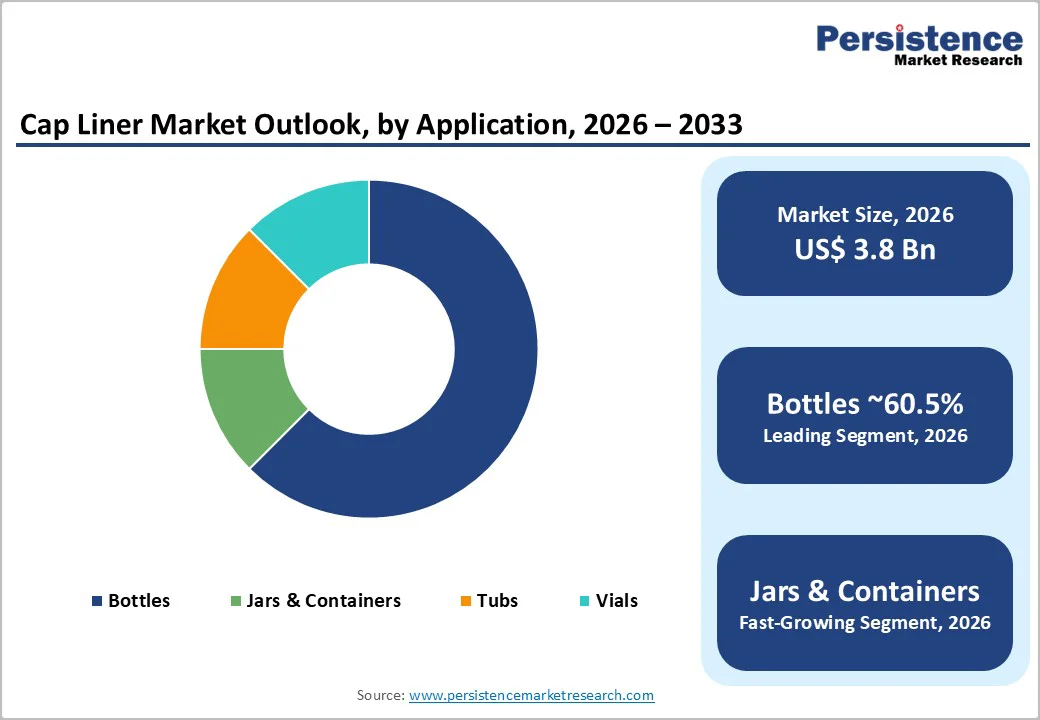

The global cap liner market size is likely to be valued at US$3.8 billion in 2026. It is expected to reach US$4.9 billion by 2033, growing at a CAGR of 3.7% between 2026 and 2033, supported by the rising need for tamper-evident and high-barrier sealing solutions, particularly across food & beverage and pharmaceutical packaging.

Stricter container-closure regulations and rising brand risk management are reinforcing the role of cap liners as essential packaging components. Heat induction liners dominate due to their reliable sealing and tamper-evidence, while sustainability and recycled-content mandates are driving material innovation. Market growth remains steady, led by North America, with Asia Pacific growing fastest.

Key Industry Highlights:

- Leading Region: North America is expected to account for approximately 37% of global market revenue in 2026, supported by high packaged food and beverage consumption, robust pharmaceutical manufacturing activity, and stringent regulatory requirements that favor tamper-evident and validated liner systems.

- Fastest-Growing Region: Asia Pacific, to register the highest growth rate globally, driven by the rapid expansion of packaged food, FMCG, and pharmaceutical production in China and India, alongside rising adoption of high-performance liner solutions across Japan and ASEAN markets.

- Investment Plans: Market participants are prioritizing investments in induction sealing technology, recyclable-compatible liner materials, and regional capacity expansion, particularly in North America and the Asia Pacific, to align with sustainability mandates and support high-volume bottling and pharmaceutical packaging demand.

- Dominant Product Types: Heat induction cap liners are anticipated to hold approximately 45% market share in 2026, owing to their superior barrier performance, tamper-evident sealing, and widespread use in beverages, edible oils, and pharmaceutical packaging.

- Leading Applications: Bottles are estimated to account for approximately 60.5% of revenue share in 2026, supported by high global consumption of packaged beverages, edible oils, sauces, and liquid pharmaceuticals, as well as the widespread adoption of induction-sealed closures for leak prevention and tamper-evident protection.

| Key Insights | Details |

|---|---|

| Cap Liner Market Size (2026E) | US$3.8 Bn |

| Market Value Forecast (2033F) | US$4.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory and Product Safety Requirements

Global regulatory frameworks require validated container-closure integrity and visible tamper evidence for pharmaceutical and many food products. Packaging regulations emphasize sealing performance, compatibility testing, and stability validation as part of product approval and lifecycle management. These requirements elevate the importance of cap liners in packaging qualification processes, particularly in pharmaceuticals, nutraceuticals, and regulated food categories.

As a result, demand is rising for liners that deliver documented barrier performance, tamper evidence, and compliance traceability. Pharmaceutical manufacturers increasingly favor liner suppliers capable of supporting validation documentation, extractables and leachables testing, and container-closure integrity studies.

The net impact is higher per-unit liner spending, especially for regulated and high-value product lines, reinforcing long-term demand stability for premium liner solutions.

Food & Beverage Volume Growth and Tamper-Evidence Expectations

Food & beverage remains the largest end-use sector for cap liners as rising consumption of bottled drinks, edible oils, sauces, and packaged condiments continues to drive large-scale liner usage. At the same time, consumer expectations for freshness, leak prevention, and visible tamper evidence have increased sharply.

These expectations are driving brand owners toward heat-induction foil liners and multi-layer sealing systems to enhance shelf life and product safety. As packaging shifts toward single-serve and on-the-go formats, liner performance becomes even more critical. The result is sustained volume growth in bottle-focused liner applications, with heat-induction liners capturing a growing share of value due to their premium performance characteristics.

Sustainability and Recycled-Content Policy Pressure

Environmental regulations and corporate sustainability commitments are accelerating the shift toward recyclable and recycled-content packaging components. Policy initiatives aimed at improving packaging recyclability and reducing plastic waste are prompting brand owners to reassess liner materials and designs.

This shift is driving investment in mono-material liners, recyclable induction seals, and paper-based alternatives that align with circular economy objectives. At the same time, companies are investing in testing protocols to validate the use of recycled materials in food-contact applications. The market impact is a gradual but sustained increase in demand for sustainable liner variants, alongside retrofit projects to qualify new materials without compromising seal integrity or regulatory compliance.

Barrier Analysis - Capital Intensity of Induction Sealing Equipment

Heat induction liners require dedicated induction sealing equipment and validated production processes. Retrofitting existing packaging lines or adding new induction sealing capability involves significant upfront capital expenditure. For small and mid-size packaging operations, equipment costs combined with process validation requirements can delay or limit adoption.

This structural challenge favors large integrated packaging groups and contract packers with scale advantages. Where linear systems require extensive residue, compatibility, or integrity testing, quality assurance and validation costs further increase total ownership costs. As a result, adoption of advanced liner technologies may remain uneven across smaller packaging operations.

Material Substitution and Recycling System Constraints

While demand for recyclable and recycled-content liners is rising, real-world recycling infrastructure and regulatory approval processes remain limiting factors. Approval pathways for recycled plastics in food-contact applications require extensive testing and documentation, which can slow commercialization.

In addition, inconsistent collection and recycling systems create challenges in securing reliable supplies of high-quality recycled materials. This gap between regulatory expectations and recycling system maturity increases supply-chain risk and lengthens development timelines. These constraints contribute to higher validation costs and delayed returns on investment for liner material innovation initiatives.

Opportunity Analysis - Paper-Based and Mono-Material Induction Liners

Advances in paper-based and mono-material induction liner technologies offer a viable path toward improved recyclability without sacrificing seal performance. These solutions reduce material complexity, simplify recycling streams, and support brand sustainability commitments.

If 10-15% of global heat induction liner volumes transition to recyclable paper-based or mono-material designs by 2030, the resulting incremental market opportunity could reach tens to hundreds of millions of U.S. dollars, depending on price premiums. Adoption is expected to be strongest in regions with strict recyclability mandates and among brands with aggressive sustainability targets.

Pharmaceutical-Grade Validated Liner Solutions

Pharmaceutical manufacturers increasingly favor liner suppliers that provide fully validated liner families, including container-closure integrity data, extractables and leachables documentation, and regulatory support services. Suppliers that bundle products with technical services can secure long-term contracts and premium pricing.

With pharmaceutical liner demand growing at approximately 7% CAGR and representing an estimated 5-8% of total liner volumes, this segment offers disproportionately high margins. Investments in laboratory infrastructure, regulatory expertise, and technical documentation create strong barriers to entry and long-term competitive differentiation.

Category-wise Analysis

Product Types Insights

Heat induction cap liners are anticipated to account for approximately 45% of the revenue share in 2026, supported by their superior barrier protection, tamper-evident functionality, and sealing consistency.

These liners are extensively used in carbonated and non-carbonated beverages, bottled water, edible oils, pharmaceuticals, and nutraceutical products, where contamination prevention and shelf-life stability are critical. The induction sealing process creates a hermetic seal that prevents leakage, product oxidation, and unauthorized access, making it the preferred solution for regulated and high-value packaged goods.

Their compatibility with high-speed automated bottling and capping lines further strengthens adoption among large-scale manufacturers.

Beverage producers, for example, rely on induction liners to ensure leak-proof sealing during transportation and extended storage. In pharmaceuticals, induction liners are commonly applied to syrup bottles and solid-dose containers to comply with safety and labeling requirements. The ability of heat induction liners to support premium positioning and regulatory compliance reinforces their continued dominance across global packaging markets.

Foam liners are likely to witness faster growth in unit volumes, particularly within cost-sensitive, resealable, and non-regulated applications. These liners are widely used in food jars, personal care containers, nutritional supplements, and household products, where ease of resealing and product accessibility are prioritized over tamper-evident sealing.

Their cushioning effect allows them to accommodate minor variations in container finishes, improving seal reliability in less controlled production environments.

Private-label food brands and small-to-mid-sized manufacturers increasingly favor foam liners due to lower material costs and simplified application requirements. For example, foam liners are commonly used in spice jars, cosmetic creams, and home-care liquids that require frequent opening and reclosing.

Growth is further supported by hybrid liner designs, in which foam liners are paired with induction foil seals to deliver both resealability and tamper-evidence. This dual-function configuration is gaining traction in premium food and nutraceutical packaging.

Applications Insights

Bottles are estimated to represent the largest segment, accounting for 60.5% of the revenue share in 2026, driven by high global consumption of beverages, bottled water, edible oils, sauces, and liquid pharmaceuticals. The widespread adoption of induction-sealed bottle closures ensures leak prevention, extended shelf life, and visible tamper evidence, all of which are critical in high-volume consumer markets.

Automated bottling lines and standardized neck finishes enable consistent liner performance and large-scale procurement efficiencies. In beverage applications, such as soft drinks and functional beverages, liners play a vital role in maintaining carbonation and preventing spillage during distribution.

Similarly, in pharmaceutical and nutraceutical liquids, bottle liners support product stability and regulatory compliance. The combination of high production volumes, repeat purchasing cycles, and standardized packaging formats makes bottles the primary revenue contributor for liner manufacturers globally.

Jars and containers are emerging as the fastest-growing application segment, supported by rising demand for resealable food packaging, premium condiments, spreads, and home-consumption products. Changing consumer lifestyles and increased at-home food usage have driven growth in packaged sauces, pickles, nut butters, and specialty foods, all of which rely heavily on reliable resealing performance.

Foam liners and hybrid liner systems are particularly well-suited for jar applications, as they provide consistent resealability after initial opening. For example, premium condiment jars and personal care containers often use foam-backed liners to balance product protection with user convenience.

Growth is also evident in plastic and glass storage containers used for dry foods and supplements. As brands continue to differentiate through packaging functionality and convenience, demand for jar-specific liner solutions is expected to outpace traditional bottle applications.

Regional Insights

North America Cap Liner Market Trends - Regulatory-Driven Induction Sealing and Recyclable Liner Adoption

North America accounts for approximately 37% of global cap liner revenues, with the U.S. representing the dominant share due to its large-scale packaged food, beverage, and pharmaceutical industries. High per-capita consumption of bottled beverages, functional drinks, sauces, and nutraceutical products sustains consistent demand for induction-sealed and pressure-sensitive liners.

The U.S. Food and Drug Administration’s packaging and labeling requirements, particularly for pharmaceuticals and dietary supplements, continue to reinforce the use of tamper-evident and validated liner systems across regulated categories.

Industry leaders such as Selig Group, Tekni-Plex, and Aptar have expanded investments in induction sealing technologies and liner material optimization to meet evolving safety and sustainability standards. For example, liner suppliers are increasingly offering recyclable-compatible induction liners designed to align with HDPE and PET bottle recycling streams, supporting brand commitments made by major beverage and food companies operating in the region.

Growth is also supported by automation upgrades in bottling and filling facilities, particularly in the U.S. and Canada, which favor consistent, high-performance liner solutions. As sustainability disclosures and extended producer responsibility frameworks gain traction at the state level, liner innovation remains closely tied to regulatory compliance and brand risk management.

Europe Cap Liner Market Trends - EU Sustainability Mandates Accelerating Mono-Material Liner Systems

Europe is a significant cap liner market, led by Germany, the U.K., France, and Spain, which generate the majority of revenue. The region’s market dynamics are strongly shaped by regulatory harmonization under EU packaging and waste directives, which emphasize recyclability, material reduction, and traceability. These regulations are accelerating the transition toward mono-material closures and liner systems that do not interfere with recycling processes.

European packaging converters and liner manufacturers, including Borealis-affiliated suppliers, Constantia Flexibles, and local specialty liner producers, are actively developing PVC-free, aluminum-optimized, and low-resin liner solutions to meet retailers' and brand owners' sustainability requirements.

Major food retailers and private-label brands in the U.K. and Germany increasingly mandate compliance with recyclability labeling standards, which directly influences liner material selection.

High automation levels across European filling lines also favor precision-engineered liners with consistent sealing performance. As environmental compliance becomes a procurement criterion rather than a differentiator, advanced liner solutions are becoming embedded in standard packaging specifications across the region.

Asia Pacific Cap Liner Market Trends - High-Volume FMCG Expansion and Pharmaceutical Sealing Demand

Asia Pacific is the fastest-growing regional market for cap liners, driven by rapid expansion in packaged food and beverage consumption, FMCG manufacturing, and pharmaceutical production.

China and India lead global volume growth due to rising urbanization, expanding middle-class consumption, and increased reliance on packaged essentials. Japan and ASEAN countries also drive demand for high-performance cap liner solutions, especially in pharmaceuticals, personal care, and premium food packaging.

Multinational packaging suppliers and regional players have expanded manufacturing capacity across China, India, and Southeast Asia to serve local bottlers and drug manufacturers more efficiently. Companies such as Selig Group and regional liner converters have strengthened partnerships with domestic closure manufacturers to support high-volume beverage and edible oil applications.

In India, stricter food safety enforcement and pharmaceutical export requirements are increasing the adoption of induction-sealed liners for both domestic and export-oriented packaging. Japan’s emphasis on product integrity and shelf-life extension continues to support demand for high-barrier liner technologies. As regional brands scale production and improve packaging quality, the Asia Pacific region remains the primary growth engine for the global cap liner market.

Competitive Landscape

The global cap liner market includes a mix of large integrated packaging and closure manufacturers alongside specialized liner producers. Large players benefit from global scale and integrated offerings, while specialists compete through material innovation, regulatory expertise, and niche pharmaceutical solutions. Market concentration is moderate, with a long tail of regional suppliers.

Recent developments include the launch of recyclable induction liners, partnerships focused on recycled-content integration, and continued consolidation aimed at securing proprietary technologies and expanding validation capabilities.

Leading companies emphasize product innovation, vertical integration, and service differentiation. Sustainability, regulatory support, and global supply reliability are key competitive differentiators.

Key Industry Developments

- In January 2025, TekniPlex introduced recyclable paper-based induction heat-seal liners for bottles and jars, designed to provide comparable barrier protection and tamper-evidence while supporting sustainability objectives in food, beverage, and nutrition packaging.

- In April 2025, Amcor unveiled its IMPRESSIONS closure liner technology, enabling full-color customization, including printed marks and QR codes on liner surfaces to enhance brand interaction and direct digital engagement.

Companies Covered in Cap Liner Market

- AptarGroup

- Amcor

- Berry Global

- Silgan Closures

- Crown Holdings

- Guala Closures

- TekniPlex

- Tri-Seal

- Pres-On

- MRP Solutions

- Mold-Rite Plastics

- The Cary Company

- Selig Group

- Alcoa Packaging

- Closure Systems International

- RPC Group

- United Caps

- Pelliconi & C.

- Cap & Seal Pvt. Ltd.

- Swati Polypack

Frequently Asked Questions

The global cap liner market is estimated to be valued at US$3.8 billion in 2026.

By 2033, the cap liner market is projected to reach US$4.9 billion.

Key trends include increasing use of heat induction liners for tamper evidence, rising demand for recyclable and mono-material liner solutions, growing emphasis on validated liner systems in pharmaceuticals, and gradual material innovation to support sustainability and recycled-content mandates.

Heat induction cap liners represent the leading segment, accounting for approximately 45% of the global market, driven by their superior sealing integrity, barrier performance, and widespread use in beverages, edible oils, and pharmaceutical packaging.

The market is expected to grow at a CAGR of 3.7% between 2026 and 2033.

Major players include AptarGroup, Berry Global, Amcor, Silgan Closures, and TekniPlex (Tri-Seal).