- Food Ingredients & Additives

- Encapsulated Flavors and Fragrances Market

Encapsulated Flavors and Fragrances Market Size, Share, and Growth Forecast 2026 - 2033

Encapsulated Flavors and Fragrances Market by Form (Powder, Liquid, Others), Encapsulation Technology (Spray drying, Coacervation, Fluid bed coating, Extrusion, Freeze drying, Others), End-user, and Regional Analysis, 2026 - 2033

Encapsulated Flavors and Fragrances Market Size and Trend Analysis

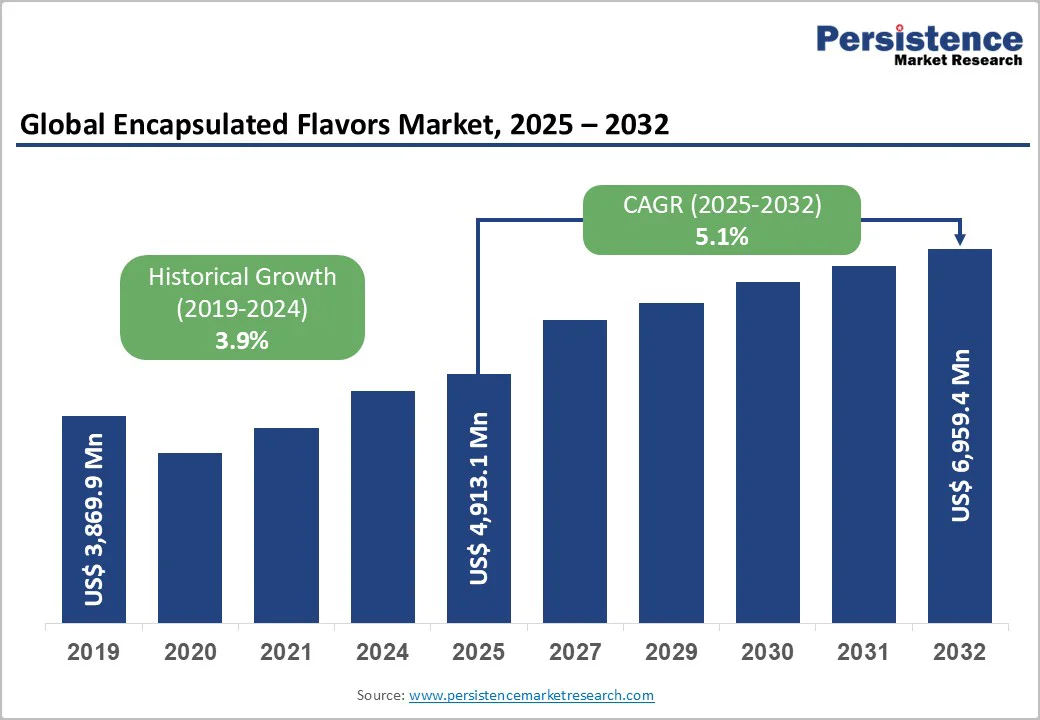

The global encapsulated flavors and fragrances market size is expected to be valued at US$ 7.3 billion in 2026 and projected to reach US$ 10.0 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033. The encapsulated flavors and fragrances market is gaining strong traction as manufacturers seek advanced technologies to improve the stability, shelf life, and controlled release of flavor and fragrance ingredients. Encapsulation protects sensitive compounds from environmental factors such as heat, moisture, and oxidation, ensuring product quality and consistency across food, beverages, cosmetics, and household products.

A key trend shaping the market is the growing demand for natural and clean-label ingredients in food and personal care products. Companies are increasingly adopting microencapsulation and nanoencapsulation technologies to deliver long-lasting sensory experiences and improve product performance. In addition, the expansion of convenience foods, functional beverages, and premium personal care products is further driving the adoption of encapsulated flavor and fragrance solutions globally.

Key Industry Highlights:

- Regional Leadership: North America is projected to remain the leading regional, supported by a mature flavors and fragrances industry, strong processed-food and home-care sectors, and continuous investments.

- Fast-growing Market: The Asia Pacific region is expected to record the fastest growth, driven by rising consumption of packaged foods, beverages, personal-care, and home-care products.

- Leading Form Type: In terms of form, powder remains the dominant segment, with an estimated 69% share in 2025, reflecting the widespread use of spray-dried encapsulated flavors in instant beverages, bakery mixes, seasonings, and dry food systems that benefit from long shelf life and ease of handling.

- Leading Encapsulation: Among encapsulation technologies, spray drying holds the largest share, estimated at about 82% of commercial encapsulated flavor production, thanks to its scalability, cost-efficiency, and ability to handle a wide range of oil- and water-soluble flavor systems for both food and non-food applications.

- Opportunity: A key opportunity lies in developing biodegradable, bio-based encapsulation platforms and advanced nanoencapsulation systems that deliver high performance while meeting tightening regulations on microplastics and synthetic polymers, particularly in laundry, personal care, and functional food applications.

| Key Insights | Details |

|---|---|

|

Encapsulated Flavors and Fragrances Market Size (2026E) |

US$ 7.3 billion |

|

Market Value Forecast (2033F) |

US$ 10.0 billion |

|

Projected Growth CAGR (2026-2033) |

4.5% |

|

Historical Market Growth (2020-2025) |

3.9% |

Market Dynamics

Drivers - Growing Demand for Stable, Clean-Label Flavor Systems in Foods and Beverages

Rising consumption of processed, convenience, and functional foods is a primary growth driver for the encapsulated flavors and fragrances market, as manufacturers seek to preserve delicate aromas and mask off notes from vitamins, minerals, and botanical extracts. Scientific reviews show that microencapsulation stabilizes volatile flavor compounds, protects them from oxidation and evaporation, and allows precise release during consumption, improving overall sensory quality and consumer acceptance. Encapsulated systems also enable incorporation of health-promoting ingredients and plant-based oils that would otherwise deteriorate or impart undesirable tastes, aligning with the surge in fortified and better-for-you products. With encapsulation in the food sector projected to grow at double-digit rates for certain functional ingredients, flavor houses and ingredient suppliers are expanding encapsulation capabilities to support new product launches and longer ambient shelf life in categories such as ready-to-drink beverages, snacks, dairy, and bakery.

Rise of Long-lasting Scents in Home and Personal Care Under Sustainability Pressure

A second powerful driver is the growing use of encapsulated fragrances in detergents, fabric conditioners, air care, and personal-care products, where microcapsules deliver controlled, long-lasting scent while limiting volatility losses in storage and use. Industry analyses of fragrance microencapsulation highlight robust growth as brands differentiate through longer-lasting, mood-enhancing scents and sensorial experiences across home and beauty products. At the same time, regulatory initiatives in Europe targeting synthetic polymer microplastics in rinse-off products are forcing innovation toward biodegradable capsule shells, pushing next-generation delivery systems into the spotlight. Leading fragrance houses such as Givaudan and DSM-Firmenich have launched biodegradable encapsulation platforms that maintain fragrance intensity while complying with emerging restrictions, reinforcing encapsulation as an essential tool for sustainable product design.

Restraints - High Production Costs and Process Complexity in Advanced Encapsulation

Sophisticated encapsulation methods such as coacervation, fluid-bed coating, and complex nano- and microcapsule systems require capital-intensive equipment and tight process control, which can increase production costs compared with conventional flavor and fragrance delivery. Spray drying remains the most economical option, but even this technique demands significant energy for hot air generation and careful optimization of feed solids, inlet temperature, and carrier composition to avoid losses of volatile actives. In markets where finished products are highly price-sensitive, such as mainstream powdered beverages or mass detergents, higher ingredient costs can hinder adoption or push buyers toward lower-loading or non-encapsulated alternatives. For smaller manufacturers, limited access to pilot-scale encapsulation lines and formulation expertise can also act as a barrier, constraining broader use of advanced systems despite their performance advantages.

Regulatory and Environmental Concerns Around Polymeric Shells and Microplastics

Another key restraint is the tightening regulatory focus on synthetic polymers and microplastics used in some fragrance and flavor capsules. The European Chemicals Agency (ECHA) has driven EU Regulation 2023/2055, which restricts synthetic polymer microparticles in rinse-off products and establishes transitional periods for encapsulated fragrance systems in detergents and personal care. This regulation, along with national initiatives aimed at reducing microplastic pollution, compels producers to redesign capsules with biodegradable or bio-sourced materials, increasing R&D and reformulation costs. Brands relying on older, non-degradable encapsulation platforms may face reformulation pressures, potential delistings, or reputational risks, particularly in environmentally sensitive markets. Meeting evolving standards while preserving performance and cost-effectiveness is, therefore a non-trivial challenge for the industry.

Opportunities- Biodegradable, Bio-based Encapsulation Systems for Next-Generation Sustainability

Shifting consumer preferences and regulatory frameworks create significant opportunities for biodegradable and bio-based encapsulation platforms in both flavors and fragrances. Fragrance leaders like Givaudan have introduced technologies such as PlanetCaps™, which deliver long-lasting scent in capsules certified as biodegradable under OECD test criteria and based on more than 50% renewable carbon, explicitly designed to help customers anticipate microplastics restrictions. Similarly, innovations like IFF’s biodegradable Envirocap fragrance capsules aim to comply with EU microplastics rules while maintaining performance in diverse laundry conditions. For flavors, encapsulation using natural carriers’ starches, proteins, gums, and solvent-free processing align with clean-label and organic-positioned foods. Companies that can scale such eco-designed systems and provide robust life-cycle data will be well positioned to secure long-term supply agreements with global food, home, and personal care brands seeking low-footprint sensory solutions.

Emerging nanoencapsulation and advanced delivery for functional, personalized products

Advanced micro- and nanoencapsulation technologies present another major opportunity, especially in functional foods, nutraceuticals, and high-value personal-care formulations. Scientific literature highlights that nanoencapsulation can improve flavor stability, bioavailability, and targeted delivery compared with conventional microcapsules, enabling more precise control of release kinetics and sensory perception. In pharmaceuticals and nutraceuticals, microencapsulation is already widely used to mask bitterness, protect active ingredients, and modulate release profiles, with strong potential to support personalized nutrition and medicine. Ingredient and flavor companies, including DSM-Firmenich, IFF, and Kerry Group, are actively investing in nanoencapsulation platforms for flavors and actives to support fortified foods, plant-based alternatives, and clinical nutrition products. As consumers increasingly expect products tailored to specific health goals and sensory preferences, encapsulation technologies that integrate data-driven formulation, modular release systems, and compatible digital manufacturing will open new premium niches in the market.

Category-wise Insights

By Form

Within form factors, powder formats dominate the encapsulated flavors and fragrances market, accounting for around 69% share in 2025. Spray-dried powders are preferred in foods, beverages, and dry mixes because they offer good flowability, ease of blending, and high stability against oxidation and volatilization. Technical literature notes that spray drying is widely used to convert flavor emulsions and essential oils into free-flowing powders, protecting sensitive compounds while simplifying storage and logistics. Powder encapsulates are extensively applied in instant beverages, bakery premixes, confectionery inclusions, and powdered seasonings, where they can be dosed accurately and remain stable throughout distribution. This explains why powders retain leadership even as liquid and slurry encapsulation grow for ready-to-drink and personal-care applications.

By Applications

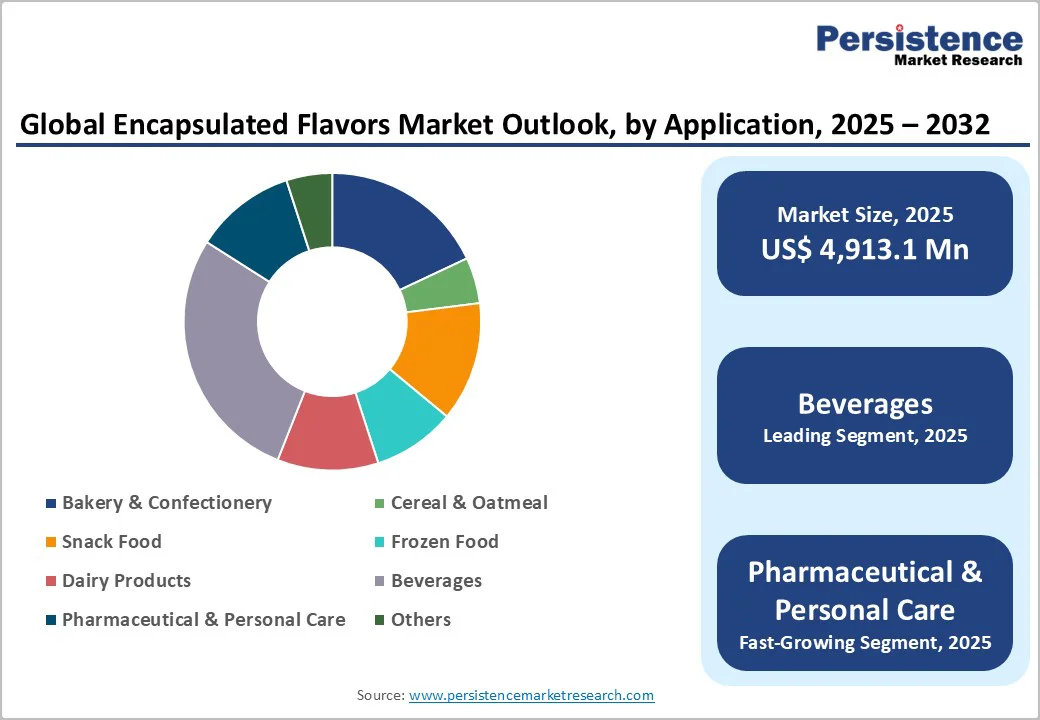

Across applications, food & beverages represent the leading end-use segment for encapsulated flavors and fragrances, accounting for an estimated market share of ~50% when combining flavors and aroma-active ingredients. Reviews of microencapsulation in the food industry show that encapsulation is widely used to protect flavors, vitamins, omega-3 oils, probiotics, and other functional ingredients from processing and storage stresses, while simultaneously masking off-tastes and controlling release. This is especially important in fortified foods, confectionery, beverages, and bakery products, where oxidative stability and flavor retention are critical for shelf life and consumer acceptance. While personal care & cosmetics, home care & household products, and pharmaceuticals are growing markets, particularly for microencapsulated fragrances and taste-masked actives, the scale and breadth of food and beverage applications cement this segment’s leadership in overall demand.

Regional Insights

North America Encapsulated Flavors and Fragrances Market Trends and Insights

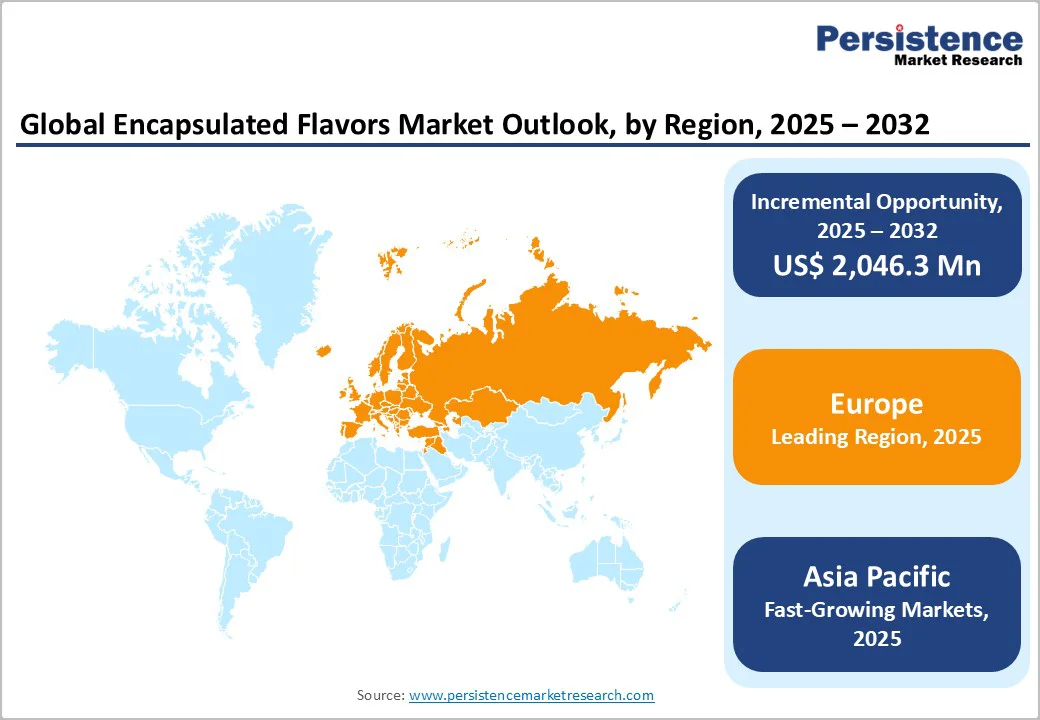

North America is the leading regional market, accounting for approximately 37% share of the global encapsulated flavors and fragrances market in 2025. The region benefits from a large, innovation-driven flavors and fragrances sector serving extensive processed-food, beverage, personal-care, and home-care industries. Market analyses of the broader flavors and fragrances space indicate that North America holds more than 20% of global revenue, underpinned by strong demand for natural, clean-label, and premium sensory experiences. Regulatory oversight from bodies such as the U.S. Food and Drug Administration (FDA) and Health Canada ensures rigorous safety evaluation of flavoring substances and fragrance ingredients, encouraging use of advanced delivery systems that maintain potency with lower dosages.

The region hosts major encapsulation and ingredient manufacturers, including Balchem Corporation, DSM-Firmenich, Ingredion Incorporated, International Flavors & Fragrances Inc. (IFF), Sensient Technologies Corporation, and Givaudan SA, which continually invest in new encapsulation plants, application labs, and digital formulation tools. Balchem’s decision to build a high-capacity microencapsulation facility in New York, expanding production of its BakeShure®, ConfecShure®, and MeatShure® systems for bakery, confectionery, and meat applications, exemplifies this commitment to scaling controlled-release technologies in the region. With retailers and consumer brands emphasizing label transparency, shelf-life extension, and differentiated taste and scent, North America is expected to remain a core market for encapsulated flavors and fragrances across both food and non-food categories.

Asia Pacific Encapsulated Flavors and Fragrances Market Trends and Insights

The Asia Pacific region represents the fastest-growing market for encapsulated flavors and fragrances, supported by rapid urbanization, rising disposable incomes, and the expansion of packaged foods, beverages, and personal-care products in countries such as China, India, Japan, and ASEAN member states. Broader flavors and fragrances analyses indicate that Asia Pacific is set to become the largest regional market globally by 2033, with particularly strong growth in natural and specialty ingredients. Encapsulation plays a central role in stabilizing flavors in powdered beverages, instant noodles, confectionery, and fortified foods that serve a growing middle class and youthful population with evolving taste preferences. In parallel, the proliferation of laundry detergents, fabric softeners, and air-care products across the region drives adoption of microencapsulated fragrances that provide long-lasting freshness under diverse washing conditions.

Manufacturing advantages such as competitive labor costs, expanding ingredient-processing capacity, and supportive industrial policies are encouraging both global and regional players to invest in encapsulation plants and R&D centers in China, India, and Southeast Asia. Companies like Givaudan SA, Symrise AG, IFF, and Takasago International Corporation have expanded their footprint in the region, adding application labs and fragrance encapsulation lines to serve local preferences and fast-moving end markets. As regulatory frameworks around microplastics and food-additive labelling continue to evolve, Asia Pacific is expected to move quickly up the value chain, combining volume growth with increased focus on sustainable and higher-performance encapsulation technologies.

Competitive Landscape

The encapsulated flavors and fragrances market is characterized by intense competition among global flavor and fragrance manufacturers focusing on advanced encapsulation technologies and product innovation. Leading companies such as Givaudan, International Flavors & Fragrances, Firmenich, Symrise, and Sensient Technologies dominate the market through strong R&D capabilities, diversified product portfolios, and global distribution networks. These players collectively hold a significant share of the market and continuously invest in microencapsulation, nanoencapsulation, and sustainable ingredient technologies to improve flavor stability and fragrance longevity. Strategic partnerships, acquisitions, and expansion into emerging markets are common competitive strategies. Additionally, smaller specialized companies are entering the market with innovative and clean-label encapsulation solutions, further intensifying competition.

Key Developments:

- In November 2025, Givaudan expanded its PlanetCaps technology for personal care applications, offering fragrance encapsulation that fully complied with ECHA standards and served as a biodegradable, microplastic-free solution. The company also introduced the IRRESISTIBLE Laundry Serum, designed to enhance scent performance in fabrics.

- In July 2025, International Flavors & Fragrances (IFF) launched ENVIROCAP, an innovative fragrance delivery technology developed for fabric care applications. The solution was fully biodegradable, vegan-compatible, and compliant with ECHA regulations.

Companies Covered in Encapsulated Flavors and Fragrances Market

- Balchem Corporation

- DSM-Firmenich

- Encapsys

- Givaudan SA

- Ingredion Incorporated

- International Flavors & Fragrances Inc. (IFF)

- Mane SA

- Matrix Flavours and Fragrances

- Robertet Group

- Sensient Technologies Corporation

- Symrise AG

- Takasago International Corporation

- Others

Frequently Asked Questions

The Encapsulated Flavors and Fragrances Market is expected to reach around US$ 7.3 billion in 2026.

A key demand driver is the growing use of encapsulated flavors to stabilize sensitive ingredients, extend shelf life, and mask off-notes in food & beverages, especially in fortified, functional, and plant-based products where clean-label positioning and consistent taste are critical.

North America currently leads the global market, supported by a large processed-food and home-care base, strong presence of major flavor and fragrance companies, and ongoing investments in advanced encapsulation facilities and technologies.

A major opportunity lies in biodegradable and bio-based encapsulation platforms and advanced nanoencapsulation systems that comply with emerging microplastics regulations while delivering high-performance flavor and fragrance release for laundry, personal care, and functional foods.

Prominent players include Balchem Corporation, DSM-Firmenich, Givaudan SA, International Flavors & Fragrances Inc. (IFF), Ingredion Incorporated, Sensient Technologies Corporation, Symrise AG, Mane SA, Robertet Group, and Takasago International Corporation, alongside regional flavor houses and encapsulation specialists.