- Non-food Packaging

- IV Infusion Bottle Seals & Caps Market

IV Infusion Bottle Seals & Caps Market Size, Share, and Growth Forecast, 2026 - 2033

IV Infusion Bottle Seals & Caps Market By Product Type (Plastic Caps, Aluminum Caps, Others), End-user (Hospitals, Pharmaceutical Manufacturers, Others), Material Type, Application, and Regional Analysis for 2026 - 2033

IV Infusion Bottle Seals & Caps Market Size and Trends Analysis

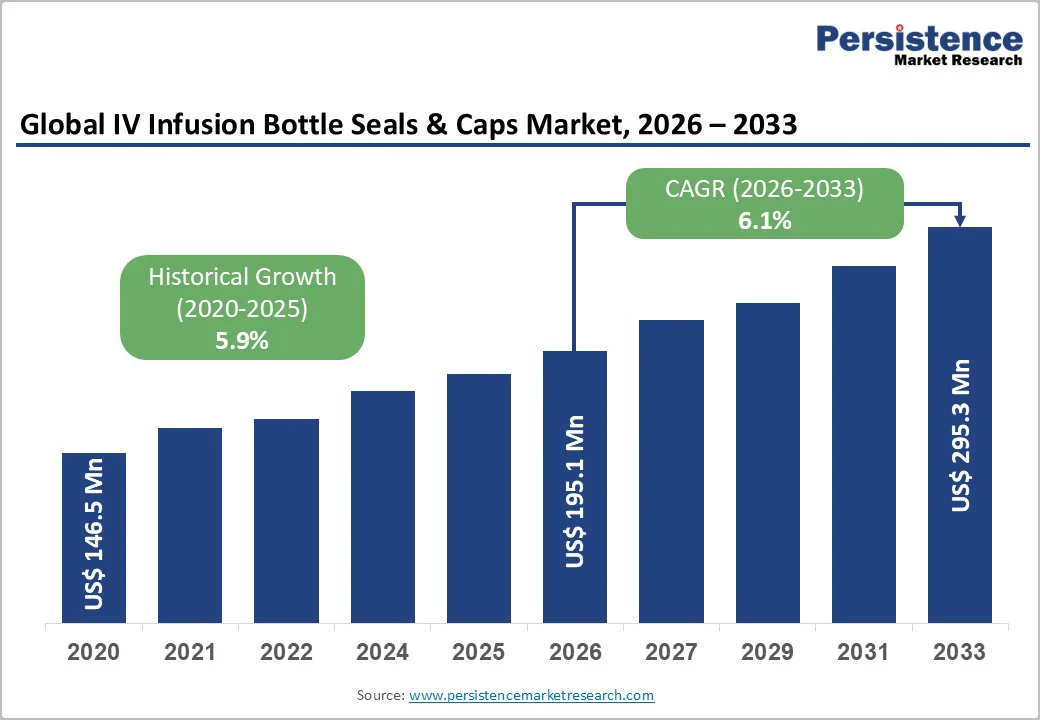

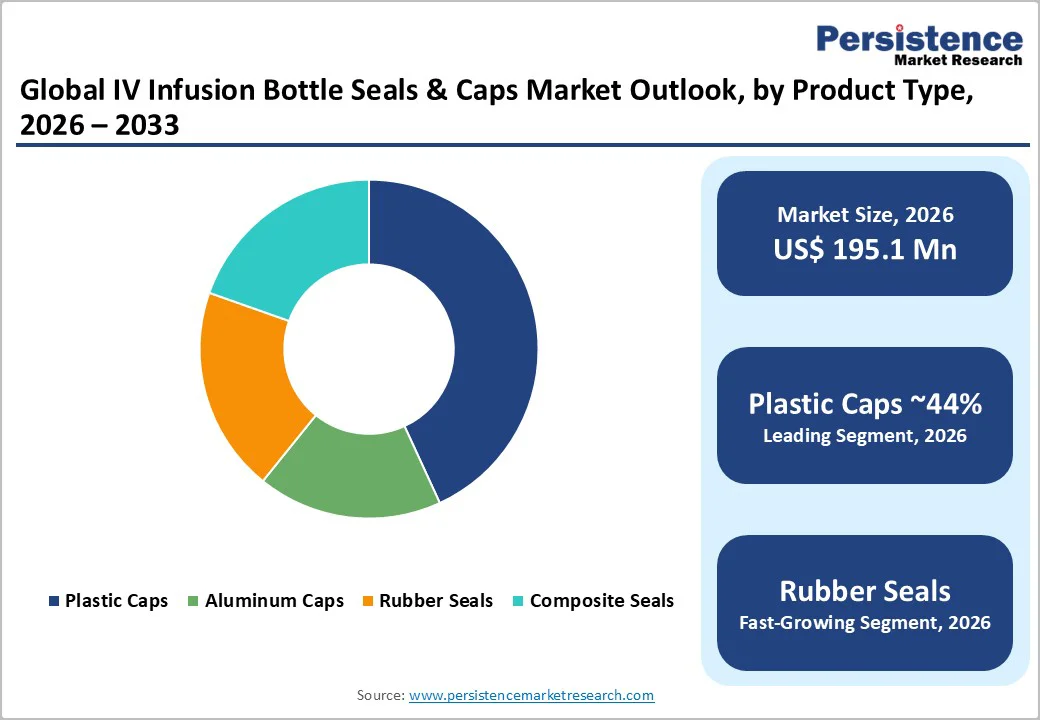

The global IV infusion bottle seals & caps market size is likely to be valued at US$195.1 million in 2026. It is expected to reach US$295.3 million by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by the rising need for reliable parenteral delivery systems in healthcare settings, where the demand for intravenous therapies continues to intensify due to broader medical applications.

The growing emphasis on contamination prevention is driving the adoption of advanced closure technologies, boosted by material innovations that improve sterility and safety. The rise of outpatient and home-based care is expanding demand for portable, secure packaging solutions that protect product integrity during transport and use.

Key Industry Highlights

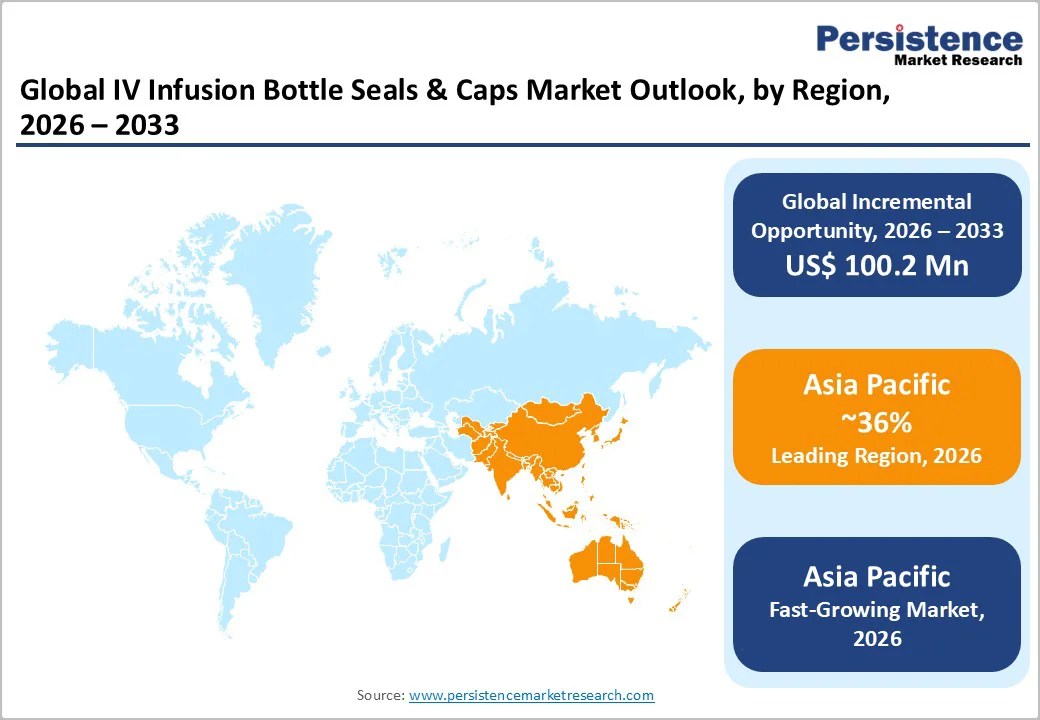

- Leading Region: Asia Pacific, expected to hold 36% of the global market share, driven by rapid healthcare infrastructure development and high-volume manufacturing in countries such as China and India.

- Fastest-growing Region: Asia Pacific, fueled by increasing chronic disease prevalence and investments in pharmaceutical production.

- Investment Plans: Major players are allocating resources toward facility expansions and R&D for sustainable materials, with examples including US$150 million in U.S. upgrades for latex-free production and US$120 million joint ventures in India for enhanced elastomer capabilities, aiming to boost capacity by 15-20% amid rising biologics demand.

- Dominant Product Type: Plastic caps, anticipated to hold 44% market share, due to their versatility, lightweight design, and compatibility with automated high-volume filling lines.

- Leading End-user: Hospitals, expected to account for 37% of the market due to high-volume procurement for inpatient infusion procedures and an emphasis on contamination prevention in clinical settings.

| Key Insights | Details |

|---|---|

| Market Size (2026E) | US$195.1 Mn |

| Market Value Forecast (2033F) | US$295.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Intravenous Therapies amid Chronic Disease Prevalence

Rising cases of chronic diseases, such as diabetes, cardiovascular conditions, and cancer, are increasing the need for frequent, reliable IV therapies, especially among aging populations that depend on long-term infusion treatments. As infection control becomes a top priority, high-quality seals and caps play a critical role in preserving sterility from production to administration.

The surge in biologics and specialty pharmaceuticals further strengthens this demand, as these sensitive drugs require robust, compliant closure systems. This direct link between growing health burdens and packaging needs not only drives consistent market growth but also pushes manufacturers to innovate with safer, tamper-evident designs, ultimately reinforcing the resilience and reliability of the medical supply chain.

Technological Advancements in Sterile Packaging Solutions

Advances in biocompatible materials and manufacturing are reshaping infusion packaging by enabling seals and caps with superior barriers against moisture, oxygen, and microbial intrusion. Low-extractable polymers and automated assembly have reduced risks of product degradation, supporting sensitive formulations such as monoclonal antibodies and vaccines.

These technologies meet growing pharmaceutical demands for closures that comply with global standards for leachables and extractables, helping minimize patient safety concerns. Improved materials also boost production efficiency, shortening lead times and reducing operational costs for hospitals and clinics.

This technological progress enhances market confidence and creates opportunities for supplier differentiation, as companies that invest in R&D can gain competitive advantages by delivering more reliable, sustainable closure solutions.

Expansion of Outpatient and Home Healthcare Services

The shift from inpatient care to community-based models is increasing reliance on home infusion programs, driving demand for lightweight, user-friendly seals and caps that are easy to open, handle, and dispose of. This trend is reinforced by efforts to reduce hospital overcrowding and expand patient self-management, supported in many regions by strong reimbursement for ambulatory services.

Closures must balance convenience with security, prompting interest in features such as flip-top mechanisms that enable quick needle access without compromising sterility. This shift highlights the need for adaptable, reliable packaging that supports decentralized care, where usability directly affects treatment adherence.

Manufacturers are responding with ergonomic designs and closures compatible with portable infusion devices, expanding access to therapies once confined to clinical settings.

Barrier Analysis - Regulatory Compliance and Validation Challenges

Navigating the complex web of international regulations for pharmaceutical packaging presents ongoing hurdles for industry participants, as approvals demand extensive testing for material compatibility, sterility assurance, and environmental impact.

These requirements often extend development timelines and inflate costs associated with documentation and audits, particularly for smaller firms entering the space. The emphasis on harmonized standards across regions adds layers of scrutiny, potentially delaying product introductions and limiting agility in responding to market shifts.

Supply Chain Vulnerabilities and Material Sourcing Issues

Disruptions in global supply networks for raw materials such as specialized rubbers and metals can hinder production consistency, exacerbated by geopolitical factors and fluctuating commodity prices. This vulnerability not only affects availability but also raises concerns about quality uniformity, as alternative sourcing may compromise the performance of seals and caps in critical applications.

Opportunity Analysis - Growth in Emerging Healthcare Markets

Regions with rapidly developing infrastructure, such as parts of Asia and Latin America, offer substantial potential for tailored closure solutions that address local needs for affordable yet effective infusion packaging.

As governments invest in expanding access to essential therapies, suppliers can capitalize on partnerships with regional manufacturers to introduce cost-optimized products that meet growing volumes without sacrificing safety features. This avenue promises long-term expansion through localized production strategies that reduce logistics barriers and align with national health initiatives.

Integration of Sustainable and Smart Packaging Features

The push toward eco-conscious materials, including recyclable composites and bio-based alternatives, aligns with global sustainability goals and consumer preferences for environmentally responsible medical supplies.

Coupled with emerging smart technologies such as embedded sensors for real-time integrity monitoring, these innovations can differentiate offerings in a crowded field, appealing to pharmaceutical companies focused on green credentials and enhanced traceability. Opportunities here extend to collaborative R&D efforts that could redefine standards for next-generation closures.

Advancements in Personalized Medicine Delivery

The rise of customized drug formulations is driving the need for adaptive seals and caps capable of handling diverse viscosities and storage conditions, creating niches for specialized solutions in oncology and rare-disease treatments. As precision therapies proliferate, there is room for suppliers to develop modular designs that facilitate small-batch production and rapid customization, thereby supporting the shift toward individualized patient care.

Category-wise Analysis

Product Type Insights

Plastic caps are expected to be the leading segment, capturing 44% of the market share in 2026, owing to their versatility and suitability for high-volume pharmaceutical production. Made primarily from lightweight, moldable materials such as polypropylene, they integrate seamlessly with automated filling and capping lines while maintaining reliable barrier performance.

Polypropylene flip caps are widely used on liquid medication bottles, providing quick, tamper-evident access for nurses during routine infusions. Their dominance is reinforced by the ease of incorporating functional enhancements, such as color-coding, which improve workflow efficiency, support rapid product identification, and reduce preparation errors in busy clinical environments.

Rubber seals are emerging as the fastest-growing segment, driven by the rising use of injectable biologics that require superior sealing to prevent leakage and contamination. Their natural elasticity ensures a secure fit and long-term stability for temperature-sensitive drugs, while advances in non-latex formulations address allergy concerns.

Butyl rubber stoppers, widely used in multi-dose biologic vials, maintain sterility through repeated needle insertions without fragmentation. As drug development shifts toward complex, multi-dose therapies, the need for durable, puncture-resistant seals increases. This momentum also encourages innovation in antimicrobial coatings, positioning rubber seals as key enablers of safer, more reliable infusion systems.

End-user Insights

Hospitals are expected to be the leading segment in 2026, accounting for 37% of the market, leveraging their scale to procure large volumes of seals and caps for routine infusion procedures that form the backbone of inpatient care.

The sheer volume of daily administrations in these institutions underscores the need for closures that endure rigorous handling, with designs prioritizing quick access and minimal waste to align with operational efficiencies in high-stakes environments.

For example, facilities such as Methodist Hospitals use disinfecting caps on IV lines to prevent bacterial contamination during medication delivery, enhancing patient safety in high-throughput settings. This reliance on durable, sterile solutions highlights how hospitals drive bulk demand, while emphasizing protocols for capping tubing ends to prevent air embolism or infection.

Pharmaceutical manufacturers are driving the fastest end-use expansion, propelled by rising biologics production that requires closures engineered for ultra-clean conditions and precise fit tolerances. Advanced therapies demand seals that withstand diverse pressures and chemical interactions while preventing particulate shedding.

As R&D pipelines grow, manufacturers increasingly collaborate on custom solutions, such as silicone-based closures integrated into sterile filling lines. Strategic investment in scalable technologies is accelerating, with specialized rubber seals used in cGMP facilities to ensure compliance during large-scale biologics manufacturing.

This tight link between therapeutic innovation and packaging evolution continues to spur the development of new closure designs tailored to emerging drug modalities.

Regional Insights

North America IV Infusion Bottle Seals & Caps Market Trends

An advanced healthcare infrastructure and a strong emphasis on innovation in drug delivery systems support North America. Significant investments in R&D fuel the adoption of next-generation seals and caps, especially those designed to strengthen contamination control and enhance patient safety.

The U.S. leads the region, benefiting from a mature pharmaceutical ecosystem and stringent regulatory oversight that encourages the integration of cutting-edge technologies, even as cost containment in public health programs moderates growth. Rising rates of chronic diseases and the expansion of home-based care models further elevate demand for portable, high-integrity packaging solutions.

The region’s regulatory environment, focused on material purity, traceability, and sterility, drives both high standards and continual advancements, including automated validation processes. Competitive dynamics favor established manufacturers with vertically integrated operations that ensure quality from raw materials through final assembly.

Partnerships with device makers are increasingly common as providers seek comprehensive system solutions. Investment activity is concentrated in biotech hubs, with growing interest in sustainable, latex-free materials aligned with evolving environmental and clinical priorities. Additional opportunities remain in underserved ambulatory and home-care segments, where customized closures can improve therapy management and support deeper market penetration.

Europe IV Infusion Bottle Seals & Caps Market Trends

Europe’s market is shaped by strong regional collaboration and standardized regulatory frameworks that support smooth cross-border trade while accommodating diverse national healthcare priorities.

Germany serves as a central innovation hub, leveraging its engineering expertise to produce precision-engineered caps suitable for stringent biologics requirements. The U.K. focuses on NHS-driven efficiencies, while France integrates advanced closure solutions into its growing nutraceutical sector. Spain adds value through cost-efficient manufacturing that supports wider EU distribution networks.

Growth is driven by harmonized directives that promote patient-centric design and by demographic pressures from an aging population, which increase demand for dependable infusion safeguards. The Medical Device Regulation further unifies approval pathways while introducing sustainability mandates that accelerate industry shifts toward recyclable and low-impact components.

Competition features both multinational leaders and specialized firms offering modular product lines adaptable to various therapies. Investments continue flowing into green technologies, reflecting EU incentives for low-carbon production.

A notable development is the establishment of a new facility dedicated to advanced tamper-evident solutions, strengthening regional supply security. Together, these factors position Europe for steady, meaningful growth, with significant opportunities emerging in Eastern markets seeking affordable, compliant closure variants.

Asia Pacific IV Infusion Bottle Seals & Caps Market Trends

Asia Pacific is expected to dominate, hold 36% of the market share in 2026, propelled by demographic scales and infrastructural leaps that are redefining access to infusion therapies across urban and rural divides. Asia Pacific is also the fastest-growing region.

China leads with its vast manufacturing base and policy-driven healthcare reforms, enabling rapid scaling of closure production for domestic and export needs. At the same time, Japan excels in high-tech integrations such as electron-beam sterilized seals.

India's generic drug sector and ASEAN's collective investments in public health further amplify regional momentum, creating synergies in supply chain localization. Core drivers involve population-driven chronic care escalations and manufacturing cost advantages that attract global partnerships, fostering innovations in affordable, durable packaging suited to diverse climates.

Regulatory environments vary, with China's alignment with international norms accelerating imports and India's evolving standards easing market entry, though intellectual property safeguards remain a focus area. The competitive field is consolidating around efficiency-focused entities, with expansions into smart features differentiating leaders.

Investment surges target digital-enabled facilities, highlighting opportunities in home infusion booms. A key development is a joint venture that enhances elastomer capabilities, poised to capture rising ambulatory demand and solidify Asia Pacific's role as a global pivot.

Competitive Landscape

The global IV infusion bottle seals & caps market is moderately concentrated, with a handful of influential entities shaping strategic direction through their scale and expertise in specialized components.

Leading firms collectively influence a majority of transactions, leveraging established reputations for reliability to maintain loyalty among pharmaceutical partners. This setup, blending consolidation at the top with niche innovators below, strikes a balance between stability and creativity, though it requires vigilant adaptation to regulatory evolution.

Prominent approaches revolve around continuous refinement of core technologies and broadening geographic reach through alliances. Leaders distinguish themselves via tailored compliance expertise and eco-integrated designs, while nascent models emphasize data-driven customization for precision therapies.

Key Industry Developments

- In February 2025, Becton Dickinson and Company (BD) announced the acquisition of Scapa Group plc's IV closure unit, bolstering its sterile packaging capabilities and expanding its global bottle-seal manufacturing footprint.

- In May 2025, ICU Medical, Inc. and Otsuka Pharmaceutical Factory, Inc. completed a joint venture named Otsuka ICU Medical LLC, creating one of the largest global IV solutions manufacturing networks with an estimated 1.4 billion annual units to strengthen supply chain resiliency and drive innovation in North America.

Companies Covered in IV Infusion Bottle Seals & Caps Market

- B. Braun Melsungen AG

- West Pharmaceutical Services, Inc.

- Baxter International Inc.

- Nipro Corporation

- Gerresheimer AG

- Aptar Pharma (AptarGroup, Inc.)

- Daikyo Seiko Ltd.

- Datwyler Holding Inc.

- Ompi (Stevanato Group)

- SCHOTT AG

- Medtronic plc

- Fresenius Kabi AG

- SGD Pharma SAS

- Berry Global, Inc.

- Amcor PLC

- CCL Industries Inc.

- Prasad Meditech

- Medline Industries Inc.

- Wuxi Qitian Medical Technology Co., Ltd.

- Jiangsu Best New Medical Material Co., Ltd.

Frequently Asked Questions

The IV infusion bottle seals & caps market size is estimated to reach US$1.14 million in 2026.

By 2033, the IV infusion bottle seals & caps market value is projected to reach US$1.78 million.

Key market trends include increasing adoption of high-barrier flip-off seals, strong shift toward polymer-based and aluminum-polymer hybrid closures, and expansion of ready-to-fill (RTF) IV container systems.

Aluminum seals remain the leading product type due to their robust tamper-evidence, compatibility with glass IV bottles, and widespread adoption across hospital and clinical infusion lines.

The IV infusion bottle seals & caps market is projected to grow at a CAGR of 6.7% between 2026 and 2033.

Major companies include West Pharmaceutical Services, Datwyler Holding, SGD Pharma, Nipro Corporation, and Stevanato Group.