- Non-food Packaging

- Plastic Caps and Closure Market

Plastic Caps and Closure Market Size, Share, and Growth Forecast, 2025 - 2032

Plastic Caps and Closure Market by Closure Type (Screw Caps, Flip-Top Caps, Dispensing Caps, Child-Resistant Caps, Tamper-Evident Caps, and Misc.), Material Type (Polypropylene (PP), High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), and Others (Polystyrene, Bio-based Plastics) Industry, and Regional Analysis for 2025 - 2032

Plastic Caps and Closure Market Size and Trends Analysis

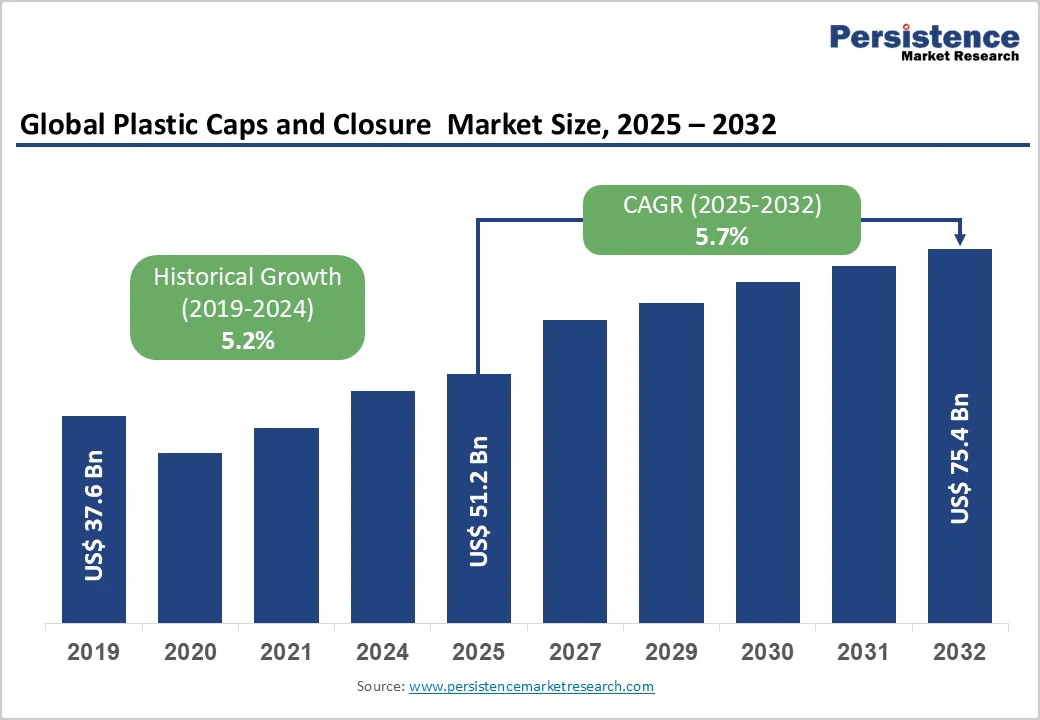

The global plastic caps and closure market size is likely to value at US$51.2 billion in 2025 and is projected to reach US$75.4 billion, growing at a CAGR of 5.7% between 2025 and 2032.

This market expansion is driven by escalating consumer demand for food and beverage products, stringent regulatory mandates for product safety and sustainability, and rapid technological advancements in material science and manufacturing processes.

Key Industry Highlights:

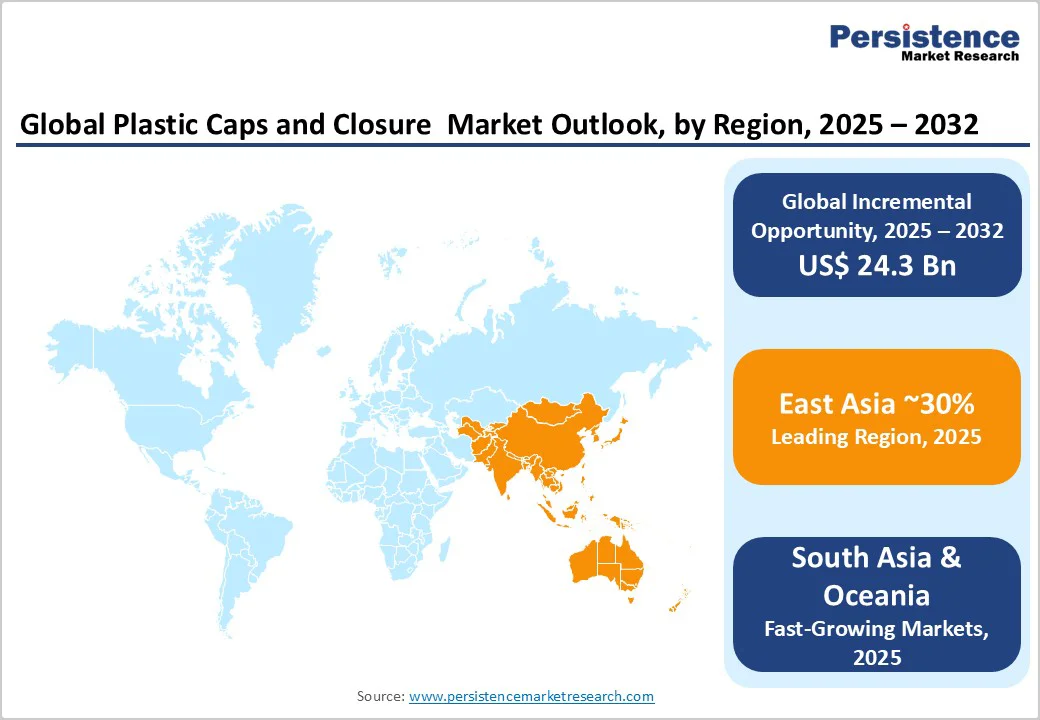

- East Asia dominates the global plastic caps and closure market with a 30% value share, driven by high beverage and pharmaceutical production in China and expanding consumer goods industries in Japan and South Korea.

- Europe holds a 24% market share, leading regulatory compliance through the EU PPWR and tethered-cap mandates, which are driving large-scale material innovation and equipment retrofits across manufacturers.

- North America represents 21% of global market value, led by the U.S. beverage and pharmaceutical sectors, with beverage closures growing at 6-7% CAGR due to demand for functional drinks and sustainability upgrades.

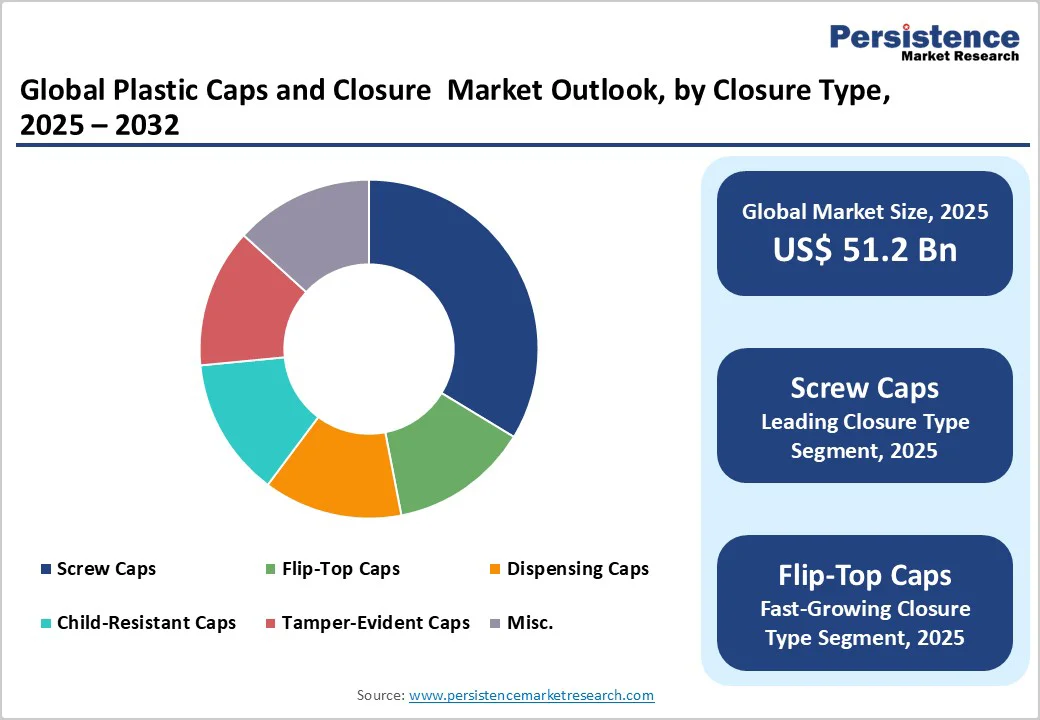

- Screw caps command the largest share at 43% of global volumes, supported by their widespread compatibility with beverage, dairy, and pharmaceutical packaging lines.

- Flip-top caps are the fastest-growing closure type, driven by rising demand for convenience packaging in personal care and cosmetics applications.

- Polypropylene (PP) remains the leading material, accounting for 47.8% of global share, favoured for its chemical resistance, thermal stability, and suitability for high-speed injection moulding.

- The food and beverage industry accounts for 66% of total market demand, underpinned by high consumption in bottled water, dairy, and ready-to-drink categories across Asia and North America.

| Key Insights | Details |

|---|---|

| Plastic Caps and Closure Market Size (2025E) | US$ 51.2 Bn |

| Market Value Forecast (2032F) | US$ 75.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

Market Dynamics

Drivers - Surging Consumption in Food and Beverage Manufacturing

The food and beverage manufacturing sector represents the dominant end-use application for plastic caps and closures, commanding 66% of the Global Plastic Caps and Closure Market in 2025.

According to U.S. Department of Commerce data, the American food and beverage manufacturing industry generated 16.8% of total manufacturing sales in 2021, employing 1.7 million workers. Meat processing alone contributed 26.2% of sectoral sales, while dairy, beverages, grain, and oilseeds collectively accounted for over 70% of total industry revenue.

In India, the food processing sector, valued at US$354.5 billion in 2024 is projected to reach US$535 billion by FY26, driven by urbanisation and government initiatives including the Production Linked Incentive Scheme for Food Processing Industry (PLISFPI) and Pradhan Mantri Kisan Sampada Yojana (PMKSY).

This expansion directly correlates with heightened demand for reliable closure systems in the Global Plastic Caps and Closure Market, as manufacturers require tamper-evidence, extended shelf-life solutions, and contamination prevention mechanisms. The sector's growth trajectory supports sustained demand for polypropylene and polyethylene-based closures adapted for carbonated beverages, dairy products, and ready-to-drink formats.

Regulatory Mandates Accelerating Product Safety and Sustainability Standards

Regulatory frameworks globally are fundamentally reshaping closure design and material specifications within the Global Plastic Caps and Closure Market. The European Union's Packaging and Packaging Waste Regulation (PPWR), effective January 1, 2030, mandates that all packaging achieve recyclability standards, with recycled content targets of 30% for PET contact packaging by 2030 and 65% by 2040.

The directive's requirement that beverage container caps remain tethered to bottles, effective July 3, 2024, necessitated widespread equipment retrofits, impacting manufacturing capacity and investment cycles. In North America, the FDA's child-resistant closure mandates for over 65% of prescriptions underscore pharmaceutical compliance requirements, directly driving demand for specialised closure types.

The U.S. Consumer Product Safety Commission's 16 CFR §1700.20 standard requires child-resistant packaging to remain unopened by at least 80% of children aged 42-51 months, creating engineering specifications that differentiate closure products and support market premiumization.

Extended Producer Responsibility (EPR) fee structures, phased across Europe and North America, incentivise manufacturers to adopt recyclable materials, with fees adjusted based on packaging recycling grades (A-C). These regulatory drivers create structural demand tailwinds for the Global Plastic Caps and Closure Market, as compliance investment cycles sustain capital expenditure and innovation spending.

Technological Innovation in Material Science and Manufacturing Processes

Material science advancements are enabling manufacturers to engineer closures with enhanced barrier properties, lightweighting capabilities, and sustainability credentials. Polyethylene (PE) represents the leading material choice globally due to its exceptional versatility, chemical resistance, and lightweight properties.

Post-mould tamper-evident (TE) band technology is expanding at a robust 6-8% CAGR through the forecast period, driven by flexibility in design integration and superior manufacturing economics compared to pre-mould alternatives. Injection moulding technology, accounting for 63.98% of European production volumes, continues to dominate through micron-level tolerance precision and multi-cavity throughput optimisation.

Compression moulding is recording around 4-6% CAGR as tethered-cap geometries benefit from superior thickness uniformity and material economy critical for meeting PPWR weight-minimisation mandates.

AI-enabled inline vision inspection systems are reducing scrap rates and widening profit margins across facilities in technologically advanced markets. The Global Plastic Caps and Closure Market benefits from these innovations through faster product development cycles, improved cost structures, and enhanced compliance with increasingly stringent regulatory specifications.

Restraints - Supply Chain Volatility and Raw Material Cost Pressures

Raw material pricing volatility, particularly for polypropylene and polyethylene resins, creates structural cost challenges that constrain margin expansion within the Global Plastic Caps and Closure Market.

Petroleum feedstock price fluctuations directly translate into production cost variability, with limited pricing power to end-customers during periods of elevated commodity costs. Chemical recycling infrastructure limitations constrain food-grade recycled polyethylene terephthalate (rPET) and recycled high-density polyethylene (rHDPE) availability across Europe, raising material procurement costs and restricting manufacturers' ability to meet PPWR recycled content targets cost-effectively.

Supply chain disruptions, particularly in Asia Pacific regions, are critical for raw material sourcing, delay closure deliveries, and force inventory adjustments among converters. Logistics costs remain elevated relative to historical averages, impacting supply chain economics, particularly for manufacturers serving geographically dispersed markets across North America, Europe, and Asia Pacific.

Opportunity

Smart Packaging Integration and Digital-Enabled Closure Solutions

Technological convergence between packaging and digital tracking technologies presents differentiation opportunities within the Global Plastic Caps and Closure Market. Integration of RFID tags, NFC chips, QR codes, and IoT sensors into closure designs enables brand owners to implement product authentication, traceability, and anti-counterfeiting features critical for pharmaceutical and premium beverage segments.

Coca-Cola's implementation of QR code-enabled bottle caps demonstrates commercial viability, with integrated code scanning providing consumers access to promotional content, digital coupons, and brand engagement platforms, thereby strengthening consumer loyalty and generating valuable first-party data for brand owners.

Supply chain transparency enabled through closure-embedded tracking technologies facilitates inventory management optimization, product recall efficiency, and compliance documentation, particularly valuable in regulated pharmaceutical and healthcare markets subject to strict serialization and falsified-medicine directives.

The integration of smart features commands pricing premiums of 15-25%, supporting margin expansion opportunities within the Global Plastic Caps and Closure Market for manufacturers investing in digital closure capabilities and software integration platforms.

Sustainability-Driven Portfolio Premiumization and Circular Economy Solutions

Consumer preference for sustainable packaging, coupled with regulatory mandates, is driving portfolio migration toward bio-based plastics, post-consumer recycled (PCR) content formulations, and mono-material closure designs compatible with existing recycling infrastructure.

Brands are demonstrating willingness to absorb cost premiums of 10-20% for closures incorporating 50% plus PCR content or bio-based materials, reflecting corporate sustainability commitments and consumer purchasing behaviour shifts. The Global Plastic Caps and Closures

Market benefits from this premiumization trend through the realisation of improved margins on sustainable product variants while simultaneously gaining competitive protection through regulatory compliance leadership. Development of proprietary lightweighting technologies enabling 10-15% material reduction per closure unit creates simultaneous cost and environmental benefits, supporting corporate carbon-reduction targets while preserving structural functionality.

Participation in brand-owner sustainability roadmaps, such as consumer goods companies' commitments to achieve net-zero packaging by 2040, creates long-term customer partnerships supporting durable market share protection within the Global Plastic Caps and Closure Market.

Sustainability Leadership Through Circular Economy and Recycling Innovation

The integration of recycled copper and closed-loop manufacturing offers a significant strategic opportunity for the Plastic Caps and Closure Market to strengthen sustainability leadership.

Furukawa Electric, validated under UL 2809, produces electrolytic copper foil with 100% recycled copper, substantially reducing CO2 emissions compared to virgin copper by leveraging lower energy consumption in recycling.

JX Nippon Mining & Metals has launched 100% recycled copper products and innovative mass balance schemes ensuring traceability and circularity. The direct use of scrap is gaining traction outside China, mitigating exposure to volatile copper prices.

Battery recycling capacity, projected to reach 1,500 GWh by 2030, will supply secondary copper, promoting circular economy models. Renewable energy integration in production, greener chemical use, and water recycling enhance environmental profiles and compliance with tightening European and North American regulations.

Category-wise Analysis

Closure Type Insights

Screw caps maintain the largest share, commanding 43.0% of volumes due to universal compatibility across existing beverage and pharmaceutical manufacturing infrastructure. The closure type's dominance reflects standardised International Organisation for Standardization (ISO) neck finishes, high-speed production line compatibility, and proven tamper-evident capabilities through tamper-band integration.

In European markets, screw caps retain 47.81% volumetric market share while recording only modest share erosion as specialised closure formats proliferate. Polypropylene-based screw caps dominate the functional beverage and nutraceutical segments, where cost-effectiveness and chemical resistance against acidic and carbonated contents drive specification decisions.

Cross-industry application across food and beverage, household chemicals, and industrial fluids supports high-volume production runs and economies of scale that sustain competitive pricing despite raw material inflation. Screw cap applications extend into pharmaceutical vials, dairy products, and condiment packaging, where customized designs incorporating integral living hinges, multi-start threads, and precision-engineered caps command pricing premiums of 8-12% above standard commodity configurations.

Flip-top caps represent the fastest-growing segment in 2025. The closure type's expansion reflects consumer preferences for convenience, one-handed dispensing capability, and perceived premium positioning across personal care and cosmetics markets. Flip-top cap applications in shampoos, body washes, lotions, and sunscreens demonstrate superior functional benefits, enabling rapid product access, minimising spillage, and reducing contamination risk through hinged closure designs that maintain hygiene.

Material Type Insights

Polypropylene dominates material selection within the Global Plastic Caps and Closure Market, commanding 47.8% market share in 2025 due to superior chemical resistance, fatigue strength, and heat tolerance characteristics.

The material's versatility supports applications across carbonated beverages, food products requiring high-temperature fill processes, and pharmaceutical formulations sensitive to reactive or specialised active pharmaceutical ingredients. Polypropylene's exceptional resistance to boiling water and organic solvents, combined with its ability to withstand thermal shock and maintain structural integrity across -20°C to +80°C operational ranges, positions the material as the preferred choice for comprehensive application portfolios.

Manufacturing economics favour polypropylene through established supply contracts, commodity pricing transparency, and injection-moulding process optimisation achieving cycle times of 8-12 seconds per part, supporting high-volume production competitiveness.

Polyethylene terephthalate represents the fastest-growing material segment within the Global Plastic Caps and Closure Market, expanding at 4.39% CAGR in European markets and demonstrating equivalent growth trajectories across North America and Asia Pacific. PET's lightweight characteristics, enabling 20-30% weight reduction compared to polypropylene for equivalent structural performance, directly align with PPWR minimisation mandates and corporate carbon reduction initiatives.

Industry Insights

Food and beverage applications represent the dominant end-use category within the Global Plastic Caps and Closure Market, commanding 66% market share in 2025 due to high-volume consumption patterns, stringent safety specifications, and continuous packaging innovation requirements.

Beverages, including carbonated soft drinks, juices, water, and ready-to-drink products, represent the largest subcategory, accounting for approximately 41.24% of European closure demand and demonstrating equivalent proportional dominance in North American and Asia Pacific markets.

The beverage industry's adoption of plastic caps reflects standardised PCO (pressure-closure only) neck finishes, high-speed filling line compatibility up to 2,000 caps per minute on rotary fillers, and tamper-evidence requirements mandated through food safety regulations and brand protection standards.

Cosmetics and personal care applications represent the fastest-growing end-use segment sector's growth trajectory reflects expanding consumer spending on premium skincare, specialized formulations targeting demographic segments, anti-ageing, acne-prone, sensitive skin, and brand owner investments in experiential packaging supporting unboxing engagement and social media amplification.

Regional Insights and Trends

East Asia Plastic Caps and Closure Market Trends

East Asia commands 30% of the global Plastic Caps and Closure Market value, representing the dominant regional market driven by China's 31.2% Asia Pacific market share and India's 19.2% participation.

China dominates regional markets through the scale of bottled water and carbonated beverage production concentrated in Guangdong, Zhejiang, and Sichuan provinces, coupled with robust pharmaceutical and cosmetic export industries.

Government-backed modernisation initiatives under the Made in China 2025 framework emphasize automation and quality control in manufacturing, establishing competitive advantages in precision closure production. China's beverage industry production volumes exceed 200 million units annually, establishing systemic closure demand unmatched across competing regional markets.

Japan's plastic caps and closures market emphasises precision-engineered, high-value closure systems tailored for premium food, beverage, and pharmaceutical applications, reflecting consumer preferences for ergonomic, specialty formats.

Japanese beverage exports to North America and Europe increased 14% in 2023, frequently featuring proprietary closure designs developed by domestic packaging firms, establishing competitive differentiation within premium market segments.

South Korea's well-developed consumer goods industry, expanding e-commerce adoption, and increasing demand for functional packaging solutions position the nation as a secondary growth market within East Asia, with an estimated market value approaching USD 4-5 billion.

Europe Plastic Caps and Closure Market Trends

Europe represents 24% of the global market value, characterised by mature market dynamics, sophisticated regulatory frameworks, and emphasis on sustainability-driven innovation.

Germany retained 16.51% regional share in 2024, leveraging a sophisticated industrial base and early Deposit Return Scheme adoption, promoting a high recycled-content closure uptake. German manufacturing capabilities concentrate on automotive fluid closures, pharmaceutical packaging, and plant-based dairy segments, reflecting specialized production expertise.

France and Italy collectively command significant volume through wine, spirits, and luxury cosmetics exports, dependent upon premium tamper-evident and decorative closures, establishing distinct market positioning separate from commodity beverage segments.

The European Union's Plastic Packaging with Recycling Directive (PPWR), effective February 2025, requires 30% recycled-content beverage bottles by 2030 and 65% by 2040, fundamentally restructuring material procurement and production processes. Tethered-cap mandates effective July 2024 compel manufacturers to redesign existing products, creating substantial retrofit capital requirements exceeding USD 100 million for multinational operators.

North America Plastic Caps and Closure Market Trends

North America represents 21% of the global market value, demonstrating moderate growth at 3.2% CAGR through 2030 as mature market dynamics and established production infrastructure characterize regional market structure. The United States dominates regional consumption.

Beverage applications command around 35-40%% regional market share with the fastest-growing trajectory at 6% to 7% CAGR, reflecting rising consumption of enhanced waters, relaxation mocktails, and caffeinated sports drinks penetrating retail channels. Polypropylene material dominance reflects cost-effectiveness and established supply infrastructure, generating competitive advantages resistant to substitution pressures from alternative polymers.

Competitive Landscape

The global plastic caps and closures market is moderately consolidated, characterised by the presence of a few dominant multinational companies alongside a large number of regional manufacturers catering to niche applications.

Leading players such as Berry Global Group, Silgan Holdings, AptarGroup, Amcor, BERICAP, and Crown Holdings collectively account for a significant share of global production and innovation activity, leveraging extensive distribution networks and advanced manufacturing capabilities.

These companies focus on sustainability-driven product innovation, lightweight designs, and tethered cap solutions to comply with evolving environmental regulations. Regional participants such as O. Berk Company, United Caps, and Coral Products compete through customisation and cost-effective production, maintaining competitive diversity within the market.

Key Industry Developments

- In September, 2025, Amcor introduced a new portfolio of tethered and sports closures designed for PET and glass beverage bottles, aligning with EU tethered-cap regulations and global sustainability goals. The company’s latest flat cap and lightweight closure innovations enhance recyclability and material efficiency while supporting refillable and returnable packaging systems. These closures, compliant with circular packaging requirements, strengthen Amcor’s position in the beverage segment of the global plastic caps and closures market.

- In September 2024, Berry Global introduced the Pical Pouring Closure, a tamper-evident, fully recyclable closure designed for edible oils, dressings, and sauces. Made from mono-material HDPE, the one-piece flip-top design enhances consumer convenience through easy one-handed operation and smooth product dispensing. The closure aligns with EU single-use plastic regulations and promotes circularity by ensuring all components remain within the recycling stream.

Companies Covered in Plastic Caps and Closure Market

- Berry Global Group

- Crown Holding

- AptarGroup

- Amcor

- Coral Products

- BERICAP

- Silgan Holdings

- O Berk Company

- Closures

- United Caps

- Caps & Closures Pty Ltd

- Caprite Australia Pty Ltd

- Pano Cap Limited

- Plastic Closures Ltd

- Cap & Seal Pvt Ltd

- Alpac

- Hicap Closures

- MJS Packaging

Frequently Asked Questions

The global Plastic Caps and Closure Market is projected to be valued at US$ 51.2 Bn in 2025.

The Screw Caps segment is expected to hold around 43.0% market share by Closure Type in 2025, driven by universal compatibility, tamper-evident design, and widespread use across beverage and pharmaceutical applications.

The Plastic Caps and Closure Market is expected to witness a CAGR of 5.7% from 2025 to 2032.

The Plastic Caps and Closure Market growth is driven by rising demand from the food and beverage sector, regulatory compliance for safety and sustainability, and advancements in material science and manufacturing technologies.

Key market opportunities in the Global Plastic Caps and Closure Market include smart packaging integration, digital-enabled closure solutions, and sustainability-driven product portfolio premiumization.

The leading global players in the Plastic Caps and Closure Market are Berry Global Group, Silgan Holdings, AptarGroup, Amcor, BERICAP, and Crown Holdings.