- Non-food Packaging

- Tablets and Capsules Packaging Market

Tablets and Capsules Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Tablets and Capsules Packaging Market by Packaging Type (Blister Packs, Strip Packs, Others), Material Type (Plastic, Aluminum Foil, Others), Product Type, End-user, and Regional Analysis for 2026 - 2033

Tablets and Capsules Packaging Market Size and Trends Analysis

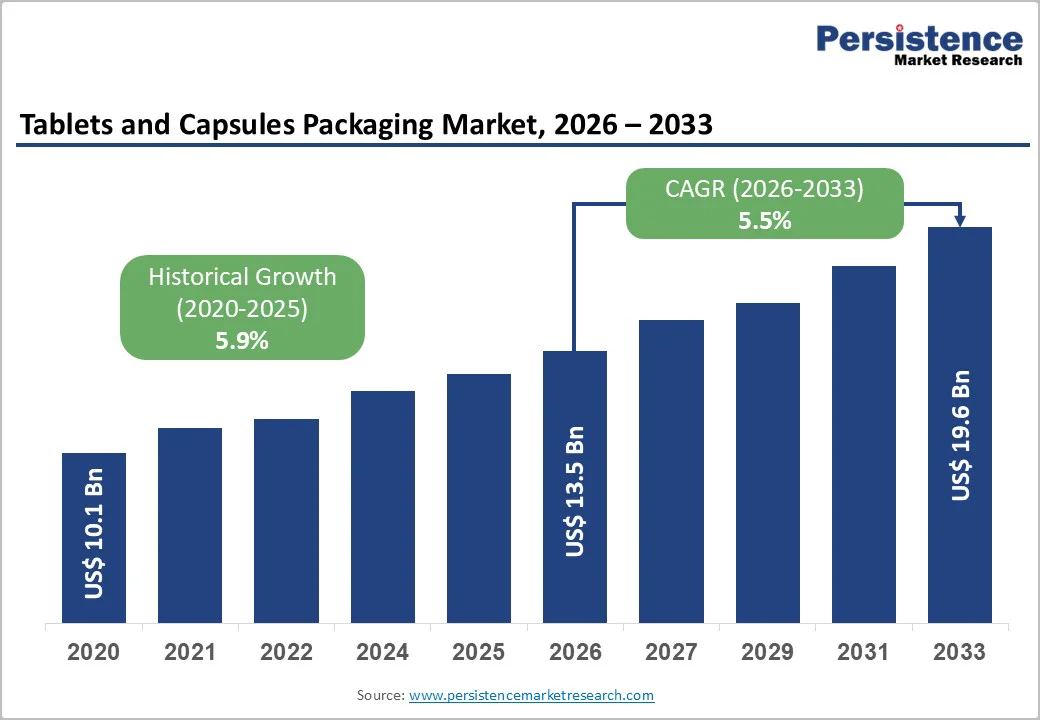

The global tablets and capsules packaging market size is likely to be valued at US$13.5 billion in 2026 and is expected to reach US$19.6 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, driven by steady growth in pharmaceutical and nutraceutical production, rising per-capita medicine consumption among aging populations, and increasing adoption of unit-dose and patient-centric packaging formats.

Blister packs and plastic-based primary packaging will remain dominant, supported by large-volume prescription demand, while higher-barrier aluminum and specialty polymer solutions are gaining traction for controlled-release and moisture-sensitive formulations.

Key Industry Highlights

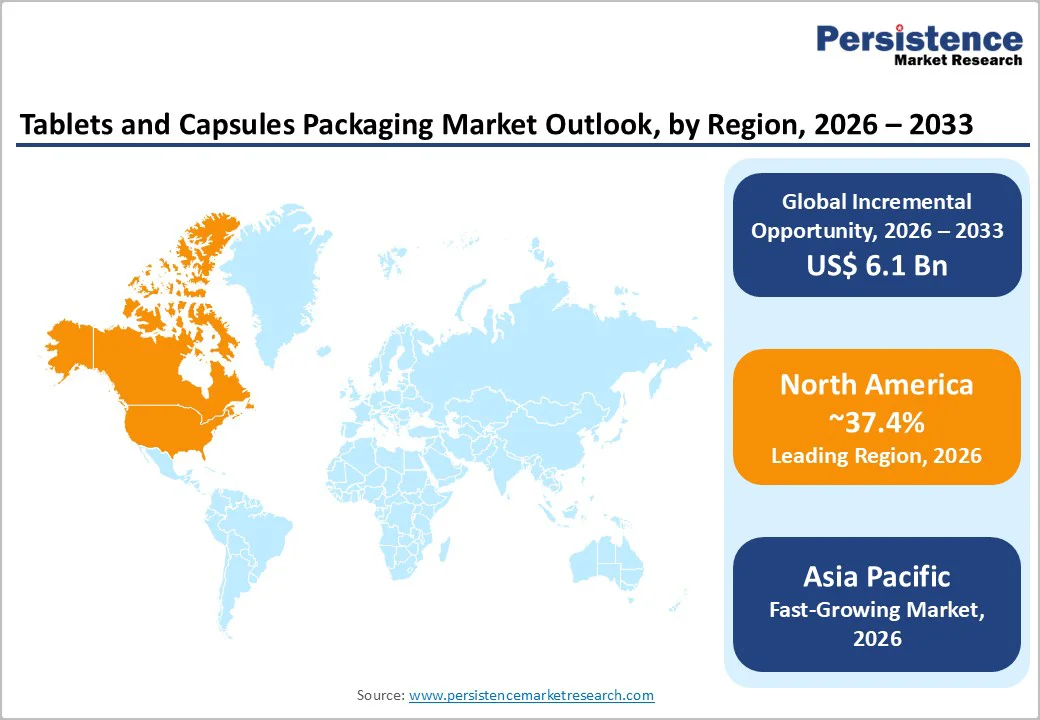

- Leading Region: North America is projected to account for approximately 37.4% of global market demand, supported by high prescription drug volumes, strong OTC penetration, and stringent regulatory requirements such as the U.S. Drug Supply Chain Security Act (DSCSA), which continue to favor advanced, compliant packaging solutions.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing regional market, driven by rapid pharmaceutical manufacturing expansion in China, India, and ASEAN, rising healthcare access, and increasing export-oriented production.

- Investment Plans: Capital investments are focused on automation, serialization, and sustainable materials, with packaging converters in North America and Europe expanding high-speed blister lines, digital track-and-trace systems, and recyclable packaging structures, while Asia Pacific sees continued investment in local conversion capacity and compliance upgrades.

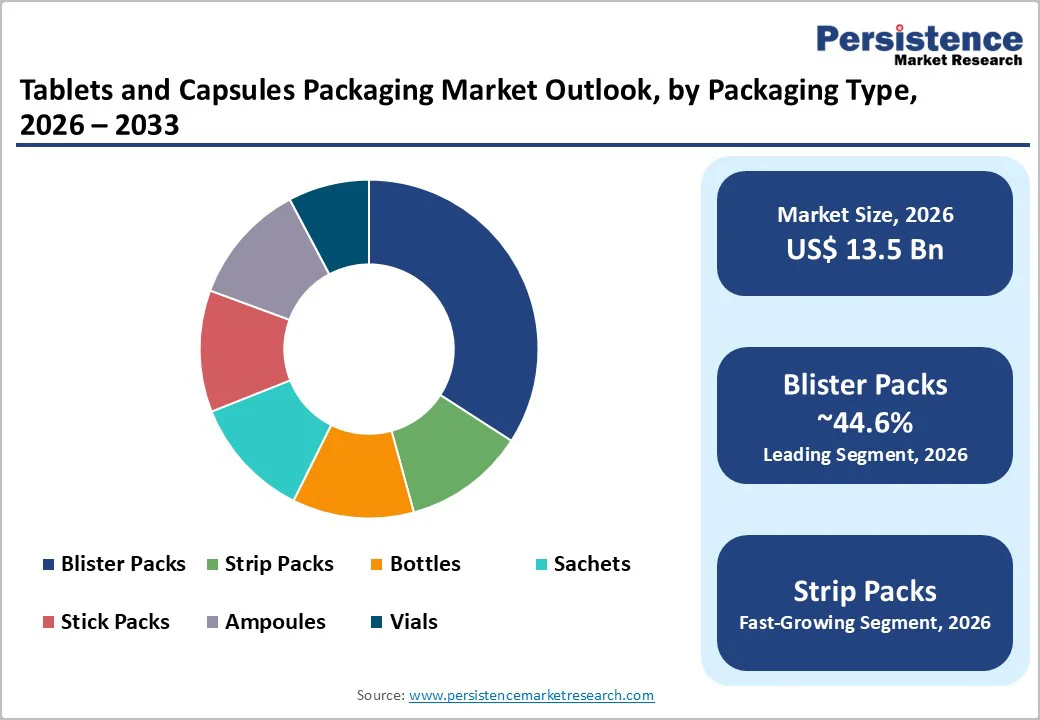

- Dominant Packaging Type: Blister packs are projected to dominate the market, accounting for approximately 44.6% of the total packaging demand, driven by unit-dose protection, patient adherence benefits, regulatory compliance, and widespread use across prescription, OTC, and hospital dispensing channels.

- Leading Material Type: Plastic materials are estimated to lead the market with around 42.3% share, supported by cost efficiency, lightweight properties, and compatibility with high-speed pharmaceutical packaging operations, particularly for blister cavities and rigid bottles used in high-volume drug production.

| Key Insights | Details |

|---|---|

| Tablets and Capsules Packaging Market Size (2026E) | US$13.5 Bn |

| Market Value Forecast (2033F) | US$19.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Aging Populations and Chronic Disease Prevalence

Global demographic shifts are materially increasing per-capita pharmaceutical consumption. The rising incidence of chronic conditions such as cardiovascular diseases, diabetes, respiratory disorders, and neurodegenerative illnesses has resulted in sustained growth in long-term medication regimens. These therapies rely heavily on tablets and capsules as the preferred oral dosage forms due to ease of administration and cost efficiency. As prescription volumes rise, demand for reliable, compliant, and scalable packaging solutions grows proportionally. Packaging demand also increases as manufacturers transition from bulk packaging toward unit-dose formats that improve adherence and safety. This demographic-driven demand supports a sustained mid-single-digit growth trajectory for tablets and capsules packaging across developed and emerging markets.

Shift toward Patient-Centric and Adherence-Focused Packaging

Regulatory bodies and healthcare systems are increasingly emphasizing medication safety, traceability, and patient adherence. This has accelerated the adoption of unit-dose blister packaging, child-resistant closures, calendar packs, and packaging formats with visual dosing cues. Compared to loose bottles, these formats increase value per packaged unit and require more advanced materials and tooling. The growing use of tamper-evident features, smart labeling, and track-and-trace compatibility further enhances packaging complexity and pricing. Compliance-enhancing packaging supports higher average selling prices and improves margins, particularly for specialized converters that meet regulatory and sustainability expectations.

Barrier Analysis - Material Cost Volatility and Supply-Chain Constraints

Volatility in the prices of key raw materials, such as resins, aluminum foil, and specialty polymers, poses a structural challenge for packaging manufacturers. Tight supply of pharmaceutical-grade inputs, including cyclic olefin polymers and high-quality glass, can lead to production delays and margin pressure. A 10-15% fluctuation in polymer feedstock prices can translate into a 3-7% increase in finished packaging costs, depending on product design and barrier requirements. Smaller manufacturers with limited purchasing power face heightened risk, while larger, vertically integrated suppliers are better positioned to absorb cost fluctuations through long-term supply agreements and diversified sourcing.

Regulatory and Qualification Burden for Drug-Contact Materials

Packaging used for tablets and capsules must meet stringent regulatory requirements related to extractables and leachables, material compatibility, serialization, and data integrity. Compliance with international standards increases development timelines and raises validation costs. For new polymer systems or innovative blister formats, extractables and leachables testing programs can extend development cycles by 6-12 months and significantly increase upfront R&D expenditure. These barriers disproportionately affect smaller converters and raise entry thresholds, reinforcing market concentration around established suppliers with regulatory expertise and validation infrastructure.

Opportunity Analysis - Sustainable and Recyclable Blister Packaging Solutions

Growing regulatory and customer pressure to reduce packaging waste and lifecycle emissions is creating strong demand for recyclable, mono-material, and reduced-plastic blister systems. Sustainable blister retrofits and recyclable thermoformed solutions offer a clear differentiation opportunity, particularly among large pharmaceutical companies with public sustainability targets. If sustainable blister solutions capture even a modest share of total blister demand by the end of the decade, they could represent a high-value revenue segment within tablets and capsules packaging. Suppliers that invest early in recyclable materials and validated sustainable designs gain a competitive advantage and long-term customer alignment.

Emerging Markets and Localized Manufacturing Expansion

Emerging regions, including the Asia Pacific, Latin America, and parts of Eastern Europe, are experiencing faster growth in pharmaceutical production and medicine consumption. Governments are expanding access to healthcare, while local manufacturers are increasing finished-dosage output. Establishing localized packaging operations, such as onshore blistering and bottle filling, reduces dependence on imports and shortens lead times. Redirecting a portion of imported packaging demand to local suppliers can unlock meaningful incremental revenue over the medium term. Packaging companies that combine regulatory-grade quality with regional cost efficiency are well-positioned to capture this growth.

Category-wise Analysis

Packaging Type Analysis

Blister packs are anticipated to account for approximately 44.6% of the market, making them the dominant packaging type across prescription, OTC, and institutional healthcare channels. Their leadership is driven by superior unit-dose protection, clear product visibility, and strong compatibility with adherence-focused designs. Blister packs enable precise dose separation, reducing medication errors and improving patient compliance, particularly for chronic therapies and elderly populations. Pharmaceutical manufacturers favor blister packs for their ability to incorporate child-resistant mechanisms, tamper-evident features, and anti-counterfeiting elements, all of which are increasingly required by regulators and healthcare providers.

Calendar blisters and printed aluminum foils allow dosing instructions, branding, and regulatory information to be integrated directly into the primary package, enhancing both safety and patient engagement. Blister packs support high-speed, automated production lines, making them cost-efficient at scale for both branded drugs and large-volume generics. They are widely used for cardiovascular, CNS, and gastrointestinal medications, as well as OTC analgesics and supplements sold through retail pharmacies. Their versatility across therapeutic categories and distribution channels continues to reinforce their leading position in the market.

Strip packs are likely to be the fastest-growing packaging format within the tablets and capsules packaging market, driven by rising demand for moisture-sensitive and high-stability formulations. Cold-form aluminum strip packs provide near-total barrier protection against moisture, oxygen, and light, making them particularly suitable for hygroscopic, effervescent, and enteric-coated tablets that are highly sensitive to environmental exposure.

Unlike conventional blisters, strip packs individually seal each dose, ensuring maximum product integrity throughout the shelf life. This characteristic is increasingly important for specialty generics, export-oriented pharmaceuticals, and products distributed in regions with high humidity or limited cold-chain infrastructure. Strip packs are commonly used for antibiotics, proton pump inhibitors, and vitamin-mineral combinations where stability is critical. Although bottles remain dominant for high-volume generics and nutraceuticals, strip packs are steadily gaining share in regulated and export markets where product quality assurance outweighs cost considerations. Growth is further supported by stricter regulatory scrutiny of product degradation and an increasing focus on dose accuracy and patient safety.

Material Type Analysis

Plastic materials are anticipated to lead, accounting for an estimated 42.3% share in 2026. Cost efficiency, lightweight properties, design flexibility, and ease of processing across high-speed pharmaceutical packaging lines drive their dominance. Thermoformed plastics such as PET, PVC, and PVdC-coated films, as well as advanced polymer blends, are widely used in blister cavities, while HDPE and PET are standard materials for bottles. Plastic packaging supports a broad range of pharmaceutical applications, from mass-market generics to OTC products, where affordability and production scalability are critical. These materials are resistant to breakage, enhance patient safety during handling, and allow integration of child-resistant closures and tamper-evident features.

Plastics enable transparent or semi-transparent designs, which are preferred in retail settings for product visibility. From a manufacturing standpoint, plastic materials are compatible with high-speed forming, filling, and sealing operations, making them ideal for large-volume pharmaceutical production. Their widespread availability and established regulatory acceptance further reinforce their leading position, particularly in mature markets with strong generic drug penetration.

Aluminum foil is likely to be the fastest-growing material segment in tablet and capsule packaging due to increasing demand for high-barrier and extended shelf-life solutions. Cold-form aluminum foil blisters provide superior protection against moisture, oxygen, and light, offering the highest barrier performance among commonly used packaging materials. This material is increasingly adopted for controlled-release tablets, specialty generics, and complex oral formulations that are sensitive to environmental degradation.

Aluminum foil packaging is especially prevalent in therapeutic areas such as gastroenterology, anti-infectives, and hormonal therapies, where stability and potency must be maintained over long storage periods. Despite higher material and processing costs than plastics, demand for aluminum foil continues to rise as pharmaceutical formulations become more complex and regulatory expectations for product integrity tighten. Its ability to ensure consistent quality throughout distribution, including in challenging climatic conditions, positions aluminum foil as a critical growth material in the evolving tablets and capsules packaging landscape.

Regional Insights

North America Tablets and Capsules Packaging Market Trends - Compliance-Driven Scale and Patient-Centric Innovation

North America is projected to lead the market, accounting for approximately 37.4% of total demand, with the U.S. representing the clear center of gravity. The region’s dominance is underpinned by its large pharmaceutical manufacturing base, high prescription drug utilization, and strong over-the-counter (OTC) consumption. According to U.S. Centers for Disease Control and Prevention (CDC) data, over 65% of U.S. adults use at least one prescription drug annually, directly sustaining demand for high-volume, compliant primary packaging formats such as blisters and bottles.

Regulatory requirements play a defining role in shaping packaging demand. The U.S. Drug Supply Chain Security Act (DSCSA) mandates end-to-end traceability, serialization, and tamper evidence, favoring well-capitalized packaging suppliers with advanced digital and compliance capabilities. Companies such as WestRock, Amcor, and Berry Global have expanded investments in serialized blister lines, child-resistant closures, and integrated labeling solutions to meet these requirements. These investments support pharmaceutical customers in maintaining uninterrupted market access while reducing recall and diversion risks.

Patient-centric packaging continues to gain traction across North America, particularly for chronic disease therapies and senior care. Calendar blister packs, senior-friendly push-through designs, and adherence-enhancing formats are increasingly adopted by branded drug manufacturers and large pharmacy chains. For example, packaging innovations aligned with adherence programs at major U.S. pharmacy retailers have accelerated demand for unit-dose blister solutions over traditional bulk bottles in select therapeutic categories.

North America remains a hub for automation, sustainability, and supply-chain resilience initiatives. Packaging converters are deploying robotics, vision inspection systems, and data-integrated quality controls to address labor constraints and regulatory scrutiny. Sustainability commitments from pharmaceutical majors have also driven increased use of downgauged plastics, recyclable blister alternatives, and post-consumer resin (PCR) content, reinforcing the region’s role as a technology and compliance benchmark for the global market.

Europe Tablets and Capsules Packaging Market Trends - Harmonized Serialization and Sustainability Integration

Europe represents a substantial share of global tablets and capsules packaging demand, supported by mature pharmaceutical manufacturing ecosystems across Germany, the United Kingdom, France, Italy, and Spain. The region benefits from strong generic drug penetration, export-oriented production, and a harmonized regulatory framework under the European Medicines Agency (EMA), which facilitates cross-border pharmaceutical and packaging supply.

Regulatory alignment across the European Union has accelerated the adoption of standardized packaging solutions, particularly serialized blister packs and tamper-evident formats. The EU Falsified Medicines Directive (FMD) continues to shape packaging investments, driving demand for high-quality printing, verification-ready designs, and validated materials. European packaging specialists such as Constantia Flexibles and Huhtamaki have expanded cold-form foil and high-barrier blister capabilities to support both branded and generic drug manufacturers operating under these requirements.

Sustainability is a defining differentiator in the European market. The EU Circular Economy Action Plan and packaging waste directives have prompted pharmaceutical companies to reassess material choices, pushing packaging converters toward recyclable structures, mono-material blisters, and reduced aluminum usage where feasible. Germany and France, in particular, have seen increased collaboration between drug manufacturers and packaging suppliers to pilot recyclable blister concepts while maintaining regulatory compliance.

Investment trends across Europe increasingly favor suppliers with clear environmental roadmaps and validated circular-economy strategies. Digitalization is also advancing, with manufacturers integrating smart serialization, track-and-trace systems, and real-time quality monitoring into packaging operations. Europe continues to set benchmarks for regulatory rigor, sustainability integration, and technical sophistication in tablets and capsules packaging.

Asia Pacific Tablets and Capsules Packaging Market Trends - Generic Manufacturing Expansion and Cost-Efficient Compliance

Asia Pacific is likely to be the fastest-growing regional market, driven by rapid expansion in pharmaceutical manufacturing in China, India, and the ASEAN countries. Growth is supported by rising healthcare access, expanding middle-class populations, and increasing consumption of both prescription medicines and nutraceutical products. India, now one of the world’s largest suppliers of generic drugs, is a particularly strong driver of demand for cost-efficient yet compliant packaging formats.

Regulatory upgrades across the region are reshaping packaging requirements. India’s tightening of Good Manufacturing Practice (GMP) norms and China’s evolving drug traceability regulations are increasing demand for validated packaging systems, high-barrier materials, and serialized solutions. In response, global packaging companies such as Amcor and Constantia Flexibles have expanded regional production and technical support capabilities to serve both domestic manufacturers and export-focused pharmaceutical firms.

Asia Pacific is also a critical manufacturing hub for blister packs and strip packs used in global pharmaceutical supply chains. Cold-form aluminum strip packs are widely adopted for export-oriented formulations destined for regulated markets in North America and Europe. ASEAN countries, including Vietnam and Indonesia, are emerging as secondary manufacturing bases, supported by government incentives and improving regulatory alignment. A combination of cost efficiency, regulatory compliance, and localized technical expertise drives competitive advantage in the region.

While price sensitivity remains high, pharmaceutical companies increasingly prioritize packaging partners that can support regulatory audits, stability requirements, and international market access. As a result, Asia Pacific continues to transition from a cost-led market to one where compliance, quality, and scalability define long-term growth trajectories.

Competitive Landscape

The global tablets and capsules packaging market is moderately fragmented, with leading multinational players leveraging scale, regulatory expertise, and integrated service offerings, while numerous regional converters serve local and generic drug markets. Market concentration remains lower than injectable packaging due to the relative accessibility of oral solid-dose manufacturing.

Competitive advantage is shaped by validation capabilities, material innovation, and end-to-end packaging solutions. Recent strategies include capacity expansion in high-growth regions, acquisitions to strengthen oral-dose portfolios, and investments in advanced and sustainable materials. Key differentiators include validated drug-contact materials, serialization capabilities, rapid qualification, and integrated fill-and-finish packaging models.

Key Industry Developments

- In January 2025, Gerresheimer AG launched Gx Cap, a digitally connected closure that enables enhanced remote therapeutic monitoring and digital traceability of prescription medication containers, strengthening digital integration across tablets and capsules packaging systems.

- In July 2025, AptarGroup, Inc. introduced its first nasal spray pump made with 52% bio-based feedstock, marking a significant sustainability milestone in pharmaceutical dosing components and broader oral solid-dose packaging ecosystems.

Companies Covered in Tablets and Capsules Packaging Market

- Amcor plc

- Gerresheimer AG

- AptarGroup, Inc.

- West Pharmaceutical Services, Inc.

- SCHOTT AG

- Becton, Dickinson and Company (BD)

- Berry Global Group, Inc.

- CCL Industries Inc.

- Constantia Flexibles

- Huhtamaki Oyj

- Nelipak Healthcare Packaging

- Uflex Limited

- Origin Pharma Packaging

- Avery Dennison Corporation

- Ardagh Group S.A.

- SGD Pharma

- Nipro Corporation

- Bilcare Limited

Frequently Asked Questions

The global tablets and capsules packaging market is estimated to be valued at US$13.5 billion in 2026.

By 2033, the tablets and capsules packaging market is expected to reach US$19.6 billion.

Key trends include the growing adoption of unit-dose blister packaging, increased focus on patient-centric and adherence-supporting designs, rising demand for high-barrier materials for moisture- and light-sensitive formulations, and accelerating investment in sustainable and recyclable packaging solutions.

Blister packs are the leading packaging type, accounting for around 44.6% of total market demand, supported by their suitability for prescription, OTC, and hospital-use medicines.

The tablets and capsules packaging market is projected to grow at a CAGR of 5.5% between 2026 and 2033.

Major players with strong and diversified portfolios include Amcor plc, Gerresheimer AG, AptarGroup, Inc., West Pharmaceutical Services, and SCHOTT AG.