- Food Packaging

- Crown Caps Market

Crown Caps Market Size, Share, and Growth Forecast, 2026 – 2033

Crown Caps Market by Material Type (Aluminum, Steel, Tin-Plated Steel), Application (Beverage, Alcohol Drinks, Non-Alcohol Drinks, Food, Pharmaceuticals and Nutraceuticals), and Regional Analysis for 2026 – 2033

Crown Caps Market Size and Trends Analysis

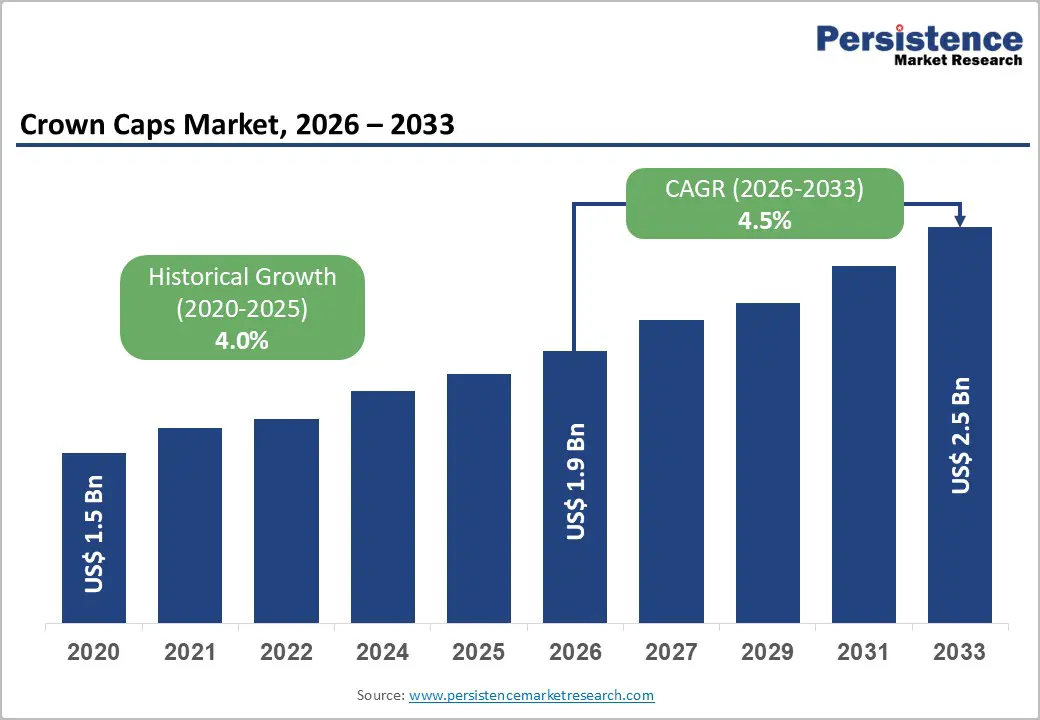

The global crown caps market size is likely to be valued at US$1.9 billion in 2026 and is expected to reach US$2.5 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by the continued preference for glass packaging across beverage, food, and select pharmaceutical applications due to its premium appeal, recyclability, and superior barrier properties. Crown caps are a reliable closure for carbonated and fermented drinks, ensuring strong sealing, tamper evidence, and high-speed bottling compatibility. The growing demand for beer, soft drinks, and premium beverages, particularly in the craft segment, is driving the need for advanced crown cap solutions. Food producers use them for sauces and condiments to maintain freshness and shelf life. Emerging markets, fueled by urbanization and rising incomes, are key to market growth.

Key Industry Highlights:

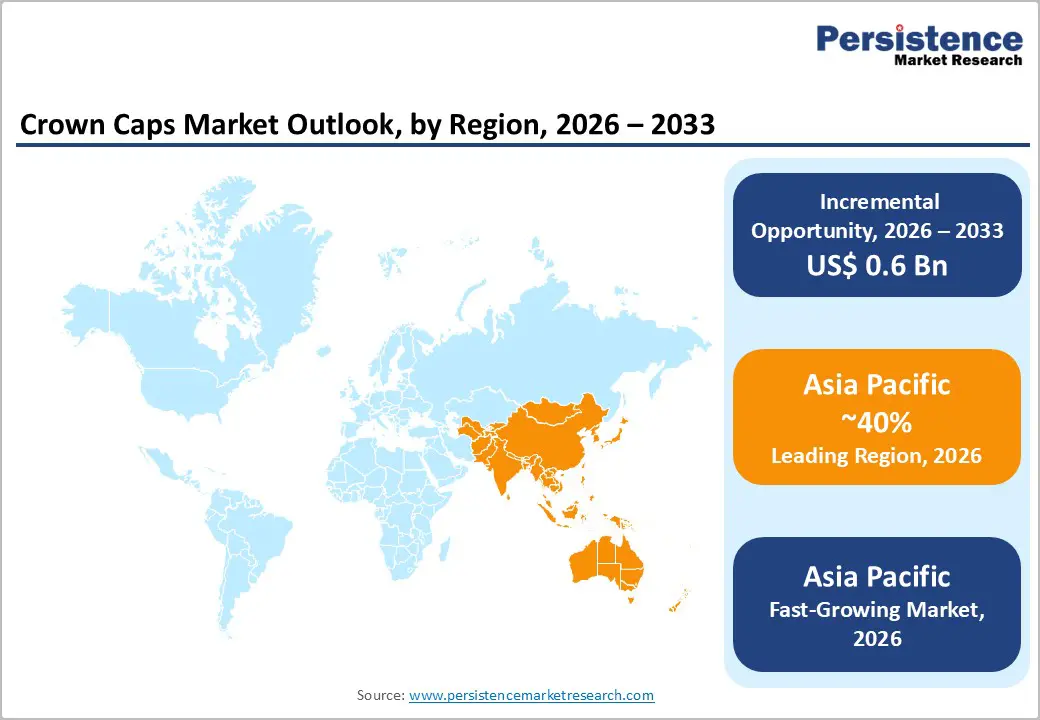

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong beverage consumption growth, expanding glass packaging adoption, cost-efficient manufacturing, and increasing investments by regional players across China, India, Japan, and ASEAN economies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the crown caps in 2026, supported by rising bottled beverage consumption, expansion of breweries and soft drink manufacturing, growing preference for glass packaging, cost-efficient production, and increasing investments by regional packaging players.

- Leading Material Type: Tin-plated steel is projected to represent the leading product type in 2026, accounting for 48% of the revenue share, driven by its excellent barrier properties, durability on high-speed lines, and suitability for premium beverage and food applications.

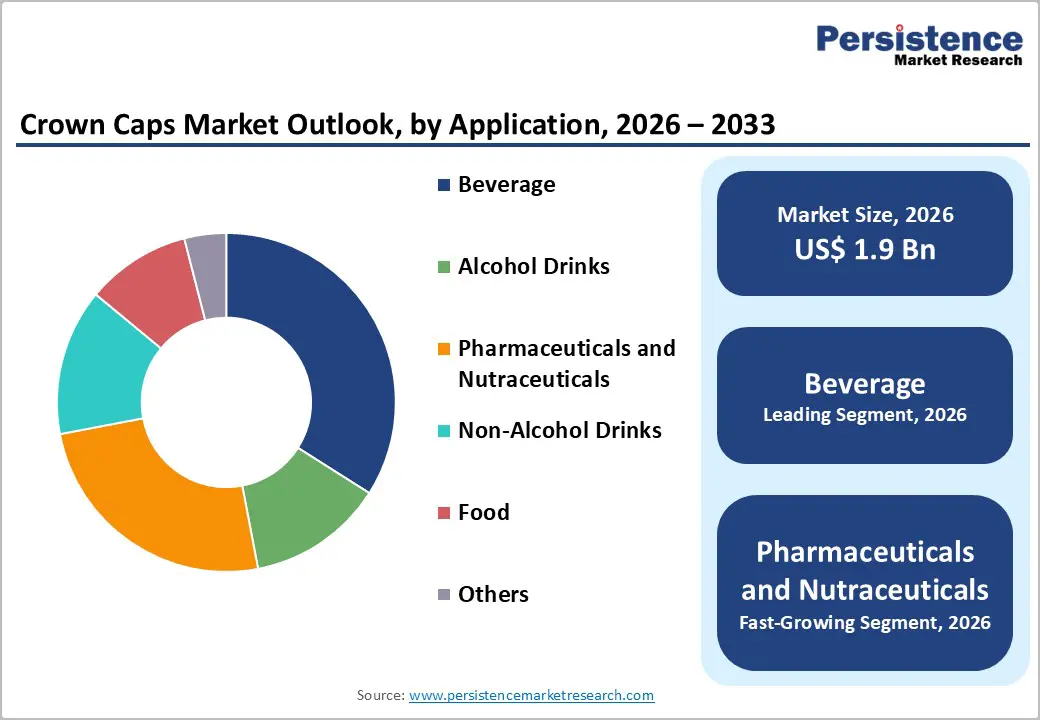

- Leading Application: Beverages are anticipated to be the leading application type, accounting for over 60% of the revenue share in 2026, supported by strong demand for alcoholic and non-alcoholic drinks, premium glass-bottle consumption, and carbonation requirements in beverage packaging.

| Report Attribute | Details |

|---|---|

|

Crown Caps Market Size (2026E) |

US$1.9 Bn |

|

Market Value Forecast (2033F) |

US$2.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of the Beverage Industry, Particularly Craft Beer and Functional Drinks

Increasing consumer preference for specialty, premium, and health-oriented beverages has led to higher demand for glass bottles sealed with reliable metal caps. Craft breweries emphasize product freshness, carbonation integrity, and distinctive branding, which crown caps provide through customizable designs and tamper-evident closures. Functional beverages, including energy drinks, fortified waters, and probiotics, require high-quality sealing solutions to maintain efficacy and shelf life. This trend has expanded production volumes, particularly in emerging markets, reinforcing crown caps as the preferred closure solution.

The rapid proliferation of artisanal and small-scale breweries has intensified competition, pushing manufacturers to adopt crown caps that combine durability with premium aesthetics. Beverage companies are leveraging crown caps as a marketing tool, employing printed designs, embossing, and limited-edition branding to attract consumers. Functional drink producers increasingly prioritize packaging that maintains product integrity under variable storage conditions, making metal closures critical for quality assurance. The rising number of breweries and beverage startups worldwide, coupled with growing urbanization and disposable income, ensures steady growth in crown cap demand.

Rising Demand in Pharmaceuticals and Nutraceuticals

Liquid medicines, syrups, dietary supplements, and nutraceutical products require tamper-evident, child-resistant, and contamination-proof closures, which crown caps effectively provide. Regulatory mandates on product integrity, safety, and traceability drive the adoption of metal closures. Crown caps ensure hermetic sealing, protecting formulations from air, moisture, and microbial contamination, which is essential for maintaining efficacy and shelf life. Growth in preventive healthcare, wellness supplements, and functional nutraceuticals across developed and emerging markets fuels steady demand for specialized crown cap solutions in these sectors.

Pharmaceutical companies increasingly seek closures that facilitate branding, product differentiation, and anti-counterfeit measures. Crown caps with advanced liners and embossed markings allow manufacturers to maintain both safety and aesthetic appeal. The expansion of nutraceutical consumption, driven by health-conscious lifestyles and aging populations, has led to higher production volumes of liquid dietary supplements. These developments necessitate reliable, high-quality closures capable of meeting quality standards. Crown caps are not limited to beverages but are becoming indispensable in pharmaceutical and nutraceutical packaging, offering both functional protection and compliance with evolving international regulations.

Barrier Analysis - Competition from Plastic Closures and Pet Packaging

Plastic caps and PET bottles are lightweight, cost-effective, and compatible with automated bottling lines, providing competition for traditional metal closures. Many beverage manufacturers prioritize cost efficiency and supply chain simplicity, making plastics attractive alternatives. Single-use PET bottles dominate non-alcoholic beverage segments, where high-speed production and lightweight packaging reduce shipping costs. Consumer perception of convenience encourages plastic adoption. This competitive pressure limits crown caps market penetration, particularly in price-sensitive markets, where cost advantages and operational flexibility of plastic and PET packaging outweigh the benefits of metal closures.

Plastic and PET alternatives also offer diverse design options, including resealability and ergonomic caps, appealing to convenience-oriented consumers. The growing environmental debate surrounding single-use metals versus lightweight plastics creates uncertainty in material selection. While crown caps excel in sealing and premium perception, manufacturers balancing cost, consumer preference, and environmental regulations may opt for plastic closures. PET packaging growth in emerging economies, driven by high-volume beverage consumption, reduces opportunities for crown cap adoption. These dynamics present a key restraint, requiring crown cap manufacturers to innovate in lightweight alloys, recyclable liners, and branding solutions to maintain competitiveness against flexible plastic alternatives.

Supply Chain and Logistical Complexities

Metal production, tin-plating, and liner material sourcing require coordination across multiple suppliers, often involving procurement networks. Delays in raw material availability, price volatility in metals, and disruptions in transportation can impact production schedules. High-speed bottling lines demand precise and consistent quality from closures, making supply reliability critical. International regulations on import-export, packaging materials, and food safety introduce additional complexity. Managing these factors increases operational costs, inventory requirements, and lead times, posing challenges for manufacturers aiming to meet growing demand in beverage, food, and pharmaceutical segments.

Logistical constraints also extend to distribution, storage, and inventory management. Crown caps must be handled carefully to prevent damage, corrosion, or deformation, especially during transit over long distances. Seasonal demand fluctuations in beverages, such as peak beer consumption periods, require agile supply chain strategies to avoid shortages or excess stock. Manufacturers must balance production efficiency with quality control, often necessitating advanced warehousing, tracking, and packaging systems. These operational challenges, coupled with rising fuel costs and transportation disruptions, create significant barriers.

Opportunity Analysis - Premiumization and Smart Closure Technologies

Beverage and pharmaceutical companies increasingly seek closures that enhance brand perception, consumer engagement, and product differentiation. Embossed designs, digital printing, and metallic finishes enable limited-edition and craft product packaging that appeals to premium consumers. Smart closure technologies, including QR codes, NFC chips, and anti-counterfeit features, allow interactive experiences, traceability, and authentication. These innovations increase the value of crown caps beyond their functional purpose, enabling manufacturers to target high-margin segments.

The trend toward premiumization is particularly strong in craft beers, functional beverages, and specialty non-alcoholic drinks, where packaging aesthetics influence purchase decisions. Smart closures also help companies comply with traceability and safety regulations while offering marketing and data-driven advantages. Manufacturers can leverage these opportunities by investing in advanced printing, embossing, and connectivity-enabled crown caps that provide both security and an enhanced consumer experience. By differentiating products through design, technology, and sustainability, crown cap producers can expand market share and profitability.

Adoption of Advanced Liner Technologies and PVC-Free/Bio-Based Alternatives

Traditional liners, often PVC-based, are being replaced by environmentally friendly, food-safe materials that meet sustainability regulations and consumer expectations. Bio-based and recyclable liners reduce environmental impact while maintaining airtight seals and corrosion resistance. Advanced liners also improve product integrity, prevent flavor contamination, and extend shelf life in beverages, food, and pharmaceutical applications. As companies adopt green packaging strategies and regulators encourage sustainable alternatives, crown cap manufacturers can differentiate themselves by offering innovative closure solutions aligned with environmental responsibility.

Advanced liners allow crown caps to meet increasingly stringent food safety and regulatory standards across markets. Manufacturers can leverage PVC-free and bio-based liners to appeal to eco-conscious consumers, particularly in premium and craft segments. Innovations in liner design also enhance tamper-evidence, sealing performance, and compatibility with high-speed bottling, providing functional advantages alongside sustainability benefits. The growing emphasis on circular economy practices and corporate environmental responsibility strengthens demand for these advanced closures. By integrating bio-based and high-performance liner technologies, crown cap producers can capture new market segments, reduce environmental footprint, and reinforce their position as leaders in sustainable packaging solutions.

Category-wise Analysis

Material Type Insights

Tin-plated steel is expected to lead the crown caps market, accounting for approximately 48% of revenue in 2026, driven by its cost-effectiveness, mechanical robustness, and compatibility with high-speed bottling operations. Its durability ensures consistent sealing for carbonated beverages, preventing leakage and maintaining product quality across large-scale production. Tin-plated steel, in particular, offers superior barrier properties, corrosion resistance, and a glossy finish that enhances premium packaging, making it ideal for both beverage and food applications. For example, major beer brands such as Heineken utilize tin-plated steel crown caps to preserve carbonation and maintain the integrity of glass bottles while providing a premium aesthetic that aligns with brand positioning.

Aluminum is likely to represent the fastest-growing segment in 2026, supported by its lightweight, corrosion-resistant, and infinitely recyclable properties. Aluminum crowns appeal strongly to craft and premium beverage producers, where aesthetics, sustainability, and consumer perception play a critical role. For example, craft beer producers such as BrewDog are increasingly adopting aluminum crown caps for limited-edition or seasonal bottles, leveraging their high-quality finish and design flexibility to enhance brand appeal. Aluminum’s lightweight nature reduces shipping costs, while advanced alloys and hybrid designs maintain sealing integrity and barrier performance comparable to steel.

Application Insights

Beverages are projected to lead the market, capturing around 60% of the revenue share in 2026, supported by their reliance on reliable metal closures for carbonation and freshness. Alcoholic beverages, especially beer, benefit from crown caps’ airtight sealing properties and compatibility with traditional glass bottles. For example, Budweiser employs crown caps extensively for its standard and premium beers, ensuring carbonation retention, product safety, and tamper evidence while supporting high-speed production lines. Non-alcoholic beverages, including carbonated soft drinks and bottled water, also rely on metal closures to maintain quality during storage and transport.

Pharmaceuticals and nutraceuticals are likely to be the fastest-growing application in 2026, driven by regulatory requirements for tamper-evident, child-resistant, and contamination-proof closures. This segment benefits from crown caps’ ability to maintain product integrity, extend shelf life, and comply with stringent safety standards for liquid medicines, syrups, and dietary supplements. For example, Ayurvedic liquid nutraceutical brands such as Dabur’s Chyawanprash syrups increasingly utilize metal crown caps with specialized liners to ensure tamper-evidence and maintain bioactive compound stability. Rising health-conscious consumer demand and the expansion of liquid nutraceutical products amplify this growth.

Regional Insights

North America Crown Caps Market Trends

In 2026, North America is expected to be a key market for crown caps, fueled by a well-established and evolving beverage packaging sector that prioritizes durable, high-quality metal closures for both alcoholic and non-alcoholic beverages. As beverage companies strive to meet growing consumer demands for sustainability and adhere to stricter environmental regulations, there is a noticeable shift toward adopting recyclable, eco-friendly closure solutions. For instance, Crown Holdings Inc., a leading U.S. packaging manufacturer, is actively advancing recycling initiatives and improving closure performance. This reflects broader regional trends towards sustainable, compliant metal closure solutions that enhance brand differentiation and support environmental objectives.

Innovation in packaging technologies and customization is another key trend shaping the North America crown caps market. Brands are leveraging advanced digital printing, enhanced liner formulations, and customization capabilities to differentiate products in crowded retail environments. These developments accommodate both aesthetic branding needs and functional performance requirements, such as tamper-evidence and improved seal integrity, which remain critical for beverage and specialty liquid products.

Europe Crown Caps Market Trends

Europe is likely to be a significant market for crown caps in 2026, due to its deeply rooted beverage culture and advanced packaging landscape, making it one of the most mature and stable regions. European countries such as Germany, the U.K., and Belgium have longstanding traditions of beer and mineral water consumption, where crown caps remain essential for carbonation retention, product freshness, and brand presentation. Regulatory emphasis on sustainability and recycling has strongly influenced market dynamics. European Union directives and national recycling targets compel manufacturers to adopt lightweight, recyclable materials and PVC-free liners to comply with strict environmental standards, reinforcing demand for metal crown closures over plastics.

Competitive dynamics in the European crown caps segment are driven by innovation, sustainability commitments, and strategic expansions by key players. Companies are investing in advanced material science and production capabilities to meet evolving market and regulatory demands. For example, Pelliconi & C. SpA, an Italian manufacturer with a strong European footprint, has been intensifying its focus on sustainable crown caps that align with circular economy goals through improved recyclability and eco-friendly coatings, catering to both traditional beverage producers and premium wine bottlers.

Asia Pacific Crown Caps Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by rapid expansion in beverage consumption, rising disposable incomes, and robust manufacturing capabilities across major economies such as China, India, and Southeast Asian nations. The region’s strong demand for bottled beers, carbonated drinks, and artisan beverages reinforces the preference for crown closures, which ensure carbonation retention and product freshness, especially in glass packaging formats. Government initiatives promoting sustainable packaging and recyclable materials strengthen metal closure adoption.

The region packaging market is highly competitive, with several manufacturers introducing value-added, tamper-evident, and customizable closures that cater to consumer preferences for premium, safe, and sustainable packaging. Beyond beverages, there is significant uptake of crown caps in segments such as nutraceuticals and specialty food products, driven by growth in health-oriented liquid formulations. For example, Silgan Holdings Inc. has strengthened its presence by launching advanced closure designs and expanding production facilities in South Korea and India, aligning with the region’s sustainability mandates and diverse application needs.

Competitive Landscape

The global crown caps market exhibits a moderately fragmented structure, driven by the coexistence of several large multinational manufacturers and a diverse base of regional and niche players competing across materials, applications, and geographies. While top converters collectively hold a sizeable portion of capacity, smaller firms contribute innovation, customization, and localized service offerings that enhance competitive intensity. The industry emphasizes sustainable and technologically advanced solutions, with companies focusing on recyclable materials, smart printing, and tamper-evident designs to meet evolving regulatory standards and end-user preferences.

With key leaders including Crown Holdings Inc., Pelliconi & C. SpA, Nippon Closures Co., Ltd., Silgan Holdings Inc., and Guala Closures Group S.p.A., the market is defined by both scale and specialization. These players compete through continuous product innovation, expanded geographic footprints, strategic partnerships, and investments in sustainability and digital capabilities.

Key Industry Developments:

- In January 2026, Ajanta Bottle Pvt Ltd launched its 30/40 ML ABPL Bold Glass Bottle, designed for skincare and cosmetic brands seeking premium packaging. Targeting the growing personal care and beauty segment, the bottle features a 47 ± 2 ml OFC, a 135 g weight, and a 19 mm bold neck, making it perfect for serums, oils, and luxury liquid formulations. Its design boosts shelf appeal and supports functional performance, aligning with trends favoring glass packaging for high-end, natural products.

- In November 2025, Nipra Industries introduced its pry-off crown caps at Drinktec India 2025 in Mumbai, marking its entry into the traditional crown-closure market. After initial success with select customers in beer, RTD, and carbonated beverage segments, the company aimed to expand its customer base both domestically and internationally, driven by shifts in India’s demographics and growing alcohol consumption, especially among the young population.

Companies Covered in Crown Caps Market

- Ajanta Bottle

- Amigo Sampoorna Panacea

- Arishtam

- Brewnation

- Brijrani Enterprises

- Brouwland

- Crown Holdings Inc.

- Pelliconi & C. SpA

- Nippon Closures Co., Ltd.

- Silgan Holdings Inc.

- Guala Closures Group S.p.A.

Frequently Asked Questions

The global crown caps market is projected to reach US$1.9 billion in 2026.

The crown caps market is driven by rising demand for glass-bottled beverages, especially beer and carbonated drinks, along with growing preference for recyclable, tamper-evident, and premium metal closures.

The crown caps market is expected to grow at a CAGR of 4.5% from 2026 to 2033.

Key market opportunities in the crown caps market include premiumization of beverage packaging, adoption of smart and decorative closures, and growing demand for sustainable, PVC-free, and recyclable liner technologies.

Ajanta Bottle, Amigo Sampoorna Panacea, Arishtam, Brewnation, Brijrani Enterprises, and Brouwland are the leading players.