- Chipsets & Processors

- Battery Management ICs Market

Battery Management ICs Market Size, Share, and Growth Forecast 2026 - 2033

Battery Management ICs Market by IC Type (Battery ICs, Battery Authentication ICs, Battery Fuel Gauge ICs, Battery Protector ICs, Others), Application (Automotive, Industrial Equipment, Medical Devices, Consumer Electronics, Others), Regional Analysis, 2026 - 2033

Battery Management ICs Market Size and Trend Analysis

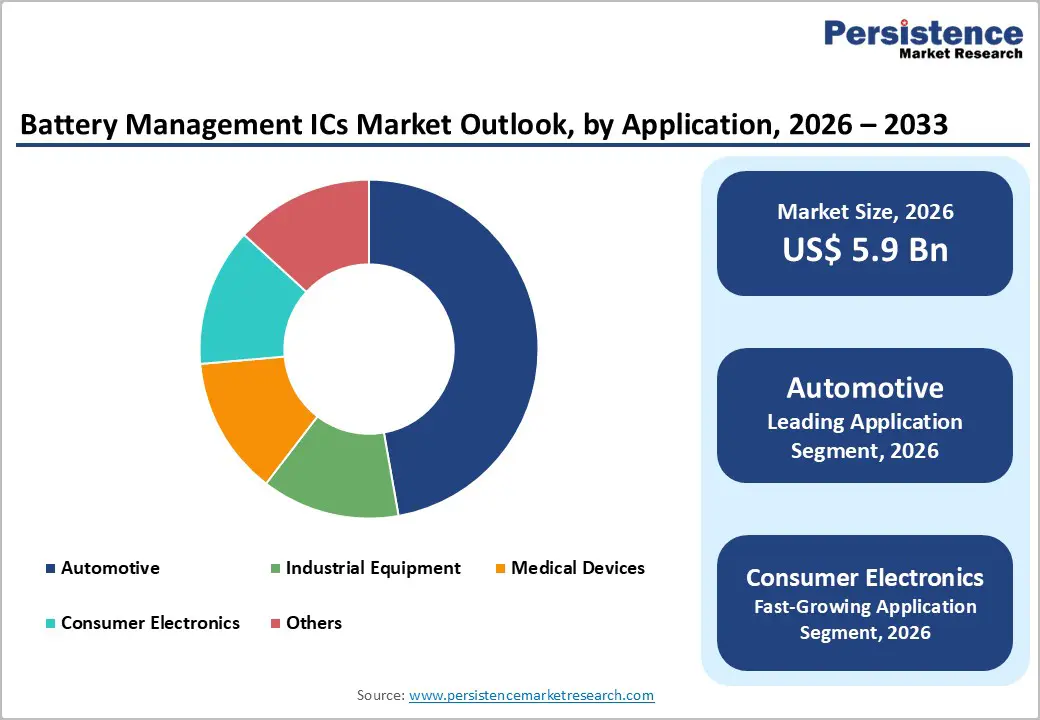

The global battery management ICs market size is expected to be valued at US$ 5.9 billion in 2026 and projected to reach US$ 8.5 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

The market is experiencing steady growth driven by the accelerating electrification of transportation and the surging demand for energy storage systems across industrial and consumer segments. The proliferation of lithium-ion battery applications in electric vehicles, portable consumer electronics, and renewable energy infrastructure is creating substantial demand for sophisticated battery management semiconductor solutions.

Key Industry Highlights:

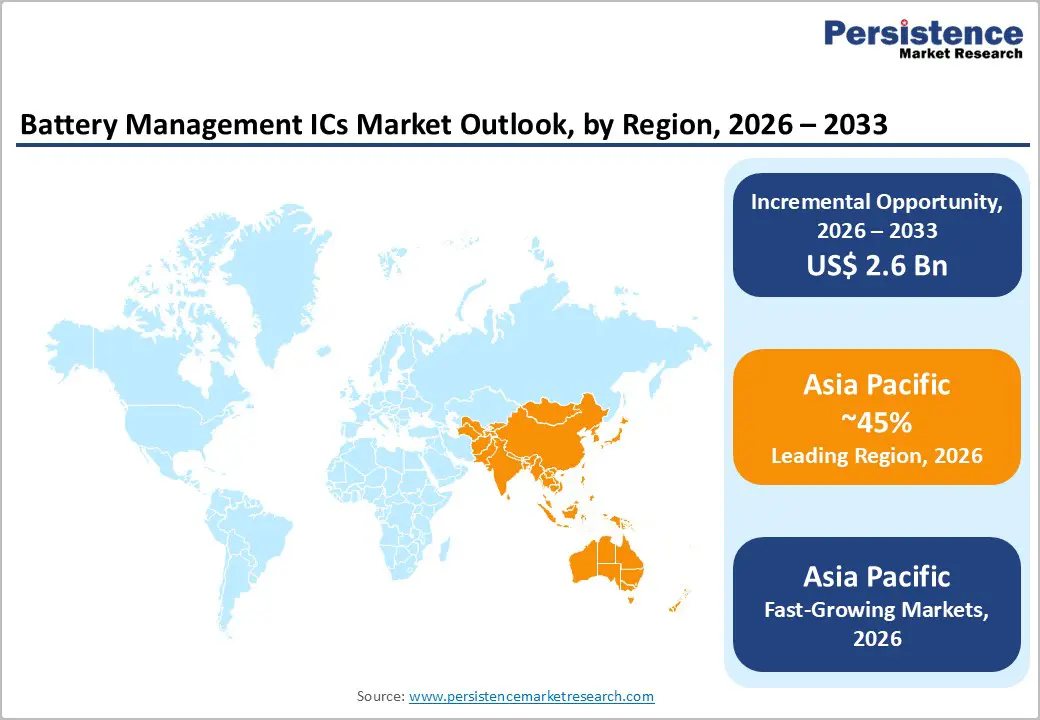

- Leading Region: Asia Pacific remains the largest battery management IC market with about 45% global share, driven by its dominance in lithium-ion battery manufacturing, 62% share of global EV production, and the scale advantages of CATL and BYD.

- Fastest Growing Region: North America is the fastest-growing region with a projected 7.8% CAGR through 2032, supported by large-scale clean energy investments under the Inflation Reduction Act and rising domestic EV and storage deployments.

- Dominant Segment: Battery Fuel Gauge ICs hold roughly 36% of the IC type market in 2025 due to their widespread use in consumer electronics for precise state-of-charge measurement and low-power performance.

- Fastest Growing Segment: Consumer Electronics applications are the fastest-growing category with an estimated 7.2% CAGR through 2032, driven by expanding adoption of portable and wearable devices requiring compact battery management solutions.

- Key Market Opportunity: Advanced authentication and anti-counterfeiting battery management ICs present a major opportunity as counterfeit products rise globally and industries increasingly adopt SHA-256-based secure identification solutions.

| Global Market Attribute | Key Insights |

|---|---|

| Battery Management ICs Market Size (2026E) | US$ 5.9 billion |

| Market Value Forecast (2033F) | US$ 8.5 billion |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.9% |

Market Dynamics

Drivers - Accelerating Electric Vehicle Adoption and Battery Pack Complexity

The global electric vehicle market has experienced unprecedented expansion, with over 14 million EV sales recorded worldwide in 2023, establishing a compelling growth trajectory for battery management IC demand. Modern electric and hybrid vehicles require highly sophisticated battery management systems that monitor, balance, and protect multi-cell lithium-ion battery packs containing dozens to hundreds of individual cells operating at voltages exceeding 400 volts in contemporary vehicle architectures.

Battery management ICs provide essential functionality including cell-level voltage monitoring with precision exceeding 1.4 millivolts, current sensing, thermal management, and fault detection capabilities critical for ensuring vehicle safety and maximizing battery performance and longevity. Premium automotive manufacturers including BMW and Mercedes-Benz, have integrated advanced battery management ICs specifically engineered to improve driving range and charging efficiency characteristics that directly influence consumer purchasing decisions in the highly competitive EV market segment.

Integration of Battery Management Systems with Renewable Energy Storage and Industrial Applications

The rapid expansion of renewable energy capacity, combined with growing deployment of utility-scale and distributed energy storage systems, is creating substantial demand for battery management ICs capable of monitoring and protecting large lithium-ion battery installations. Energy storage systems deployed for grid stabilization, microgrid applications, and industrial backup power require battery management ICs that can coordinate operation of massive battery arrays containing thousands of cells organized in complex configurations, necessitating specialized monitoring and balancing architecture.

Industrial equipment manufacturers are increasingly implementing battery management solutions in material handling equipment, power tools, and backup power systems where extended battery performance directly influences operational efficiency and total cost of ownership calculations. The convergence of renewable energy expansion with storage system deployment, particularly in markets such as the United States where the Inflation Reduction Act of 2022 allocated US$ 369 billion for clean energy initiatives, is establishing a secular growth trajectory for battery management IC consumption across stationary energy storage applications.

Restraints - High Design Complexity and Extended Development Cycles in Automotive Applications

Battery management IC designs for automotive applications must navigate increasingly stringent safety standards, including ISO 26262 functional safety requirements and ASIL-D safety integrity levels that establish rigorous development, testing, and validation procedures extending product development timelines to 18-36 months from concept to production release. The integration of multiple protection mechanisms including overcurrent detection, overvoltage protection, thermal shutdown, and cell balancing functionality into miniaturized semiconductor packages, increases design complexity substantially while requiring extensive validation against diverse operating conditions, environmental stresses, and failure modes.

Automotive manufacturers maintain conservative supplier qualification processes and typically require long-term supply commitments from battery management IC suppliers, creating significant barriers to entry for emerging competitors and limiting design flexibility for established manufacturers seeking to introduce innovative architectural approaches.

Regulatory Compliance Burden and Evolving International Standards

The regulatory landscape surrounding battery management systems and lithium-ion battery safety has become increasingly complex, with the European Union Battery Regulation 2023/1542 introducing new requirements effective from February 18, 2027, mandating digital battery passports and sustainability tracking mechanisms for all industrial and electric vehicle batteries exceeding 2 kilowatt-hours capacity.

Medical device battery management requires compliance with multiple overlapping standards including IEC 62133, UL 2054, ISO 13485, and IEC 60601-1, each imposing distinct design and validation requirements that increase development costs and extend time-to-market timelines for medical-grade battery management solutions. Battery management IC manufacturers must maintain compliance across multiple geographies with divergent regulatory frameworks, requiring parallel development efforts and certification processes that significantly increase operational expenses without generating proportional revenue increases.

Opportunity - Expansion of Battery Management ICs in Small and Medium-Sized Industrial Equipment and Consumer Wearables

The proliferation of battery-powered industrial equipment, including cordless power tools, automated guided vehicles, material handling systems, and robotics, is creating substantial opportunities for battery management IC suppliers to address the mid-market segment, historically underserved by complex automotive-grade solutions. Industrial equipment manufacturers increasingly demand integrated battery management ICs offering simplified integration pathways, reduced bill-of-materials costs, and extended battery lifespan that minimize replacement frequency and customer downtime.

WAN users are increasingly planning to implement advanced battery management solutions in the coming years, demonstrating substantial market runway for cost-optimized battery management IC solutions targeting the industrial equipment segment. Additionally, the proliferation of wearable health monitoring devices, connected IoT sensors, and portable consumer electronics generates consistent demand for ultra-low-power battery management ICs specifically engineered for single-cell and multi-cell configurations with minimal power consumption impact on overall device battery life.

Emergence of Advanced Authentication and Anti-Counterfeiting Battery Management IC Functionality

The expansion of global battery supply chains and the increasing prevalence of counterfeit battery products in consumer and industrial markets has created compelling demand for battery management ICs integrating advanced authentication mechanisms including SHA-256 cryptographic protocols and unique device identification features that prevent unauthorized battery pack replication. Premium battery management IC solutions incorporating proprietary authentication algorithms and 160-bit secret key encryption are commanding significant pricing premiums, with leading vendors such as Analog Devices incorporating these features into fuel gauge and protector IC products serving automotive and medical device applications.

Government initiatives promoting electrification and battery manufacturing localization, particularly in regions such as India where ATL established Asia’s largest lithium-ion battery manufacturing facility with over US$ 430 million investment, are establishing new markets for authenticated battery management solutions addressing counterfeiting concerns across rapidly expanding regional battery supply chains.

Category-wise Analysis

IC Type Insights

Battery Fuel Gauge ICs emerge as the leading segment within the IC Type category, commanding approximately 36% of the battery management IC market share in 2025. These specialized semiconductor devices integrate Coulomb counters that calculate precise battery state-of-charge measurements by monitoring cumulative current flow through the battery pack, providing system controllers with accurate remaining operating time predictions critical for consumer satisfaction and device usability. Battery fuel gauge ICs utilize 16-bit resolution measurement architecture, enabling accurate voltage, current, and temperature monitoring capabilities while maintaining ultra-low power consumption profiles essential for portable and wearable applications. Battery fuel gauge ICs communicate with system controllers through industry-standard I²C interfaces, enabling seamless integration into existing embedded system architectures while supporting sophisticated battery health monitoring algorithms that predict battery degradation and optimize charging protocols.

Application Insights

Automotive applications lead the application segment with approximately 42% market share in 2025, representing the dominant end-user for advanced battery management IC solutions. Modern electric vehicle battery packs contain dozens to hundreds of individual lithium-ion cells that require coordinated monitoring, balancing, and protection across voltage ranges exceeding 400 volts in contemporary EV architectures, necessitating sophisticated multi-cell battery management ICs capable of achieving 1.4 millivolt precision across simultaneous measurements of numerous battery cells. The automotive segment’s leadership reflects substantial investments by global vehicle manufacturers in EV platform development, with IEA Global EV Outlook 2024 data indicating Asia Pacific produced over 60% of global lithium-ion batteries specifically destined for automotive applications in electric and hybrid vehicles.

Regional Insights

North America Battery Management ICs Market Trends and Insights

North America represents the fastest-growing regional market, expected to expand at an estimated 7.8% CAGR through 2033, driven by substantial government investments in domestic EV manufacturing and energy storage infrastructure. The Inflation Reduction Act of 2022 allocates US$ 369 billion for clean energy initiatives, including vehicle electrification and domestic battery manufacturing expansion, incentivizing automotive manufacturers, including Tesla and General Motors, to scale battery production facilities across the United States and develop robust supply chains for critical components, comprising battery management ICs.

Regulatory compliance requirements, including the EPA emission standards and state-level mandates establishing aggressive EV adoption targets, are establishing consistent baseline demand for automotive-grade battery management solutions. North American enterprises demonstrate strong adoption of energy storage systems for grid stabilization and backup power applications, with utility companies and industrial operators increasingly implementing battery energy storage systems requiring sophisticated battery management IC solutions for operational monitoring and performance optimization across diverse climatic conditions and extended deployment timelines.

Europe Battery Management ICs Market Trends and Insights

Europe maintains the second-largest regional market position with approximately 28% market share, characterized by leadership in automotive battery management IC innovation and sustainability-focused regulatory frameworks. The European Union Battery Regulation 2023/1542 establishes comprehensive requirements, including digital battery passports, sustainability tracking, and recycled content mandates effective from February 18, 2027, for all industrial and electric vehicle batteries exceeding 2 kilowatt-hours capacity, requiring battery management IC manufacturers to ensure compliance with increasingly stringent environmental and traceability standards.

Major European automotive manufacturers, including Volkswagen Group, BMW, and Mercedes-Benz are accelerating EV platform development with sophisticated battery management system requirements, establishing substantial regional demand for advanced battery monitoring and protection IC solutions. Germany specifically is expected to experience significant growth at an estimated 6.5% CAGR through 2032, driven by leadership in automotive manufacturing and government initiatives promoting domestic battery manufacturing capabilities through joint ventures and technology partnerships with Asian battery manufacturers.

Asia Pacific Battery Management ICs Market Trends and Insights

Asia Pacific emerges as the dominant regional market, accounting for approximately 45% of global battery management IC market share in 2025, driven by massive lithium-ion battery manufacturing capacity and accelerating electric vehicle adoption across China, Japan, and South Korea. IEA Global EV Outlook 2024 data indicates Asia Pacific produced over 60% of global lithium-ion batteries, with China supplying approximately 80% of global battery cells and commanding nearly 60% of the EV battery market through manufacturer dominance by companies including CATL and BYD.

India is emerging as a critical growth market within the Asia Pacific region, with ATL launching Asia’s largest lithium-ion battery manufacturing facility in Haryana with over US$ 430 million investment, establishing significant regional demand for battery management IC solutions supporting domestic manufacturing expansion. India’s lithium-ion battery demand is projected to surge to approximately 150 gigawatt-hours by 2030, according to industry projections, representing a substantial market opportunity for battery management IC suppliers supporting accelerating EV adoption and renewable energy storage deployment across the Indian subcontinent.

Competitive Landscape

The global battery management IC market reflects a moderately fragmented structure where established semiconductor manufacturers retain a competitive advantage through deep analog design capabilities, robust fabrication ecosystems, and long-standing relationships with automotive and industrial OEMs. The market is shaped by high entry barriers driven by stringent automotive qualification standards, complex multi-cell monitoring requirements, and substantial R&D investments necessary for next-generation designs.

Competitive strategies increasingly emphasize integration, with vendors consolidating monitoring, balancing, protection, and authentication functions into highly efficient system-on-chip architectures to reduce customer design complexity and bill-of-material costs. Market leaders are strengthening their positions by expanding mixed-signal capabilities, investing in predictive analytics for battery health, and developing enhanced security features to support traceability and anti-counterfeiting initiatives. Strategic acquisitions, technology partnerships, and expansion into fast-growing EV and energy storage ecosystems are central to capturing design wins in a rapidly scaling global battery manufacturing landscape.

Key Market Developments

- October 2025: STMicroelectronics unveiled a prototype power delivery system for NVIDIA's 800 VDC architecture, leveraging SiC, GaN, and silicon technologies to enhance efficiency in next-generation AI data centers and factories.

- April 2022: Infineon introduces TLE9012DQU and TLE9015DQU battery management ICs for optimized cell monitoring, balancing, and extended lifetime in automotive and industrial applications.

Companies Covered in Battery Management ICs Market

- STMicroelectronics

- Infineon Technologies

- Texas Instruments

- Maxim Integrated

- Microchip Technology

- Diodes Incorporated

- Panasonic Industry Co. Ltd.

- Analog Devices

- Eutech Microelectronics

- Rohm Semiconductor

- Renesas Electronics

- LAPIS Technology Co., Ltd.

- NXP Semiconductors

- Toshiba Corporation

- Nuvoton Technology Corporation

Frequently Asked Questions

The Battery Management ICs market is projected to reach US$ 5.9 billion in 2026, expanding steadily from 2020 due to rising EV and energy storage adoption.

Key drivers include rapid EV adoption, growth in renewable energy storage, and tightening global battery safety regulations.

Asia Pacific dominates with around 45% share, supported by its leadership in lithium-ion battery production and EV manufacturing.

The major opportunity lies in advanced authentication and anti-counterfeiting battery IC solutions for high-value applications.

Leading players include STMicroelectronics, Infineon Technologies, Texas Instruments, Maxim Integrated, and Microchip Technology, with competition from Renesas, Analog Devices, and NXP.