- Energy Storage Solutions

- Micro Battery Market

Micro Battery Market Size, Share, and Growth Forecast, 2025 - 2032

Micro Battery Market by Battery Type (Primary (Non-Rechargeable), Secondary (Rechargeable)), Format (Button/Coin Batteries, Thin-Film Batteries, Others), Application (Consumer Electronics, Medical Devices, Others), and Regional Analysis for 2025 - 2032

Micro Battery Market Share and Trends Analysis

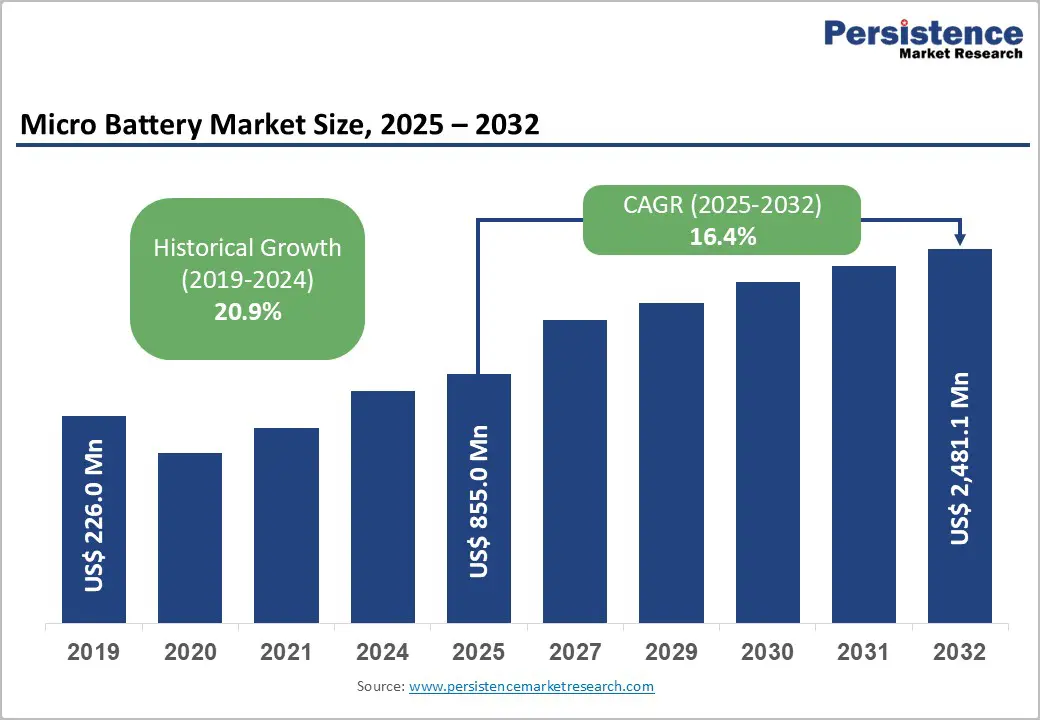

The global micro battery market size is likely to be valued at US$855.0 Million in 2025. It is estimated to reach US$2,481.1 Million by 2032, growing at a CAGR of 16.4% during the forecast period 2025 - 2032, driven by evolving applications in medical devices, consumer electronics, and the rapidly growing IoT sector, alongside regulatory shifts favoring rechargeable battery technologies.

The market is strategically positioned at the convergence of advancing flexible and thin-film battery technologies and the increasing miniaturization of smart electronics. Regional dynamics, supported by Asia Pacific’s manufacturing hubs and North America’s innovation ecosystems, establish a comprehensive growth landscape for investors and enterprises looking to leverage these transformative industry trends.

Key Industry Highlights

- Fastest-growing Battery Type: The secondary (rechargeable) battery type segment is forecast to expand at the highest CAGR, becoming the leading growth driver by 2032.

- Fastest-growing Format: Thin-film battery formats are projected to grow fastest from 2025 to 2032, supporting flexible and implantable device applications.

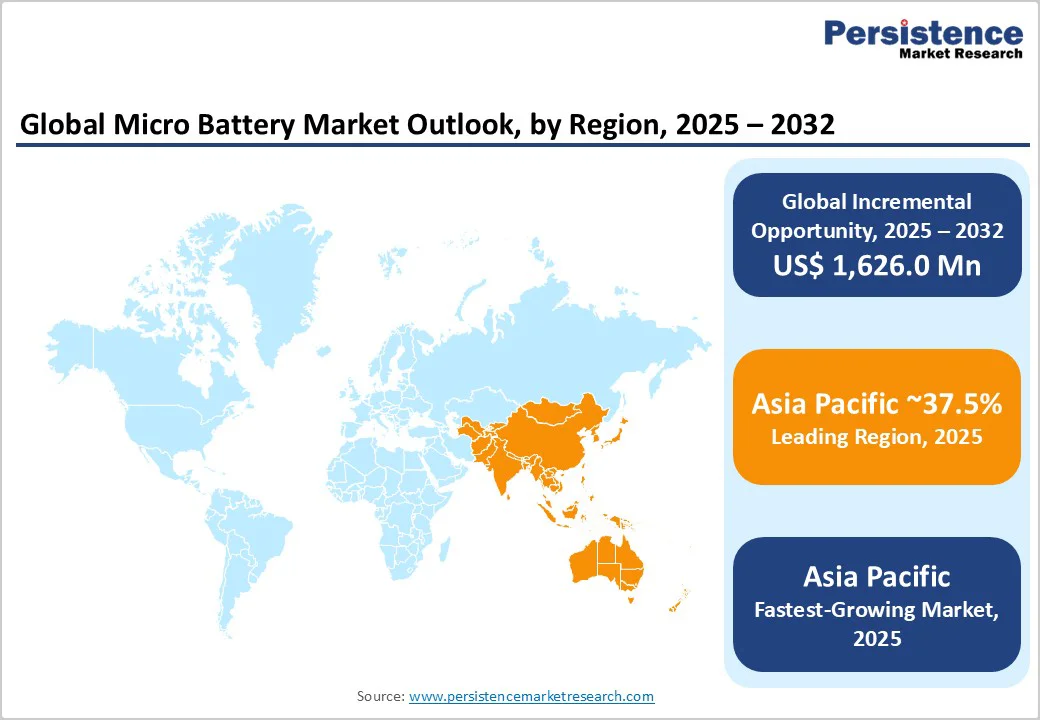

- Regional Dynamics: Asia Pacific is anticipated to be the leading and fastest-growing region in 2025, driven by its manufacturing dominance and access to raw materials.

- Key Driver: Regulatory frameworks, such as the 2023 European Union (EU) Batteries Regulation, are proving instrumental in driving the demand for sustainable and rechargeable micro batteries.

- Industry Trends: The introduction of next-generation batteries, such as silicon-anode solutions, the acquisition of battery startups, and operational expansion into the Asia Pacific are the most prominent industry trends.

- October 2025: Murata Manufacturing announced the transfer of its micro primary battery business to Maxell, Ltd., allowing Murata to focus its resources on expanding its cylindrical lithium-ion secondary battery business, targeting power tool and energy storage system markets.

| Key Insights | Details |

|---|---|

| Micro Battery Market Size (2025E) | US$855.0 Mn |

| Market Value Forecast (2032F) | US$2,481.1 Mn |

| Projected Growth (CAGR 2025 to 2032) | 16.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 20.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Shifts Accelerating Rechargeable Battery Adoption

Regulatory frameworks such as the 2023 European Union (EU) Batteries Regulation and the U.S. Environmental Protection Agency (EPA) 's environmental mandates are continually tightening requirements for battery sustainability, recycling, and hazardous materials reduction. This legislation is catalyzing a major market driver by accelerating the transition from primary (non-rechargeable) to secondary (rechargeable) micro batteries.

The shift intends to reduce the lifecycle environmental impact of batteries, aligns with corporate sustainability goals, and enables enhanced device longevity. For example, the EU requires minimum levels of recycled content and prohibits mercury in batteries, thereby prompting manufacturers to innovate in solid-state and lithium-ion microbattery technologies.

This regulatory encouragement is translating into increased investment, research, and product launches tailored toward durable, rechargeable micro batteries.

High Production Costs Impacting Advanced Battery Technologies

The micro battery market's growth is visibly hindered by elevated production and material costs, particularly for advanced formats such as solid-state and printed thin-film batteries. These costs arise from specialized raw materials, precision manufacturing processes, and the need for rigorous quality and biocompatibility certifications, especially critical in medical implants where failure is not an option.

Current estimates indicate that production costs can exceed those of traditional coin or alkaline batteries considerably, narrowing margins for manufacturers and potentially limiting market penetration in cost-sensitive emerging markets.

Supply chain restrictions for key materials such as lithium, cobalt, and silver further exacerbate this cost barrier. For instance, lithium prices spiked significantly over the 2021 - 2023 period, as reported by the U.S. Geological Survey (USGS).

Manufacturing scale-up challenges, including yield optimization for printed batteries, prolong time-to-market and constrain pricing flexibility. These challenges have necessitated targeted strategic investments in process innovation, vertical integration, and supplier diversification.

Utilization of Micro Battery Use in Smart Textiles and Wearable Electronics

An emerging and lucrative growth avenue lies in integrating microbatteries into smart textiles and wearable electronics, driven by rising consumer demand for health-monitoring garments and flexible electronics. Innovations such as fabric-based printed batteries and stretchable zinc-ion fiber batteries are enabling seamless integration of power sources into textiles, enabling continuous monitoring of biometric data with enhanced user comfort.

Strategic collaborations between textile manufacturers, battery producers, and electronics firms can foster proprietary battery integration that optimizes energy density while maintaining garment flexibility and washability.

Policy initiatives promoting wearable health technologies for aging populations in developed economies further incentivize innovation and commercialization. For market participants, early investments in flexible battery R&D and establishing manufacturing partnerships in textile hubs, such as South Asia, offer a substantial first-mover advantage and the potential to capture a rapidly expanding segment with high-value customer loyalty.

Category-wise Analysis

Battery Type Insights

Primary (non-rechargeable) batteries are projected to retain leadership in 2025, commanding an estimated 55% share of the total market value. This leadership is founded on the long-established reliability of primary batteries in critical low-drain applications requiring exceptional shelf life and stable voltage output, such as hearing aids, remote controls, and medical implants.

Mercury-free primary chemistries, including silver oxide, are increasingly favored due to tightening regulatory pressures on toxic substances, ensuring compliance with global environmental standards, and facilitating continued market relevance. Despite this dominance, the segment’s growth trajectory is relatively moderate due to saturation in traditional applications and rising preferences for rechargeable alternatives driven by sustainability concerns.

Secondary (rechargeable) batteries are set to emerge as the fastest-growing segment from 2025 through 2032. Anchored in expanding uses within electric micromobility, implantable devices requiring extended service life, and wearable consumer electronics, rechargeable micro batteries benefit from technological advances in lithium-ion and solid-state chemistries.

Manufacturers are responding to increasing regulatory mandates that incentivize rechargeable technology adoption through stricter recycling and content legislation. The rapid CAGR highlights a pivotal industry shift toward sustainability-aligned energy storage solutions, creating significant opportunities for suppliers investing in next-generation rechargeable micro batteries.

Format Insights

Button/coin batteries are slated to dominate with an estimated 40% of the micro battery market revenue share in 2025. Their widespread use in devices universally requiring compact and reliable power underpins this position, supported by mature manufacturing infrastructure and well-established global distribution networks.

Silver oxide and alkaline manganese chemistries prevail in this format, preferred for their consistent voltage output and long shelf lives, especially in medical implants and small consumer electronics. Constraints related to rigidity and limited adaptability to emerging flexible and wearable form factors moderate future growth potential.

Thin-film batteries are identified as the fastest-expanding format between 2025 and 2032. Their unique advantages, including ultra-thin, lightweight profiles and compatibility with flexible substrates, position them as indispensable enablers of next-generation wearable technology, flexible medical implants, and IoT sensor nodes.

The expansion of thin-film batteries is further driven by advances in deposition technologies and materials engineering, improving energy density, cycle life, and durability.

Application Insights

The consumer electronics segment is poised to lead applications, capturing an estimated 38% revenue share in 2025. This dominance stems from the extensive use of micro batteries in smartwatches, wireless earbuds, remote controls, and portable smart devices, where miniaturization, weight, and energy density are critical.

The segment’s growth trajectory is influenced by the continuous innovation cycle and consumer preference shifts toward wearable technologies and enhanced battery longevity.

The medical devices segment is likely to be the fastest-growing application over the 2025 - 2032 period, fueled by technological advances in implantable cardiac devices, drug delivery systems, and wearable biosensors that require highly reliable, biocompatible, and long-lasting microbatteries.

Stringent regulatory compliance, including U.S. Food and Drug Administration (FDA) approvals and international medical standards, creates barriers to entry and premium market opportunities for suppliers delivering high-performance, secure, and safe energy solutions.

Regional Insights

North America Micro Battery Market Trends

North America is forecast to grow moderately, supported by a robust innovation ecosystem concentrated in the U.S. The U.S. market benefits from an advanced healthcare infrastructure, driving early adoption of implantable medical devices, expanded integration of IoT applications, and significant private and public-sector R&D investments in battery technology breakthroughs such as solid-state and printed batteries.

Regulatory frameworks enforced by bodies including the EPA and FDA emphasize sustainability and device safety, accelerating the penetrative adoption of rechargeable micro batteries compliant with evolving environmental statutes.

Regional market growth is also being augmented by diversification into niche applications, including autonomous medical devices and smart city sensor networks. Investment trends in North America reveal a strong emphasis on vertical integration and technological partnerships, facilitating accelerated commercialization and scale.

The competitive landscape comprises multinational players leveraging a blend of organic innovation and strategic acquisitions to consolidate leadership and explore emerging technological frontiers.

Europe Micro Battery Market Trends

Europe is slated to account for an estimated 29% share of the global market in 2025, with Germany, the U.K., France, and Spain as principal contributors. The region’s growth is propelled by harmonized regulatory measures under the EU Batteries Regulation, effective since 2023, which impose robust directives on the recyclability, material sourcing, and lifecycle management of batteries, catalyzing the transition toward rechargeable micro battery adoption.

European manufacturers benefit from strong governmental and EU-level innovation initiatives, including Horizon Europe programs, fostering collaboration across battery chemistry developments, recycling technologies, and circular economy integration.

The competitive market structure is characterized by medium-sized specialized firms and emerging tech startups complementing legacy players, with an emphasis on solid-state and thin-film innovation pathways. Investment trends increasingly focus on expanding manufacturing capacity and capability upgrades aligned with sustainability and regulatory compliance, positioning Europe as a pivotal strategic node in the global micro battery landscape.

Asia Pacific Micro Battery Market Trends

Asia Pacific is projected to be the fastest-growing and largest regional market for micro batteries, commanding approximately 37.5% of the market share on account of its manufacturing dominance and raw material access.

China, Japan, South Korea, and India serve as key markets, where governmental subsidies and policy incentives underpin rapid technology adoption and supply chain growth. The high CAGR is driven by favorable macroeconomic trends, extensive IoT deployment, smart city initiatives, and e-mobility adoption.

China leads production capacity with comprehensive battery materials access, while Japan and South Korea contribute technology leadership in chemistry and device miniaturization. India’s widening consumer base and manufacturing ecosystem present substantial incremental market opportunities.

Regulatory reforms enhancing battery sustainability and recycling complement industrial investments, stimulating strategic manufacturing relocations and R&D center expansions by global multinationals. Asia Pacific’s competitive landscape features a mix of dominant international manufacturers and agile local firms, with continued investments fostering deep vertical integration and innovation across formats and chemistries.

Competitive Landscape

The global micro battery market landscape demonstrates moderate consolidation, with approximately 64% of the market share is controlled by leading multinational corporations, including Panasonic Corporation, Sony Corporation, Samsung SDI Co. Ltd., Murata Manufacturing Co. Ltd., and Energizer Holdings.

These established companies leverage diversified product ranges encompassing primary and rechargeable chemistries, multiple form factors, and a wide application reach. Beyond these incumbents, the market is fragmented with numerous emerging specialized firms targeting niche segments such as flexible printed batteries and textile-integrated solutions, creating a vibrant innovation ecosystem.

Market concentration is moderate, balancing scale-driven competitive advantages with niche startups driving disruptive innovation. Competitive positioning largely hinges on proprietary battery chemistries, regulatory approvals, and manufacturing excellence, with many leaders pursuing vertical integration to control supply chains and reduce time-to-market.

While large players dominate capital-intensive segments, smaller firms focus on agile development cycles, flexible customization, and collaboration with device original equipment manufacturers (OEMs) to secure footholds in emerging use cases.

Key Industry Developments

- In November 2025, Ensurge and Corning formed a joint development agreement to create ultra-high-energy-density solid-state microbatteries using Corning’s Ribbon Ceramic technology. The partnership targets high-volume sectors, including consumer, medical, industrial, and defense, and accelerates advanced microbattery manufacturing and commercialization efforts.

- In August 2025, Ilika and Cirtec Medical began U.S. manufacturing of StereaX solid-state microbatteries at Cirtec’s Rochester facility. This strategic collaboration enhances supply chain security for medical implants by leveraging Ilika’s technology and Cirtec’s precision manufacturing, supporting rapid commercialization and regulatory compliance.

- In May 2025, ITEN and A*STAR Institute of Microelectronics integrated solid-state microbatteries using advanced packaging, enabling in-package energy storage. This innovation enhances energy efficiency, reduces device size, improves reliability, and offers eco-friendly, hazardous-material-free batteries for longer device life and less electronic waste.

Companies Covered in Micro Battery Market

- Panasonic Corporation

- Sony Corporation

- Samsung SDI Co. Ltd.

- Murata Manufacturing Co. Ltd.

- Energizer Holdings

- VARTA AG

- Tadiran Batteries

- Renata SA

- Dynapower North America, Inc.

- Cochlear Limited

- Freudenberg Group (Freudenberg Battery & Energy Technology)

- Hitachi Chemical Company Ltd.

- Blue Spark Technologies

- MicroBattery Inc.

- Global Battery Solutions

Frequently Asked Questions

The global micro battery market is projected to reach US$855.0 Million in 2025.

Evolving applications in medical devices, consumer electronics, the rapid growth of the IoT sector, and regulatory shifts favoring rechargeable battery technologies are driving the market.

The micro battery market is poised to witness a CAGR of 16.4% from 2025 to 2032.

Advancing flexible and thin-film battery technologies and the increasing miniaturization of smart electronics are key market opportunities.

Panasonic Corporation, Sony Corporation, Samsung SDI Co. Ltd., and Murata Manufacturing Co. Ltd. are the key market players.