- Energy Storage Solutions

- Li-ion Pouch Battery Market

Li-ion Pouch Battery Market Trends, :Size, Share, and Growth Forecast 2025 - 2032

Li-ion Pouch Battery Market by Capacity (1 - 3Ah, 5 - 10Ah, 10 - 15Ah, 16 - 30Ah, 40 - 50Ah, 50 - 100Ah), by Rated Voltage (6V, 12V, 24V, 48V, 60 - 72V, 96V), Chemistry (Lithium Cobalt Oxide, Lithium Manganese Oxide, Lithium Nickel Manganese Cobalt Oxide, Lithium Iron Phosphate, Lithium Titanate), by End-user (Electric Vehicles, Cell Phones, Battery Powered Off-Road Vehicles, Robotics, Energy Storage Systems) Regional Analysis, 2025 - 2032

Li-ion Pouch Battery Market Size and Trend Analysis

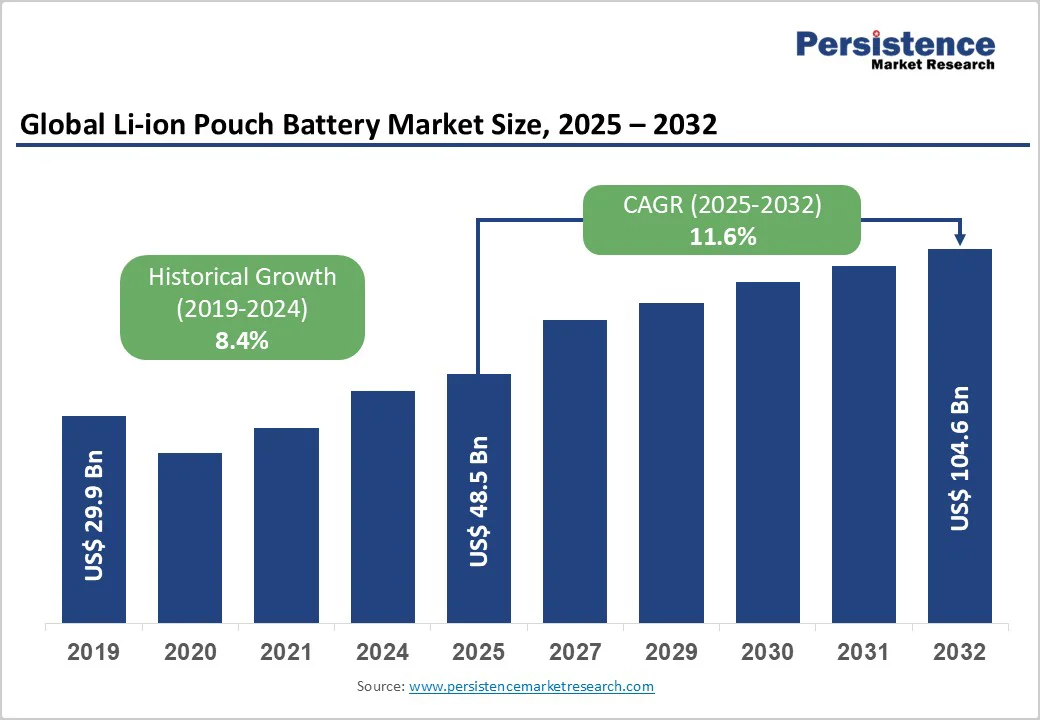

The global li-ion pouch battery market size was valued at US$ 48.5 billion in 2025 and is projected to reach US$ 104.6 billion by 2032, growing at a CAGR of 11.6% between 2025 and 2032.

This remarkable growth trajectory is driven by the accelerating adoption of electric vehicles, increasing demand for lightweight and flexible battery solutions, and the rapid expansion of energy storage applications across various industries.

The market’s expansion is further supported by technological advancements in battery chemistry, manufacturing efficiencies, and government initiatives promoting clean energy technologies worldwide.

Key Market Highlights:

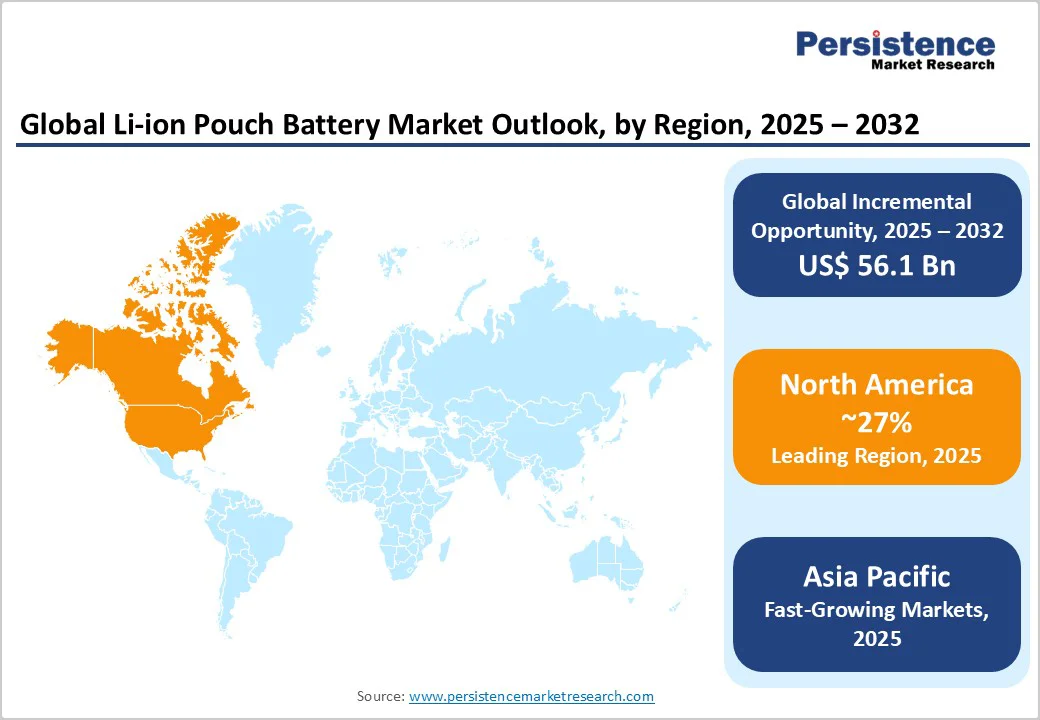

- Leading Region: North America leads the Li-ion pouch battery market with 27% share, supported by substantial government investments exceeding US$3 billion in domestic battery manufacturing and recycling infrastructure.

- Emerging Region: Asia Pacific emerges as fastest-growing region with a 13.5% CAGR through 2032, driven by massive investments in EV manufacturing and breakthrough technologies from CATL, BYD, and Toshiba.

- Dominant Segment: 50-10Ah capacity segment dominates with 38% market share due to optimal balance for electric vehicle and energy storage applications requiring high-capacity, lightweight solutions.

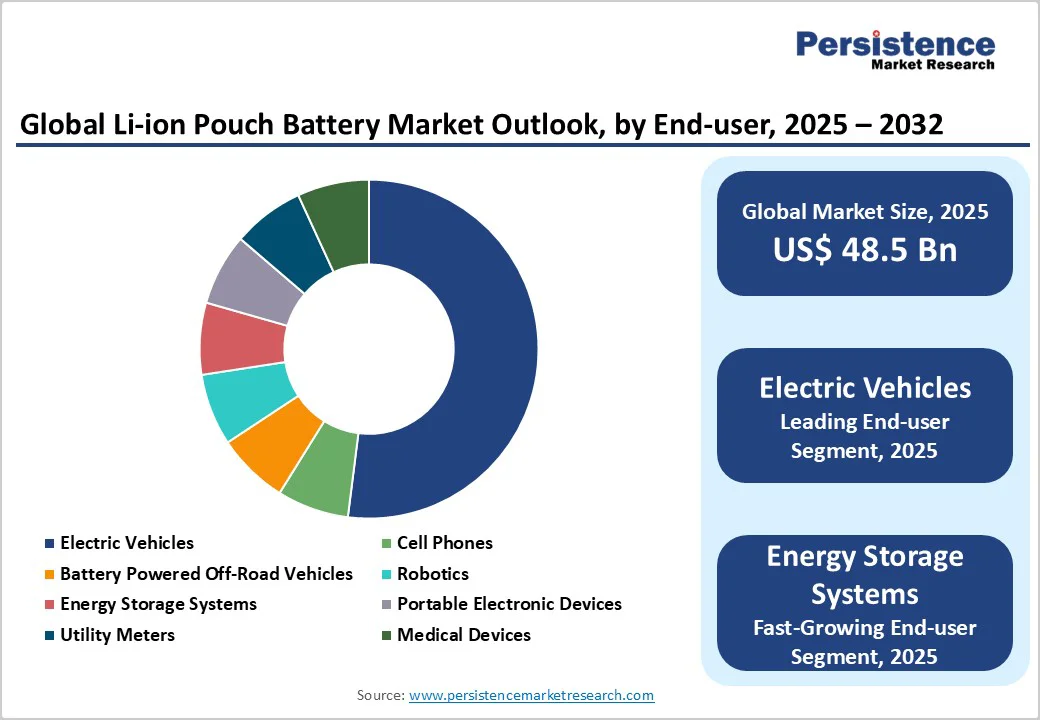

- Fastest Growing Segment: Electric Vehicles represent the largest end-user segment with 52% share, reflecting the automotive industry’s rapid electrification and superior performance characteristics of pouch battery technology.

- Key Opportunity: Anode-free battery technology creates significant growth opportunities with potential 25% capacity improvements, demonstrating industry commitment to next-generation energy storage solutions.

| Key Insights | Details |

|---|---|

| Li-ion Pouch Battery Market Size (2025E) | US$ 48.5 bn |

| Market Value Forecast (2032F) | US$ 104.6 bn |

| Projected Growth CAGR (2025 - 2032) | 11.6% |

| Historical Market Growth (2019-2024) | 8.4% |

Market Dynamics

Driver - Rising Electric Vehicle Adoption and Automotive Electrification

The Li-ion Pouch Battery Market is experiencing unprecedented growth driven by the global shift toward adopting electric vehicles and automotive electrification initiatives. According to the U.S. Department of Energy, lithium-ion batteries have become the preferred energy storage solution for electric vehicles due to their high energy density, longer cycle life, and superior performance characteristics.

Electric Vehicle Market is expected to grow at 14.6% CAGR between 2025 and 2032, reaching US$ 1.9 trillion further driving demand for advanced pouch battery technologies. Government policies across major economies, including China’s target for BEVs to constitute over 50% of new personal vehicle purchases by 2025 and the European Union’s commitment to achieve net-zero emissions by 2050, are creating substantial market opportunities.

Expanding Energy Storage Systems and Grid Integration Applications

The growing deployment of renewable energy sources and smart grid infrastructure is significantly driving demand for Li-ion pouch batteries in energy storage applications. Energy Storage Systems require flexible, high-capacity battery solutions that can efficiently store and discharge energy, making pouch batteries ideal for utility-scale and residential applications. The U.S. Department of Energy has awarded US$125 million in funding for research to enable next-generation batteries and energy storage technologies, emphasizing the strategic importance of advanced battery solutions.

Lithium Iron Phosphate Batteries Market growth is particularly driven by stationary energy storage applications, where LiFePO4 pouch cells offer superior safety, long cycle life exceeding 2000 cycles, and stable performance across wide temperature ranges. The European Battery Regulation (2023/1542) promotes sustainable battery manufacturing and end-of-life management, creating favorable conditions for high-performance pouch battery adoption in grid storage and renewable energy integration projects.

Restraint - High Manufacturing Costs and Raw Material Price Volatility

The Li-ion pouch battery market faces significant challenges from high manufacturing costs and volatile raw material prices, particularly for critical materials like lithium, cobalt, and nickel. Toshiba Corporation has addressed these concerns by developing cobalt-free 5V-class high-potential cathode materials, but the industry still struggles with cost optimization for mass production.

Portable Battery Pack Market applications often require cost-effective solutions, creating pressure on manufacturers to balance performance with affordability. Supply chain disruptions and geopolitical factors affecting raw material availability further compound cost challenges, making it difficult for manufacturers to maintain competitive pricing while investing in advanced manufacturing technologies.

Technical Limitations and Safety Concerns

Despite technological advances, Li-ion pouch batteries face inherent limitations including thermal management challenges, potential swelling issues, and safety concerns related to thermal runaway risks. The flexible packaging of pouch batteries, while offering design advantages, requires sophisticated Battery Management Systems and protective housing to ensure safe operation.

Europe Lithium-Ion Battery Market regulations increasingly emphasize safety standards and testing requirements, adding complexity to product development and certification processes. Manufacturing consistency and quality control remain challenging due to the complex multi-layer construction of pouch cells, requiring significant investments in precision manufacturing equipment and quality assurance systems.

Market Opportunities

Emerging Applications in Medical Devices and Portable Electronics

The Medical Measurements and Portable Devices segment presents significant growth opportunities for Li-ion pouch batteries due to increasing demand for lightweight, flexible power solutions in healthcare applications. Advanced medical devices require batteries with custom form factors, high energy density, and reliable performance in critical applications.

Portable Electronic Devices market expansion, driven by IoT devices, wearable technology, and mobile computing, creates substantial demand for thin, lightweight pouch batteries that can be integrated into compact designs. Utility Meters and smart grid applications benefit from pouch batteries’ ability to provide long-term, maintenance-free operation in challenging environmental conditions.

The growing emphasis on remote healthcare monitoring and telemedicine is driving innovation in battery-powered medical devices, creating opportunities for specialized pouch battery solutions with enhanced safety and reliability features.

Category-wise Analysis

Capacity Insights

The 50 - 10Ah capacity segment holds approximately 38% share in 2025, driven by strong demand from electric vehicle and energy storage applications requiring high-capacity solutions. This capacity range represents the optimal balance between energy density and practical application requirements for modern Electric Vehicles, where manufacturers require substantial energy storage in compact, lightweight packages.

CATL’s M1C24A 3.2V 100Ah LiFePO4 Pouch Cell exemplifies this trend, offering 320Wh rated energy with 6000 cycle life at 80% SOH, making it ideal for both automotive and stationary storage applications. Battery-powered off-road vehicles and industrial applications increasingly adopt high-capacity pouch batteries for their superior energy-to-weight ratios and design flexibility compared to traditional cylindrical or prismatic alternatives.

Rated Voltage Analysis

48V rated voltage systems dominate the Li-ion pouch battery market with approximately 42% market share in 2025, reflecting the widespread adoption of 48V architectures in electric vehicles and energy storage systems. This voltage level has become the industry standard for mild-hybrid vehicles, e-bikes, and distributed energy storage applications due to an optimal balance between performance and safety considerations.

SK Innovation produces 3.7V pouch cells that are commonly configured in 48V systems through series connections, enabling manufacturers to achieve desired voltage levels while maintaining modular design flexibility. Energy Storage Systems particularly benefit from 48V configurations as they enable easier integration with existing electrical infrastructure while providing sufficient power for residential and commercial applications without requiring specialized high-voltage handling procedures.

Chemistry Analysis

Lithium Iron Phosphate (LiFePO4) chemistry leads the Li-ion pouch battery market with approximately 26% market share in 2025, driven by superior safety characteristics, long cycle life, and cost-effectiveness for large-scale applications. LiFePO4 pouch cells offer exceptional thermal stability, with operating temperatures ranging from -20°C to 60°C and charge temperatures from 0°C to 45°C, making them ideal for demanding applications including electric vehicles and grid storage.

The Lithium Iron Phosphate Batteries Market benefits from reduced reliance on scarce materials like cobalt and nickel, addressing supply chain concerns and enabling more sustainable production. Toshiba Corporation’s development of cobalt-free cathode materials further supports the industry’s transition toward safer, more sustainable battery chemistries that maintain high performance while reducing environmental impact and material costs.

End-user Analysis

Electric Vehicles represent the largest end-user segment with approximately 52% market share in 2025, reflecting the automotive industry’s rapid transition toward electrification and the superior performance characteristics of pouch batteries in automotive applications. Pouch batteries offer critical advantages for EV applications, including weight reduction, design flexibility, and efficient thermal management that directly translate to improved vehicle range and performance.

Panasonic supplies advanced pouch batteries to Tesla and other major automakers, with plans to achieve 25% capacity improvements through anode-free technology by 2027. The segment benefits from government incentives and regulatory requirements promoting electric vehicle adoption, with the Asia Pacific leading global EV production and battery demand.

Cell Phones and portable electronics represent the second-largest segment, where thin profile and lightweight characteristics of pouch batteries enable innovative device designs and extended battery life, supporting the continuous evolution of mobile technology and consumer electronics markets.

Regional Insights

North America Li-ion Pouch Battery Market Trends

North America holds 27% share in 2025, driven by substantial government investments in battery manufacturing and electric vehicle adoption initiatives. The U.S. Department of Energy has allocated over US$3 billion in grants for 25 projects to boost domestic battery production and recycling capabilities, including significant funding for American Battery Technology Co. and Cirba Solutions for advanced recycling facilities.

The Bipartisan Infrastructure Law provides US$600 million annually through 2026 for battery materials processing, supporting domestic supply chain development, and reducing dependency on foreign suppliers.

Innovation ecosystem strength is demonstrated through partnerships between national laboratories and private companies, with Argonne National Laboratory leading the Energy Storage Research Alliance (ESRA) focused on next-generation battery technologies. The region benefits from stringent safety standards and regulatory frameworks that promote high-quality battery manufacturing while supporting technology commercialization through tax incentives and research funding programs.

Europe Li-ion Pouch Battery Market Trends

Europe demonstrates a strong commitment to sustainable battery manufacturing through the comprehensive European Battery Regulation (2023/1542), which entered force in February 2024 and establishes harmonized legislation for battery sustainability and safety.

The regulation requires CE marking for all batteries from August 2024, mandates carbon footprint declarations, and sets ambitious recycling targets with minimum recovery rates for valuable materials, including copper, cobalt, lithium, and nickel. Germany, the United Kingdom, France, and Spain lead regional adoption through stringent building codes and renewable energy mandates that drive demand for advanced energy storage solutions.

European Green Deal initiative allocates €1.8 trillion in funding to advance EV-based lithium-ion battery technologies, emphasizing research innovation and sustainable material extraction practices. Battery passport requirements starting in 2027 for electric vehicle batteries will enhance traceability and support circular economy objectives, creating competitive advantages for manufacturers investing in sustainable production technologies and comprehensive lifecycle management systems.

Asia Pacific Li-ion Pouch Battery Market Trends

Asia Pacific emerges as the fastest-growing region with a 13.5% CAGR expected through 2032, reaching 2,569 GWh capacity driven by massive investments in electric vehicle manufacturing and battery production infrastructure.

China leads with CATL investing US$6 billion in Indonesia and developing breakthrough technologies including Shenxing Plus LFP battery capable of 1,000 km range, setting new industry benchmarks for performance and efficiency. BYD announced plans to launch next-generation Blade battery in 2025, following widespread adoption by OEMs including Hyundai, Kia, and Toyota.

Japan maintains technological leadership through Toshiba Corporation’s advanced NTO battery development, achieving energy density comparable to LiFePO4 with 10 times longer cycle life, demonstrating the region’s commitment to innovation. South Korea’s SK Innovation expands production capabilities while LG Energy Solution established a US$1.5 billion joint venture with JSW Energy in December 2024.

India presents significant growth opportunities through the National Programme on Advanced Chemistry Cell Battery Storage supporting 50 GWh domestic production capacity, with production-linked subsidies ranging from US$27/kWh to US$56/kWh for manufacturers establishing minimum 5 GWh production facilities.

Competitive Landscape

The Li-ion pouch battery market demonstrates a moderately consolidated structure with several key players maintaining strong positions through technological innovation, manufacturing scale, and strategic partnerships with major automotive and electronics companies.

Leading companies including Panasonic Industrial Corporation, Toshiba Corporation, SK Innovation Co. Ltd., and A123 Systems LLC, compete through advanced battery chemistry development, production capacity expansion, and vertical integration strategies.

The industry exhibits significant barriers to entry due to substantial Research and Development investments required for battery technology advancement, complex manufacturing processes, and extensive certification requirements for automotive and safety-critical applications.

Companies focus on developing next-generation technologies, including anode-free batteries, solid-state electrolytes, and cobalt-free cathode materials, while investing in automated manufacturing capabilities to achieve cost competitiveness and quality consistency across global production facilities.

Key Market Developments

- September 2025: Panasonic announced breakthrough anode-free battery technology development, targeting 25% capacity improvement and commercialization by 2027, potentially extending Tesla Model Y driving range by 145 kilometers without increasing battery pack size.

- November 2024: Toshiba Corporation developed an advanced NTO (Niobium Titanium Oxide) lithium-ion battery, achieving energy density comparable to LiFePO4 with over 10 times cycle life, targeting commercial vehicle applications with super-rapid charging capabilities.

- December 2024: SK Innovation expanded pouch battery manufacturing discussions with multiple OEMs for prismatic battery production, diversifying product portfolio beyond current pouch-type offerings while maintaining leadership in flexible battery solutions.

Companies Covered in Li-ion Pouch Battery Market

- Panasonic Industrial Corporation

- Toshiba Corporation

- Gee Power

- FDK Corporation

- SK Innovation Co. Ltd.

- Bestgo B Vertical Partners West LLC

- EPEC LLC

- Enertech International Inc

- A123 Systems LLC

- FluxPower Battery Co. Ltd.

- SOLAREDGE e-MOBILITY SpA

- CUSTOM CELLS ITZEHOE GMBH

- Fruedenberg Group

- Leclanché SA

- Echion Technologies

- YOK Energy

- Servovision Co. Ltd.

- DNK Power Company Limited

- Amperex Technology Limited

- Shenzhen Ace Battery Co. Ltd.

- Energy Innovation Group Ltd.

- EVE Energy Co. Ltd.

Frequently Asked Questions

The global Li-ion pouch battery market was valued at US$ 48.5 billion in 2025 and is projected to reach US$ 104.6 billion by 2032, growing at a CAGR of 11.6% during the forecast period.

The market is primarily driven by rising electric vehicle adoption with EV market growing at 14.6% CAGR, expanding energy storage applications, and government investments.

50-10Ah capacity segment dominates with approximately 38% market share in 2025, driven by optimal balance for electric vehicle and energy storage applications requiring high-capacity, lightweight solutions.

North America leads the Li-ion pouch battery market with 27% market share in 2025, supported by substantial government investments and established manufacturing infrastructure for battery production and recycling.

Key opportunities include Asia Pacific region expansion with 14.0% CAGR growth, anode-free battery technology with 25% capacity improvements, and emerging applications in medical devices and portable electronics.

Leading market players include Panasonic Industrial Corporation, Toshiba Corporation, SK Innovation Co. Ltd., A123 Systems LLC, CATL, BYD Company Limited, and LG Energy Solution, who maintain strong positions through technological innovation and strategic partnerships.