- Processed Food

- Nut Butter Bar Market

Nut Butter Bar Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Nut Butter Bar Market by Product Type (Peanut Butter Bars, Almond Butter Bars, Cashew Butter Bars, Hazelnut Butter Bars, and Others), by Application (Sports Nutrition, Meal Replacement, On-the-Go Snacking, and Others) by Distribution Channel (Hypermarkets, Convenience Stores, Specialty Health Stores, Pharmacies, E-commerce Platforms, and Others), and Regional Analysis from 2026 to 2033

Nut Butter Bar Market Share and Trend Analysis

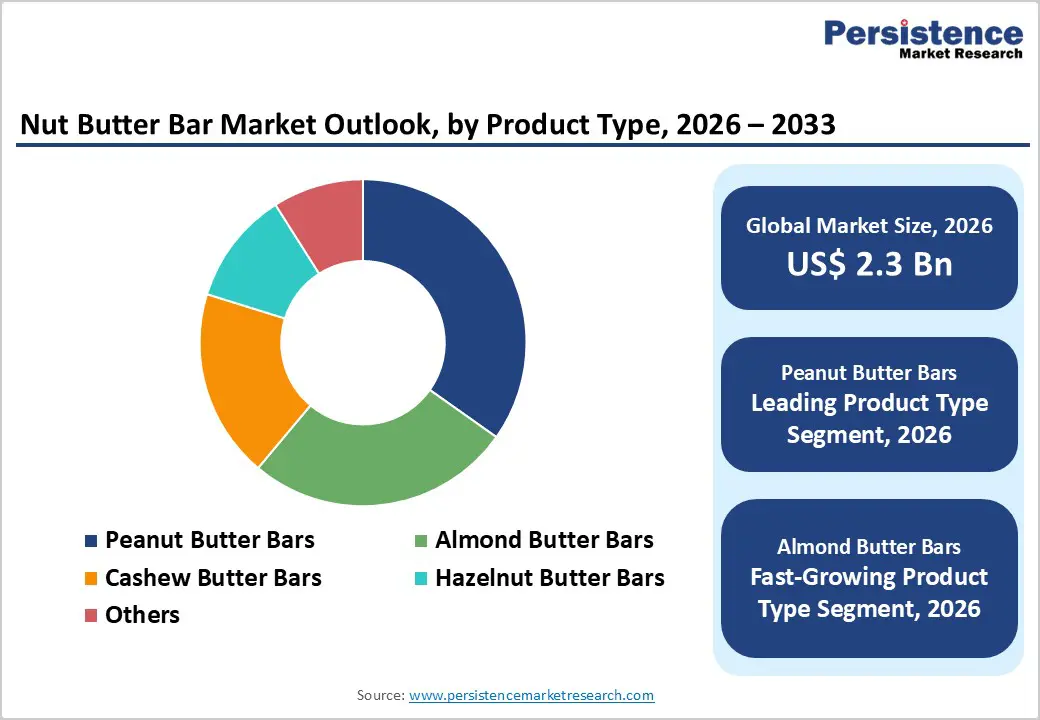

The global nut butter bar market size is estimated to grow from US$ 2.3 Bn in 2026 to US$ 3.8 Bn by 2033. The market is projected to record a CAGR of 5.8% during the forecast period from 2026 to 2033. Global consumption of nut butter bars is expanding consistently as consumers increasingly shift toward nutritious, convenient snack formats that combine protein, healthy fats, and natural ingredients.

Growing interest in balanced diets, active lifestyles, and preventive wellness has accelerated demand for snacks that deliver sustained energy while supporting weight management and overall nutrition goals. Nut butter bars are gaining strong acceptance across retail shelves, fitness channels, and online platforms due to their clean-label positioning, plant-based appeal, and compatibility with gluten-free and high-protein dietary preferences. Rising awareness around ingredient transparency and reduced sugar intake is encouraging manufacturers to introduce minimally processed formulations using recognizable components.

The category is also benefiting from increasing adoption among working professionals, athletes, and younger consumers seeking portable meal alternatives. Expansion of organized retail networks and rapid growth of digital commerce are improving accessibility across both developed and emerging economies. Continuous innovation in flavor profiles, functional enrichment, texture enhancement, and sustainable packaging is strengthening product differentiation. Additionally, the growing popularity of vegan and flexitarian eating patterns, combined with premium snack innovation and private-label expansion, continues to reinforce long-term global demand momentum.

Key Industry Highlights:

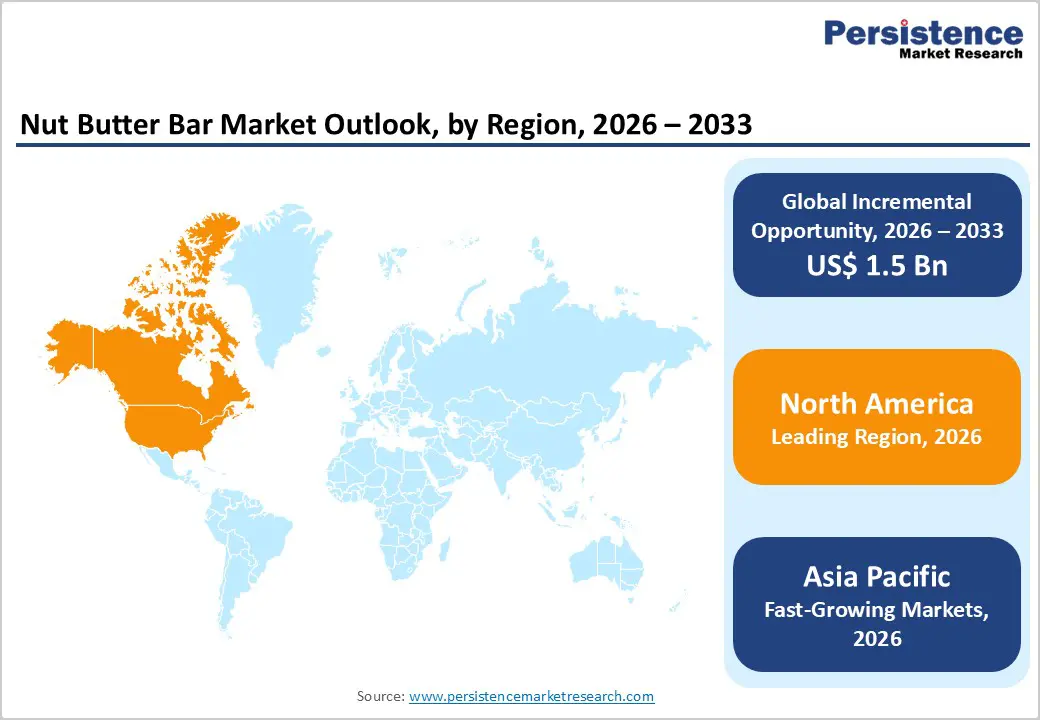

- Leading Region: North America accounts for 46.7% of global revenue, supported by strong awareness of functional nutrition, a mature sports nutrition culture, advanced retail infrastructure, and widespread availability of premium snack brands.

- Fastest-Growing Region: Asia Pacific is witnessing the most rapid expansion, driven by urban lifestyle changes, rising disposable incomes, growing fitness awareness, and expanding modern retail and e-commerce penetration.

- Leading Product Type Segment: Peanut butter bars lead the market due to affordability, extensive raw material availability, scalable manufacturing, and strong acceptance across mainstream consumers.

- Fastest-Growing Product Type Segment: Almond butter bars are gaining traction rapidly as demand rises for premium, clean-label, and sustainably sourced snack options among health-focused buyers.

- Leading Application Segment: On-the-go snacking dominates consumption, supported by convenience, portability, and increasing replacement of traditional packaged snacks with functional alternatives.

- b: Sports nutrition is expanding quickly as consumers increasingly seek protein-dense snacks suited for performance, recovery, and active lifestyle needs.

| Key Inbsight | Key Insights |

|---|---|

| Nut Butter Bar Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Dynamics

Driver - Increasing Preference for Protein-Rich, Clean-Label, and Convenient Functional Snacks

A major force accelerating category expansion is the global shift toward healthier snacking habits supported by rising awareness of nutrition, fitness, and preventive wellness. Consumers increasingly seek foods that combine convenience with balanced macronutrients, encouraging strong demand for nut butter bars containing natural fats, plant proteins, and minimal additives. These products align well with clean-label expectations, as shoppers prefer recognizable ingredients, reduced sugar formulations, and minimally processed snacks over traditional confectionery options. Growing participation in active lifestyles, gym culture, and outdoor recreation has further strengthened demand for portable energy solutions that support sustained satiety and performance.

Nut-based formulations are perceived as nutritionally dense, delivering protein, fiber, and healthy fats in compact formats suitable for daily consumption. Additionally, expanding vegan and flexitarian populations are driving the adoption of plant-derived snack alternatives that replace dairy-heavy protein products. Manufacturers are capitalizing on these trends through functional claims such as keto-friendly, gluten-free, and high-protein positioning. Rapid urbanization, increasing disposable income levels, and broader availability across organized retail and digital platforms continue to enhance accessibility, reinforcing sustained demand momentum worldwide.

Restraints - Raw Material Cost Fluctuations, Allergen Sensitivities, and Competitive Snack Alternatives

Nut butter bars rely heavily on almonds, peanuts, cashews, and hazelnuts, commodities that are vulnerable to climate variability, agricultural yield fluctuations, and global trade disruptions. Price volatility directly impacts manufacturing margins and retail pricing, particularly for premium nut varieties. Additionally, nuts are classified among common food allergens, restricting adoption among certain consumer groups and requiring strict labeling compliance, which increases regulatory and production complexity.

Shelf-life management also presents challenges, as natural formulations without artificial preservatives demand advanced packaging solutions to maintain freshness and texture stability. In many developing markets, higher product pricing compared to conventional snack foods may discourage mass adoption among cost-sensitive consumers. Competition from protein cookies, granola bars, and ready-to-drink nutritional beverages further intensifies market pressure, forcing brands to continuously differentiate through innovation. Limited awareness regarding nutritional advantages in some regions and inconsistent distribution penetration can also slow category development, particularly outside urban retail ecosystems.

Opportunity - Premium Product Innovation, Digital Retail Expansion, and Penetration into Emerging Consumer Segments

Significant growth potential is emerging through product diversification and evolving consumer expectations surrounding personalized nutrition. Brands are increasingly developing differentiated offerings featuring functional ingredients such as adaptogens, probiotics, collagen alternatives, and added micronutrients to enhance value perception. Premiumization trends encourage innovation using exotic nut blends, low-glycemic sweeteners, and indulgent yet health-focused flavor combinations that appeal to both wellness and lifestyle consumers. Expansion of e-commerce ecosystems and subscription-based snack models is creating scalable distribution pathways, enabling direct engagement with niche audiences and improving brand loyalty.

Emerging economies present attractive opportunities as rising middle-class populations adopt Western-style snacking behaviors alongside growing fitness awareness. Localized flavor development tailored to regional taste preferences further supports penetration. Sustainability initiatives, including ethically sourced nuts and eco-conscious packaging, are strengthening brand differentiation among environmentally aware consumers. Strategic collaborations between nutrition brands, fitness platforms, and retail chains are accelerating product visibility. As consumers increasingly replace traditional snacks with functional alternatives, innovation-led positioning is expected to unlock both volume growth and premium revenue opportunities.

Category-wise Analysis

By Product Type Insights

Peanut butter bars are projected to hold the largest share of the global nut butter bar market in 2026, accounting for 34.8% of total revenue. Their dominance is largely supported by lower raw material costs, wide global peanut availability, and well-established processing infrastructure that enables high-volume production. Manufacturers favor peanut-based formulations due to consistent texture, stable flavor profiles, and compatibility with protein enrichment and clean-label positioning. These bars appeal to both mainstream and fitness-oriented consumers, making them suitable for large retail distribution as well as private-label expansion. Compared with premium nut variants, peanut butter formats allow competitive pricing while maintaining nutritional value, including protein and healthy fats. Continuous innovation in flavor combinations, reduced sugar formulations, and fortified variants further strengthens adoption. Strong penetration across supermarkets, convenience outlets, and online channels reinforces the segment’s sustained commercial leadership worldwide.

By Application Insights

The on-the-go snacking segment is expected to lead the global nut butter bar market in 2026, capturing a 41.6% revenue share. Increasing urbanization, busy work schedules, and rising demand for portable nutrition solutions are major factors driving consumption. Nut butter bars are widely perceived as convenient energy sources offering balanced macronutrients, making them suitable for daily snacking occasions rather than niche sports use alone. Consumers increasingly replace traditional packaged snacks with protein-rich alternatives that provide satiety and sustained energy. Manufacturers are responding by launching compact formats, indulgent yet healthy flavor options, and portion-controlled variants targeting office workers, students, and travelers. The category also benefits from clean-label positioning and plant-based ingredient trends, which enhance consumer trust. Growth in impulse purchases across modern retail stores and digital platforms further accelerates adoption, ensuring that on-the-go consumption remains the dominant application segment globally.

By Distribution Channel Insights

Hypermarkets are projected to dominate distribution in the global nut butter bar market in 2026, accounting for a 38.7% revenue share. Large retail formats provide extensive shelf space, enabling brands to showcase diverse flavors, nutritional claims, and promotional offerings that influence purchase decisions. Consumers prefer hypermarkets for bundled purchases and product comparisons, particularly within health snack categories. Retailers also prioritize nutrition bars within wellness aisles, improving accessibility among mainstream shoppers. Established supply agreements between manufacturers and large retail chains support consistent product availability and volume sales. In-store sampling campaigns, discount strategies, and cross-merchandising alongside fitness and breakfast products further strengthen demand. While online channels continue expanding, hypermarkets remain critical for brand discovery and impulse buying. Their ability to serve both premium and value-oriented consumers ensures continued dominance within the distribution landscape.

Region-wise Insights

North America Nut Butter Bar Market Trends

North America is anticipated to dominate the global nut butter bar market in 2026, representing a 46.7% value share, with the United States serving as the primary revenue contributor. Strong consumer awareness surrounding protein intake, weight management, and functional snacking has accelerated demand for nutrient-dense bar formats across the region. Consumers increasingly prioritize clean-label, non-GMO, and plant-based products, positioning nut butter bars as convenient alternatives to traditional confectionery snacks. The region benefits from a mature sports nutrition ecosystem, widespread gym culture, and established retail infrastructure supporting rapid product commercialization.

Major brands continuously introduce high-protein, keto-friendly, and low-sugar variants to meet evolving dietary preferences. Additionally, advanced supply chains and efficient cold storage logistics enable nationwide distribution efficiency. E-commerce penetration and subscription snack models further strengthen recurring purchases. Private-label expansion by large retailers and innovation in premium nut blends continue to diversify offerings. Continuous marketing investments, influencer-driven promotions, and strong consumer willingness to pay for functional foods collectively reinforce North America’s sustained leadership position.

Europe Nut Butter Bar Market Trends

Europe’s nut butter bar market is expected to experience stable expansion in 2026, supported by increasing demand for natural, ethically sourced, and nutritionally balanced snack options. Countries such as Germany, the United Kingdom, France, Italy, Spain, and the Netherlands remain key consumption centers due to well-developed health food industries and strict regulatory standards governing ingredient transparency. European consumers demonstrate a strong preference for organic certification, sustainable sourcing practices, and environmentally responsible packaging, encouraging brands to adopt traceable supply chains. Growth in vegan and flexitarian dietary patterns further supports plant-based snack adoption, particularly almond and cashew-based formulations.

Specialty health retailers and organic supermarket chains play an important role in influencing purchasing behavior, while online grocery platforms continue gaining traction among urban consumers. Product innovation increasingly focuses on reduced sugar content, allergen-friendly recipes, and functional benefits such as sustained energy release. Collaborative partnerships between regional food manufacturers and premium snack brands also enhance market penetration, supporting long-term growth across diverse European markets.

Asia Pacific Nut Butter Bar Market Trends

The Asia Pacific nut butter bar market is projected to register the fastest growth, expanding at a CAGR of around 7.9% between 2026 and 2033, driven by rapid urbanization, rising disposable incomes, and shifting dietary habits toward healthier snacking options. Growing middle-class populations in China, India, Japan, South Korea, and Australia are increasingly adopting convenient, protein-rich foods aligned with active lifestyles. Expanding fitness awareness and exposure to Western dietary trends are accelerating the acceptance of nutrition bars among younger consumers. The region also benefits from improving retail infrastructure, including modern supermarkets and rapidly scaling online grocery ecosystems that enhance accessibility. Local manufacturers are introducing affordable variants tailored to regional taste preferences, supporting broader market penetration.

Government initiatives promoting food processing and value-added agriculture further encourage domestic production capabilities. Additionally, multinational brands are investing in localized manufacturing and partnerships to strengthen supply networks. Increasing demand across office snacking, school nutrition, and wellness-focused consumption positions the Asia Pacific as the key growth engine for the global nut butter bar market.

Competitive Landscape

The global nut butter bar market is highly competitive, with strong participation from Lerel Health Foods LLP., Petrow Food Group., Mother Nature, Mondelez International Group, and Big Spoon Roasters. These players leverage diversified nut sourcing networks, advanced processing capabilities, strong partnerships with retailers and fitness channels, and continuous innovation in plant-based, high-protein, and clean-label formulations to address growing demand across snack, sports nutrition, and meal replacement applications.

Rising health awareness, increasing preference for convenient functional snacks, and expanding vegan consumption are driving innovation, while manufacturers focus on premium ingredients, sustainable sourcing, flavor diversification, private-label expansion, and e-commerce growth to strengthen global market presence.

Key Industry Developments:

- In October 2025, Hormel Foods Corporation and Forward Consumer Partners announced a strategic partnership under which the Justin’s® brand, including its nut butter and organic chocolate product portfolio, will operate as a standalone company, with Forward holding a 51% stake and Hormel retaining 49%.

- In July 2025, Pip & Nut, a U.K.-based nut snack and nut butter brand, introduced its Almond Butter Stuffed Oat Bar, marking its entry into almond butter-filled snack formats and expanding beyond its established range of peanut butter-stuffed oat bars to meet growing demand for plant-based snack alternatives.

- In June 2025, RXBAR introduced its High Protein bar and Nut Butter & Oat Lemon Honey Cashew Butter variant, featuring 18g of protein and made with six simple ingredients, offering a gluten-free, plant-based snack designed to deliver clean nutrition, improved taste, and functional performance without artificial additives.

- In April 2025, Justin’s expanded its nut-based snack portfolio by launching JUSTIN’S® Peanut Caramel Nougat Chocolate Candy Bars, reinforcing its presence in the nut butter bar category through indulgent yet clean-label formulations made with simple, responsibly sourced ingredients, targeting consumers seeking premium functional snack options with balanced taste and nutrition.

Companies Covered in Nut Butter Bar Market

- Lerel Health Foods LLP.

- Petrow Food Group.

- Mother Nature

- Mondelez International group.

- Big Spoon Roasters

- Mars

- Alpino Health Foods

- American Dream Nut Butter

- Hewyn

- Pip & Nut

- Justin's, LLC

- Rainbow Nut Butter

- THE HERSHEY COMPANY

- YouBar

- Perfect Snacks

- leclosdesprinces.com.

- Mirchi E-Commerce Private Limited

- bettrfood

- ROYAL NUT COMPANY

- Others

Frequently Asked Questions

The global Nut Butter Bar Market is projected to be valued at US$ 2.3 Bn in 2026.

Rising demand for convenient, high-protein, clean-label snacks driven by health consciousness, active lifestyles, and increasing adoption of plant-based nutrition.

The global Nut Butter Bar Market is poised to witness a CAGR of 5.8%between 2026 and 2033.

Product innovation in functional formulations, premium nut variants, and rapid expansion of e-commerce and emerging health-focused consumer markets.

Lerel Health Foods LLP., Petrow Food Group., Mother Nature, Mondelez International group, and Big Spoon Roasters are some of the key players in the green banana flour market.